@olddog100ua 1) tank economy

2) blame tanked economy as left over from “frothy” previous Biden admin

3) set bar very low with tanked economy

4) show modest growth from low bar tanked economy by 2027

5) take credit for “recovery” from “disastrous” prior Biden admin

@FidiumFiber No, I was able to reach someone via email. I suggest you update your phone system. I waited for 35 minutes in silence on the phone and finally gave up after receiving an email response.

And thank you for replying to this.

@Amtrak You really need to overhaul that chat support. It’s embarrassing TBH.

I’m trying to book 1 way ride POR to BOS and getting an error message on site. Is it not available?

@EPBResearch@BlauGloriole Breaking down $100 ($000s) mortgage for purchase of house:

1) Creating loan: Dr loan $100, Cr deposit $100

2) Transferring funds to seller bank: Dr deposit $100, Cr reserve $100

Result:

Lending bank: Reserve down $100, loan up $100

Seller bank: Reserve up $100, dep up $100

$STWD CEO: "The federal government makes no mistake is leaning across all the banks, big and small, and saying reduce your exposure to the Office segment. I don’t know what they think is going to happen to a $3 trillion asset class but it will take down the banks"

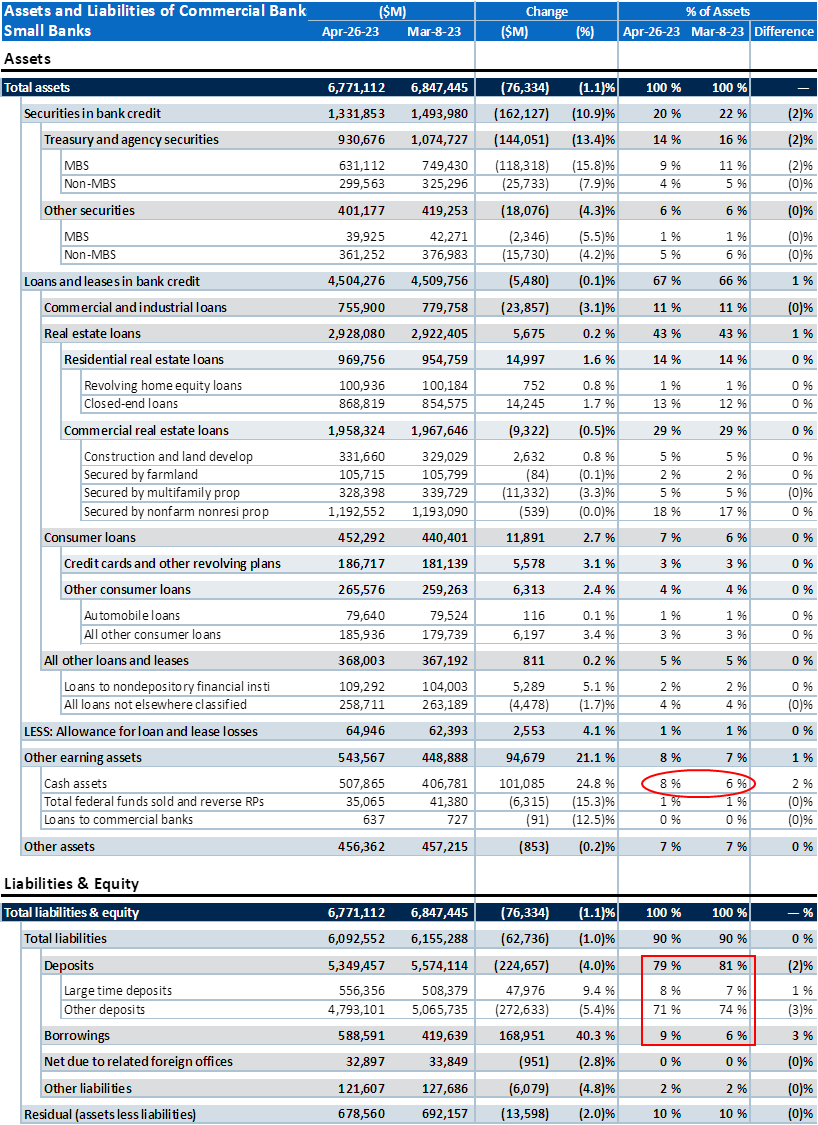

@BobEUnlimited Comparing the 4/26 reading to the 3/8 lows for small banks, liquidity positions much better with funding mix shifted to wholesale. Implications for NIMs.

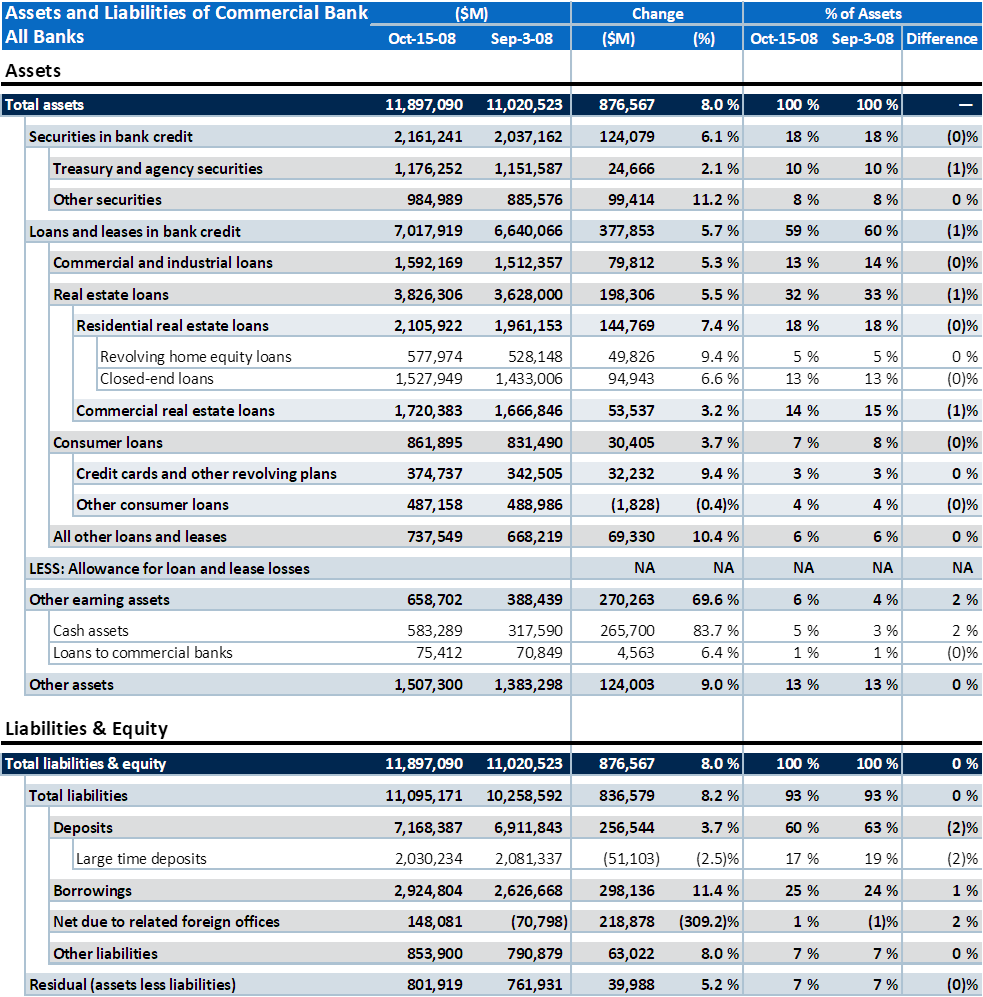

@profplum99 The spike in the time period you've chosen is from 9/3/08 to 10/15/08, which was when Lehman failed (9/15/08). Here's a full balance sheet comparison showing everything went up. I'm guessing the spike in loans is more of a reporting thing than actual credit extension.

@AswathDamodaran I think part of the problem is that years of QE created excess deposits and Basel III incentivized banks to put this excess liquidity into securities. This works if rates get lower and lower, which is unsustainable in the long run as you eventually hit the zero bound.