So apparently $CBOE $ICE $CME and $MIAX are drawing down because the Commodity Futures Trading Commission has allowed Kalshi and Coinbase to introduce a new derivatives product - perpetual crypto futures.

"Perpetual futures, or "perps", are derivatives that lack a traditional expiration date, allowing traders to maintain positions indefinitely without the need to roll over contracts. These instruments also permit high degrees of leverage — often as much as 50-to-1 — enabling investors to amplify their exposure to market moves."

This is apparently the first time that these products have been offered in the US.

Thomson Reuters frames the sentiment/fears in the following way: "The move has sparked concerns that perpetual futures approval for other asset classes could raise competition for incumbent derivatives exchange platforms".

My immediate thoughts are:

1) The approval of a new type of derivate product is a good thing for incumbent exchange businesses. More products = more trading = more volume = more fees = more revenues = more operating income at very high margins. Offering new products for trading is part of their business model.

2) There is nothing proprietary about the contract structure itself. In other words, the incumbents can offer perps with regulatory approval. In fact, "the CFTC issued a policy statement encouraging Designated Contract Markets (DCMs) that wish to list perpetual contracts referencing asset classes not covered by the Order (e.g., agricultural products, precious metals, equity securities, narrow-based security indexes) to voluntarily submit those contracts for Commission review and approval under Regulation 40.3". [Lowenstein Sandler: https://t.co/CPAP5BghTE]

3) Incumbent revenues and earnings are mostly insulated because perps are not a substitute for their main products and services. Perps are not a substitute for options or derivatives settled with physical delivery; and data licensing segments are unaffected.

4) Competition is not fatal to exchange businesses. As Horizon Kinetics points out in their Q3'23 letter (See "The Competition Question"):

a) Exchanges usually have proprietary products - e.g., CBOE's exclusive rights to trade S&P 500 Index options through December 31, 2032;

b) Exchanges can always expand their product offerings around their main products;

c) "The very existence of a related or even identical product on a different exchange creates additional trading and arbitrage opportunities between the two, since slight momentary price differences arise, so that both exchanges experience increased volume";

d) "Trading begets more trading. Anything that lowers the barriers to transacting, like greater volume and liquidity, lower fees, faster execution, better data access and analysis, also begets more trading. The size of the pie is not fixed".

5) Nothing has impacted the incumbents' ability to compound their earnings in their existing business lines as toll booths on the overall volume of trading of securities. They continue to benefit from volatility in good times and bad. To quote HK: "As a croupier, [the securities exchange] simply collects the fees for accessing and participating in the venue it operates. It is true that if trading volumes decline, there will be earnings leverage on the downside, just as there is on the upside. But unless there will be a permanent decline in activity, it will be merely interim cyclicality".

Net assessment: Drawdown is unwarranted; presents an opportunity.

Let me know if you disagree or if I'm missing something.

S&P average single-stock 1m put-call skew has now collapsed to the lowest level in Goldman Sachs entire dataset.

Translation: Everyone is a bull.

Source: Goldman Sachs

@lhamtil I’d be curious to hear opinions of people in the industry as to the extent data centers actually crowd out residential construction. I would expect it to compete more with commercial for land and labor.

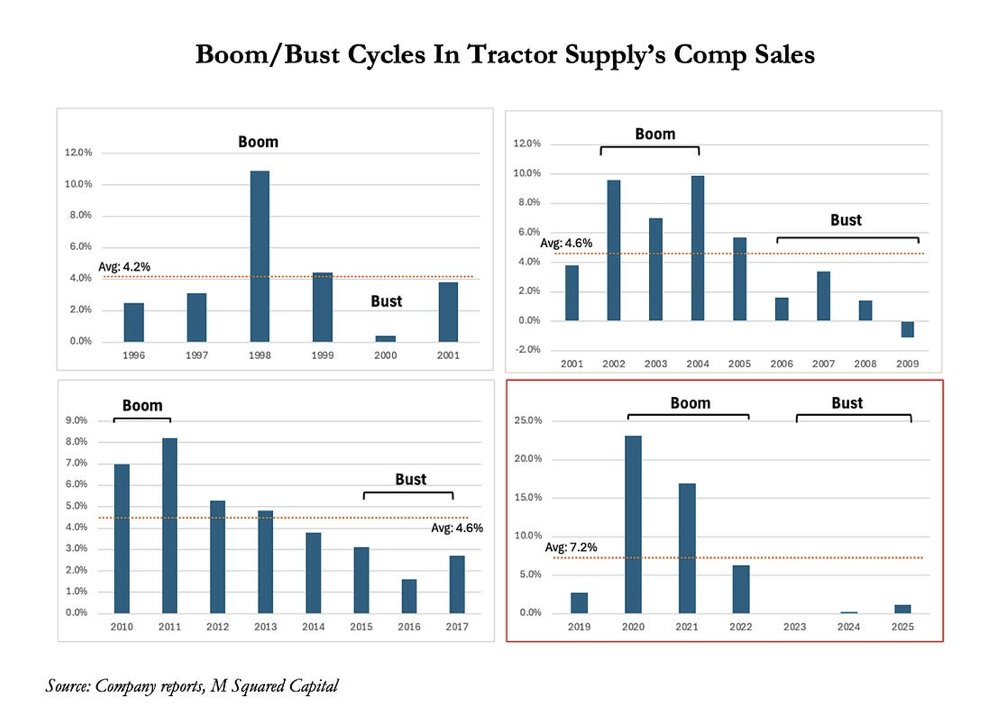

(2/3) $TSCO: CUE The Cyclical Nature Of This Company

The last time we witnessed a 50% drawdown in Tractor Supply’s stock was 2016-2017. Interestingly it was also the last time the company had a 3%-5% comp algo that it failed to live up to. This was exacerbated by commentary from then CEO Greg Sanford blaming farm incomes for the shortfall after many years of saying their business has a low correlation to that data set (they quickly reversed their position on that idea following the stock sell off). We see similarities to that level of narrative change with C.U.E. (consumable, usable, edible) categories seemingly no longer as non-discretionary as formerly claimed (particularly companion animals). The investment thesis that previously supported historically unprecedented valuation levels was largely based on non-discretionary features combined with a highly captive rural audience. We note that the forward P/E in 2016-2017 dropped from a high of ~25x to a low of ~13x.

In this note we dig into the cyclical nature of Tractor Supply’s business. Not necessarily that everything sold is discretionary but more from a perspective that many of the non-discretionary products (immediate needs based) often don’t have repeat purchase qualities, contributing to several boom/bust cycles this century alone (as opposed to what you see at retailers like Costco and Kroger). Weather drives much of the demand and while that might be non-discretionary in moments (such as lawnmower sales in 2024 following several years of drought), it doesn’t necessarily mean those same sales will materialize in subsequent years. We also investigate what looks like active company efforts to mask weakness in supposedly non-discretionary CUE categories through both category definition restatements and physical store expansion.

It’s unfortunate the company stumbled out of the gates following the decision to return to a 3%-5% long-term comp algo at the end of 2024. We look back in history to better understand why the company originally lowered its long term algo to 3%+ in 2018. The simple answer here is it appears market share gains from regional competitors no longer supported upside enjoyed for most the century prior. We don’t understand why management became optimistic as some current comp driving initiatives had already proven troublesome prior to the algo increase (specifically Garden Centers). If anything, it seems the company made a major bet on Direct Sales last year that also missed and now is downplaying the initiative almost entirely with limited recent commentary only towards how the initial investment cycles in 2Q26.

...(Abridged)...

Now that it seems the 3% to 5% long-term comp algorithm is probably too optimistic (as reflected by the stock’s weakness post quarter), we try to think through what a reasonable expectation should be for the next several years. The company’s history proves that it really isn’t as non-discretionary as management likes to purport, with several boom/bust cycles this century alone. Throughout the full cycle of the first three examples, the company was ultimately able to average comps of 4.2% to 4.6%. With the most recent COVID cycle the company is still running at an exceptionally higher average of 7.2%. We believe that indicates continued subdued results are likely on the horizon for the foreseeable future to return to a normalized trendline. In the past, market share gains probably helped to stabilize the boom bust cycle. This might be one reason why the bust phase of the cycle is already the worst this century despite aforementioned comp driving initiatives.

...(Abridged)...

This is a highly abridged version of this 7 page note. Subscribers can find the complete deep dive note and financial model at our website in post #3 of this thread (link also in profile).

We currently have coverage of 20 consumer/retail companies and will always provide all work on Nike and Restoration Hardware for free. See our website for more information.

It's a feeding frenzy.

Retail stock trading volume this month is on track to finish 10% above the previous record set during the January 2021 meme stock bubble.

LIQN Ep 6 | Jared Sleeper, Partner at Avenir

@JaredSleeper (34m)

Jared Sleeper is one of the sharpest software investors I know. He started at Putnam, venture at Matrix, public equities at COATUE, and now he's a partner at Avenir

It's a timely conversation as AI is forcing every software investor to ask THE tough question... "Is AI destroying software moats, creating new ones, or just exposing which companies never had one?"

Hope you enjoy our talk on AI, changing business models, and where security fits in the big picture.

![firstadopter's tweet photo. 👀 "we think the [Google Cloud] margin rise is an illusion" - @SemiAnalysis_ $GOOGL https://t.co/AktwrC3e6U](https://pbs.twimg.com/media/HJWGdltXYAg-7xc.jpg)