A thread on where the US stands in its ongoing desire to learn Portuguese🧵

My bro @hkuppy has flagged an interesting development that I hadn’t fully appreciated in the context of #bigflip (hattip @INArteCarloDoss) until this weekend.

Namely, the US is now a 2-speed economy.

1/

@AbrahamNoubani_ @swingtrader Don’t trade short term options, don’t over-lever on futs, and pick a point where you can admit your thesis was wrong to stop out. Risk management is the game

1/ In the second half of the 16th century, Britain plunged into an energy crisis. At the time, the primary source of energy driving the British economy was heat derived from the burning of wood, and Britain was literally running out of trees.

@kittysquiddy Classic seasonal harvest selling pressure on the CBOT (US winter wheat harvest runs early June - late July) compounded by terrible liquidity, broader commodity flush, unlikely port reopening rumors. Global S&Ds still tighter YoY even with bumper Russian crop. Leans bullish

@kittysquiddy Then there’s this.. USD strength and WTI weakness is the only thing keeping a lid on US grains imo. New crop vols and cash mkts paint much different picture than futs @BenniKim

I am normally the first to respect the market and refrain from buying one that is no longer rising on bull news, but in the oil market’s case I will make an exception. Despite the parade of positive catalysts over the past few days (Libya, Caspian, Europe) we got a big smash.

1/7

Good Morning from #Germany, which is falling as an economic powerhouse on a global scale. Germany’s trade surplus is gone. Foreign trade balance came in at MINUS €1bn in May, which is the 1st negative print since 1991 due to its energy problems & weakness in manufacturing.

@kittysquiddy I actually disagree with this. Feed prices higher but so are live board prices. Standard production metrics such as weights, birthings, etc haven’t deviated from normal levels like you would expect if farmers were under pressure. Speaking from US perspective anyways

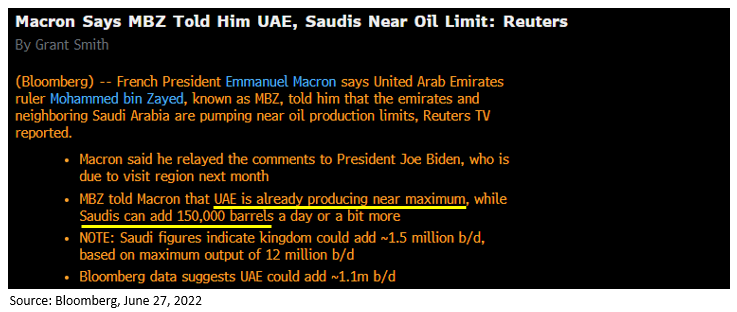

Someone help me out! OPEC spare capacity exhaustion in 2 months then 5 years for Saudi to add 1MM Bbl/d, US shale capped at 0.6-0.8MM Bbl/d per year, and supermajors flat. With annual demand growth of 1+MM Bbl/d...where exactly are the barrels supposed to come from???