@Dcpcooks I’m interested from your experience how the 5% level on us long yields is defended against usually in the past. What would it take to break out of this secular downtrend and in the case what do you think the short-term reaction will be? Is trading a breakout viable?

@TechCharts I like this a lot, short equities has so much noise rn and volatility is too elevated for a good entry for long options. This euro trade has all the right macro tailwinds and dosent depend on something shocking developing in the gulf from what I can tell

Food for thought.

Trump, Hormuz and the End of the Free Ride

For half a century, Western strategists have known that the Strait of Hormuz is the acute point where energy, sea power and political will intersect. That knowledge is not in dispute. What is new in this war with Iran is that the United States, under Donald Trump, has chosen not to rush to “solve” the problem. In Hegelian terms, he is refusing an easy synthesis in order to force the underlying contradiction to the surface.

The old thesis was simple: the US guarantees open sea lanes in the Gulf, and everyone else structures their economies and politics around that free insurance. Europe and the UK embraced ambitious green policies, ran down hard‑power capabilities and lectured Washington on multilateral virtue, secure in the assumption that American carriers would always appear off Hormuz. The political class behaved as if the American security guarantee were a law of nature, not a contingent choice. Their conduct today is closer to Chamberlain than Churchill: temporising, issuing statements, hoping the storm will pass without a fundamental reordering of their responsibilities.

Trump’s antithesis is to withhold the automatic guarantee at the moment of maximum stress. Militarily, the US can break Iran’s residual ability to contest the Strait; that is not the binding constraint. The point is to delay that act. By allowing a closure or semi‑closure to bite, Trump ensures that the immediate pain is concentrated in exactly the jurisdictions that have most conspicuously free‑ridden on US power: the EU and the UK. Their industries, consumers and energy‑transition assumptions are exposed.

In that context, his reported blunt message to European and British leaders, you need the oil out of the Strait more than we do; why don’t you go and take it? Is not a throwaway line. It is the verbalisation of the antithesis. It openly reverses the traditional presumption that America will carry the burden while its allies emote from the sidelines.

In this dialectic, the prize is not simply the reopening of a chokepoint. The prize is a reordered system in which the United States effectively arbitrages and controls the global flow of oil. A world in which US‑aligned production in the Americas plus a discretionary capability to secure,or not secure, Hormuz places Washington at the centre of the hydrocarbon chessboard. For that strategic end, a rapid restoration of the old status quo would be counterproductive.

A quick, surgical “fix” of Hormuz would short‑circuit the dialectic. If Trump rapidly crushed Iran’s remaining coastal capabilities, swept the mines and escorted tankers back through the Strait, Europe and the UK would heave a sigh of relief and return to business as usual: underfunded militaries, maximalist green posturing and performative disdain for US power, all underwritten by that same power. The contradiction between their dependence and their posture would remain latent.

By declining to supply the synthesis on demand, and by explicitly telling London and Brussels to “go and take it” themselves, Trump forces a reckoning. European and British leaders must confront the fact that their energy systems, their industrial bases and their geopolitical sermons all rest on an American hard‑power foundation they neither finance nor politically respect. The longer the contradiction is allowed to unfold, the stronger the eventual synthesis can be: a new order in which access to secure flows, Hormuz, Venezuela and beyond, is explicitly conditional on real contributions, not assumed as a right.

In that sense, the delay in “taking” the Strait, and the challenge issued to US allies to do it themselves, is not indecision. It is the negative moment Hegel insisted was necessary for history to move. Only by withholding the old guarantee, and by saying so out loud to those who depended on it, can Trump hope to end the free ride.

I spent time in Shenzhen last year and when I saw Merz come back from China saying Germans need to work more I immediately knew what broke his brain because I lived the exact same cognitive shock

my first week in Huaqiangbei I burned through 4 prototype iterations of a motor controller board for less than a thousand bucks total, back home a friend was working on something similar and spent over 12 thousand for a single revision that took almost two months to arrive

when you live that contrast in your own hands with your own project something permanently shifts in how you see the world and it goes way deeper than speed & cost

what Shenzhen actually built is a collective learning organism, imagine 20 PCB fabs 15 injection mold shops 30 component distributors and a hundred firmware freelancers all within a 2km radius, looks insanely redundant from the outside until you realize redundancy is actually information density in disguise

I watched this firsthand with an injection mold supplier I was working with, this guy had seen a hundred founders iterate similar thermal designs over 6 months so he proactively modified his tooling before I even opened my mouth, he knew what I needed before I knew what I needed, the intelligence lives in the relationships between the nodes and it compounds daily

the west thinks about manufacturing as a cost center you optimize by centralizing…

China accidentally built a distributed neural network of manufacturing intelligence where knowledge diffuses horizontally across thousands of agents faster than any single western company can process internally

so when Merz comes back and says we need to work a bit more I think he saw the problem but COMPLETELY misdiagnosed the solution, telling Germans to work harder is like telling a horse to gallop faster when the other side built a combustion engine

the gap is ARCHITECTURAL

it’s ecosystem density, you need a custom connector in Shenzhen you walk 200 meters, in Munich you send an email and wait 3 weeks

it’s iteration speed, parallel search vs sequential optimization at the system level, it’s risk tolerance, Chinese founders ship something broken on Monday fix it Tuesday ship again Wednesday while European companies are still in the approval phase for the pilot program of the feasibility study…

and Merz only saw the surface, what he missed is the tier 2 cities like Hefei Chengdu Wuhan replicating the Shenzhen model at scale right now

BYD going from irrelevant to outselling every european automaker combined in roughly 5 years, Huawei building its own 7nm chip under maximum sanctions when every analyst said it was physically impossible & behind all of that a government that treats advanced manufacturing as an existential national priority while europe debates whether AI needs another ethics committee

I think what we’re watching is the most asymmetric economic competition in modern history and most western leaders are still framing it as a productivity problem when it’s actually an ontological one

Europe & America are optimizing variables that China stopped tracking years ago meanwhile China is compounding on dimensions the west has no framework to even measure

Merz at least had the courage to name

it out loud and I respect that genuinely but working a bit more inside a broken architecture just means you arrive at the wrong destination slightly faster

We need to rule the database — and end its rule over us.

Citrini assumes AI will destroy thousands of high-paying jobs and create none in return. He’s missing the real story.

The modern job has become soul-draining, mind-numbing database slavery. Millions of talented, ambitious people spend hours of their lives chained to a screen: fixing other people’s mistakes, chasing missing fields, reformatting decks for the tenth time, and babysitting bloated spreadsheets no one will ever read.

Our entire existence is ruled by the database. You can’t board a plane, clear security, close a mortgage, pay taxes, or resolve a customer issue unless the system approves — and it’s wrong half the time. Customer service has been reduced to apologizing while you clean up someone else’s mistake.

This system is broken, expensive, and — until AI — no one saw another way.

Fear of the unknown is why AI scares so many people. They see only disruption and lost jobs because they can’t picture the world when the drudgery finally dies. This is why Citrini's piece below struck a nerve.

That’s why we don’t just want agentic AI. We need it.

We need thousands — soon millions — of intelligent agents to annihilate this soul-crushing layer. When that weight lifts, work transforms.

Humans get to do what lights us up: judgment, relationships, creativity, and solving problems that matter. The office stops being a prison. It becomes a place people genuinely want to be — buzzing with collaboration and the thrill of “we built this together.”This is the real revolution: better, richer, more human lives at work.

The transition won’t be easy. Transitions never are. But we need it.

The only question is whether the people at the top have the courage to let the old model die. Many C-suite leaders fought hard against even basic hybrid work. If they struggled with that, how will they lead the bigger reinvention coming? The bitter irony: their own jobs are most at risk.

That’s why the most exciting companies today are run by 30-year-olds with no legacy baggage. So, are the boomer executives ready to reinvent themselves, or will they scream that everyone needs to stay stuck in the past as slaves to the database, as they demanded everyone stay slaves to the office when they fought remote work?

Prediction:

$AMZN is going to go on a generational run from 2026 - 2030 as the market realizes it’s one of the most defensible businesses in the world.

Price right now $200.

Check back in 4 years.

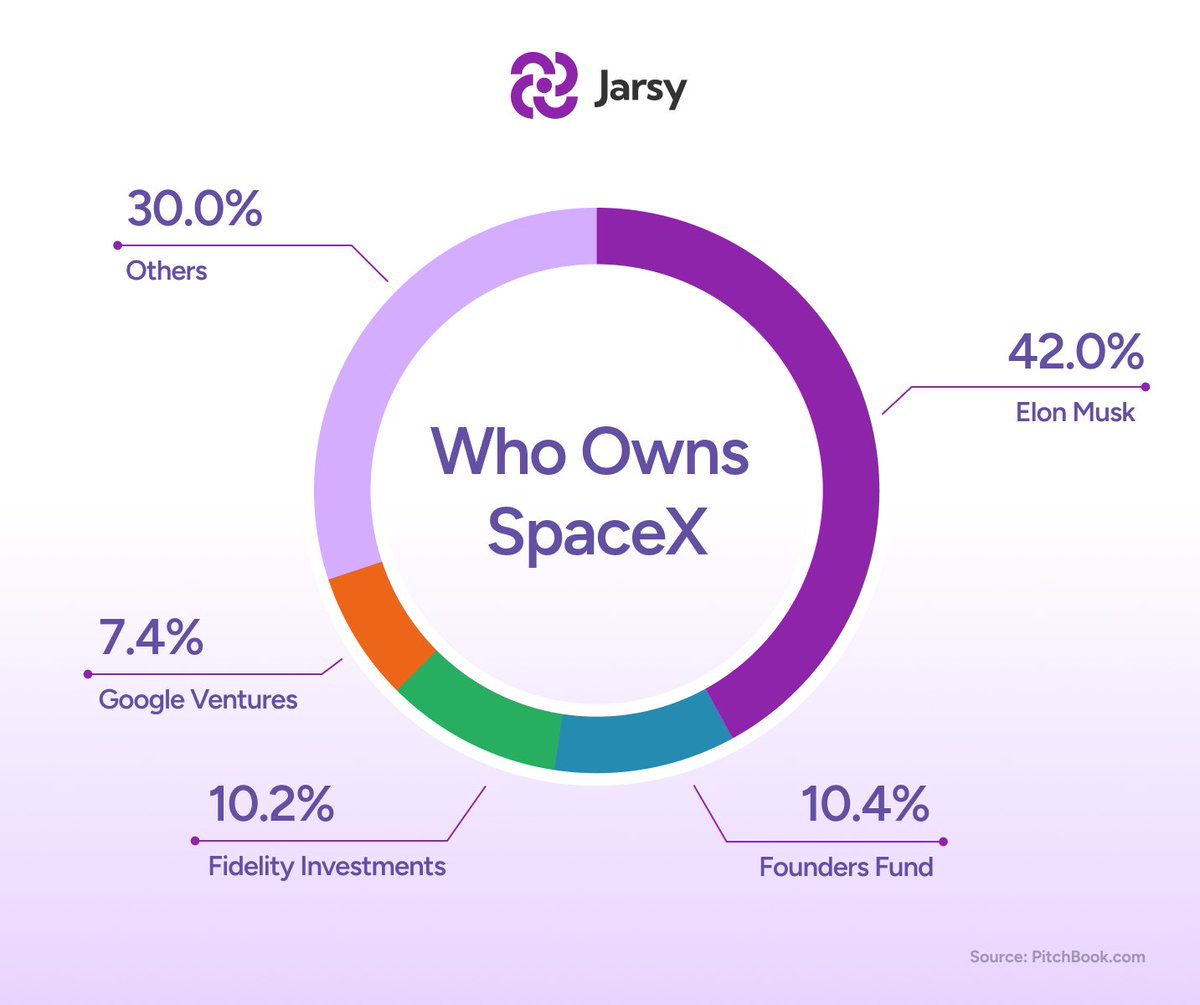

Google is the biggest winner in the SpaceX IPO.

Back in January 2015, Google made a decision that most venture capitalists would call insanely risky.

They threw $900 million at SpaceX when the company was valued at just $12 billion.

Elon had recently figured out how to land rockets.

Starlink was literally just a PowerPoint deck.

The company was burning through cash like water trying to prove the entire concept of reusable rockets could actually work.

On paper, this looked like Google throwing away nearly a billion dollars on a moonshot.

But they saw something everyone else missed.

A founder willing to do the impossible and a company building what would become essential infrastructure for the next decade.

Fast forward to February 2026 and that single decision is about to make Google the biggest winner in what's shaping up to be the largest IPO in human history.

SpaceX is prepping for a mid June IPO at a $1.5 trillion valuation.

Google's 7.4% stake is about to be worth approximately $111 billion.

That's an increase of over $110 billion from their original $900 million investment.

To put it another way, every dollar Google invested just turned into roughly $123.

The reason Google deserves the title of biggest winner isn't just about the raw numbers, though those are absolutely staggering.

It's because they made this bet when nobody was paying attention.

SpaceX could have easily gone under.

In 2015, SpaceX had never successfully landed a rocket and recovered it.

The Falcon 9 had only been flying for a few years.

Starlink was a concept that most people in Silicon Valley thought was a distraction from the core business.

Revenue was basically nonexistent compared to today.

Yet Google saw the market opportunity.

A company with an effective monopoly on launching things to space at scale.

A founder with unlimited conviction and a business model that would become increasingly valuable as the world's data and compute needs exploded.

What makes this different from other venture capital wins is the sheer trajectory.

If you plot SpaceX's valuation from 2015 to 2026, it's almost vertical.

From $12 billion to $36 billion by 2020.

Then jumping to $100 billion by 2021.

$180 billion by 2023.

$210 billion by mid-2024.

$350 billion by late 2024.

Now sitting at $1 Trillion in February 2026.

The IPO target is $1.5 trillion.

Every year, the valuation roughly doubles or triples.

That's the kind of growth trajectory that only happens when you're building something genuinely transformative.

Google got to ride that entire wave with a single check.

The reason Google is the standout winner compared to other early shareholders is also about timing and positioning.

Fidelity Investments also made a big bet alongside Google in 2015.

They've obviously done well too.

But Google's stake is the single largest outside shareholder position after Elon.

They're getting the ability to influence a company that's basically becoming a fourth branch of government in terms of how critical space launch capability is.

No other private company can claim that level of control over orbital infrastructure.

Here's what's actually wild about this whole thing: most people don't even know this is happening.

Because SpaceX is a private company, Google's stake has been sitting on their balance sheet essentially at cost for a decade.

The gain has been completely hidden from casual observers.

But the moment SpaceX IPOs, that $111 billion position becomes real.

It shows up in earnings.

It fundamentally changes how people view Alphabet as an investment.

That's a massive catalyst that a lot of investors aren't positioned for.

What also makes Google the biggest winner is that they didn't need to take this risk and they knew it.

Google had mountains of cash.

They were already the dominant search company.

They could have just kept doing what they were doing and still been worth hundreds of billions of dollars.

But Sundar Pichai and the team at the time made a strategic bet that space infrastructure was going to matter.

They believed that reusable rockets would become foundational.

They were convinced that SpaceX was the only company that could pull it off.

They were right.

And now they're about to collect one of the largest venture capital payouts in history.

The other thing that makes this interesting is that Google gets strategic benefits on top of the equity upside.

By owning 7% of SpaceX, Google has visibility into the company's satellite internet plans.

They can negotiate favorable launch terms for their own ambitions in space.

They're essentially hedged into the space economy at scale.

As AI compute demands keep growing and data centers need more bandwidth, having ownership in the only company that can reliably launch satellites becomes incredibly valuable.

So Google is securing their own infrastructure future.

When the IPO closes in June and Google's stake becomes liquid and tradeable, we're going to see headlines everywhere.

Google turned less than a billion dollars into over $100 billion.

But the real story is that they had the foresight to make the bet when almost nobody believed in SpaceX.

They had the patience to hold it for a decade.

While the company became the most valuable private company on Earth.

That's what separates truly great venture capital wins from lucky bets.

Beyond AI…

China isn’t building towards 20,000 TWh of electricity generation so that they can power their datacenters for AI.

Nobody needs 10,000 TWh to train AI models, and they aren’t doing that. So what are they up to?

China is very obviously targeting the thing beyond AI datacenters, which is the enormous energy demands of ubiquitous robotics.

Datacenters benefit from Moore’s Law, the law of ever improving compute efficiency.

But mechanical actuators obey the laws of Newtonian motion which have no scope whatsoever for moving greater quantities of mass with ever smaller quantities of energy.

China is skipping a whole paradigm.

Their bet being they can backfill AI, once they have total domination over physical work.

China is building the god body first (the robot fleet, or rather the infrastructure that allows it), and will build the god brain later. Probably speed running it, aided by espionage.

America is building the god brain first and hasn’t really thought much about the god body.

The two strategies are quite different and we should acknowledge this.

The AI race risks being a strategic cull-de-sac, a pyrrhic victory, because the longest lead part of the future stack is building the energy system you need to operate an automated Newtonian economy at such a scale.

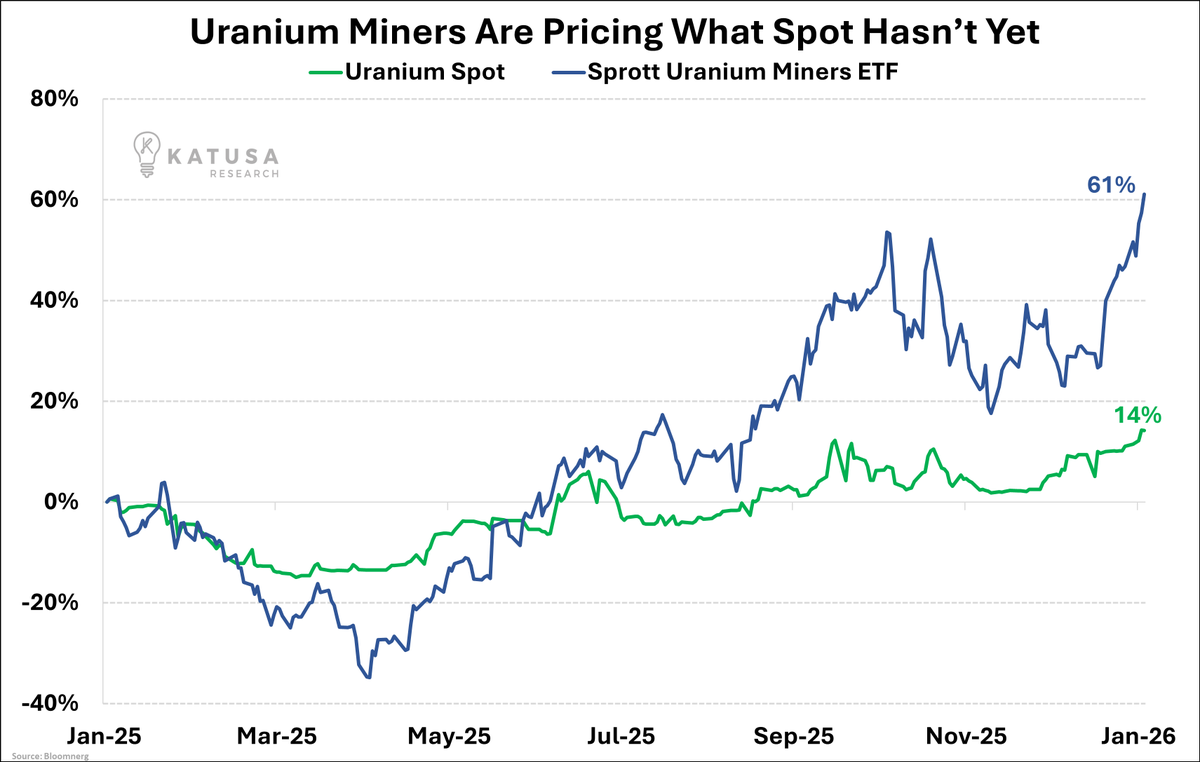

Watch Uranium

Almost 30% of Uranium is uncontracted, resulting in poor spot price performance.

Utilities keep waiting for cheaper pounds that aren't coming.

And every month they wait, the deficit grows.

When they finally buy, spot won't walk higher. It'll gap.

"Recently, senior executives at Salesforce have admitted, both internally and publicly, that they massively overestimated AI’s capabilities. They have found that AI simply can’t cope with the complex nature of customer service and totally fails at nuanced issues, escalations, and

It looks like $META’s depreciable life on its capital base ($210B at 6/30/25) was 11-12 years, as of the 2Q. If the true economic life on its GPU’s is actually 2-3 years, most of its “profits” are materially overstated.

@swingtrader Do you tend to add to winners or add to positions as they drift against you before the bigger move? I always hear different opinions and possibly it’s situational - but do you have a preference?

@swingtrader question - this mean your basically focused on trading price solely? and not volatility because the atm strikes will the closest to the current volatility and you will have less of a chance to capture the profits you would on a slightly otm coming in.

@dlacalle_IA@ryanmcmaken@mises Hello Professor Lacalle, I am an undergraduate Political Economy Student - I follow your research regularly on your English YouTube channel. I am interested in pursuing a masters program at IE, and taking on of your classes. What programs are you most closely involved in?