@JonathanCohn Hey buddy...Can I ask... why do political commentary folk cross into Economic/Business topics?

I mean, come on... this is so obviously not your circle of knowledge.

🚨 JUST IN: The DOJ has officially CHARGED Nicholas Matthew Scelfo with threatening to MURDER an ICE agent and his family here in Newark

He now faces up to 10 YEARS in prison.

Per DOJ, Scelfo ADMITTED he’s the one on video, and saw it circulating in the media in the hours leading up to his arrest.

Scelfo will appear today in front of a federal magistrate judge today in Newark.

This is a SERIOUS federal felony. 18 U.S. Code § 115: “Influencing, impeding, or retaliating against a Federal official by threatening or injuring a family member.”

Not looking good for this guy!

Do you live in Michigan and want real news you won't see on your local evening news? If so, follow me now- @DaveBondyTV. I left the mainstream media after 25 years to go independent.

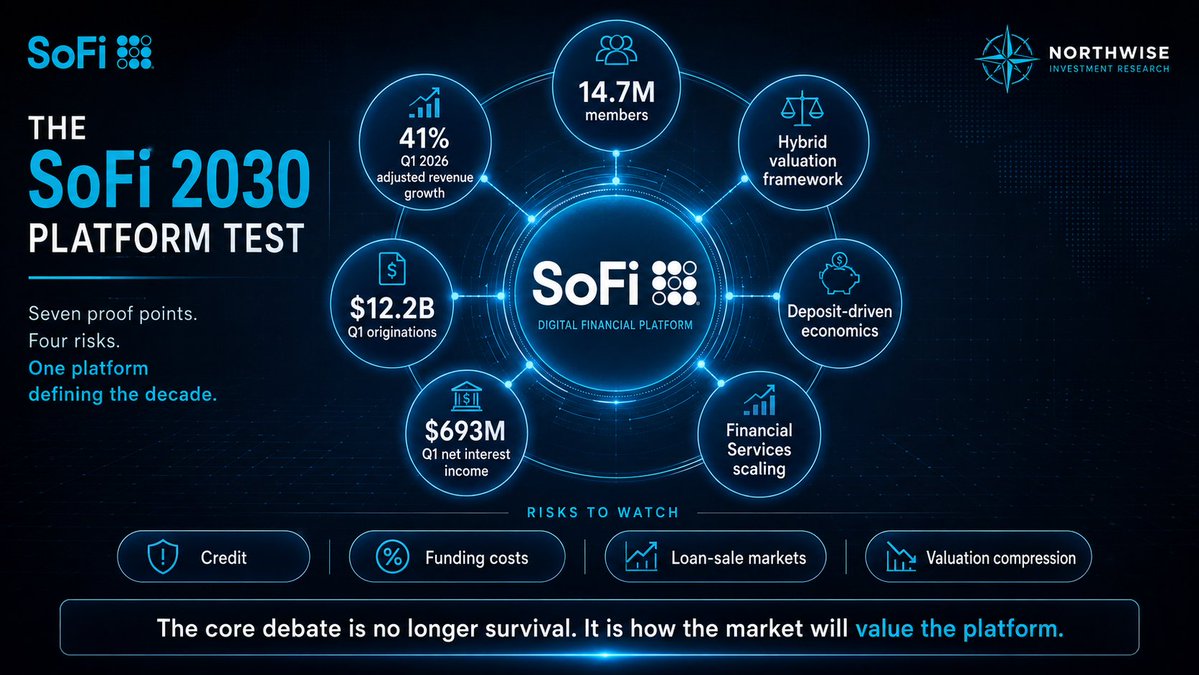

Our $SOFI report and modeling is here! We see Sofi as an incredible opportunity at these levels long term.

Check out our full report in the first comment. ⤵️

We first began buying $SOFI under $10 last April. We don't think we will ever get that opportunity again.

However, we see buying Sofi under $20 today as a similar value proposition with the phenomenal growth, product expansion, and leadership from Noto.

$SOFI is attractive to us because the market debate appears to be lagging the operating reality.

The old debate was whether SoFi could become sustainably profitable. That was the right debate when the business was still proving out the bank charter, absorbing the student loan disruption, and showing investors that growth could translate into earnings.

That is no longer the central question.

The more relevant debate is how SoFi should be valued if the business continues shifting from a lending-led fintech into a broader digital financial platform.

Q1 2026 showed why that distinction matters.

SoFi reported roughly 41% adjusted revenue growth, reached 14.7M members, generated $12.2B in originations, and produced $693M of net interest income. Those numbers do not describe a company merely surviving a difficult rate environment. They describe a financial platform still adding scale, deepening relationships, and expanding its earnings base.

The lending engine remains important. Personal loans, student loans, and home loans still drive a large portion of near-term economics. That creates real credit-cycle risk, and we do not think investors should pretend otherwise.

But lending is increasingly only one part of the structure.

The bank charter gives SoFi access to deposit funding, which changes the economics of the lending business. Deposits lower reliance on wholesale funding and make the balance sheet more strategically valuable over time.

Financial Services is the second piece. As more members use SoFi for banking, brokerage, payments, credit, and other products, the value of each customer relationship can rise without requiring the company to constantly reacquire the same customer through new lending campaigns.

That is why product density matters more than member growth alone.

A one-product customer is still a fairly shallow relationship. A customer using checking, savings, direct deposit, investing, credit, lending, and financial tools inside the same ecosystem is a very different economic asset.

The Technology Platform remains the least clean part of the thesis. Galileo and Technisys still need to prove that they can become more than strategic optionality. If that segment remains weak, it limits the platform argument. If it stabilizes, it adds another layer to the business that the market is not giving much credit for today.

The valuation question follows from all of this.

If SoFi is valued only as a volatile online lender, the multiple ceiling is lower. Credit risk dominates the discussion, loan-sale markets matter more, and investors focus heavily on near-term charge-offs and funding costs.

If SoFi is valued as a digital bank, book value growth, deposit quality, net interest income, and return on equity become more important.

If SoFi is eventually valued as a premium financial platform, the market has to account for member growth, product density, fee revenue, balance sheet compounding, and the possibility that SoFi becomes a primary financial relationship for a large base of digitally native customers.

That is the thesis.

The stock is not attractive because the risks are gone. It is attractive because the risks are visible while the market may still be applying an outdated frame to a business that is changing underneath it.

The risks we are watching most closely are credit performance, funding costs, loan-sale market demand, dilution, Technology Platform execution, and valuation compression.

But the core question has moved on.

SoFi no longer needs to prove it can survive.

It needs to prove the market is wrong to value it like survival was the only thing it ever achieved.

🚨 FRANCE HAS BEEN INVADED and predominantly 3rd worlders are WREAKING HAVOC!

The entire city burned, mass businesses looted, and the usual suspects carried it out.

NEVER allow this to come to America!

Law, order and our culture must be protected 🇺🇸

@kevinmyoung Pretty sure Jesus wouldn’t be a democrat, I very confident he knows there are only two genders and you can’t pick your gender. STFU dumb ass.

$SOFI... Guys... not sure if this is trying to make the rounds, but there is ZERO argument for suggesting that $SOFI isn't holding adequate cash vs deposits.

See below, and just to give you a sense for it, go have a look at $WFC's balance sheet for comparison.

Such a claim is just... well... send them to me, plz...