Buysider; An entire winter of denominations snows down from the sky, hundreds of thousands, millions, but every flake, every thousand melts in your hand.

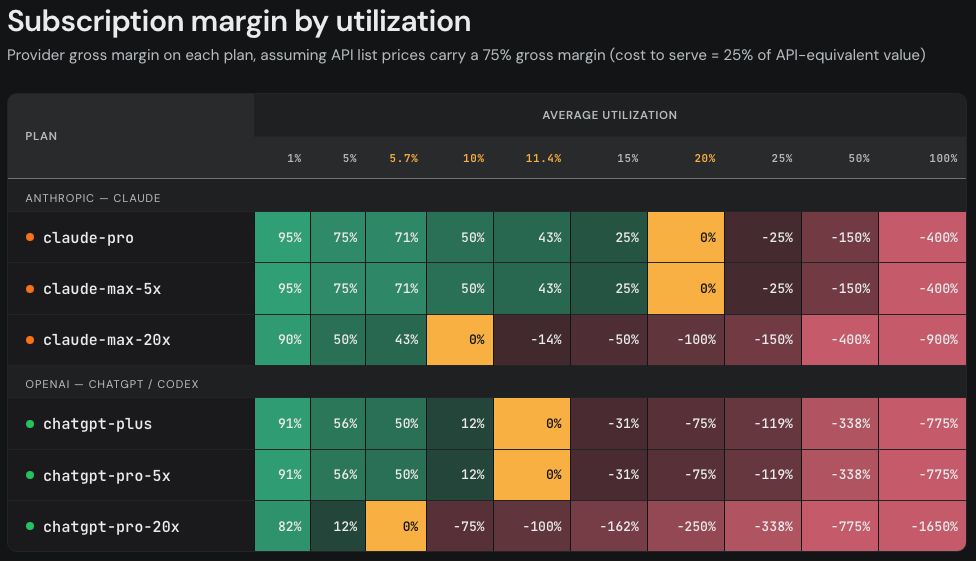

The margin on a subscription plan is a function of the average utilization. If we assume both companies have 75% API gross margins, this results in the following subscription margins. (3/4)

Unternehmer lachen empört über Bärbel Bas!

„Wir brauchen eine gerechte Verteilung“, sagt die SPD-Frau beim Tag des Familienunternehmens. Und betont weiter: „Natürlich wollen wir eine andere Verteilung.“

https://t.co/CzVMlXCF1x

What's happening today in AI infrastructure looks very similar to the 1998-1999 fiber optics overbuilding.

People said internet demand would be huge and insatiable. They were right. Demand was huge and insatiable.

But guess what? Most of those companies either went bankrupt or nearly did. When everybody invests at once, you get overcapacity.

Bloomberg: "Things change fast in AI. One minute corporate desk jockeys are competing to use AI coding and reasoning tools as much as possible, the next their bosses are complaining about budgets being pulverized and start rationing usage. Now OpenAI CEO Sam Altman concedes that costs have become a “huge issue” for customers and he’s reportedly considering “drastically” cutting prices to rein in rival Anthropic PBC’s lead in the corporate market...This prospect of a price war is deeply uncomfortable for “hyperscaling” tech giants such as Amazon and Microsoft who’ve been spending wildly on AI infrastructure so they can sell computing capacity to the big AI firms. The cost of components going into these data centers keeps rising, so any threat to OpenAI and Anthropic profits (and thereby their own ability to keep spending) is troubling."

In my December report on "GenAI & Productivity" (https://t.co/kEx5Z4BJH7), I warned the market was underestimating what a lack of pricing power could mean for hyperscalers. To quote the report:

"LM Arena is one of the most closely watched leaderboards of model performance. Its results are telling. As of writing this, the score gap between the top-ranked model—Google’s Gemini 3-pro—and the model of the 9th-ranked company (the 23rd-ranked model overall)—Deepseek’s V3.2—is just 4.5 percentage points. That may be a material capability gap today. However, it’s also testament to how fragile LLM leadership is moving forward.

While there’s a lot of speculative fear about how a single LLM could rise to dominance and what that could mean for economic, societal, and political stability, we believe the bigger concern for investors today is how relative model parity could compromise pricing power. Tech giants have thrived on monopolies and duopolies for a decade or more. Now, they’re in an LLM arms race where it’s unclear when or even if ever leadership will be sustainable.

There’s already evidence of pricing power challenges. In January, Google dropped the price of its AI business tools by more 50%. Then in December, it was reported that Microsoft is struggling to get customers to increase spending. To quote a Bloomberg article: “One Microsoft sales unit had asked salespeople to increase customers’ spending on the company’s Foundry marketplace by 50% in the last fiscal year. But fewer than one-fifth of salespeople in that unit met their targets.” Model weakness is undoubtedly contributing to those pricing challenges. Nonetheless, we believe competition from akin models will apply downward pressure on pricing at least for the next three years."

While some of those details are now outdated, the dynamics remain the same. Learn more about Sage Road Research here: https://t.co/Wgwz2xnvR6. Interested in subscribing? Message me.

Bloomberg link: https://t.co/5KO08wpla6

The margin of safety is almost gone

Hyperscaler capex is approaching telecom bubble levels as a % of operating cash flow... and once the buildout starts leaning more on equity & debt the market is going to look at it differently

5 out of the 7 stocks in the Magnificent Seven have actually underperformed the S&P 500 since the start of 2025, a very different picture than 2023-2024.

Only Google and Nvidia have outperformed.

Bernstein non electrical network and grid build as a copper and aluminum demand source. Aluminum hand copper and price-elastic substitutes with tradeoffs.

“80% of transmission capex goes to aluminum” $CENX

🧠 AI MEMORY SHORTAGE (60 SEC BREAKDOWN)

We modeled supply vs demand for HBM4 = the memory every AI chip is bolted to. Only 3 companies on earth make it - $MU is one of them.

▪️Demand > supply every quarter through 2028

▪️Worst gap: late 2027 (only ~70% of orders filled)

▪️Bottleneck isn't fabs, it's stacking machines

▪️16 perfect layers per chip (1 crooked layer= trash)

📡SK hynix just panic-ordered more = the signal.

▪️Price path: $16.60 → $30+/GB. Bull: $53

▪️Buyers not bluffing: each $16.60/memory ~$29/yr AI revenue

▪️Micron at $900 looks expensive, but trades under 8x our 2028 estimate.

▪️Street EPS went $12 → $108 in a year.

The market believes the money, but it just doesn't believe it lasts - our model says it lasts through 2027, but 2028 is the fight.

🔔4 smoke alarms to get us out early:

▪️memory prices below model

▪️machine orders slowing

▪️AI revenue per GB rolling over

▪️+94% YoY industry growth peaking

Every boom funds the overbuild that ends it - our alarms are built to ring 2 quarters before the top🚀

US 10-year Treasuries are offering about the greatest amount of yield versus the S&P 500's earnings yield going back to 2003. Either earnings have to keep outperforming, or bonds will start looking like an increasingly attractive alternative.

Data from Altimeter:

Morgan Stanley now projecting $GOOG to spend $299B on CapEx next year up 57% from $190B this year

The biggest revision to previous estimates by a country mile.. $MSFT. CapEx est. revised from $178B to $276B in 2027 🤯

Hyperscaler CapEx now est. >$1.1T

The brilliant Eric @bonabeau creates a scenario engine for the IPOs of SpaceX, OpenAI, and Anthropic. He combines fast-entry index inclusion demand, pro-rata funding sales from existing constituents, discretionary retail rotation out of incumbent equities, and lock-up-driven supply releases. The engine allows you to tune the parameters. No answers but a lot to think about. Full paper in tab at the top right: https://t.co/d9FthtAj1C

Very interesting and scary report from Morgan Stanley

The financial engineering behind hyperscaler capex

The truly unsettling part of the AI boom isn’t how much money is being spent

It’s how that money is being engineered through accounting

Hidden liabilities (> $1.8T)

Huge obligations sit off‑balance‑sheet: nearly $1T in purchase commitments, $800B+ in leases not yet started, $2T+ in RPO.

Future cash outflows that don’t show up as debt.

The coming depreciation hit

Profits look good only because spending is stuck in CIP.

Big Tech faces $520B+ in depreciation over 3 years.

ORCL’s depreciation ratio: 7% → 28%.

Supplier financing pressure

Unpaid capex is ~$110B.

ORCL’s DPO exploded from 35 → 170 days.

The whole supply chain is effectively financing the AI build‑out.

Lease accounting gray zones

Whether GPU contracts count as leases or services is subjective — and companies use that flexibility to shift billions on/off the balance sheet.

$ORCL = the most aggressive

Largest lease commitments, RPO up 300%+, capex‑to‑sales hitting 189%.

Oracle is running the highest financial leverage in the ecosystem.