Hi all: We are currently looking to hire a full-time Pre-Doctoral Research Assistant for the Department of Finance at the LSE. This position is ideal for students who are considering a PhD in Economics or Finance. More details can be found using the link below!

🚨#finance#conference alert🚨

There are still a few hours left to submit to the HEC-McGill Winter Finance Workshop!

Discuss finance under 15 feet of pure white snow in early March in Québec's Charlevoix region.

Please retweet!

The JFE is doing a special issue on innovations in the financial system! The call for papers is here:

https://t.co/tW0zJoqA7Z

Andreas Fuster will be the guest editor handling the papers.

Hey, we're hiring! HEC Montréal's Finance Department is looking for a tenure-track assistant professor.

Read more here: https://t.co/YDrsfhBJtk and don't hesitate to reach out and chat about the position.

@EmilyAGallaghe1 In “Household Responses to Phantom Riches” we have a triple DiD combining calendar and event time in Figure 6 Panel B https://t.co/NZgBEqe45F

@David__Mathias@benjaminfelix@RationalRemind@FelixFattinger I find that disclosed estimated values by issuers are reasonable - for products with fixed maturities, it’s straightforward to convert them to annual fees. One needs to be more careful with autocalls or callable products.

@David__Mathias@benjaminfelix@RationalRemind@FelixFattinger Longer maturity is typically associated with lower fees and therefore better performance, so you are probably right that these structures are better than what I cover in the discussed research article. Still, without proper understanding of their embedded fees, hard to recommend.

I had a lot of fun talking to @benjaminfelix and @CameronPassmore about structured products - their performance, fees, and the role of attractive headline returns (which often do not translate to attractive realized returns) in investor demand.

https://t.co/6XzXJJ5zr9

Sijoitustiedettä 3:

Yksityissijoittajille myytävät strukturoidut sijoitustuotteet herättävät tasaisin väliajoin keskustelua. Monet näistä tuotteista tarjoavat usein (mutta eivät aina) joko osittaista tai kokonaista suojaa sijoituksesi nimellispääomalle, (1/x)

@benjaminfelix Exactly. The advertised rates of upside returns and downside protection seem attractive. This is what drives investor demand.

Once all the complex features are taken into account, the products are often dominated by listed options.

https://t.co/Ebk58I4PBX

Structured products are designed to offer some degree of principal protection and participation in the upside of risky assets.

This seems like an attractive proposition, but have you ever wondered why the banks are so eager to sell them?

A worthwhile addition to this thread:

A sample of 28,000+ structured products lose money both ex ante and ex post due to their embedded fees.

On average they charge 6–7% in annual fees and lose 6–7% relative to risk-adjusted benchmarks.

https://t.co/HZKqeMjcdC

Hey #finance folks, conference alert! Submit your papers to the 2023 Canadian #Derivatives Institute Conference by May 4th.

To submit, email your paper to [email protected]. That's it. No fees.

The conference is on Sep 14th-15th in Montreal. Last year's program ⬇️

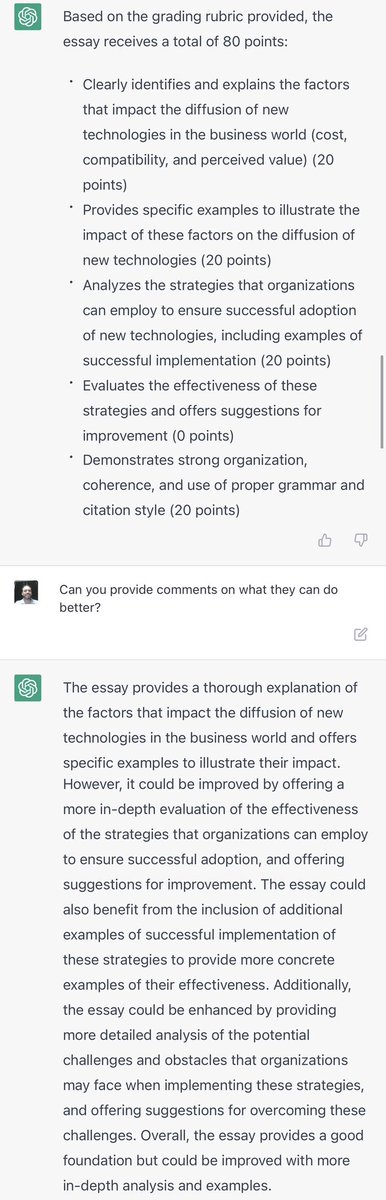

Look, if everyone is worried about students cheating on essays for AI, instructors can just cheat right back.

I asked OpenAI to give me an essay question & make a rubric for grading. I had GPT-3 actually write the essay.

I then had the OpenAI grade the essay & give comments. ✅

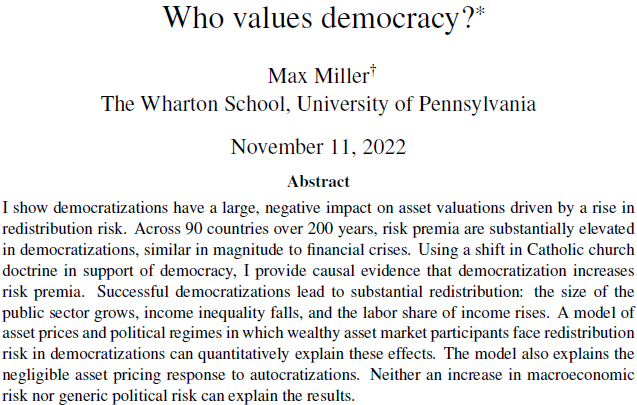

🧵🧪My coauthor Max Miller @mjmill611 has a great JMP

1⃣ Transitions from autocratic to democratic governments are periods of high risk-premia on stock markets.

Why? Established elites fear the redistribution that often follows a successful democratization

https://t.co/HzEd6un6WO

🚨New @Stata package alert🚨

I have finished a complete overhaul of the 𝗽𝗹𝗼𝘁 suite of ultra-fast graphing commands for large datasets!

Updated commands:

✅ use simplified syntax

✅ are downloadable from SSC

✅ come with detailed help files

✅ allow for finer customization