Full 🔊 interview of @elonmusk earlier today, by Texas Governor @GregAbbott_TX , discussing SpaceX’s aspirations for the moon, Mars, and onward to the stars!

(courtesy the Sean Hannity radio podcast) $SPCX

Our internal assessment is that Grok 4.5 is roughly comparable to Opus 4.7, but much faster. The combination of capability, faster speed and lower cost is what makes it competitive.

We are closing the loop on real-world usefulness, not benchmarks. Hardcore engineers at Tesla & SpaceX find Grok 4.5 genuinely useful, which is what actually matters.

🎙️Podcast with @stevenmarkryan! Deep Dive on why he's buying @SpaceX stock 🚀

He made me EVEN MORE bullish!? Didn't know that was possible 😂

Our first ever publicly recorded conversation. This was a blast!! ⚡️

1:22 Do you own $SPCX??

4:13 How do you justify a $2T Valuation for @Spacex? AI Datacenters

9:23 Starlink’s Insane Potential

15:23 Cursor Acquisition & Grok Build

22:37 Competition from Anthropic & OpenAI

25:22 SpaceX Is AI Compute Maxxing On Earth

27:49 Agents Will Change How We Build Code

29:48 Orbital Compute & Starship

46:54 Bidding War for SpaceX Compute

51:21 Grok can help SpaceX with AI

53:36 SpaceX Bearcase

55:42 Fall of the Mainstream media

1:04:57 Terafab not getting enough coverage

1:09:14 Asteroid Mining, Raw Materials from the Moon

1:10:04 The Tesla + SpaceX Merger

This was one the most eye-opening podcasts regarding the $TSLA & SpaceX merger that I have ever done.

Many Tesla shareholders will say it wouldn't be fair if Tesla stock is not at least $700 prior to a merge with SpaceX but @nextbigfuture breaks it down for us why it's necessary for Elon to merge Tesla & SpaceX ASAP for it to benefit Tesla investors massively.

His example was how xAI investors agreed to merge with SpaceX, even though more than 60% of the combined company’s revenue is currently coming from AI compute rentals, which generate roughly 100% direct net profit margins. At the same time, xAI investors would only own 20% of the merged entity. It may have looked unfair on the surface, but as Brian explained in the podcast, a closer look shows that the structure was actually very good for xAI and its investors.

We deeply spoke about what is the realistic scenario of when a merger could happen and what premium $TSLA will get.

YOU DO NOT WANT TO MISS THIS PODCAST!

This was an awesome podcast and is available for YouTube Members and X subscribers only until Saturday morning!

GET YOUR POPCORN(s) READY!

https://t.co/wUjw2l3aYC

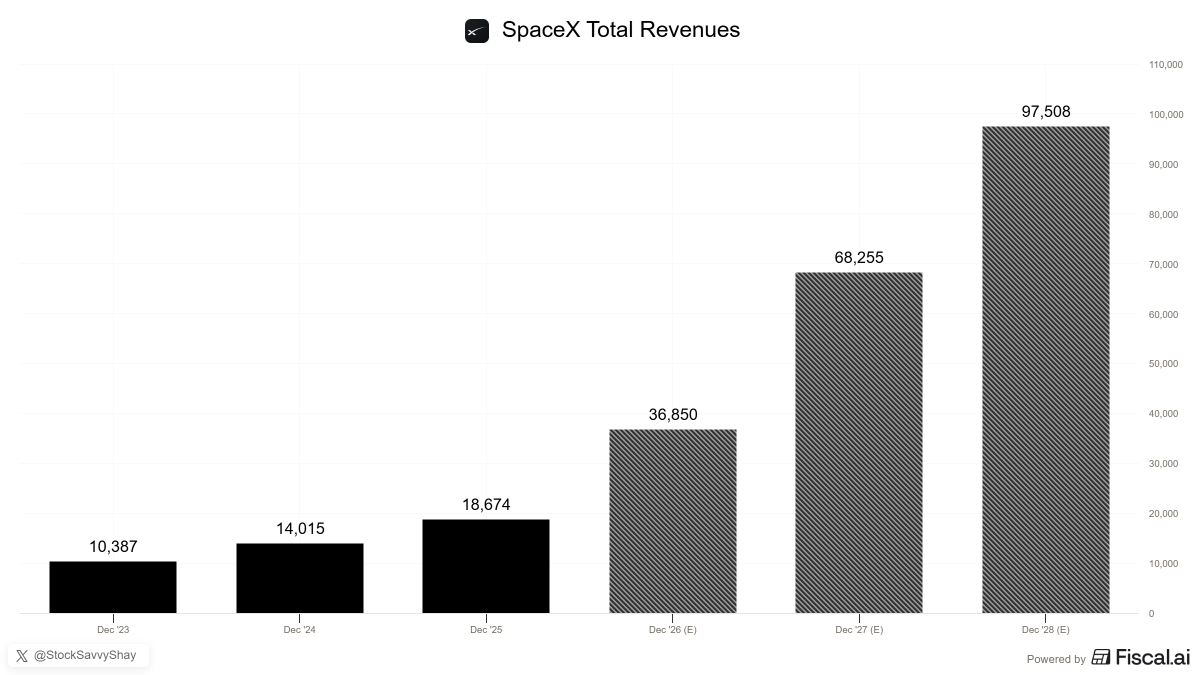

$SPCX is expected to approach ~$100B of revenue by 2028 which would make SpaceX one of the fastest-scaling businesses in the world at this size.

The reason that ramp is even possible is that SpaceX controls the launch layer, uses that launch capacity to scale Starlink, uses Starlink cash flow to fund Starship and is now adding direct-to-cell, V3 satellites, AI compute leasing and Grok/X distribution on top.

Starlink has scaled past 10M subscribers in under five years and is still early with next-gen V3 satellites carrying 10x the downlink capacity of V2 and direct-to-cell already reaching millions of devices across 30+ countries through partnerships with 30+ mobile carriers.

Starship is the piece that widens the lead further because at ~10x payload of Falcon 9 and built for full reusability where it can collapse the cost per kg to orbit and deploy V3 satellites at scale so every Starship improvement feeds directly back into cheaper launch and a denser Starlink network.

The new wildcard is AI compute where SpaceX is leasing spare Colossus capacity to $GOOGL and Anthropic at a combined ~$26B annualized run rate. What makes that even more interesting is that the recent Cursor acquisition also gives SpaceX a direct play in the application layer meaning it can own the compute, own software that runs on it and use X as a distribution channel.

The path to ~$100B by 2028 comes from launch, Starlink, direct-to-cell, Starship, AI compute and software distribution all compounding inside the same platform in a theme that's just getting started.

Grok 4.5, based on our 1.5T V9 foundation model, with Cursor data added in supplemental training, is now in private beta at SpaceX & Tesla. Early evals show performance close to, perhaps exceeding Opus.

RL is continuing to significantly improve the model, and the Grok Build harness gets better every day.

Nice work by all those involved!

Completely trained from scratch new models will be released by @SpaceX every month this year.

HERE IS THE FULL SPACEX $SPCX SHARE UNLOCK TIMELINE

Right now only 4.9% of shares are in the free float.

Here is how that changes over the next 14 months:

Early unlock window (Jul - Dec 2026):

Aug 8: 11.8%

Aug 20: 15.2%

Sep 9: 17.7%

Sep 24: 20.1%

Oct 9: 22.6%

Oct 24: 25.1%

Nov: 27.6% → 37.5%

Dec 8: 40.0%

On Day 366, June 12, 2027: Elon's 46.1% stake becomes eligible ... The free float jumps from 50.8% to 96.9% in a single day.

By September 2027 the float reaches 100%.

Tesla and SpaceX over the next few months:

• June 18: CRSP index inclusion for SpaceX. Triggers an estimated $4-7B in forced buying by passive funds.

• June 18: FTSE Russell index inclusion for SpaceX. Triggers an estimated $6-9B in forced buying by passive funds.

• June 26: MSCI index inclusion for SpaceX. Triggers an estimated $3-5B in forced buying by passive funds.

• End of June: HW3 Tesla owners get FSD V14 Light. Expect possible delays.

• July 2: Tesla Q2 vehicle and energy storage delivery report.

• July 6: NASDAQ 100 index inclusion for SpaceX. Triggers an estimated $8-12B in forced buying by passive funds.

• Late July: Tesla Q2 earnings call.

• Early-mid August: SpaceX Q2 earnings call, their first earnings call as a public company.

• 2 trading days after SpaceX's Q2 earnings released: 30% of eligible insider shares unlock (equates to 12% of all outstanding shares).

NOTE: Since only about 40% of all outstanding shares are eligible for early release lockups, that 30% above equates to 12% of all outstanding shares. Elon's shares, board member shares, and some others, are subject to an extended lockup of 366 days. Together, the shares subject to these extended lockup restrictions represent 60% of SpaceX's outstanding shares.

• August 21: 7% of eligible insider shares unlock (equates to 2.8% of all outstanding shares).

• September 10: 7% of eligible insider shares unlock (equates to 2.8% of all outstanding shares).

• September 25: 7% of eligible insider shares unlock (equates to 2.8% of all outstanding shares).

• September: Indexes rebalance. SpaceX will then have a higher weighting in those indexes due to an increase in the public float from insider shares being unlocked. Passive funds would likely need to purchase billions of dollars worth of additional shares to bring their holdings in line with the new index weight.

• October 2: Tesla Q3 vehicle and energy storage delivery report.

• October 12: 7% of eligible insider shares unlock (equates to 2.8% of all outstanding shares).

• October 26: 7% of eligible insider shares unlock (equates to 2.8% of all outstanding shares).

• Late October: Tesla Q3 earnings call.

• Early-mid November: SpaceX Q3 earnings call.

• 2 trading days after SpaceX's Q3 earnings released: 28% of eligible insider shares unlock (equates to 11.2% of all outstanding shares).

• December 9: 7% of eligible insider shares unlock (equates to 2.8% of all outstanding shares).

• December: Indexes rebalance again. SpaceX will then have an even higher weighting in those indexes due to an increase in the public float from insider shares being unlocked. Passive funds would likely need to purchase billions of dollars worth of additional shares to bring their holdings in line with the new index weight.

(The Cursor acquisition will likely affect these lockup percentages slightly)

SpaceX has exercised the option to acquire @cursor_ai in an all-stock transaction with the goal of building the world’s most useful AI models.

For the past few months, SpaceXAI has been jointly training a model with Cursor, which will be released in Cursor and Grok Build soon.

We look forward to working closely with the Cursor team to advance our frontier AI capabilities

To everyone questioning SpaceX / $SPCX’s highly successful IPO and its $2.1T market cap, let me share what I believe is the best arbitrage setup.

Do you know $SATS?

$SATS is expected to receive 261.8M shares of $SPCX, worth roughly $42B based on the 6/12 closing price.

Yet SATS’ current market cap is only about $33B.

Short: $SPCX

Long: $SATS

$SATS will effectively own approximately 2% of SpaceX / SPCX.

According to the SPCX prospectus, in exchange for acquiring spectrum from SATS, SPCX will pay SATS 261.8M shares of SPCX stock, roughly $8.5B in cash, and an additional ~$2.0B in cash to cover interest payments that SATS would otherwise have been responsible for.

In addition, SATS is expected to sell roughly $23B of spectrum to $T.

The transactions with $T and SPCX were approved by the FCC on 5/12. If no petition for reconsideration was filed by 6/11, the approval should likely have become final automatically. As of 6/14, I have not confirmed any petition for reconsideration.

Also, the spectrum transfer structure is SATS → TRUST → SPCX. Since the SATS → TRUST transfer has already been completed, I believe the closing risk is relatively low.

Now let’s calculate $SATS NAV.

My base NAV assumptions:

SPCX ownership: approximately 2%

SATS basic shares outstanding: 298M

Fully diluted shares after convertible bonds: 348M

I use 348M shares in the calculation below.

Cash proceeds from spectrum sales to $T and $SPCX:

From $T: approximately $23B

From $SPCX: approximately $8B in cash

Total: approximately $31B

Assuming the convertible bonds are converted into equity, net cash after debt repayment would be roughly $11B.

Regulatory / escrow / contingent liability haircut: -$2.5B

Net cash after haircut: approximately $8.5B

Remaining operating business value: $10B

Based on roughly $300M of operating income in Q1 2026 × 4 quarters × 8x multiple.

Even after the spectrum sales to $T and $SPCX, SATS will retain remaining spectrum assets. The most notable example is AWS-3 paired spectrum, which SATS previously planned to sell to $VZ for approximately $9.8B.

If we conservatively value the remaining spectrum at $10B, that adds approximately $28.7 per share of NAV based on 348M shares.

Formula:

SATS NAV

= {SPCX market cap × 2% + net cash after haircut + remaining operating business value + remaining spectrum value} / 348M shares

= {SPCX market cap × 2% + $8.5B + $10B + $10B} / 348M shares

SATS NAV by SPCX market cap:

• SPCX $2.0T → SATS approximately $197

• SPCX $2.25T → SATS approximately $211

• SPCX $2.5T → SATS approximately $226

• SPCX $2.75T → SATS approximately $240

• SPCX $3.0T → SATS approximately $254

This is my personal analysis, not financial advice.

There has been a lot of hand wringing on the appropriate valuation of SpaceX. Some large institutions believe SpaceX can only be valued at half what the market seems to be willing to pay for it. Others are claiming it has 15X appreciation ahead of it.

Almost all of this difference of opinion comes down to how comfortable you are modeling beyond 2030 and what valuation method you use.

2030 valuation using a traditional Gordan DCF produces a very different result than a 2040 EV/EBITDA Multiple. Both have pros and cons. Most analysts don’t really discuss this and lead with a headline number.

We are very comfortable modeling out to 2040, as large portions of what SpaceX is proposing is real world infrastructure, which provides modelable physics constraints to anchor against.

The analysis we released today explores this in-depth, its open to the public all the way through IPO. I highly encourage you check it out prior to then.

https://t.co/McShCl78uo

We’ve run 5,000 monte carlo runs across 500 variables (real number, even though it sounds fake) and three valuation methods.

This video is of a 3D cloud chart showing every simulation outcome expected in valuation output across two of the most impactful variables to the model when using an EV/EBITDA multiple from 2026 to 2040.

The horizontal axis is the steepness of the orbital data center demand S-curve.

The vertical axis is the rate at which chip compute efficiency becomes cheaper.

Each of the 5,000 dots is one simulated future; green dots are the ones where SpaceX's 2040 value clears the $1.77T IPO line, over time.

Under EV/EBITDA valuation through 2040, 96% of our simulated futures clear the expected IPO price once the bell rings Friday.

We aren’t publishing this publicly to tell investors what the stock is worth, we’re publishing this to help investors understand the world of outcomes, what the fundamentals suggest through 2040, and what frankly most analysis simply won’t share.

SpaceX is a generational company working on long term infrastructure harnessing a domain no one has been able to tap in so far: space.

It deserves doing the work as an investor. because this in not financial advice.

The cleanest way to hold SpaceX is a bond stapled to a call option (AI-Compute); Starlink is the bond, the near term SatCom annuity that funds the next flywheel.

Understand the world of outcomes and take your position accordingly.

Comparables and P/E won't take you far enough.