How to setup your Claude code project?

TL;DR

Most developers skip the setup and just start prompting. That's the mistake.

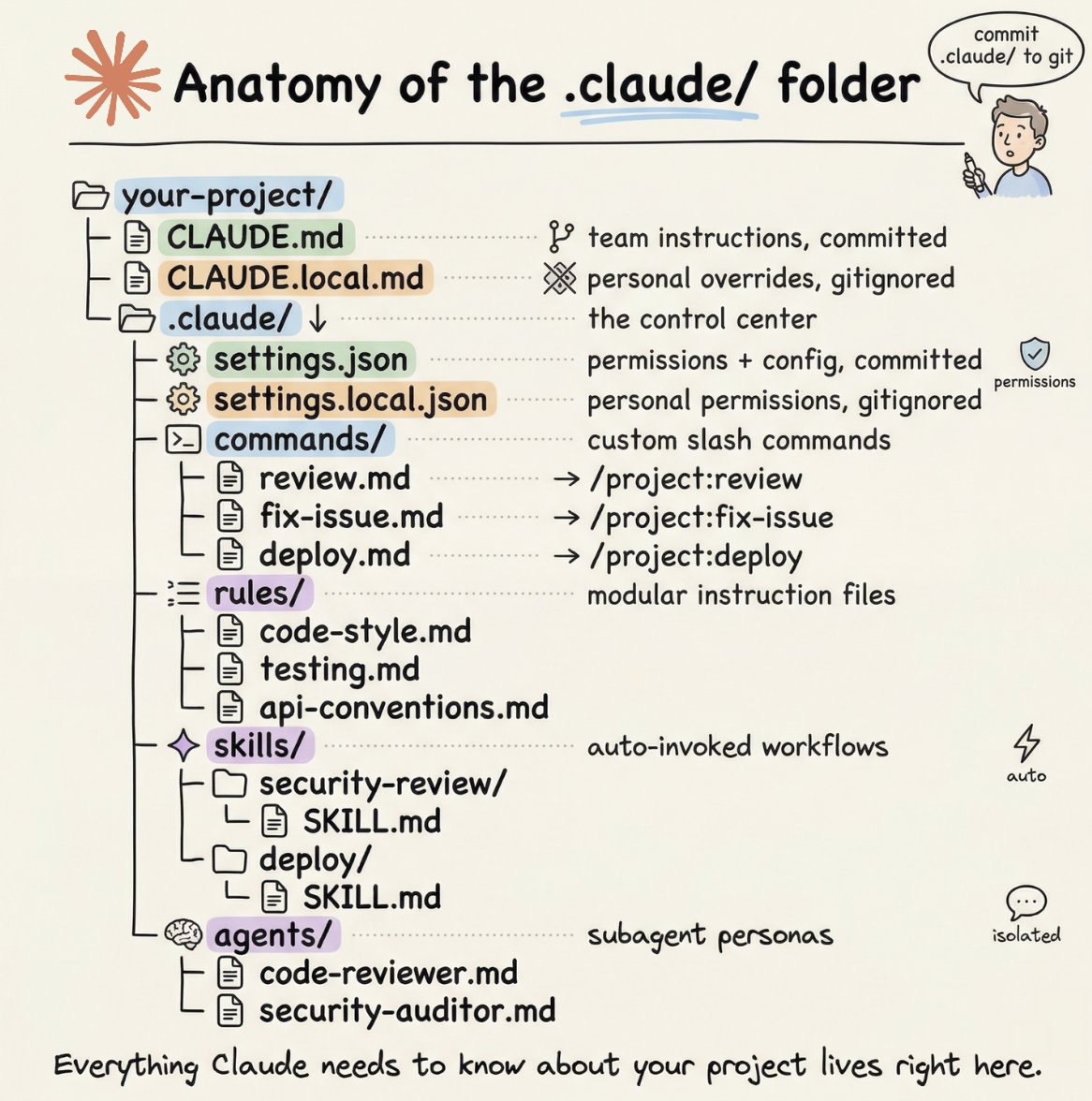

A proper Claude Code project lives inside a .𝗰𝗹𝗮𝘂𝗱𝗲/ folder. Start with 𝗖𝗟𝗔𝗨𝗗𝗘.𝗺𝗱 as Claude's instruction manual. Split it into a 𝗿𝘂𝗹𝗲𝘀/ folder as it grows. Add 𝗰𝗼𝗺𝗺𝗮𝗻𝗱𝘀/ for repeatable workflows, 𝘀𝗸𝗶𝗹𝗹𝘀/ for context-triggered automation, and 𝗮𝗴𝗲𝗻𝘁𝘀/ for isolated subagents. Lock down permissions in 𝘀𝗲𝘁𝘁𝗶𝗻𝗴𝘀.𝗷𝘀𝗼𝗻.

There are two .𝗰𝗹𝗮𝘂𝗱𝗲/ folders: one committed with your repo, one global at ~/.𝗰𝗹𝗮𝘂𝗱𝗲/ for personal preferences and auto-memory across projects.

The .𝗰𝗹𝗮𝘂𝗱𝗲/ folder is infrastructure. Treat it like one.

The article below is a complete guide to 𝗖𝗟𝗔𝗨𝗗𝗘.𝗺𝗱, custom commands, skills, agents, and permissions, and how to set them up properly.

Told a FAANG Hiring Manager I couldn't land interviews without sending 500 applications a month.

She laughed.

Made me use her application strategy. 5 interviews in 10 days.

"You're not intolerant to the job market. You're intolerant to how you position your value," she said.

Here are 18 systems she used differently:

Our official skills repo is open source: https://t.co/X3yOgU0tRd

Equip your agents with curated skills for iOS and Android development, Office file editing, and visual effects with GLSL shaders.

There are more open source projects coming!

This Is Not a #Metaplanet Bull Post

It took me a while to get to this as I'm on holiday with my kids, but I've been seeing both praise and criticism following Metaplanet's recent filings from March 16th. I wanted to properly read through everything before sharing my own thoughts - it’s a bit long since there’s a lot to cover, so bear with me.

First, a quick recap.

The structure has two components:

Common stock + 26th Warrants → overseas institutional investors (Anson, Alyeska, Brookdale, and 11 others). 107.4M shares at ¥380 (+2% premium), paired with fixed-strike warrants at ¥410 (+10% premium). Immediate cash: ¥40.8B (~$255M). If warrants exercise: another ¥44.5B (~$276M). Payment date: March 31.

27th Series Moving Strike Warrants → EVO FUND. 100M shares with daily-adjusted exercise price at zero discount to closing, mNAV ≥ 1.01x condition, floor at ¥298 (revisable to ¥187), exercise suspension at the company’s discretion. Estimated proceeds: ¥37.1B (~$234M). Exercise period: April 2026 – April 2028.

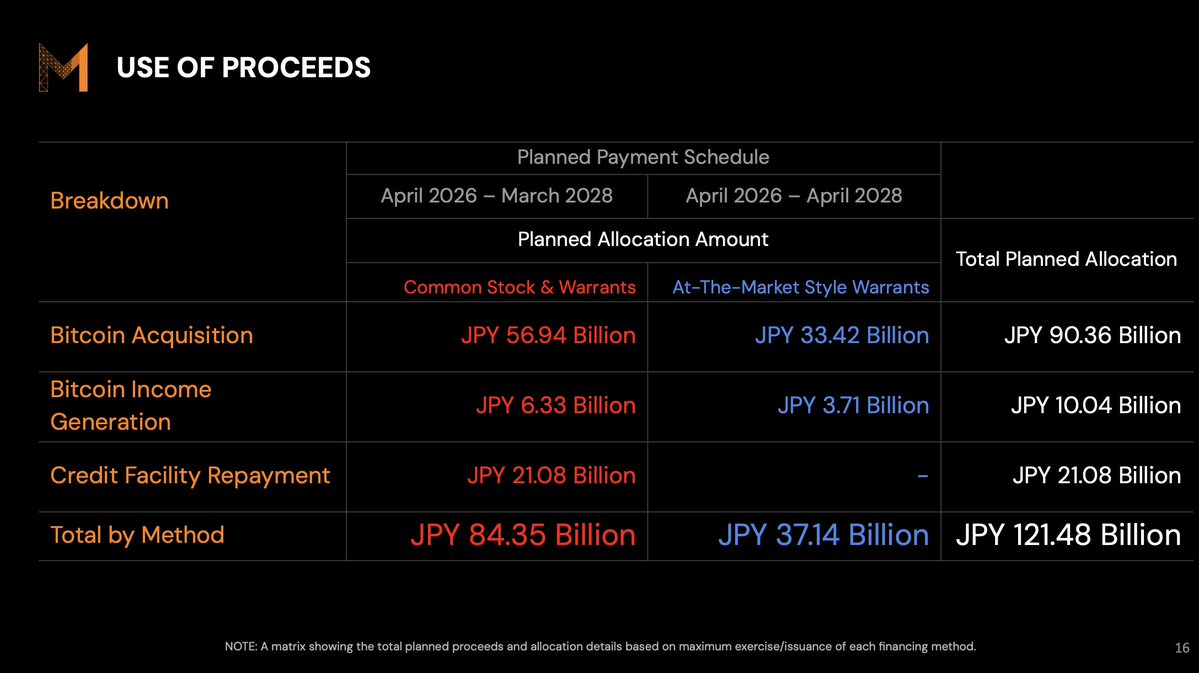

Total potential capital: ¥121.48B (~$770M). This is in addition to the total potential $135M from the Jan private placement. Between the two, we’re looking at ~$905M in total capital, equivalent to 37% of their current BTC treasury.

They also cancelled the 23rd and 24th series warrants (210M shares, floors at ¥637 and ¥777) through December 2027. They couldn’t realistically be exercised, so now they effectively have a structure that can be activated with more flexibility around current price levels.

Use of Funds (at full exercise):

→ ¥90.36B ($573M) to BTC acquisition ~75%

→ ¥10.04B ($64M) to Bitcoin Income Generation (BIG) ~8%

→ ¥21.08B ($134M) to credit facility repayment ~17%

-----

The mNAV Clause

EVO FUND can only exercise when mNAV ≥ 1.01x. In the previous warrant structures, there was nothing preventing exercise at non-accretive levels, and frankly that was always something on my mind. If BTC ran and the stock underperformed, warrants could be exercised into weakness. This mNAV floor is a protective feature that retains optionality.

Having said that, it’s not 100% airtight, since the mNAV calculation is EV-based. Enterprise Value (Market Cap + Debt + Prefs − Cash) ÷ BTC NAV

At the current 1.11x mNAV, take out the debt and prefs, and the equity-to-BTC ratio is approximately 0.97x. That would mean that issuance at current relative levels would not be accretive, even though mNAV is >1.01x.

As a result, there seems to be a lot of criticism of this clause, and fear that it will be exercised too aggressively at non-accretive levels. IMO, it’s a useful guardrail that is more effective than simply having nominal price levels that are completely disconnected from the relative value / mNAV.. and having it as a floor doesn’t mean they will automatically allow selling at any level >1.01x. They’ve already suspend exercise at levels that didn’t make sense, and clearly stated that their ultimate priority is to maximize BTC yield.

-----

Bitcoin Income Generation

Page 21 of the 27th series notice contains an important disclosure.

Their target is ~2% per year in option premium revenue against BTC NAV. Assuming preferred issuance at 25% of BTC NAV with a 5% dividend rate, the annual dividend burden equals ~1.25% of BTC NAV. The income business at 2% covers the preferred dividend with a 60% margin of safety — without relying on BTC price appreciation.

The way I see it, the 2% target (as is the 25% prefs/treasury soft cap) is a floor, and ultimately will depend on what they’re generating in income. With BTC implied vol running at ~55-60%, annualized premium yields are around 30-35%. At a collateral base of 5-10% of their BTC holdings, that would generate 1.5-3.5% yield on their treasury.

Perhaps what I like most about this business is that it is in some ways counter cyclical to Bitcoin itself. The same volatility that results from violent selloffs is jet fuel for this business, and allows them to acquire more BTC at lower prices. So, in some ways it is a built-in hedge, that limits downside while enhancing upside.

But anyway, I’m digressing.. this isn’t new, but I think framing it this way showcases the strength and value of the innovation here.

For Q1 2026, I estimate roughly $26-31M in revenue and ~$18-22M in operating income at 71% margin. That would put the annualized revenue run-rate at ~$104-124M — potentially ahead of their ¥16B ($105M) full-year target. And this is before the March funds are deployed.

The other hidden feature in this business, is that as their scale grows, so does the income base, proportionally — and that income base supports larger preferred issuances at lower coupons, which fund more BTC acquisition without diluting common equity. The amplification effect compounds over time.

-----

The Capital Structure: Preserving a Pristine Balance Sheet

While the $134M in credit facility repayment from this raise certainly feels like leakage, it's an important step in preparing the balance sheet for optimal prefs issuance, while simultaneously retaining optionality in case of a continued BTC correction.

MERCURY was priced at 4.9% in November 2025 when mNAV was 0.88x and leverage was rising. With a stronger balance sheet (more BTC collateral, less debt), more recurring revenue/income, and a potentially higher mNAV, the next preferred issuance could potentially price tighter.

On a $500M preferred issuance, the difference between 4.9% and 3.5% is $7M/year in savings — allowing them to issue more in prefs and buy more BTC.

The filing also mentions (as before) that preferred share listing on the TSE is in preliminary consultation. A listed preferred creates a liquid public market — dramatically broadening the investor base and likely compressing the coupon further.

The debt repayment improves the credit profile. The credit profile lowers the cost of prefs. The cheaper prefs fund non-dilutive BTC accumulation. The BTC accumulation grows the income capacity. The income capacity covers the preferred dividend and then some.

-----

Scale is the Moat

Would you rather own 10% of a company that holds 100 BTC, or 0.01% of a company that holds 100,000 BTC? In both cases your effective Bitcoin ownership is the same,

But the answer depends on what your ownership gives you access to that you cannot replicate yourself.

At 100 BTC, you own a stock that holds Bitcoin. And if that’s all I get, then I’d rather own the BTC directly.

At 100,000+ BTC, you own a lot more than just your pro-rata ownership in the Bitcoin - and that cannot exist without scale: institutional-grade options underwriting, credit facilities, index eligibility creating passive bid under the stock, the ability to absorb significant institutional allocations, preferred share issuances at favorable terms to amplify BTC exposure, and the foundations for a Bitcoin-focused asset management business and a venture arm seeding the ecosystem.

None of that is possible at 100 BTC. All of it becomes possible — and self-reinforcing — at scale.

From their filing: “The Company believes that holding Bitcoin at the scale of approximately 210,000 BTC as a medium-term target is not intended merely to accumulate assets, but has significance in building a strong financial foundation that enables the development of financial services based on Bitcoin.”

Strategy accumulated so fast and so aggressively that their lead became structurally permanent. Now Metaplanet needs to do the same before the window closes. Every day at 35K instead of 50K or 100K is a day where a well-capitalized competitor could theoretically replicate the playbook. The lead needs to become impractical to close, and hence lock in a permanent moat.

So with that said, while issuing equity at mildly accretive levels may seem like a waste to current shareholders, it implicity adds value to the shares by bringing everyone closer to achieving an imprenetrable position with a ton of future options. The flip side of course, is that it means more capital is required to achieve the same BTC returns in the future. So it’s a balance that management need to carefully find, while being nimble, retaining optionality, and adapting to different markets.

Needless to say, prefs are the potential golden goose in this equation, as they provide permanent capital matching the duration of Bitcoin, while delivering the highest potential BTC yield -> especially if dividends are fully funded via income, and hence carry zero dilution.

-----

Reigniting the Engine

@DylanLeClair posted recently "We’re working to find a balance to get the engine humming again." https://t.co/OI5enuVFFX

This flywheel is self-reinforcing once it starts humming: accretive issuance → BTC purchase → BTC/share grows → justifies higher mNAV → mNAV expands → enables larger accretive issuance → repeat. Consistency, and the ability to generate BTC yield in all market conditions is a critical factor here.

The bigger challenge is that the flywheel naturally decelerates as the treasury scales, given the finite nature of Bitcoin.

This is why the seeds they are planting now matter. Metaplanet Ventures (¥4B into BTC infrastructure), Metaplanet Asset Management, the JPYC stablecoin stake, Bitcoin Magazine Japan. If they generate cash flows that justify a permanent mNAV premium above 1.0x, the flywheel never needs to stop and the company can issue (predominently prefs supported by operating cash flow) accretively in perpetuity.

-----

Useful Metrics

I want to propose a framework for the industry. Three metrics that let you evaluate any BTC treasury raise in a way that makes them comparable across companies, and that can be tracked as a trend in any given company.

eNAV_i (Issue Price / BTC NAV per share) — the true premium at which each share is sold relative to its BTC backing. Uses the actual issue price and excludes debt and preferred shares from the numerator — unlike mNAV, which inflates the reading by the full value of the capital stack above equity. This is the number that determines whether issuance is accretive to common shareholders' BTC per share. Above 1.0 = accretive. Below 1.0 = dilutive.

CI (Capital Raised / BTC NAV) — the intensity. How much are you expanding the balance sheet relative to what you hold? Metaplanet's March raise: 9.8%.

Δ BTC/share = (1 + CI) / (1 + CI/eNAV_i) − 1 — the exact accretion. The percentage change in BTC per share from the raise.

Metaplanet March equity at ¥380: eNAV_i of 1.066 (issue price was 6.6% above BTC NAV per share). At 9.8% CI: +0.56% BTC/share accretion.

If the 26th warrants exercise at ¥410 (+10% premium): eNAV_i rises to 1.15. Δ BTC/share: +1.3%. Although this depends on the BTC price at the time the warrants are exercised, so it’s less straightforward.

Preferred shares are the endgame. No common shares issued = no dilution = eNAV_i is effectively infinite.

Track eNAV_i across consecutive raises to see whether the flywheel is accelerating or decelerating.

-----

Closing Thought

My sense here is that, while the critical arguments carry some truth, IMO they are mostly fuelled by the negative price action across the whole space, including of course Metaplanet. Had we been making ATHs, I doubt anyone would be criticising any of these moves. Price action has a way of dictating sentiment.

I like what they’re doing. I like (and trust) the team. And I like the macro backdrop.

I’m looking forward to the AGM next week, where I expect more to be revealed, in addition to an update on their BTC holdings (my estimate is 37-38K BTC). That’s all for now.

Disclosure: I hold Metaplanet shares. Some of my calculations are ‘napkin math’. Not financial advice. All errors are my own.

$MPJPY $MTPLF

Ready to deploy AI agents? NVIDIA NemoClaw simplifies running @openclaw always-on assistants with a single command.

🦞 Deploy claws more safely

✨ Run any coding agent

🌍 Deploy anywhere

Try now with a free NVIDIA Brev Launchable 🔗 https://t.co/eAbqav9A4x

🚨 This is how engineers at Amazon, Google, and Shopify actually use Claude Code.

It's called GSD (Get Shit Done) and it solves context rot the quality degradation that destroys your Claude Code sessions as the context window fills up.

No BMAD. No enterprise sprint theater. No Jira nonsense.

Here's how it works:

You run one command

→ /gsd:new-project

→ It interviews you until it fully understands your idea

→ Spawns parallel research agents to investigate your stack

→ Creates atomic task plans with XML structure Claude actually understands

→ Executes in fresh 200k context windows per task

→ Commits every single task to git automatically

Here's the wildest part:

Your main context window stays at 30-40% the entire time.

All the heavy lifting happens in subagent contexts. No degradation. No "I'll be more concise now." Just clean, consistent execution.

Engineers at Amazon, Google, Shopify, and Webflow trust this thing.

MIT license. One command to install:

npx get-shit-done-cc@latest

Link in the first comment 👇

It‘s incredible how many people are shitting on Metaplanet right now.

Look, I get it, we‘re down >80% from the ATH. The Japanese market is a bit shaky in general, macro wise. It‘s not clear yet that Metaplanet‘s prefs will be approved, and if so, when.

Also, the market and their ¥637 MSW program has backed them into a corner for the past 6 months or so.

People are giving up left and right, showing signs of PTSD.

In fact, the current sentiment feels very bottom-ish. Max pain, capitulation.

If prefs are not approved, that would be a huge blow, of course. But it wouldn‘t be the end.

Management has demonstrated a willingness to use any tool at their disposal to raise more capital and increase Bitcoin per share.

Remember that 1 year ago, Metaplanet held ~3,200 BTC. Today, they hold 35,102 BTC. 10x in 12 months.

Soon, it will be >40,000 BTC, and until the end of the year their goal is to reach 100,000 BTC.

I believe they have a good chance to achieve this goal.

They also have the chance to completely own the Japanese market. Become Japan‘s Strategy, and even beyond, as they will become a key player of the Japanese Bitcoin ecosystem.

Once Bitcoin is at 200K, all this negative sentiment will be long forgotten.

Bookmark it.

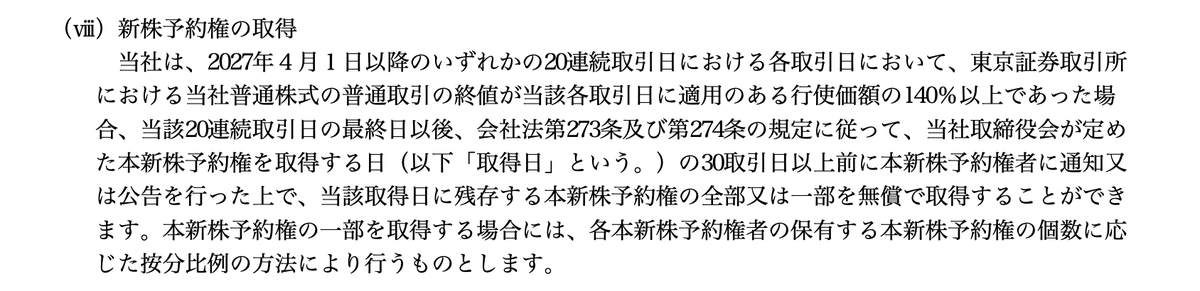

More on the Metaplanet fixed-strike warrants. Per the term sheet, the warrants have a soft call after 12 months if the stock trades up 40%+. The terms are still pretty favorable to the buyer, but this is better for the company than a straight 2 year warrant.

"(viii) Acquisition of Stock Acquisition Rights

The Company may, if the closing price of the Company's common stock in regular trading on the Tokyo Stock Exchange equals or exceeds 140% of the exercise price applicable on each such trading day, on each trading day during any 20 consecutive trading day period on or after April 1, 2027, acquire all or a portion of the remaining Stock Acquisition Rights at no cost on the date set by the Company's Board of Directors for the acquisition of the Stock Acquisition Rights (hereinafter referred to as the "Acquisition Date"), in accordance with the provisions of Articles 273 and 274 of the Companies Act, upon providing notice or public announcement to the Stock Acquisition Rights holders no fewer than 30 trading days prior to such Acquisition Date. In the event that the Company acquires a portion of the Stock Acquisition Rights, such acquisition shall be conducted on a pro rata basis in proportion to the number of Stock Acquisition Rights held by each holder."

https://t.co/OWA8KNbNMJ

Today we're introducing the world's first AI CMO.

Enter your website and it deploys a team of agents to help you get traffic and users.

Try it now at https://t.co/KbAE6FNgzE

You should be using Claude Code to run your entire work day.

Here's exactly how, from @thevibePM, field CPO at $2.6B @pendoio:

1:47 - The one command that plans his whole day

21:42 - His Claude.MD Setup

33:42 - Skills vs MCP vs Hooks

40:11 - Why he left Cursor for terminal

I’m an amateur investor, self taught and never got very sophisticated. No college and was an electrician for 20 years. I don’t believe most people should trade options, certainly not if they have gambling tendencies. I’ve always discouraged friends from using leverage and was highly critical of MSTU/X late 2024/ early 2025.

Options knowledge can be useful even if you never touch options. Most people lose money with options and therefore most people probably shouldn’t touch them. I still watch a couple of dividend YouTube channels and despite having little interest in most dividend investing, I like to keep other avenues in mind and want to be ready to switch to an alternative or hybrid method if I feel compelled.

There are simple games I like to play with options. The most important one I’ve done since 2009 involves estimating what a certain strike and date option “should” be trading at. I got good at it over time and imo this helps me judge if options are cheap or expensive. I may look at a 6 month or 1 year chart of the stock first to get an idea of the volatility and make sure earnings is not between now and option expiration, or if it is, account for that. If you tend to think they always look cheap or always expensive then you aren’t getting closer to reality. If they’re cheap I like to buy. Expensive? I sell.

Another fun game is finding comparable rates of (potential) return with a stock or between stocks. Whether you’re bullish or bearish MSTR/STRC, you can slice this a few different ways. STRC pays about 1.4% per 6 weeks with taxes deferred (ROC dividends currently). Looking at April 17th options (6 weeks away), I could get 3.7% by selling the $100 strike put option. So if I have $10k cash I’ll earn $370 for essentially promising to buy 100 shares of stock at $100/share if price is lower than $100 on the close of April 17th. As long as it’s trading above $96.30 ($100-$3.70), I would make money. Even after tax I’d make around 2% for 6 weeks vs STRC paying about 1.4% with taxes merely deferred. If I’m in a lower tax bracket or in a tax free account, I could sell the $80 strike April 17th put option and get $1.50 which is almost 2%. Another way is to sell a vertical credit put spread, higher premium rates if the price stays above my upper strike but more risk. I could sell the $60 strike put for around $0.65 (which by itself is a 1% premium) and buy the $50 put for $0.40. This makes the premium profit $0.25 and since the width of the spread is $10, that’s 2.5% returns. Though, in this case I lose 100% of my bet if price closes under $50 on April 17th and my breakeven is MSTR closing at $59.75.

Extending the same exercise to 1 year is also fun. STRC pays 11.5% annually. MSTR has Jan 2027 and June 2027 puts, so let’s examine January, expiring in a little over 10 months. Selling the $100 strike pit pays $20/share (20%) so the breakeven is the stock being at $80. Some will calculate the premium differently as I wouldn’t need $10k cash to promise to buy 100 shares at $100 a piece if I’m getting paid $20/share immediately. Really I could make this trade with $8,000 account, and since I’m still earning that $20 ($2,000 for 1 put contract representing 100 shares), I’m really earning 25% premium before tax. Even selling the $50 strike yields about 12% in 10 months calculating things this way. Spreads don’t look much better as the $50 to $40 pays about $1.50 or 15% with $40 being complete loss. Spreads also take a long time to increase in value if the expiration date is far off, but tend to trade more stably since you have forces largely balancing themselves out if the stock swings up or down.

There are pros and cons to all of this. This isn’t at all me saying any one seems to be less risk than the other, though sometimes in similar situations I get that feeling.

Jeff Bezos on why too many ideas can destroy a company, and the discipline that built Amazon's inventive edge:

"Jeff, you have enough ideas to destroy Amazon."

That's what senior executive Jeff Wilke told Bezos after just one year of working together.

Bezos was confused. He pushed back: "What do you mean?"

Wilke was a manufacturing expert. He explained it simply:

Every new idea Bezos released created a backlog. Work piling up, adding no value, creating distraction instead.

The fix wasn't to stop having ideas. It was to control when they came out:

"You have to release the work at the right rate that the organisation can accept it."

So @JeffBezos changed how he operated.

He started keeping lists, holding ideas back, and waiting until the organisation had the bandwidth to absorb them.

But then he flipped the problem entirely.

He asked: "How do I build an organisation that's ready for more ideas?"

His answer was structural: get the right senior team, give leaders real executive bandwidth, and build a company capable of running multiple bets at once.

And there's a benefit he didn't expect. Slowing down made the ideas themselves better:

"If you are releasing the ideas through time, it forces you to prioritise them better. You end up sharpening the ideas better."

The constraint becomes a filter. The ideas that survive the wait are the ones worth acting on.

The result? Faster execution, less distraction, and better ideas.

Here's the prompt:

## Workflow Orchestration

### 1. Plan Mode Default

- Enter plan mode for ANY non-trivial task (3+ steps or architectural decisions)

- If something goes sideways, STOP and re-plan immediately – don't keep pushing

- Use plan mode for verification steps, not just building

- Write detailed specs upfront to reduce ambiguity

### 2. Subagent Strategy

- Use subagents liberally to keep main context window clean

- Offload research, exploration, and parallel analysis to subagents

- For complex problems, throw more compute at it via subagents

- One task per subagent for focused execution

### 3. Self-Improvement Loop

- After ANY correction from the user: update `tasks/lessons.md` with the pattern

- Write rules for yourself that prevent the same mistake

- Ruthlessly iterate on these lessons until mistake rate drops

- Review lessons at session start for relevant project

### 4. Verification Before Done

- Never mark a task complete without proving it works

- Diff your behavior between main and your changes when relevant

- Ask yourself: "Would a staff engineer approve this?"

- Run tests, check logs, demonstrate correctness

### 5. Demand Elegance (Balanced)

- For non-trivial changes: pause and ask "is there a more elegant way?"

- If a fix feels hacky: "Knowing everything I know now, implement the elegant solution"

- Skip this for simple, obvious fixes – don't over-engineer

- Challenge your own work before presenting it

### 6. Autonomous Bug Fixing

- When given a bug report: just fix it. Don't ask for hand-holding

- Point at logs, errors, failing tests – then resolve them

- Zero context switching required from the user

- Go fix failing CI tests without being told how

### 7. Task Management

1. **Plan First**: Write plan to `tasks/todo.md` with checkable items

2. **Verify Plan**: Check in before starting implementation

3. **Track Progress**: Mark items complete as you go

4. **Explain Changes**: High-level summary at each step

5. **Document Results**: Add review section to `tasks/todo.md`

6. **Capture Lessons**: Update `tasks/lessons.md` after corrections

### Core Principles

- **Simplicity First**: Make every change as simple as possible. Impact minimal code.

- **No Laziness**: Find root causes. No temporary fixes. Senior developer standards.

- **Minimal Impact**: Changes should only touch what's necessary. Avoid introducing bugs.