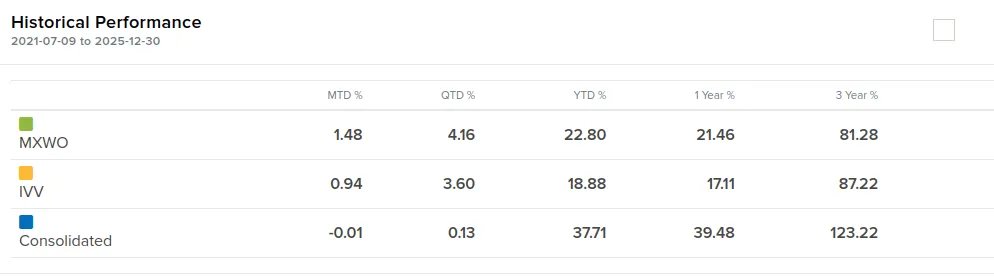

Published my review of 2025 on Substack as well as Blogger since I need a backup platform in case things get blocked. Main portfolio up ~37% with ASX up around 15-20%. Mentioned most of my positions as well as what I think of the AI supply chain buildout.

@AlphaExponent I'm probably on opposite extremes on this compared to the average person. I think dreams are legitimate as real memories as experiences are the root. I think photos are often not real as the poses and smiles often wouldn't exist if not for the photo itself.

@capytalmgmt They were also buying shares in the 2017-2018 period if i recall correctly so buying back wouldn't be a perfect indicator in this case...

I have a small position as they are apparently making humanoid hands which should be adjacent to their expertise in tactile buttons

With the new budget, Australia has got to be one of the least attractive tax jurisdictions to live in for capital growth? Minimum 30% tax rate irrespective of marginal tax is insane.

Aus gov and it's infinite genius trying to resolve a demand problem with housing by making it relatively more attractive than other asset classes as it's held over longer time frames.

Seems like I have 1 day left to go on a shopping spree for stocks before CGT changes come in, and after that will either be assets to be held for 15+ years or high dividend stocks.

Tough times...

@nevergr33dy IDK about unusually innovative. Most of their tech projects seems to have failed to gain traction such as e-clad and seem to be relying on the original innovations. Near term concerns about tunsten input costs.

@valuedrift@testinprodcap Undercapacity in novel/5a attractions. Overcapacity in fake old towns that everyone visited a million times. Feel it's the same story with China market in general. Oversupply of the mundane and undersupply of the novel. Then everyone copies the novel and it becomes new mundane

CNGR $2579.HK might benefit if Solid State starts commercialising due to each battery containing higher nickel content. 20x 2025 earnings. 1Q 2026 earnings is 80-100% higher than 1Q 2025. No idea if it's sustainable but margins are already low.

Recently, a lot of updates on Solid State Battery out of China -> supply chain is commercializing.

For solid Lithium Sulfide electrolyte, 光华科技 has achieved 6N purity already & 天赐材料 has reached 5N+ purity.

Equipment makers & mineral suppliers have also achieved new tech level.

innovation is required at every step. When you see CATL or BYD produce solid state battery & install them in EVs next yr, don't forget all the suppliers that have also raised their game.

Looking at the numbers of $951.HK Chaowei Power and it's quite funny.

Market cap is 1.5B which is what they spend a year on R&D pretty much.

Since 2021, Revenue has almost doubles but net profit has almost halved resulting in a net margin of 0.5%.

At 4x P/E and 0.2 P/B, 4% div

Quick thread on my recent holiday to China:

Have spent more than 1/3rd of my life there visiting biennially for last decade so not too much new, just some observations with some rants. Maybe each comment will be a theme.

@valuedrift Hard to make like a like for like comparison since I was in different cities in a different season but I had no milk tea this time compared to 2 years ago. The shops weren't really featuring it, much more fruit/matcha based now. Maybe mixue made everyone sick of it

@statarbed Highly doubt it imo. Can't think of a time and soe has been privatised on HK and crcc has hardly been at the forefront at increasing shareholder returns. Cousins at crrc have been doing a much better job. Hope would be having a kpi like ROE at SOEs where they reduce the e part.

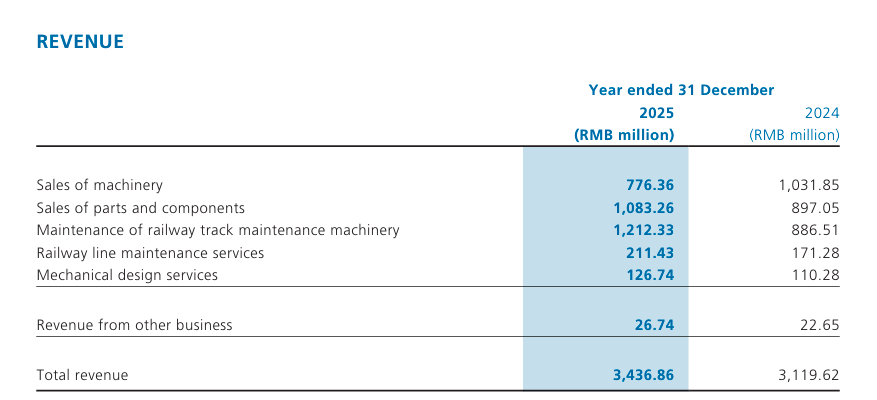

With all the * Deep Value account spopping up, waiting for one called HK/China Deep Value pitching something like $1786.HK CRCC High Tech where Net Cash is 1.4x Market Cap, 0.15x Book, 7x Earnings and where revenue is likely now mostly recurring in a monopoly maintaining rail

9. For investing, there's really nothing too new. It's like opposite of investing in the West, consumer is shit, will bargain like hell and be extremely fickle. Unlike the west, better to be away from the consumer and just buy inputs to consumer companies.

Xi apparently really likes Wang Yang Ming and we are again seeing the merging of Idiologies. I like the concept of the Right action is only valid at the right time, obviously not a unique chinese idea as it's also similar to Hegel I believe