99% of business books are trash and should be blog posts

I've wasted a lot of time reading stupid ones, here are the ones that are actually useful:

- only the paranoid survive (grove)

- amp it up (slootman)

- hard thing about hard things (horowitz)

- score takes care of itself (walsh)

- zero to one (thiel)

- skin in the game (taleb, not really business book but can make it into one)

- alchemy (rory)

- confessions of an advertising man (ogilvy)

- what you do is who you are (horowitz)

bonus:

- beginning of infinity (deutsch), which really everyone should read several times per year

- biographies of other business people

skip anything by grant, sinek, greene, maxwell or gladwell

How to trade the liquidation levels.

These are @binance Leverage Traders Liquidation Levels. The Red lines are high leverage (100x+). The Yellow are medium (50-100x) the Blue are low leverage 25-50x). When the price hits these lines the trader is liquidated if they did not exit, add margin or stop out. Use these levels to trade crypto. Forget traditional TA it is a retail trap. Follow the liquidity in crypto.

-Where the top blue lines end is Short Setup A

-Where the upper yellow lines meet the upper blue lines is Short Setup B

-Where the upper red lines meet the upper yellow lines is Short Setup C

-Where the upper red lines meet the upper yellow lines is Long Setup C

-Where the lower yellow lines meet the lower blue lines is Long Setup B

-Where the lower blue lines end is Long Setup A

IMO: ALWAYS WAIT FOR SETUP A.

ALWAYS USE A STOP LOSS. EXIT IN PROFIT. MOVE STOP LOSS IN THE MONEY AS SOON AS POSSIBLE.

NFA. Nobody has a crystal ball. Use as a guide. Trade carefully with good stop loss management. Educational purposes only.

The wait is over!

Introducing... 🥁

Bitcoin Quantile Model v2.

You’re going to want to bookmark this post—and follow for regular model updates.

After months of research and development, I’m very proud of this model—my flagship quantile framework.

I’m confident it’s one of the best—if not the best—long-term Bitcoin investment frameworks available.

As a full-time, unpaid Bitcoin researcher, I’m often asked how people can best support my free content.

Simply bookmark, repost, and comment on my posts :)

Thanks for all your continued support!

— PlanC

Key Features & Improvements:

1. Quantile lines never cross—mathematically impossible.

2. Cycle-length agnostic.

3. 133,000+ data points and 1,500 lines of code.

4. Fits and stores 999 quantile levels (τ = 0.001–0.999 in 0.001 steps) and identifies which level the last price is closest to.

5. Fits the two leading decay functions (stretched exponential decay & exponential decay) and selects the better fit via quantile-appropriate AIC.

Uses Akaike weights to identify the best-supported model.

Akaike weights (AIC-based):

Stretched exponential decay: 96.4%

Exponential decay: 3.6%

6. Piecewise Quantile Regression — Linear + Stretched Exponential Decay (Nonlinear).

This week, @PresidioBitcoin hosted the Bitcoin Quantum Summit (https://t.co/BQKeHv1apV). I was thrilled to be invited to attend, and wanted to write up a thread about what I learned this week. I’ll save my commentary for the end, and start with where we are, the challenges we (might) need to solve, and some of the solutions that have been proposed or that people are thinking about.🧵

I respect everyone’s time, so I won’t waste any more of it on childish drama. Let me settle this once and for all:

I created the Quantile Model, and Sina has been a major contributor to its evolution.

The core breakthrough was the quantile approach; the best way to implement it is still being refined, and an improved version will be released soon.

Sminston developed the Decay Channel Model, which I consider one of the best Bitcoin models to date.

APSK introduced the Years-Ahead Power Curve, another outstanding independent model and likewise among the best for Bitcoin.

Giovanni discovered a line on a log-log chart, but has at times tried to claim credit for the significant contributions by Sminston, Sina, APSK, and me.

So, while one angry Italian shouts for attention, four other gentlemen are focused on adding value.

I’ll let you be the judge.

MAJOR CELSIUS TAX UPDATE! Approach to Realize ENTIRE Amount as a THEFT LOSS in 2024 Taxes!

Disclaimers: USA Only | I Am Not Your Personal CPA | Do Your Own Research & Talk to Your Own Tax Professional | Write-Up Focuses on Class 5 Creditors

========================================

Full Video Explanation + Whiteboard Calculation: https://t.co/5UlLL2Npfu

What changed?

After much in-depth analysis and discussions with tax attorneys and individuals close to this case, and the guidance published on 3/14/2025 in Chief Counsel Memorandum 202511015, I have gained additional insights into how the IRS is likely to view the Celsius bankruptcy and associated tax implications. Through these discussions and research, I have reason to believe that losses related to this bankruptcy can be claimed as theft losses via Form 4684, and deducted in-full on Schedule A as an itemized deduction.

For many, this is MUCH more favorable than the Capital Loss approach, as the impact of the loss can be used as a deduction against taxable income instead of needing capital gains to offset against.

Is this approach more favorable?

For many, this approach is more favorable as the losses will be utilized as an itemized deduction against taxable income rather than a capital loss. This distinction is crucial because, without capital gains to offset against, only $3,000 of capital losses can be applied to taxable income each year, with any remaining losses carried forward. However, if you have enough capital gains to offset against, then the full capital loss can be utilized.

With that said, there are a few nuances that need to be considered. First, it's important to understand that this is an itemized deduction. If you typically take the standard deduction, and your losses are not very significant, then this approach may not be more beneficial. Talk with your tax preparer to better understand how this approach impacts you and your personal situation.

What is the reasoning behind this approach?

There are a few factors that play into this approach. When viewed all together, it becomes clear there is an opportunity to take this loss as an itemized deduction as opposed to a capital loss. A few questions need to be answered to help determine how to handle this...

What type of loss is this?

Personal casualty

Theft, or Loss on deposits in insolvent or bankrupt financial institutions

Does the loss qualify under IRC §165(c)(2)?

Is the loss a capital or ordinary loss?

When can you recognize the loss?

Where is it reported?

Should the loss on Form 4684 push to Schedule 1 as an above-the-line deduction or Schedule A as an itemized deduction?

Answering these questions is vital to determining how to handle this loss.

Let's dive in...

1. What type of loss is this?

This is a theft loss by means of fraud. This loss switched from a loss on deposits to a theft loss in 2023 upon Mashinsky's indictment and guilty plea. This is a vital distinction.

2. Does the loss qualify under IRC §165(c)(2)?

Yes, IRC §165(c)(2) allows for deductions for losses incurred in transactions entered into for profit, outside of a trade or business.

Everyone who got involved with Celsius was doing so with a profit-seeking interest. Individuals moved crypto assets to the platform with the intention of profiting from various earning offerings provided by Celsius.

This qualification is absolutely vital; the 2017 Tax Cut and Jobs Act have disallowed personal casualty and theft losses for the tax years 2018-2025, unless related to a federally declared disaster. In fact, all miscellaneous itemized deductions were completely disallowed. HOWEVER, deductions under IRC §165(c)(2) are explicitly excluded from the definition of "miscellaneous itemized deductions" under Section 67(b)(3) and allows for an exemption for losses incurred in transactions that were entered into for-profit. Please see the "Theft losses" section of Topic no. 515, Casualty, disaster, and theft losses where it states: "For tax years 2018 through 2025, individual taxpayers with theft losses are allowed a deduction if the loss is due to theft related to a transaction entered into for profit".

3. Is the loss a capital or ordinary loss?

Since this is (1) a theft loss and (2) a qualified loss under IRC §165(c)(2), this is claimable as an ordinary loss, fully deductible against taxable income as an itemized deduction and not limited to $3,000 per year (assuming no capital gains to offset against).

4. When can you recognize the loss?

When recognizing a loss for tax purposes under IRC §165, the key factor is determining when the loss becomes fixed and determinable with reasonable certainty. Generally, a loss is deductible in the year it is sustained, meaning when the taxpayer can establish that there is no reasonable prospect of recovery. According to Treas. Reg. §1.165-1(d)(2)(i) and recent IRS guidance (Chief Counsel Memorandum 202511015), a taxpayer does not need to prove that recovery is impossible, nor must they be an "incorrigible optimist." Instead, the loss is sustained when, based on the facts available at year-end, it is reasonably certain that the remaining portion is irrecoverable.

In the case of the Celsius Network LLC bankruptcy, creditors faced an evolving recovery estimate, raising questions about whether to deduct their losses in 2023 or 2024. The initial Chapter 11 plan was confirmed on November 9, 2023, fixing a 67% expected recovery (for Class 5 creditors), which could potentially justify taking a 33% loss in 2023. However, the final modified plan, confirmed in January 2024, increased the recovery estimate to 79.2%, meaning the actual irrecoverable portion was 20.8%. While there is a possibility a reasonable position exists to recognize the loss in 2023, given the information available at year-end, the more conservative approach is to wait until 2024, when the recovery amount was finalized. Ultimately, taxpayers must weigh the certainty of their loss at the end of 2023 against the IRS standard requiring that losses be sustained in the year they become reasonably certain.

See the timing section below for more detailed analysis.

5. Where is it reported?

Form 4684 (Casualties and Thefts) is used to report personal casualty and theft losses. Section B is used to report casualty and theft losses of business and income-producing property.

6. Should the loss on Form 4684 push to Schedule 1 as an above-the-line deduction or Schedule A as an itemized deduction?

Section B, Part II distinguishes losses from (i) Trade, businesses, rental, or royalty property (which pushes to Form 4797/Schedule 1) and (ii) income-producing property (which pushes to Schedule A).

The definition of "income-producing property", as defined by Form 4684 Instructions, is "property held for investment, such as stocks, notes, bonds, gold, silver, vacant lots, and works of art".

Crypto assets align with the definition of "income-producing property" and therefore the loss should be pushed to Schedule A.

Please note, gains from this are treated differently and will go to Schedule 1.

Key considerations for timing of when to recognize the gain/loss

Background

The timing of recognizing a deductible loss under IRC §165 depends on when the loss becomes fixed and determinable with reasonable certainty. Courts have recognized that a bankruptcy court’s confirmation of a Chapter 11 plan serves as the definitive event that fixes a loss, allowing it to be recognized in the year of final confirmation.

The Court Ruled That the Chapter 11 Plan is Final and Binding on All Creditors

Judge Martin Glenn ruled in In re Celsius Network LLC, Case No. 22-10964 (MG) that the confirmation of the Celsius Chapter 11 Plan on November 9, 2023, was a final, legally binding event on all creditors.

The final modified plan was confirmed in January 2024, establishing the definitive terms of creditor recoveries.

The ruling emphasized that the confirmation order settled, expunged, and discharged all claims, binding all creditors to its terms and permanently enjoining them from pursuing any further claims against Celsius.

The November 9, 2023, confirmation order stated an expected recovery of 67% for Class 5 Claims, while the final modified plan in January 2024 increased the recovery estimate to 79.2%. This established the irrecoverable loss at either 33% or 20.8%, depending on which point in time is used.

Note: For those who claimed the loss in 2023 using the original 33% irrecoverable amount, distributions received in excess of the original plan need to be recognized as income in the year received.

Key Legal Precedents Supporting Loss Recognition Upon Plan Confirmation

Rosenberg v. Commissioner (1986 T.C. Memo 1986-28)

The Tax Court held that confirmation of a bankruptcy plan can serve as the identifiable event fixing a loss for tax purposes.

In Rosenberg, the taxpayer’s investment in a partnership that filed for Chapter 11 became worthless upon plan confirmation, which determined the extent of recoverable assets.

The court ruled that the bankruptcy confirmation order constituted a final, identifiable event fixing the taxpayer’s loss, making it deductible in the year of confirmation, even if there remained a small possibility of additional recovery. The key factor is that the confirmation order established with certainty the extent of allowable recovery, satisfying the IRS standard for a deductible loss.

General IRS and Court Position on Bankruptcy and Theft Losses

Under Treas. Reg. §1.165-1(d), a loss is deductible in the year it is sustained, meaning when it is finalized and no longer subject to substantial recovery.

Courts have ruled that confirmation of a Chapter 11 plan legally fixes the recovery amount, making the loss recognizable in that tax year, even if distributions occur later.

Treas. Reg. §1.165-1(d)(2)(i) states that if there is a reasonable prospect of recovery, the loss is not deductible until it becomes reasonably certain that no further recovery will occur. The January 2024 confirmation of the final modified plan fixed the recovery amount at 79.2%, eliminating uncertainty regarding the remaining 20.8% loss, making it deductible in 2024.

IRS Chief Counsel Memorandum 202511015 further clarifies that a loss is not deductible if there remains a reasonable prospect of recovery at the end of the year. However, this does not require that there be no possibility of recovery, nor must a taxpayer be an “incorrigible optimist” to justify taking the deduction. The memorandum states that a taxpayer’s determination should be based on the facts available at the end of the tax year, and they need only establish that recovery is not substantially likely, rather than impossible.

Reasonable Basis for Taking the Loss in 2023

The initial confirmation order on November 9, 2023, fixed a recovery estimate of 67%, establishing 33% as permanently lost at that point.

Based on the IRS standard that a loss is deductible when the amount is fixed and determinable, there is a reasonable position to take the deduction in 2023 based on the information available at the end of the year.

Since the final plan modifications in January 2024 only adjusted the recovery percentage from 67% to 79.2%, it is reasonable to argue that the core elements of the loss were already fixed in 2023.

More Conservative Approach: Recognizing the Loss in 2024

The final modified plan was confirmed in January 2024, finalizing the exact recovery percentage at 79.2% and setting the irrecoverable portion at 20.8%.

A more conservative position would be to wait until 2024, when the finalized recovery amount was set, removing any remaining uncertainty about the loss.

This approach aligns with Treas. Reg. §1.165-1(d)(2)(i) and Chief Counsel Memorandum 202511015, released 3/14/2025, which stress that a loss is not sustained if there is still a reasonable prospect of additional recovery at year-end.

Application to Celsius Bankruptcy

The Celsius Chapter 11 Plan was initially confirmed on November 9, 2023, binding all creditors and eliminating their right to any further independent claims.

The final modified plan was confirmed in January 2024, setting the final expected recovery percentage and fixing the amount of loss with reasonable certainty.

The plan initially stated that creditors could expect to recover 67% of their claims, legally determining that 33% was permanently lost as of the end of 2023.

The final plan increased the expected recovery to 79.2%, meaning the actual irrecoverable portion became 20.8% in 2024.

Since the final, modified plan was confirmed in 2024, the most conservative approach is to recognize the loss in the 2024 tax year.

However, given that the 67% recovery was fixed in 2023, there is a reasonable position to recognize the loss in 2023 based on the facts known at year-end.

Timing Conclusion

There is potential for a reasonable argument to be made to take the loss in 2023, as the 67% expected recovery rate was fixed by the confirmation order on November 9, 2023, and the loss was determinable with reasonable certainty at year-end.

A more conservative approach would be to recognize the loss in 2024, when the final modified plan was confirmed in January, setting the exact recovery at 79.2%.

Based on bankruptcy law, IRS regulations, and case precedents, the confirmation of the final modified Celsius Chapter 11 Plan in January 2024 serves as the final, identifiable event fixing the loss.

Taxpayers may choose to deduct the loss in either 2023 or 2024, depending on their risk tolerance and interpretation of reasonable certainty under Treas. Reg. §1.165-1(d).

TL;DR recap

> Individual taxpayers (not connected with a trade or business) engaged with Celsius with a profit motive.

> Individual taxpayers were made aware of a potential loss in 2022 upon Celsius filing for bankruptcy and freezing their accounts.

> This loss became a theft loss in 2023 upon Mashinksy's indictment and pleading guilty to several counts of fraud.

> Due to a reasonable prospect of recovery being unknown, and the bankruptcy court still attempting to recover assets, no theft loss could be deducted in 2022 under § 165.

> Celsius distribution plan was approved on November 9, 2023 and was modified and made final in January 2024, with all recoveries explicitly defined and fixing the irrecoverable portion of claims.

> With the irrecoverable portion of claims fixed, and substantially all recoveries distributed in 2024 (96%+), a case can be made that the loss becomes fixed and determinable with reasonable certainty as of December 31, 2024.

The above facts result in a deductible theft loss under §165(c)(2) in 2024.

Conclusion

Overall, this approach can be much more favorable for many Celsius victims as the loss can be taken as an itemized deduction, not limiting taxpayers to only deducting $3,000 a year (assuming there are no other capital gains to offset). While this approach is more favorable for most, it is very important to ensure that all your records are well-kept and up-to-date. It is vital you have an accurate history and understanding of your cost basis as this is the primary driver of your gain/loss.

In addition to this, it would be a good idea to attach a statement to your return explaining:

The nature of the loss

The facts supporting its deductibility under §165(c)(2)

How the amount was calculated (point to form 4684 and ensure your cost basis and fair value calculations are tied up nice and neat in your records)

In the event of an audit, having your records accurate and organized will ensure a smooth and swift process.

As always, consult with your own tax professional and discuss your approach with them. Cheers.

========================================

Example of loss calculation

To summarize the calculation:

Celsius gain/loss = the FMV of “new” assets received - the cost basis of assets lost (not “returned”).

“Returned” BTC/ETH needs to be carved out of both the FMV of assets received as well as the cost basis of assets lost.

Scenario Key Assumptions:

ETH was the only asset owned with a total cost basis of $60,000

Claim amount is $30,000

Class 5 creditor with 79.2% of claim recoverable

Determine what the Preliminary Loss is:

79.2% x $30,000 claim = $23,760 expected recovery

$60,000 cost basis - $23,760 expected recovery =$36,240 preliminary loss

Identify Cost Basis and FMV of "Returned" Assets:

Through inspection of records, "returned" ETH has a FMV of $8,685 and a cost basis of $4,000

Adjust Expected Recovery and Lost Cost Basis for "Returned" Amounts:

$23,760 expected recovery - $8,685 "returned" FMV = $15,075 adjusted recovery

$60,000 total cost basis - $4,000 "returned" cost basis = $56,000 adjusted cost basis

Calculate Claimable Gain/Loss

$15,075 adjusted recovery - $56,000 adjusted cost basis = -$40,925 LOSS.

Note: By "returning" the low cost basis tax lots, the claimable loss is actually larger than the preliminary loss. Strategizing your returned tax lots is a tax optimization opportunity!

========================================

Resources for Help

I have added an entirely new section to the course which covers EXACTLY how to (1) reflect all of this in a tax software so your software stays up-to-date with accurate cost basis and (2) calculate this loss and fill out the appropriate forms to report with your return. The course now contains an excel sheet which will do the calculation for you + access to our private discord for CPA support.

Link in bio: Complete Celsius Tax Guide Course (+How to Reflect in Koinly)

This course is currently 50% OFF for just $399 $199. THIS SALE WILL BE ENDING 3/21!

If you would like to talk with me or my team and want help doing this for you by the 4/15 deadline, feel free to book a consultation below. We offer reduced-cost services to perform the calculation and provide you your applicable forms, we just need you to provide your cost basis and distribution data.

Link in bio to book a consultation!

Happy tax filing everyone,

Justin Zanardi, CPA, Count On Sheep

How to read my liquidation level charts:

- Red lines are 100x high leverage positions

- Yellow lines are 50x mid leverage positions

- Blue lines are 25x lower leverage positions

- Numbers along the top show the top of the range

- Numbers along the bottom show the bottom of the range

- Blue price chart is the price of the asset on #Binance

Now how to use this information:

The exchange will sweep aka "flush" high leverage red lines 99.9% of the time.

The exchange will sweep aka "flush" mid leverage yellow lines 78% of the time.

The exchange will sweep aka "flush" lower leverage blue lines 20% of the time.

The safest and most reliable trade is:

Wait patiently for the lower blue lines to be swept (once a week on average or longer in a bullish trend) and Long or spot buy there. The bottom of the range number is their target.

On the other side, wait patiently for the upper blue lines to be swept (once a week on average or longer in a bearish trend) and Short or take profits there. The top of the range number is their target.

Patience will be rewarded. Trading in the range is extremely dangerous and 90% of traders will lose money.

@martypartymusic@krakenfx@tether Possibly they see it as competition to their CBDCs which they can inflate the supply of at will. Not so with USD backed stables

Update 1: #Bitcoin Quantile Model

You asked for it, and here it is—1,000 lines of code later!

👉 Follow for regular updates.

As a full-time, unpaid Bitcoin researcher, I’m often asked how people can best support my free content.

It’s simple: just engage with and share my posts!

Thank you all for your continued support :)

— PlanC

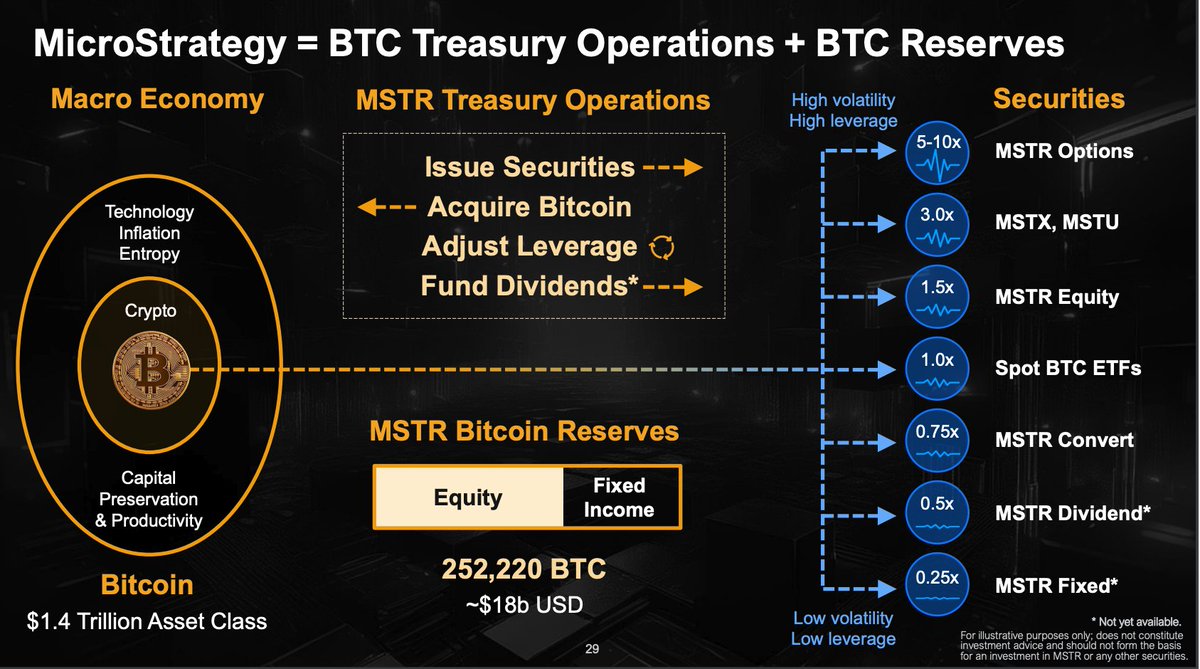

Analysis on $MSTR Preferred Stock Target Raise

*MicroStrategy to Target a Capital Raise of Up to $2 Billion of Preferred Stock*

link: https://t.co/MuXKBTFXOa

(Very long post, trigger warning)

First, what is a preferred stock? If you want a good primer, here's a @PrestonPysh video from 12 years ago going through the basics: https://t.co/862SIn9Ydm

So what is a 'Perpetual' preferred stock, and what might it mean for $MSTR??

TLDR: A perpetual preferred stock is a hybrid financial instrument that combines features of debt and equity, offering fixed dividend payments with no maturity date. It sits between debt and common stock on a company's capital structure, meaning preferred shareholders are paid dividends before common shareholders (no dividends for common shareholders in this case) but after debt holders.

In liquidation, they also have priority over common stockholders. While preferred shareholders usually lack voting rights, they benefit from a more stable income stream and greater security in dividend payments. This structure allows companies to raise capital without diluting voting control (!!!!!), while offering investors a balance of income and relative safety.

The most important thing to understand is that as the preferred stock is perpetual, there is no lump sum principal repayment. There will be an annual dividend, and depending on the rate it is issued at, it is equivalent to pulling forward 10-20 years of buying power.

At a 5% rate, you are essentially pulling forward 20 years of cash.

So lets dive into the profile of preferreds:

Preferred stocks are low volatility, and provide less upside than common equity typically. Banks, Utility companies, REITs, etc.

For some numbers:

Globally, there is 3,488 issues of preferred stock worth over $1m outstanding. On average, $555m per issue, worth approximately $1.93 trillion in aggregate.

More specifically, if we narrow it down to parameters that match where $MSTR likely targets, there are currently 306 securities that check the following boxes:

- Exchange listed

- Perpetual

- U.S. listed issuer

- $378m avg. value per issue

- $115.69 billion in aggregate across 306 issues

- Avg. initial dividend rate of 6.283%

So who is the target buyer for preferred stock?

- Insurance companies

- Pension funds

- Mutual funds

- Banks

Notably, preferred stock can be held as Tier 1 or Tier 2 capital on bank balance sheets under Basel III banking regulations.

Preferred stocks are low volatility, low performance, income generating securities. Shown below is the 60-day historical volatility of a preferred stock index. 10% volatility, or about 1/10th of $MSTR currently.

This will be the first time we are seeing what falls under the '$MSTR Dividend*' category that MicroStrategy teased on its Q3 earnings presentation.

Slide 29: https://t.co/FDkL5lIv9l

However, there is an extremely important advantage that $MSTR has compared to nearly all other preferred issuers:

Volatility. (Not to mention subsequent common stock liquidity, performance, and $BTC exposure)

"The perpetual preferred stock may include features such as (i) convertibility to our class A common stock." - MSTR Preferred Stock filing https://t.co/MuXKBTFXOa

What $MSTR can provide to fixed income investors is an indefinite $BTC backed call option

Let's do some option math:

The value of MSTR calls options with the market implied vol (87%), based on a reference price of $332 per share of $MSTR :

+50% out of the money:

- 1-year expiry: $89.56 (26.36% of price today)

- 5-year expiry: $222.13 (65.4%)

- 10-year expiry: $286.28 (84.28%)

- 20-year expiry: $326.42 (96.10%)

Now, let's do something much MUCH further out of the money, just for the sake of the example.

The value of +500% (!) out of the money calls options with the market implied vol (87%), based on a reference price of $332 per share of $MSTR :

- 1-year expiry: $20.93 (6.16% of price today)

- 5-year expiry: $140.97 (41.50%)

- 10-year expiry: $243.16 (71.59%)

- 20-year expiry: $314.73 (92.66%)

Are you starting to understand how valuable an indefinite call option on a ~90% volatility $BTC beta stock can be for fixed income investors??

The right tail 'risk" is massive for an indefinite call option on a hyper-volatile stock.

The path forward for Saylor and Co. is selling volatility, this time, to preferred stock investors. It's not debt that has to be paid down outside of the annual dividend, and even if we generously assume they pay an average preferred rate of ~6% (I would bet they fetch below average), that would only be $120m per year in dividends on a $2 billion raise, for a company that raised > $15b in equity capital alone in 2024. Non-issue.

We have no idea what the pricing will look like i.e. where $MSTR will place the strike, or what the initial dividend rate will be, so we are just sort of approximating for now.

I can't see $MSTR issuing preferred without a conversion option at some ratio to common stock. After-all, volatility is THE product, and BTC Yield is the Key Performance Indicator. The indefinite optionality is THE most interesting product that MSTR can sell to the fixed income market.

Thus, given the immense theoretical value of the imbedded indefinite call, it might make sense to apply a conversion ratio less than 1.0 for every preferred share to common.

Something like 0.50, or 0.20 conversion into common for every share of preferred for a conversion ratio (i.e 2 or 5 shares of preferred stock convert into 1 share of common stock) could make sense; but again, we can't know until its been priced and placed.

But what we do know is how much Saylor and team emphasize the value of volatility.

"Volatility is vitality."

The treasury team has spoken at length about selling volatility (only through convert issues thus far) and recycling the proceeds back into BTC.

This selling of volatility is how they take the preferred market by storm.

Using our example from above, if an $MSTR call option was striked +500% out of the money (approx $2000/share currently), with 5 shares of preferred converting to 1 share of common stock, the theoretical call option in each preferred share (with a 10-year expiry just for the sake of the math) would be $48.63 of value. For just the option, nevermind the dividend paying component of the preferred share (!!!!). Now, instead of 10 years make it indefinite...

The most interesting thing to watch for will be the provisions that the conversion contains in the preferred offering.

In the past, when $MSTR has issued convertible bonds, the bond has contained all sorts of provisions for the convertible component; a put option imbedded for the buyer of the debt, a call option that $MSTR can redeem if the bonds rise past a certain value after a period of time, etc. I posted some of that theoretical math here: https://t.co/4g9KwIN6Ds

The point of all these provisions is to essentially cap the upside and the downside of the convertible option.

The imbedded 5-6 year call option in the convertible debt is purposefully neutered, because the convert buyers aren't actually interested in the directional exposure.

These convert arb desks are in the business of 'gamma-trading', as they look to delta hedge out their exposure almost instantly. Nevermind exposure for six years, not even six months, weeks or days. These buyers hedge exposure on day 1.

So, they neutralize the value of the call so as to target something like approx 50% delta, so for every $1 billion of bonds that are issued, the convert bond arbitrage desks will short sell something like $500m of equity to lock in immediate gains.

But, the preferred stock could be a bit different.

Given the indefinite nature of the option (read: PERPETUAL preferred), an uncapped call would hold EXTREME value, even if the call was striked laughably far out of the money, given the immense volatility and time value of the option (as laid out above).

Stepping back, the preffered market is just a relative larger scale than converts. For scale, the total size of the convert market in the United States for listed securities is 1,360 bonds worth $302 billion, compared to $572 billion in total for all preferred stock.

However, narrowing the parameters to what $MSTR is looking for: a 0% coupon issue attractive to arb desks is a much smaller market. There is a total of $50 billion of zero coupon convertible debt for listed companies in the United States. $MSTR is already far and away the largest and most active issuer in this market.

Time to level up to a larger pool of capital.

The market for preferred stock in the U.S. is large, and the allocator class is entirely different, with much deeper pockets.

A question to all preferred stock buyers by forced mandate: Would you like exposure to a random tranche of the thousandth largest regional bank, Utility companies, and/or REITs, or would you like low volatility, high sharpe ratio upside exposure to the world's preeminent Bitcoin Treasury Company?

No comparison.

So, what's it all mean?

In essence, $BTC has infiltrated the fixed income market; and the dreaded uncertainty (read: volatility) that every smug TradFi allocator spent the past 15 years making fun of, is the very reason that these $MSTR preferreds will likely be the top performing preferred security in the market before long, just like the $MSTR converts and the common stock have been.

$MSTR bears have no idea what just hit them.

Oh, and don't get me started on the potential BTC Yield here...

END/