Check the latest self-custodial open strategies here: https://t.co/GDZBBsXQfb

The Open Strategies #trade automatically on #DEXes and #DeFi protocols. Trading capital is in on-chain vaults so you can withdraw your crypto whenever you want.

Portfolio margin is technical, but simple, and it quietly decides how much capital a trading firm wastes.

The most widespread approach in crypto, position-level margin, looks at each trade on its own and requires you to post collateral against each one. So a firm long BTC on one venue and short BTC perps on another, a book that's close to flat, gets charged for both legs as if they were separate bets. The better hedged you are, the more you get penalized. That's backwards.

Portfolio margin fixes the lens. It stress-tests the whole book across price and volatility moves, then sizes margin to the risk that's actually left after offsetting positions cancel out. Every TradFi prime broker has margined equities this way for decades.

The catch is that TradFi portfolio margin operates within a single clearinghouse, where everything nets out because it all sits in one place. Crypto has no shared clearinghouse. Your positions live across CeFi and DeFi venues that can't net what they can't see. Building one risk view across all of them is the hard part.

That's what @sparkdotfi is running on @ArkisXYZ .

The options market has started to price in more risk in the short term than in the medium term. This is unusual because we would expect for uncertainty to increase along with the time horizon.

There is historical precedent for this, and bears are not going to like it. Given that risk is sufficiently hedged, the market usually rallies …/

KyberSwap 🤝 @o2dotapp

KyberSwap has integrated o2 as a new PMM liquidity source, bringing deeper liquidity and better rates for traders.

Just trade on KyberSwap.

ForgeYields USDC is currently earning 12% annualised.

@ForgeYields allocates to looping / leveraged lending.

Pendle, Curve, Balancer, concentrated liquidity, and direct lending opportunities based on their Hallmark risk engine.

https://t.co/hZ5hp02R05

Trading Strategy is heading to New York for @Vault__Summit, Stable Summit and Agentic Finance Summit.

Calling for #quants, #assetmanagers, #Alagent developers, #vaultcurators, and #DeFi protocol teams! Meet us for live demos and see our latest datasets

https://t.co/DrFaeBoXpS

Edge and hedge on Hyperliquid by @blothecap is now the top five vault across 3000+ DeFi vaults.

Lifetime ann. returns ~80%.

"Running a quantitative delta neutral long, short strategy with a leverage of around 3x."

https://t.co/Qz5vwsLhlB

🌊 Lagoon v0.6 is live.

Our largest release since launch — 11 new capabilities, fully audited, shaped by managers running 120+ vaults across 18+ chains.

Three themes: deeper security, manager autonomy, strategy modularity.

Here's what ships 👇

v0.6 is live, our biggest release since launch!

Since the first release in October 2024, we’ve been actively gathering feedback from vault operators and asset managers running 120+ vaults across 18+ chains to build the best possible product.

This update delivers exactly that: better UX for LPs with the sync redeem feature, deeper security with NAV guardrails, greater manager autonomy, opt-in compliance features, and true strategy modularity. All shaped directly by the teams using Lagoon every day.

Audited by @Nethermind and @trailofbits.

(Claude Opus 4.7 ran a pre-audit too. It approves. 🤖)

Huge thanks to everyone who contributed. Onward 🌊

K Pool vault on Lighter keeps grinding up

Vault description: Discretionary MTF low lev set ups on "tokens in play" through a strict selection criteria. Disciple of orderflow, price action, market structure and volume.

https://t.co/qDI5Ox87EH

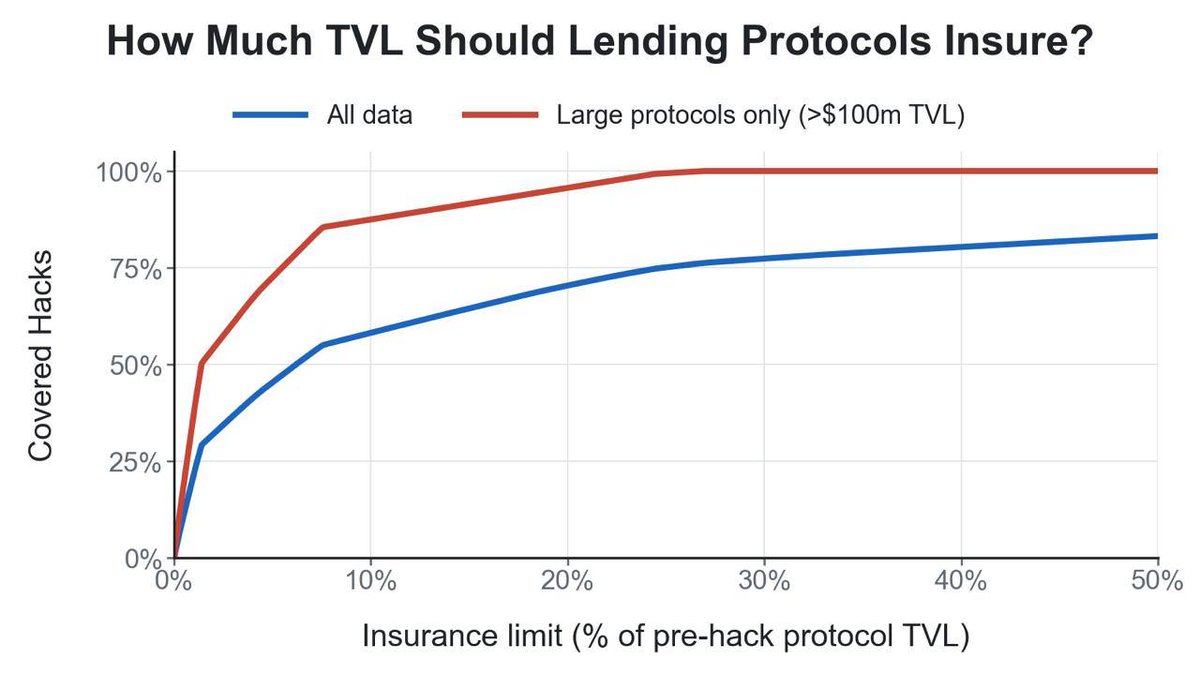

How do you get DeFi insurance for under 20bps?

It all relates to how much insurance protocols should actually pay for per TVL.

From shopping around, I can confidently say that the price in the market being offered is between 1.5-4% on lending and borrowing crime insurance.

"but.. but.. you said the expected value is 3bps"

yes but the insurers are:

1) skittish about cover, and

2) they have to take into account Expected Shortfall, and given no-one is buying cover they have pretty high concentrations on what they write.

How the hell do you get to <20bps when you're paying 2% ?

Start with defn of protocol crime insurance for hacks:

- exclude bridge-related events

- Solana and EVM

- Protocol exploits or oracle manipulation involving a theft, a few others things too but it's PROTOCOL stuff

Lets also give an explicit counter-example...

START EXAMPLE SIDE QUEST >>>

As a concrete example, most people in crypto talk about the "Aave hack". @aave didn't get hacked by any stretch of the imagination, you would definitely know if they did.

@aave had a credit event. A collateral lost its peg because of an error in technical configuration. That error was propagated from a criminal cyber attack / hack on a bridge, who had also made an error in a recommendation to their client on their DVN setup.

This is not a protocol hack of @aave and no crime insurance policy covering Aave would pay out for this.

This is a credit default risk and protected by a Credit Default Swap.

Where it gets confusing is that Aave's DAO appoints risk managers that are supposed to price the margins for collateral. However, you spin it though, the risk manager missed a credit event and the protocol remained resilient.

What should ideally have happened is @aave have umbrella, collateral have Crime & E&O coverage and Bridge has Crime & E&O coverage. Insurers then get triggered by both collateral and bridge and then sue each other to decide who pays what %.

There could be some argument that the risk manager might have some liability but it's going to be hard ground to justify because they have a framework, it's very public, they published their homework and we all deposited in a non-custodial fashion.

<< END EXAMPLE SIDE QUEST

Getting back to the quant stuff.

When you look at all the data of the 600 lending/borrowing protocols and 100+ hacks, especially on the larger protocols (of which there are nearly 20 hacks now) you notice something kind of interesting.

The data suggests that the majority of protocols get pinged for a low proportion of their overall TVL. In fact the largest protocol hack was @eulerfinance and even that zero-day took about 63%

There is a myth that is misunderstood, by even some brokers I discussed this with this morning, that hacks are total loss scenario. It might be for random off-the-book hedge funds but in the public and open-source Ethereum / Solana landscape we see all and it says the losses are varied but on average a small ratio.

In fact you would cover 73% of all losses if you had just 5% of the TVL insured.

Now hold up.

If quotes in the market are around 1.5-4% and we can insure a large chunk with just 5% of cover then the passthrough to lenders is 1.5-4% / 20 per unit of TVL

However, Increased Limits Factors kick in

(honestly I don't even know if that's the correct acronym expansion, I just know it as "ILF")

Insurers will generally insure blocks and create a "tower" which means that those at the bottom of the tower have higher risk. If the bottom of the tower is priced at 1% then the next guy might be happy to do next-loss cover at 90bps which implies an ILF of 90/100 = 90%

On average ILF can vary but I think it's conservative to estimate around 95-99%. One of my broker buddies has also said there is a commercially minimum rate around 60bps so no matter how high the tower, you'll pay at least 60bps to get someone out of bed on each tower chunk.

When you look at how this scales, on $1b of coverage you would buy actually just $50m of cover which would cover 73% of all losses.

You would pay between 120.4bps and 325bps on that $50m

You would pass through ONLY 5-19bps though to lenders.

From a protocol perspective this is a total no brainer and insane that people don't do it more.

The caveat? And why I care.

"Unpermissioned DeFi is broadly uninsurable", a well known DeFi broker.

Plug @KeyringNetwork...

Lucky for you fuckers we charge no money on this and Keyring can onboard users with ZKPs in 3-30 seconds without selfies or passports. And most importantly, there is no backend review process, so you remain fully decentralised without triggering "points of control" for regulators.

If you want to get insured, it's likely you'll want to look at putting a door lock on the think you insure to get a non ridiculous quote. Or get a quote at all.

@reisnertobias@GrowiHF Currently, $20B is earning better than the US treasury note rate in DeFi vaults

82% of vault TVL is earning better than US bank savings rate average

https://t.co/mrbuOwmx02

Building an AI trading agent is still way harder than it should be: Fragmented docs. Poorly structured APIs.

We’ve been investing heavily in the integration stack to fix that. If you’re operating agents, GMX is officially your execution layer. ⬇️

1/2

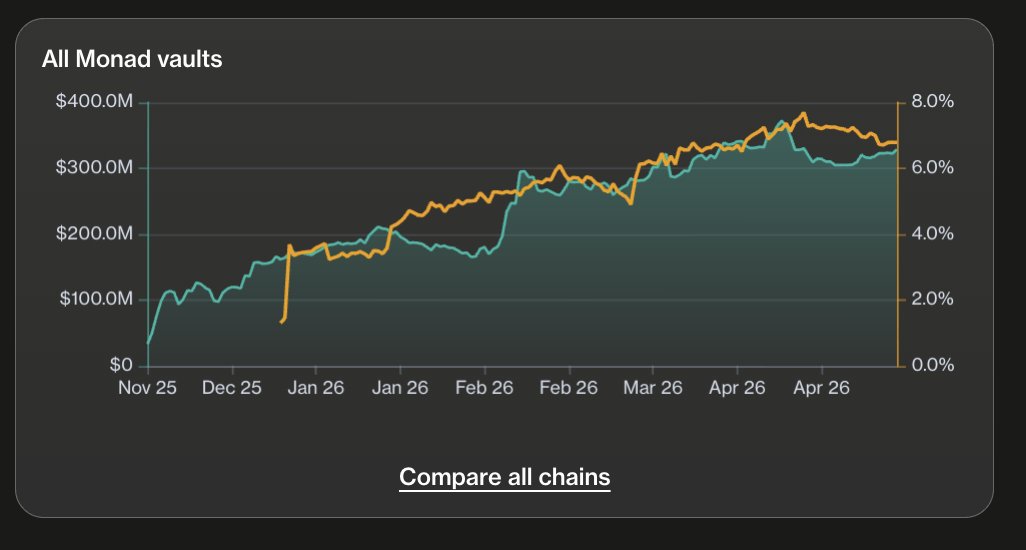

The @alphagrowth1 AUSD is the number one vault on Monad at the moment.

This Euler vault has a 16% historical monthly return.

Unlike more traditional Euler vaults, this vault does the leverage on the Balancer AMM.

BPT is the liquidity provider (LP) token issued by Balancer, a decentralised automated market maker (AMM) on Monad and other blockchains.

https://t.co/VFCK5wNSnA

The vaults on @monad is the only chain where the yield has been going up for the last few months

https://t.co/Ccgl83VmnI

Both TVL and TVL-weighted average returns are increasing