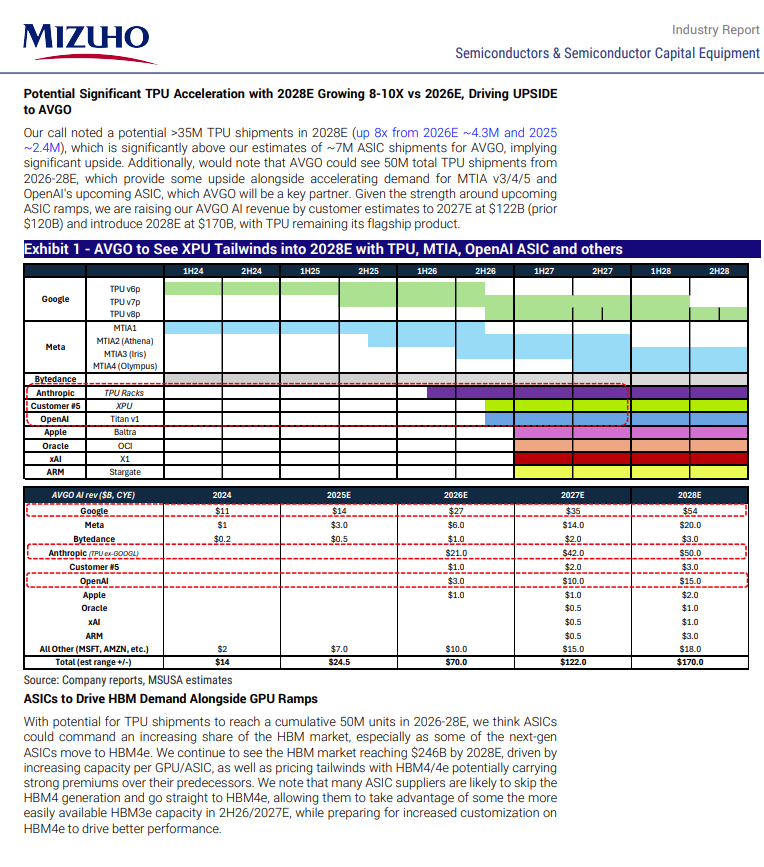

Mizuho ASIC channel checks: pounding table on $AVGO

"potential >35M TPU shipments in 2028E (up 8x from 2026E ~4.3M and 2025 ~2.4M), which is significantly above our estimates of ~7M ASIC shipments for AVGO"

"We believe OAI ASIC is in development with 10GW AVGO project (Nexus) adding to TPU/MTIA/ARM roadmap."

"Our call noted $ARM AI ASIC chip development ongoing as we continue to expect a launch in late-2026E/early-2027E"

" $MU : With potential for TPU shipments to reach a cumulative 50M units in 2026-28E, we think ASICs could command an increasing share of the HBM market, especially as some of the next-gen ASICs move to HBM4e"

this is one of the first very very early glimpses of ai’s impact on the supply side of the economy.

the entirety of the western capitalist apparatus relied on allocation of scarce resources towards production of goods & services, but as the inputs required continue to go to ~zero for both bits & atoms (this will take longer), it’s likely the idea of pricing power will fade away over time (esp if there is real self replication).

& if pricing power fades at scale, capitalism as we know it is roughly over. or on the flip side, in certain areas there might be one entity who has all of the pricing power due to some glitch (exclusive access to a single input, etc). either way you might get edge outcomes over the long horizon where most things become near free but few things become insanely expensive.

1/5

I'm a cardiologist. I have spent twenty years watching cholesterol destroy arteries, trigger heart attacks, and kill people I care about.

Today, Eli Lilly presented data that may begin to end that era.

VERVE-102. A single infusion. One dose. It uses base editing to permanently turn off the PCSK9 gene in your liver.

Presented today at the European Atherosclerosis Society Congress:

88% reduction in PCSK9.

62% reduction in LDL cholesterol.

Sustained up to 18 months.

No treatment-related serious adverse events.

One infusion. Not daily pills you forget to take. Not monthly injections. One dose — and your cholesterol may stay low for the rest of your life.

Wrapped up the global @EQDerivatives conference.

Recap:

Option selling and call overwriting programs continue to grow rapidly as they fit neatly into the modern adviser suite selection process. Institutions and advisers continue to gravitate toward products that generate distributable yield and smoother return profiles. Dealers are feasting off the persistent price insensitive and largely dogmatic flows that naturally emerge from these programs.

Buffered ETFs are scaling at an incredible pace and are quickly becoming another dominant yield enhancement vehicle within adviser platforms. The growth trajectory and investor appetite are substantial. Similar to covered call products, these structures create large, recurring, price insensitive flows that dealers are increasingly monetizing and positioning around.

QIS allocations continue to get larger across institutional portfolios. A significant portion of that participation remains yield generating in nature. But people are wary that it’s just all a game of elegant backtests and poor live results.

FLEX options are growing massively in size. Although they function somewhat like quasi structured products due to their customization, dealers and hedge funds are becoming increasingly creative in how they utilize them for hedging. It feels like only a matter of time before FLEX volume meaningfully explodes from current levels.

Classical relative value signals appear to be decaying at a rapid pace. Many of the traditional vol arb relationships that worked for years are becoming increasingly noisy. The industry as a whole has become much more sophisticated in sourcing and implementing newer RV frameworks, while many legacy shops appear to have been left behind structurally.

There are still many fantastic managers across L/S equity, commodities, macro, and other areas. However, it is becoming increasingly difficult to allocate to high quality volatility hedge funds. Many of the strongest vol managers have already been absorbed into pod structures at large multi manager firms. As a result, there is a growing sense of adverse selection among the remaining standalone vol managers. Hedge fund database performance numbers across the vol space seem to reinforce this dynamic as well.

There is now such a large oversupply of volatility selling coming from U.S. structured product issuance, particularly in the 1Y to 2Y part of the surface, that larger trading firms are actively building specialized teams specifically designed to capture and warehouse that edge.

Despite nonstop geopolitical tension and increasingly unstable macro headlines, the overwhelming institutional appetite still remains yield focused. In practice, that largely translates into continued structural short volatility exposure across the system. The demand for income generation continues to dominate discussions.

Insurance companies remain, by a very wide margin, some of the largest volatility traders on the street. The amount of Vega sold through the VA market has become staggering. Simultaneously, the RILA market has grown into hundreds of billions of dollars in assets and has become one of the fastest growing insurance product categories in the United States over the last several years.

A meaningful portion of the industry does not appear to be hedging tenor for tenor in this environment. Instead, we are increasingly seeing shorter dated puts being utilized as substitutes for longer dated downside protection. In a scenario where equities continue grinding lower over time, that mismatch could become extremely problematic.

Portable alpha appears to have fully repaired its reputation. A growing number of large institutions are revisiting and implementing portable alpha frameworks as a portfolio optimization tool. In a world where passive investing continues to dominate traditional sources of outperformance, institutions are increasingly looking for ways to layer differentiated alpha streams on top of core beta exposure

Every variant of Monte Carlo Tree Search faces the explore-exploit tradeoff: pick the branch that looks best right now, or test new branches?

Algorithms like PUCT, used in AlphaGo, score each move with two competing terms.

One is how good a move looks based on your exploration up till now. The other is a novelty bonus that rewards moves you've not visited much.

The neat thing is that, over time, the term dominating the overall score shifts automatically. The algorithm hands off from 'explore' to 'exploit' all on its own.

@ericjang11 explains how it works:

CEREBRAS UPSIZES IPO TO $4.8B AFTER 20X DEMAND

$CRBS filed to sell 30M shares at $150-$160 each, up from 28M shares at $115-$125.

At the top of the new range, the AI chipmaker would raise roughly $4.8B, compared with $3.5B under the prior terms.

Reuters says the IPO drew orders for more than 20x the shares available.

The deal is set to price May 13.

Cerebras makes AI inference chips and lists Amazon and OpenAI among customers.

This is the strongest public-market demand signal yet for a pure-play AI chip IPO.

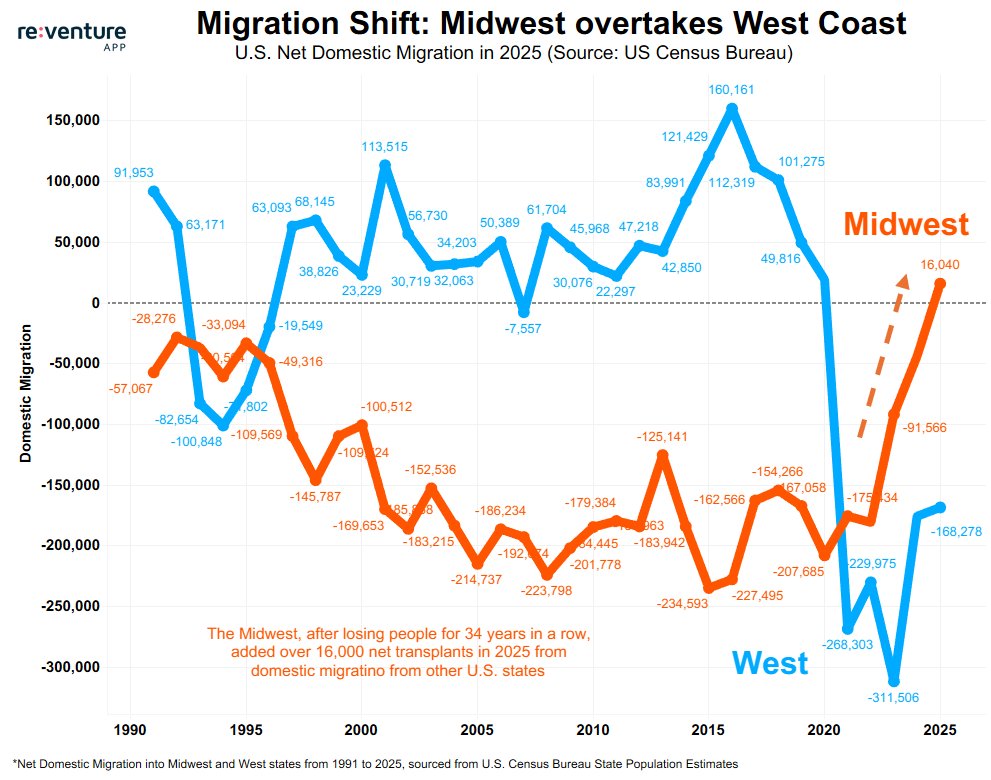

A new migration shift is happening in the U.S.

The Midwest, after losing people for 30+ years, is now surging. With +16,000 migration in 2025.

On the flip side, people are leaving the West Coast.

California continues to lose people, and the losses are spreading to other West Coast states.

And the Midwest seems to be gaining. Likely due to its affordability, climate resilience, and improved job prospects due to manufacturing onshoring.

If this trend continues, it has the potential to dramatically reshape the U.S. Housing Market.

Download to see more migration data: https://t.co/pLvj026xCj

This is what SaaS bears think is happening and it's why near-term resilient fundamentals, buyback announcements, and AI pivots are producing uninspiring bounces in stocks like $ADBE

Six years ago it we thought it'd take 10 million qubits to break any Bitcoin public key.

Four years ago it was 2 million qubits.

16 hours ago Google published a paper showing it can be done with 500,000 qubits in 20 minutes.

Race is on. Top prize?

$76 billion: Satoshi wallet

I feel like I’ve been talking too much about myself, so to shift the conversation back to memory…

It looks like Samsung’s semiconductor division may genuinely be heading toward a strike. The union is demanding a performance bonus equal to 20% of operating profit, while management is holding firm, saying it cannot remove the cap on bonuses.

The union seems willing to do whatever it takes to eliminate the bonus gap with SK Hynix. There is a real possibility that Samsung’s memory production lines could actually be halted.

Once a line is shut down, it can take as long as two months to restart. The losses could amount to tens of billions of dollars.

That would be good news for Samsung’s competitors. In the near term, SK Hynix and Micron look like the obvious beneficiaries.

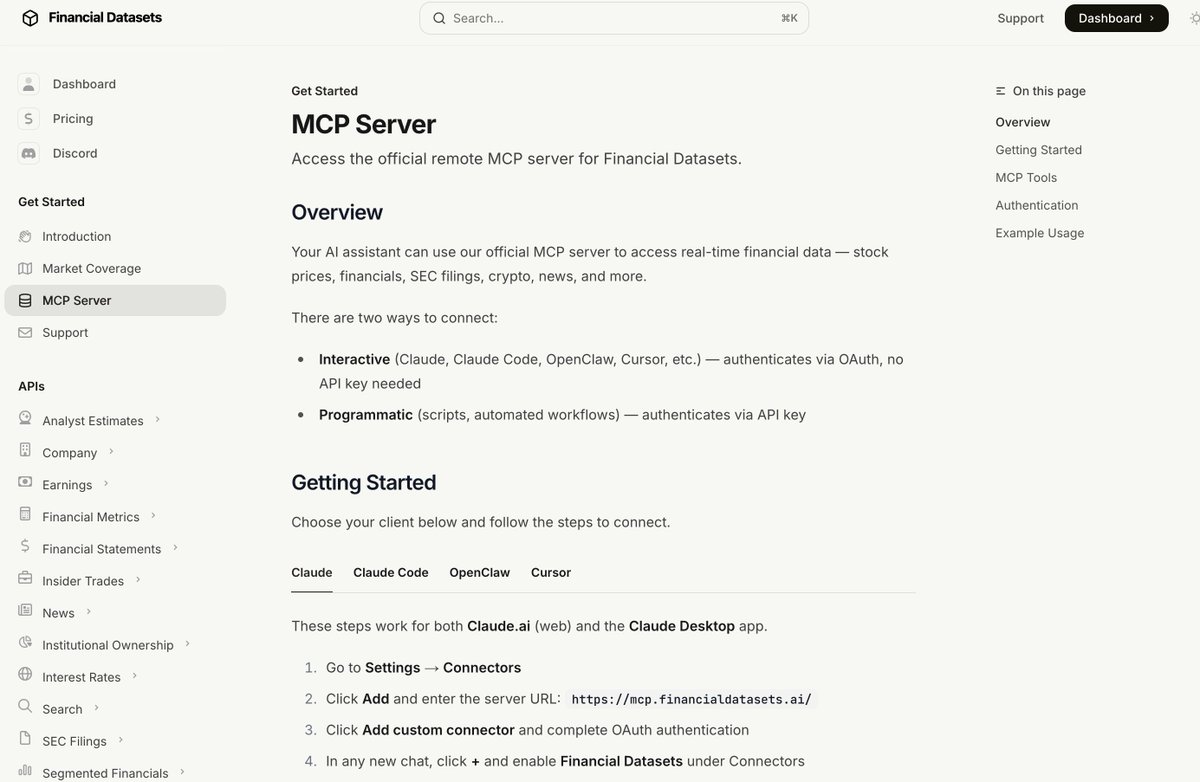

Claude can now directly access Financial Datasets through MCP.

You can ask questions in natural language and access income statements, balance sheets, cash flow statements, and more for 17,000 companies over the past 30 years.

Too bad Bloomberg isn’t publicly listed.

Back in the day, Goldman Sachs was the premier Wall Street bad guy. The investment bank attracted endless scrutiny of the supposedly conflicting and asymmetric arrangements that powered its broker dealer operations. Key among these were its primary dealer arrangements. Today, that attention has shifted to market makers like Jane Street. Key to the perceived conflict is the privileged role these institutions often play as “authorised participants”.

The AP term was entirely obscure to most journalists before I started writing about it, and frequently dismissed as an operational irrelevance. “Nothing to see here”.

In reality it represents a new type of primary dealer relationship. Except there is a difference. While the Goldmans of this world operated as de facto APs to the New York Fed, modern market makers operate as APs to thousands of ETFs, which (when you deconstruct them) amount to pseudo miniature currency board that back their “units” (we used to call tokens units) with a plethora of different assets, swaps and other mechanisms.

All these entities (including the NY Fed) have one objective. Keeping their units pegged to some sort of index.

ETFs mostly track stock and market indices. Par (aka “the peg”) equals the index minus the management fee. How they achieve that is often not as transparent as you would think.

The NY Fed’s objective is ensuring its tokens deliver returns commensurate with an interest rate that fluctuates based the decisions of its FOMC.

The difference is that its rate shifts based on the price externalities over supply of their own units create in the market even if they achieve their target.

The same thing does not happen with ETFs. The externalities are ignored and available to market makers like Jane Street to exploit.

The analogy isn’t that ETFs are the Fed. It’s that both systems issue “units” to maintain a peg. When unit creation becomes a structural funding loop rather than a marginal arbitrage, price externalities accumulate somewhere. The question isn’t whether the trades close overnight. It’s whether the systemic supply effect of constantly reopening them alters price formation over time — and who captures that transfer.

Holy shit… Your anonymous internet identity can now be unmasked for $1 😳

Not by the FBI. By anyone with access to Claude or ChatGPT and a few of your Reddit comments.

ETH Zurich and Anthropic just dropped a paper called “Large-Scale Online Deanonymization with LLMs” and the results are the most alarming privacy research I’ve read this year.

They built an automated pipeline that takes your anonymous posts, extracts identity signals, searches the web, and figures out who you are.

No human investigator needed. Fully autonomous. Works on Hacker News, Reddit, LinkedIn, even redacted interview transcripts.

Here’s how bad the numbers are.

On Hacker News users: 67% identified correctly.

When the system made a guess, it was right 90% of the time.

On Reddit academics posting under pseudonyms: 52%.

On scientists whose interview transcripts were explicitly redacted for privacy: 9 out of 33 still got unmasked.

The pipeline works in four steps they call ESRC. Extract identity signals from your posts using LLMs.

Search for candidate matches using embeddings across thousands of profiles.

Reason over top candidates with models like GPT-5.2. Calibrate confidence so when it does guess, it’s almost never wrong.

The classical deanonymization method from the famous Netflix Prize attack? Nearly 0% recall across every test.

LLMs didn’t just improve on old techniques. They made old techniques look like toys.

When they scaled to temporally split Reddit profiles, matching a user’s old posts to their newer ones across a full year gap, the pipeline hit 67% recall at 90% precision and 38% recall at 99% precision.

Meaning even a year of changed interests and different conversations wasn’t enough to hide.

More reasoning compute = better deanonymization. High reasoning effort doubled recall at 99% precision in some tests. As frontier models get smarter, this attack strengthens automatically. Every model upgrade is a privacy downgrade.

What makes it nearly impossible to defend against: the pipeline splits into subtasks that all look benign. Summarize a profile.

Compute embeddings. Rank candidates. No single API call screams “deanonymization.” The researchers themselves say they’re pessimistic that safety guardrails or rate limits can stop it.

Their conclusion is blunt: “Users who post under persistent usernames should assume that adversaries can link their accounts to real identities.” And it extrapolates.

Log-linear projections suggest roughly 35% recall at 90% precision even at one million candidates.

Every throwaway account. Every anonymous forum post. Every “nobody will connect this to me” comment.

It’s all searchable micro-data now. And the cost to run the full agent on one target is less than a cup of coffee.

Practical anonymity on the internet just died. The paper killed it with math.

I spent 100 hours over the past week researching, writing and editing the piece we just put out.

It’s a scenario, not a prediction like most of our work. But it was rigorously constructed, dismissing it outright requires the kind of intellectual laziness that tends to get expensive.

And we’ve released it for free. Hopefully you enjoy it.

https://t.co/YK8E11GcDU