MSTR Summary (As I understand it)

The market basically has an extremely large overhang of a potential BTC seller. Now MSTR has been a big reason why rallies at highs have always continued on longer than it should - it is an essential indicator to track for the health of the bull market - early stage bull = MSTR buys usually was sustained continuous bullish momentum ; late stage bull = MSTR buys would hold price up, before a nuke after the announcement that Saylor has been buying

Now this is potentially unravelling, essentially because the day of reckoning has come - after all, when someone buys, one must ask - how does he get the capital to buy? Saylor has historically funded it through equity financing / convertible notes / term loans / and more recently, preferred equity product financing - and I'll try to explain it simply as how I understand it.

Now for most of the time, equity financing was actually a very sustainable ponzi. Equity had no guarantee of returns. That is a good thing. Of course, this all came at the expense of MSTR shareholders, but the idea that I believe Saylor had, was that "we are selling the stock, to buy something that has more convexity than the stock (BTC), so that, in 10 years, we will end up with a lot more money, and so the stock will be a lot higher" - i.e you're trading short term PA for long term CAGR

This of course assumes a lot of things - 1) that BTC will be higher in 10 years, 2) that BTC has some sort of CAGR, and 3) that stock price will reflect this, and 4) that people will buy the story, and 5) that the market will like it, will reward it (and it has, for the past 4 years)

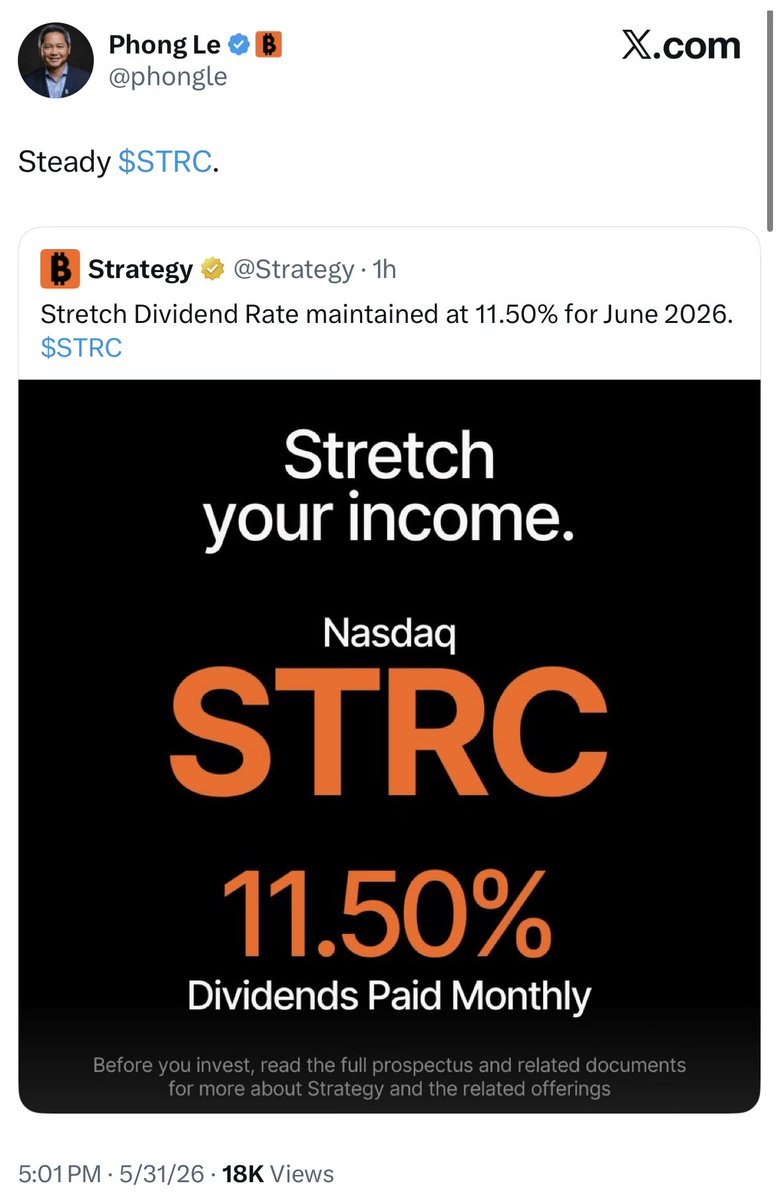

Now, all's well. This is where we get to the trouble - Saylor launched a bunch of new products recently - STRC / STRD / etc. I'm not an expert in these products, so feel free to correct me where I'm wrong, but these are preferred shares that pay yield. They say: Hey, give me cash. I'll give you yield. This yield varies in order to keep the product at par value ; i.e If today it goes to 90, the yield increases to get people to "buy" it so as to "peg" it there;

I'm not going to go through each product - they all work slightly differently. The rest are fixed yield instead of variable; All you have to understand is at this point, MSTR now began giving out money (i.e having yield)

This is a bad thing and where the story is now. Having obligations means having to spend cash to pay yield, which means, in a company that hinges on an assumption of the 15% CAGR of a magical internet asset with no real cashflows ( other than software biz) - where is the money coming from?

The way I see it, you basically have an extremely huge cloud looming on the horizon. You don't know when the hurricane will start, but you see it. This is enough to prevent BTC from reaching new highs in the first place - it is possible to kick the can down the road, to "look away from the hurricane", but the hurricane is there all the same, just waiting for its reckoning.

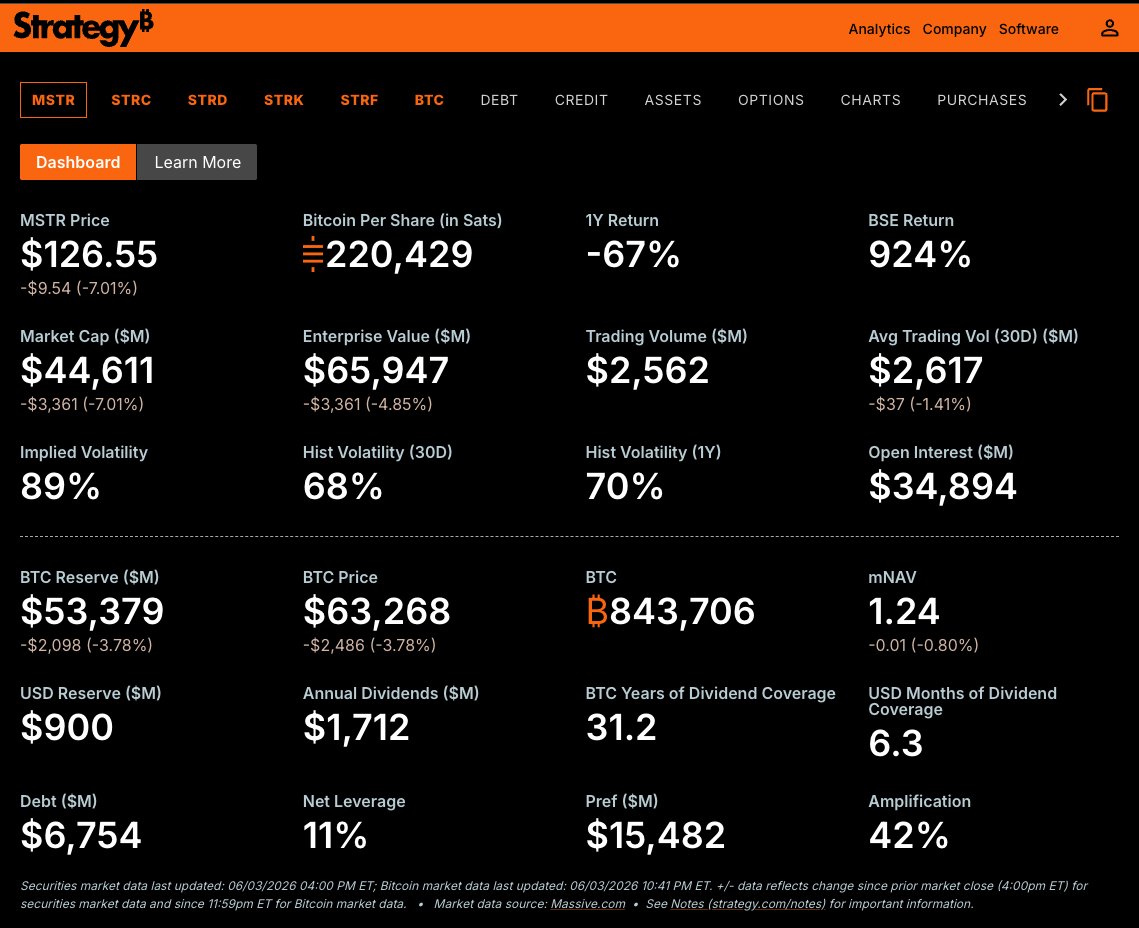

He holds $53 BILLION in Bitcoin (Based on Price of 63k), yet only has enough cash for 6 months of dividend coverage (numbers are from https://t.co/Dn0HtZunrC). And back in February they claimed a $2.25 Billion reserve - this reserve has been drawn hard (now it's 900M)

Saylor has 3 ways out. And again - this is just my analysis - I could be missing something:

1. Stop the yield. He can theoretically (since these are all preferreds, correct me if I'm wrong) just stop payments.

2. Somehow finance more $ to pay dividends, either by selling more MSTR, or raising debt.

3. Sell BTC to pay his bills

Now, obviously, the second-order effects of all of these are incredibly bad no matter how you see it.

For 1) if he does that, faith in MSTR would collapse, stock prices would probably go down, STRC goes to Mordor, and maybe he doesn't have to sell BTC, but there are still obligations to pay, so it doesn't fully solve the issue. The thing is - stop paying STRC can be done, but it's like putting a bandaid when your arm gets cut off.

Because what happens here is that (and this is where I'm relying on Claude, who read the offering doc) - he stops the cash from going out, but the obligation still exists - i.e He can stop the payment, but he can't cancel the debt. It's like your landlord coming to you for this month's rent, and you defer it to next month - but you now have to pay two months' worth of rent next month, not just a month's rent

STRC is cumulative - so stopping = you don't pay cash now, but the amount you skipped gets added to a tab and grows. And because STRC is a "Perpetual Stretch Preferred Stock" with perpetual being the key word here, there is no maturity date, it doesn't end, and the only true way to stop it is by buying it back with cash. Else, the dividend just keeps compounding at the back.

Buying back is an option, and according to Claude, the cash redemption price is $101 per share - so $8 Bn if he wanted the whole STRC stack gone. But that's where we come back to the above - he doesn't have the cash!

For 2) It's like rolling your credit card bill. This months bill comes in - you take a new credit card, use it to pay your old one, and for the next month, you're chilling, and you extend the runway. Now if BTC magically goes up to 200k, then you are safe, you can pay your obligations, selling some BTC won't matter.

For 3) This is the worst case scenario. I mean, this is just a doom loop. On 1st June, MSTR already filed a sale of 32 BTC (2.5m), the first strategic / material sale in history. The other sale was in 2022, and that was a tax-loss sale which they bought back immediately. BTC instantly went down by 6-7% on the day, and it's down 12% since then. If they sell more, BTC is just going to go down faster than they would get $ back from selling, and they're basically left holding the bag.

My analysis:

For now, the markets will probably stay at a standstill until this is resolved. Everyone is watching to see what Saylor will do. Again, he owns roughly 4% of all BTC. And what happens if BTC keeps going down? That would be a doom loop playing out. And putting yourself into the mindset of a buyer - why would I buy BTC here, when I know there is a potential seller coming here tomorrow?

I'm reminded of an old joke in the office that our head of trading used to say, that originated on wall street:

A trader thinks that the prices of eggs are going to increase, and so he contacts his broker and asks him to buy 1,000,000 egg futures at $1.70

Sure enough, a week later, the price of egg futures is $2.50, and the trader, happy to ride his winners, places an order for 3,000,000 more egg futures

Next month, at $4.30 a piece, he pats himself on the back and restructures his liquid investments to buy another 10,000,000 egg futures

At the end of the quarter, egg futures are trading at $7, and the trader finally calls up his broker and tells him to sell them all

The broker replies: “To who? You’re the egg man!”

PSA: This is a personal opinion piece written in my individual capacity, not on behalf of or attributable to my employer. It is not investment research, a recommendation, or an offer or solicitation to buy or sell any security or asset.

It does not constitute financial advice and should not be relied upon for any investment decision; readers should do their own research and consult their own advisors. All views are my own as of the date of writing and may change without notice. Factual claims are drawn from public sources and may contain errors or become outdated.

I hold no position, long or short, in BTC, MSTR, or any related security, and have no economic interest in the price of any asset discussed. I receive no compensation from any party in connection with this piece.

$900m cash - $1.7B annual dividend obligations

he clearly can't sell BTC, only options left are to sell MSTR stock or shut off the dividend

time-bomb probably has 3 months left

Counterpoint:

The fact that the bottom 50% pay some taxes doesn’t mean they have skin in the game.

It’s an illusion. In reality, they are net consumers of tax revenue. Their share of total federal income taxes is only about 4%.

They receive significantly more in government benefits and services than they contribute.

But the illusion creates the appearance of contribution, which leads them to compare their payments to those of higher earners. Amid all the misleading rhetoric about “fair share,” many genuinely believe they’re already paying more than their portion while others are shirking.

Most don’t see this dynamic of net-consumption clearly today.

It will become obvious once their federal income tax is reduced to zero because the government’s fiscal reality won’t meaningfully change.

The illusion of contribution will simply dissolve.

The left picture is Japan 80 years after two nukes.

The right is Cuba after 66 years of communism.

The only thing more dangerous than nukes is leftist governance!

The best thing about sticking around for a bear market is you’re in the seat ready to pounce and position in preparation for the bull.

You don’t have to re-familiarise yourself tokens or narratives and you’ve developed a strong sense for what will perform well.

You’re immediately ahead of the game vs all the newcomers/tourists who fomo back in scrambling around trying to figure out what to buy.

It’s been a long journey but you’re in the driving seat.