Some of my PnL on long put positions. I know people got heavy bags of OTM put before the sell-off. Lesson from @JeffLia12309881, regularly get some puts when they are cheap, measured by premium short APR on @GreeksLive.

The global macro landscape just underwent a massive regime shift.

Forget everything you knew about the Powell era. The new Warsh-Bessent axis (Fed + Treasury) isn't just managing the economy—they are aggressively weaponizing the U.S. Dollar.

Here is the breakdown of the 2026 framework 🧵👇

1/ The biggest misconception on Wall Street? "Rate cuts = Weak Dollar."

Treasury Sec. Scott Bessent completely dismantled this on CNBC. His doctrine: A strong dollar doesn't need high rates; it needs unbeatable fundamentals.

Even if the Fed cuts, the USD stays king. Why? 👇

2/ The Productivity Premium:

Capital flows to growth, not just nominal yields. By lowering the cost of capital for hyper-productive sectors (AI infra, semis, energy), global money will flood into U.S. equities, artificially propping up the greenback.

3/ "QT for Rate Cuts"

Fed Chair Kevin Warsh is surgically decoupling liquidity from interest rates.

Active QT drains excess institutional reserves (keeping the dollar scarce & credible).

Rate Cuts lower borrowing costs for real-economy CapEx.

No more broad money printing

4/ This is the Greenspan playbook for the AI era. The axis views the AI boom as a historic, disinflationary supply-side shock.

If AI drives massive output per worker, wages can rise and the Fed can cut rates without triggering inflation. Productivity is the ultimate shield.

5/ The Gold Duality:

Short-term: High real yields and Bessent's tactical crackdowns on speculative anomalies will act as a heavy lid on Gold. Expect event-driven dips.

Long-term: De-dollarization & debt expansion mean Gold eventually breaks out. Buy the tactical dips.

6/ The 2026-2030 Playbook:

The mechanical formulas of the past are dead. We are entering a discretionary, trader-friendly "Maestro" era.

Winners: High-quality U.S. Tech, AI Infrastructure, Advanced Domestic Manufacturing.

Losers: EM assets, unhedged short-dollar bets.

End.

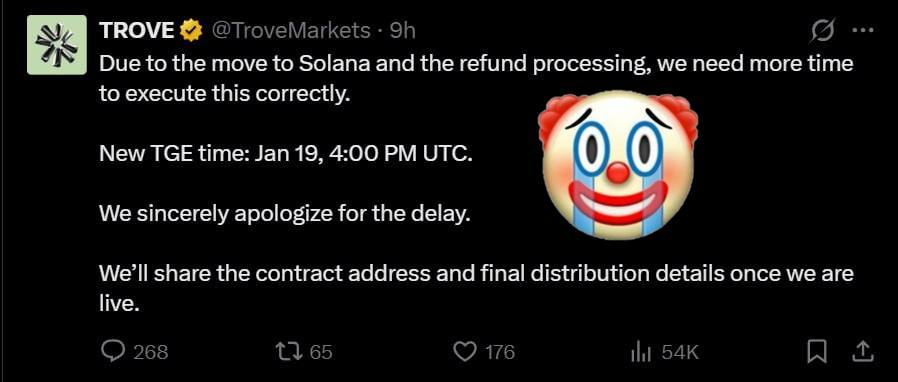

TROVE update (last 24h):

1/ The “nervous LP” keeps TWAP-dumping HYPE. ~75% already sold (~370k HYPE).

2/ TROVE co-founder officially sunset the entire HIP-3 project on Hyperliquid. New plan: “pivot to Solana and build a DEX from scratch” (classic).

3/ TGE delayed multiple times. Latest promise: Jan 19, 4:00 PM UTC.

4/ ~$5.4M from the ICO was moved into a SafeProxy (Gnosis Safe) — no refund contract, no timeline, no explanation. This is roughly the amount they promised to return. Still not refunded. Address: 0x787571c7e0b2fc0bcf64c75bc98bf842eef8107d

Let’s be real:

Angel round funds look fully off-ramped, the remaining HYPE is being dumped, and funds are likely leaving the chain (through XMR?). Rug risk has never been higher.

At this point the devs only decision is whether to:

walk away with ~$2.5M quietly, or

try to grab ~$9M and deal with real legal consequences.

Absolute clowns🤡

airdrops in 2024

> announcement + checker + claim + tge = same day

airdrops in 2025

> potential hint of token

> confirmation of token

> listing in kaito + cookie + bantr + wallchain

> registration date announcement

> miss registration

> allocation reveal day announcement

> allocation reveal

> allocation adjustment

> presale date announcement

> delay the presale

> presale

> tge date announcement

> binance alpha listing

> team and vc selling

> coin 90% dropped

> claim open for community with 30% unlock at tge

> not eligible to claim and going back to @metawin to make it all back

many such cases.

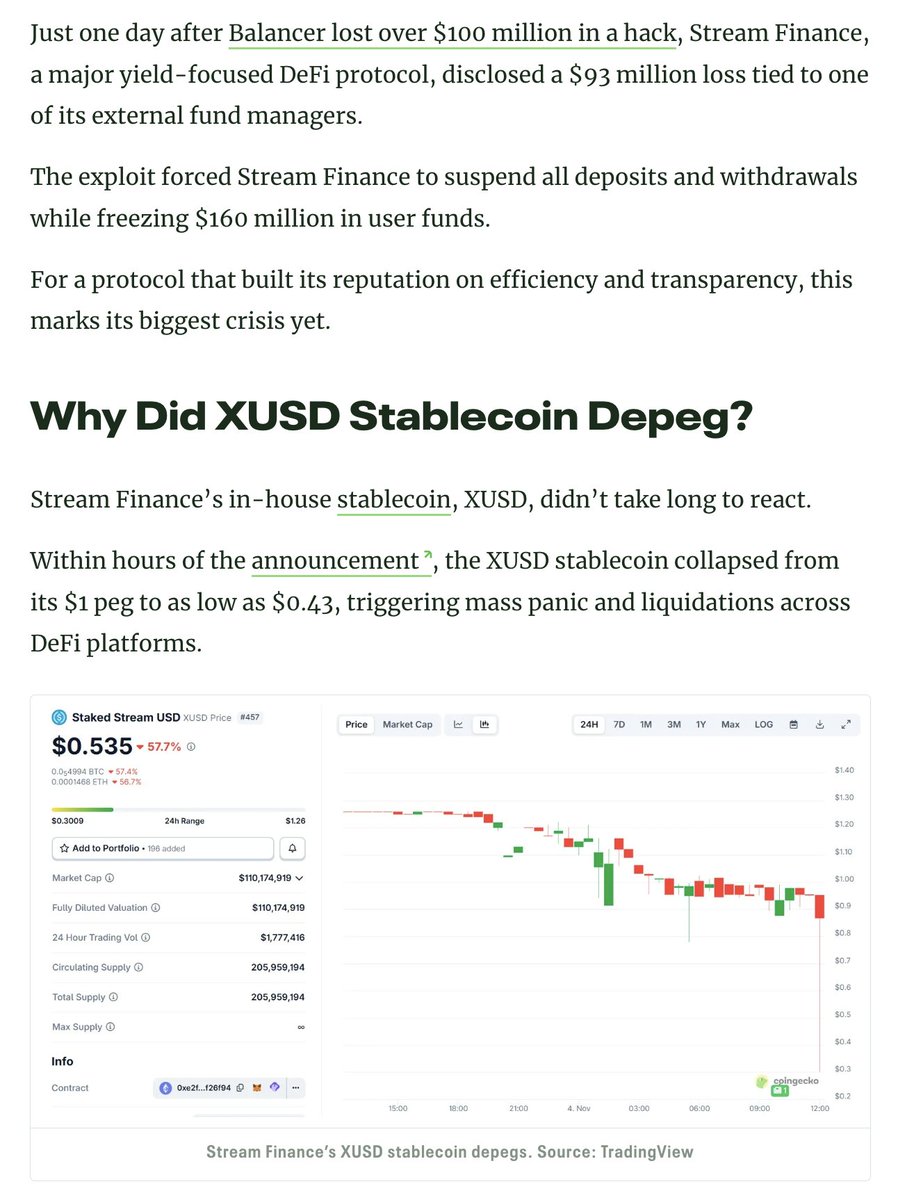

Oct 10th Red Friday: the root cause of Stream xUSD blowing up, the longer version

Stream xUSD is a "tokenised hedge fund" masquerading as a DeFi stablecoin, claiming to run delta-neutral strategies. Now Stream has gone underwater in questionable circumstances. Over the past five years, multiple projects have followed this playbook, attempting to bootstrap their own token through revenue generated from delta-neutral investments. Some successful examples include: MakerDAO, Frax, Ohm, Aave, Ethena.

Unlike many of its true(er) DeFi competitors, Stream lacked transparency regarding its strategies and positions. Only $150M of the claimed $500M TVL was visible onchain on portfolio trackers like @DeBankDeFi. It turned out that Stream had invested in offchain trading strategies run by proprietary traders, and some of these traders blew up, leaving a claimed hole of $100 million in losses.

1. As reported by @CCNDotComNews https://t.co/xl5Lg5UJAY

The $120M Balancer DEX hack on Monday did not play any role in this.

According to rumours (which we cannot confirm, as Stream does not disclose), offchain trading strategies involving "selling volatility" are reportedly involved. In quantitative finance, "selling volatility" (also known as being "short volatility" or "short vol") refers to implementing trading strategies that profit when market volatility decreases, remains stable, or when realised (actual) volatility turns out lower than the implied volatility priced into financial instruments. If the underlying asset's price doesn't move significantly (i.e., low volatility), the options may expire worthless, allowing the seller to retain the premium as profit. However, this approach carries substantial risk, as a sudden spike in volatility can lead to large losses—often described as "picking up pennies in front of a steamroller."

2. More about selling volatility: https://t.co/PFMKglgM7M

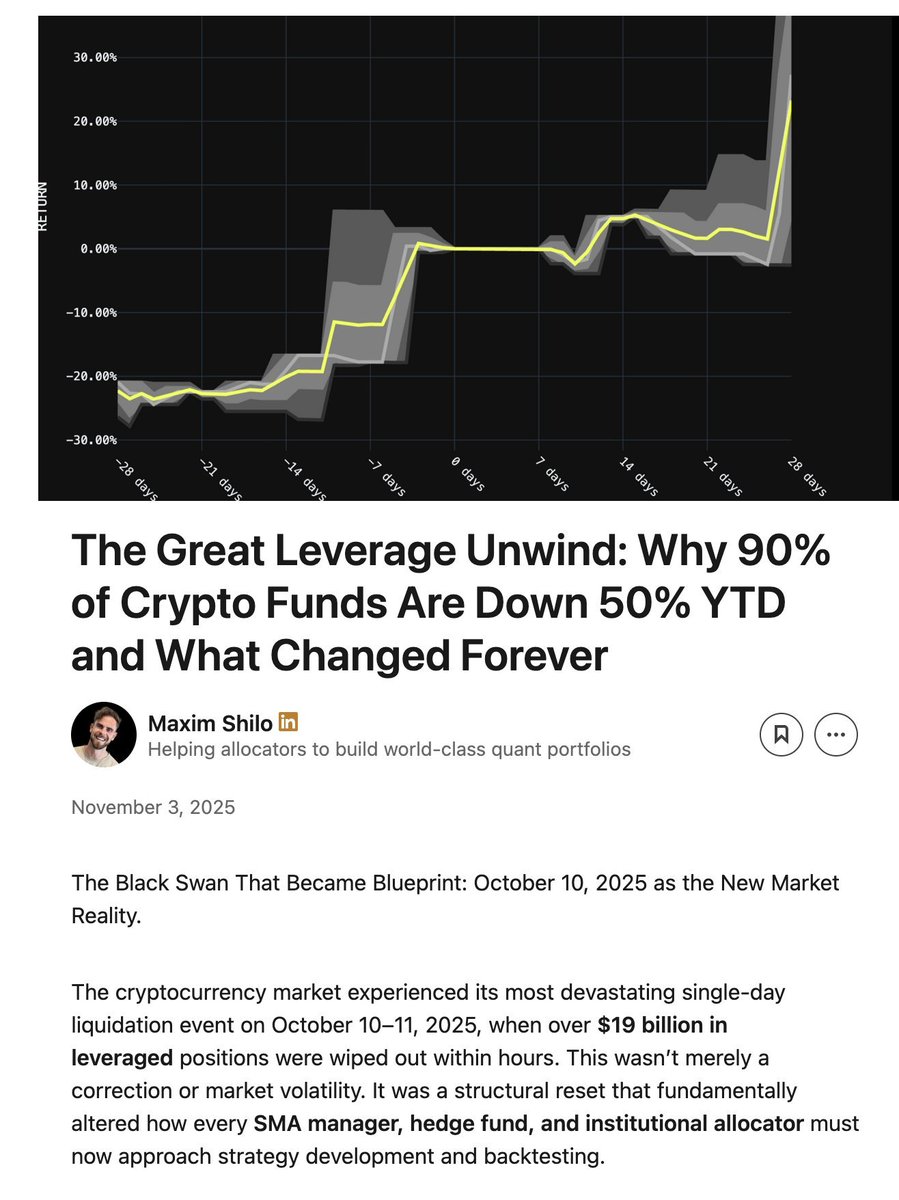

We had such a "spike in volatility" even on October 10th, on the Red Friday. A systematic leverage risk built up across cryptocurrency markets over time, driven by the euphoria surrounding Donald Trump in 2025. When Mr Trump announced new tariffs on Friday afternoon October 10th, all markets panicked, and this panic spread to the cryptocurrency markets. In a panic, it pays to panic first and sell off what's ensured. This sell-off resulted in a cascading liquidation.

As the leverage risk had built up over a long period and taken the systematic leverage to a high level, the perpetual futures markets lacked sufficient depth to unwind and liquidate all leveraged positions smoothly. In this situation, Automated Deleverage (ADL) systems kicked in and started to socialise losses across profitable market participants. This further twisted markets already knee-deep in the madness.

3. What is automated deleverage: https://t.co/oenx9YMmNn

The volatility resulting from this event was a once-in-a-decade event in the cryptocurrency markets. While not unseen, such drops had occurred earlier in the early cryptocurrency markets of the 2016 era. We do not have good data from this era, so most algorithmic traders have based their strategies on recent "smooth volatility" data. As we have not seen such spikes recently, the leveraged positions, even if with very modest leverage of ~2x, were blown up.

There is a good write-up by Maxim Shilo here about what this event meant for the algorithmic traders and how cryptocurrency trading is likely to be permanently changed after the Red Friday:

4. Shilo on how Oct 10th changed crypto algo trading https://t.co/Vys51p2rg3

Now we have the first dead bodies surfacing from the Red Friday events, and Stream got hit.

The definition of a delta-neutral fund is that you cannot lose money. If you lose money, you are, by definition, not delta neutral. Stream promised to be delta neutral, but behind everyone's backs, they had invested in proprietary, non-transparent, off-chain strategies. Delta neutral is not always black and white; hindsight is easy. Many experts would likely deem these strategies too risky to be considered truly delta neutral. Because these strategies could backfire. And backfire they did.

When Stream lost their principal in these bad trades, Stream became insolvent.

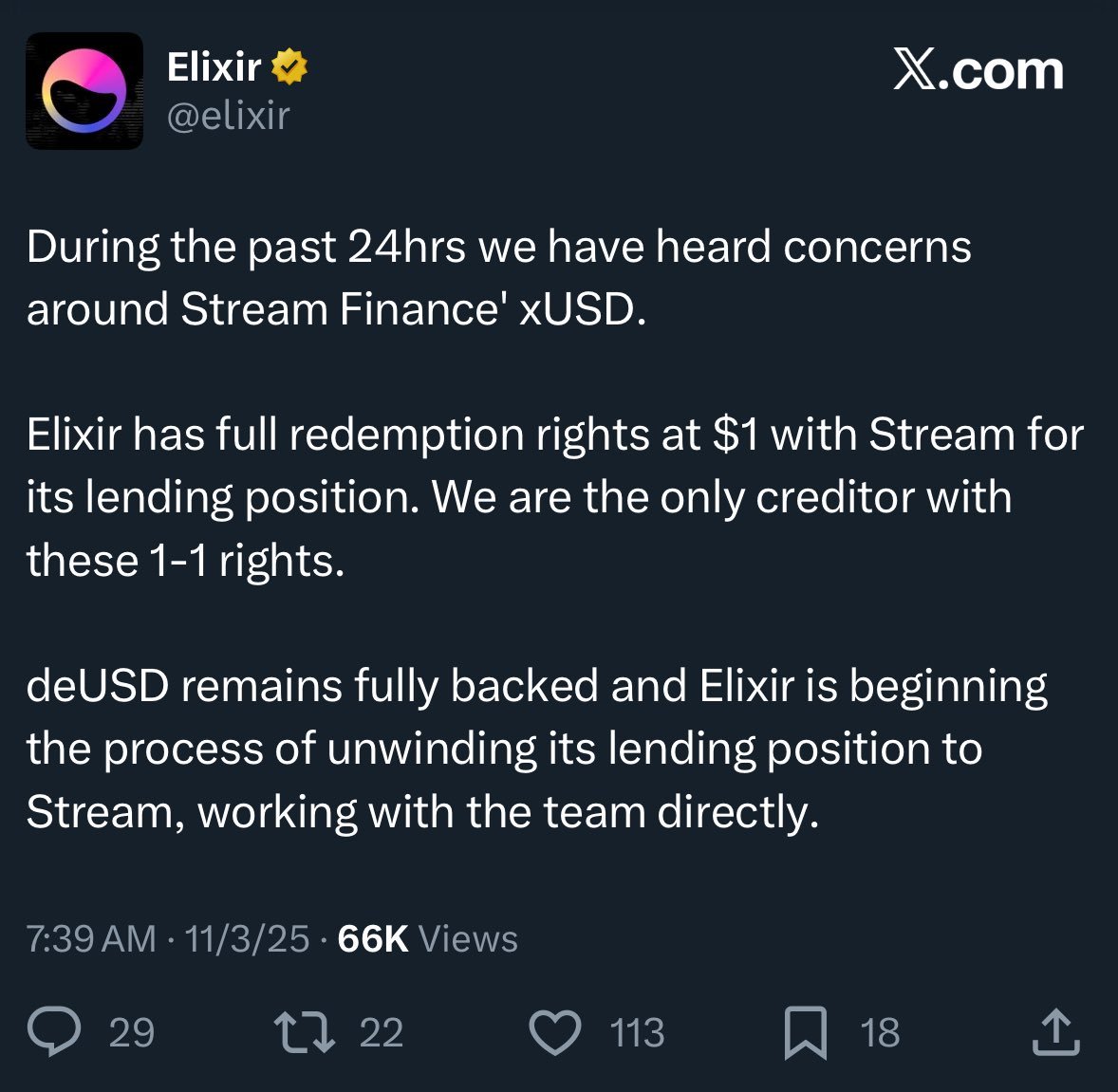

DeFi is risky, and losing some of your money is ok. You can still get your dollars back to 100%, and a 10% one-time drawdown is not devastating if you are earning a 15% annual yield. However, in this case, Stream had also leveraged itself to the hilt by "recursive looping" lending strategies with Elixir, another stablecoin.

5. What is recursive looping: https://t.co/54hh5vpbdK

6. How did Stream lever up and how much: https://t.co/rwES6JpNqo

To add to the insult, Elixir claims "seniority" based on an offchain agreement for the recovery of their principal in the case Stream goes bust. This would mean Elixir receives more money back, while other DeFi investors in Stream receive less (or no) money back.

Due to a lack of transparency, recursive looping, and proprietary strategies, we do not actually know the losses incurred by Stream users. The Stream xUSD stablecoin price is currently trading at $0.60 per dollar.

Because this was not disclosed to these DeFi users, many of these users are now extremely pissed off at both Stream and Elixir: not only losing money, but losses are socialised to ensure rich Americans from a Wall Street background keep the profit.

This event also affects lending protocols and their curators:

"Everyone who thought that they were lending on Euler against collateralised positions was literally engaged in uncollateralised lending by proxy" -Rob from @infiniFi.

Furthermore, since Stream did not have transparency or onchain data on its positions and profits and losses, in the light of these events, users began to suspect that Stream was fraudulently appropriating users' profits for the management team. Stream xUSD stakers rely on Stream self-reported "oracles" for their profit, and third parties cannot confirm if any calculations are correct or fair.

How to tackle this?

Incidents like Stream are avoidable, especially in a young industry like DeFi. The rule "high risk, high reward" always applies. However, to use this rule, you must first understand the risk: not all risks are made equal, some of risk can be unnecessary. There are several reputable yield farming, lending, and stablecoin-as-a-tokenised-hedge-fund protocols that are transparent about their risk, strategies, and positions.

@StaniKulechov from @aave discusses DeFi curators and when the excessive risk taking may happen here:

7. Stani on the recent DeFi risk realisation events https://t.co/5ToOeK0Hf3

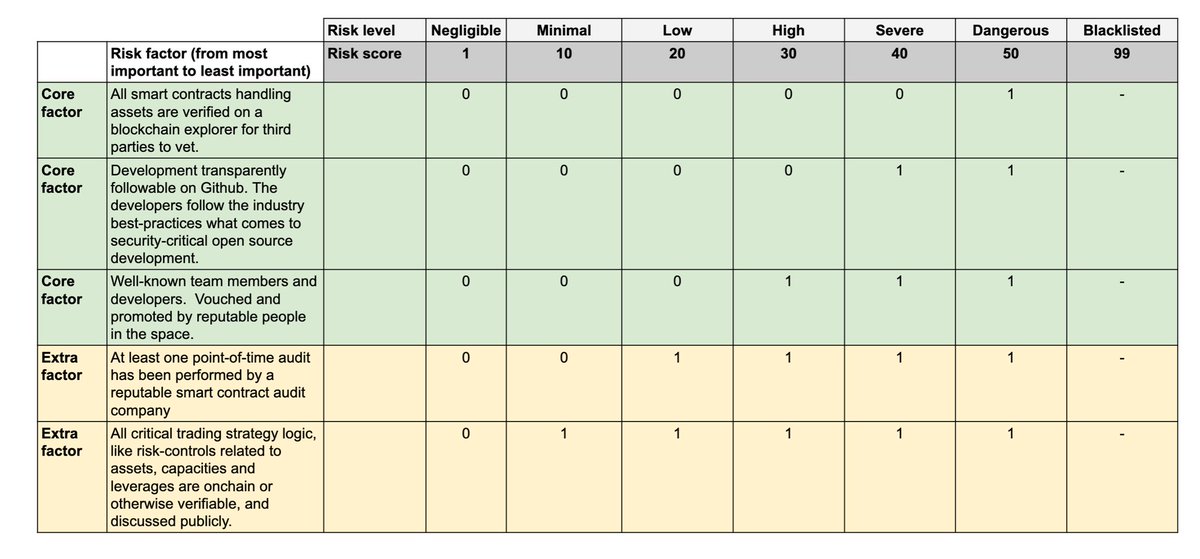

To make the difference between "good vaults" and "bad vaults" more obvious, at Trading Strategy, we have begun publishing our own Vault Technical Risk Score in our DeFi vault report.

8. Read the announcement about Vault Risk Framework here: https://t.co/MflrFKmUrW

The technical risk refers to the likelihood of losing money invested in a DeFi vault due to poor technical execution. The Vault Technical Risk Framework offers a straightforward tool for categorising DeFi vaults into higher- and lower-risk categories. The technical risk score does not get rid of market risks like bad trades, contagion or so on, but it guarantees that a third party can assess those risks.

With better information available for DeFi users, capital allocation will shift towards good actors, and incidents like Stream will be less severe in the future.