Some followers specifically asked for the RBZ Jewellers concall summary - A solid sign of progress. Investors are now tracking businesses, taking ownership, and focusing on fundamentals over price swings. Feels like a real milestone since I started sharing companies as a financial markets educator.

https://t.co/XFWWF82mQj

Here is the Breakdown :

Q1 FY26 Financials

Revenue: ₹74 Cr (↓8% YoY),

Weak demand due to no major festivals this quarter

Akshaya Tritiya preponed to Q4 FY25 → led to 45% QoQ decline

EBITDA: ₹13 Cr (↓8% YoY),

Margin slightly improved to 17.2% (+9 bps YoY)

PAT: ₹7 Cr

PAT margin: 9.3%

Segment-wise Revenue

Retail: ₹45 Cr (↑ marginally YoY)

Wholesale: ₹29 Cr (↓20% YoY)

Job Work: Grew by 8% YoY

Management Outlook

Confident of a strong H2 led by festive + wedding demand

Inventory being optimised; festive collections being launched

IG Expo (Mumbai) saw robust B2B orders booked ahead of Raksha Bandhan, Janmashtami & weddings

Q&A Highlights

Capacity Utilisation & Capex

Current mfg. capacity: 2,000 kg/year

FY25 utilisation: ~66%; FY26 target: 100%

Due to gold price doubling, capacity now supports ~₹2,000 Cr revenue

No expansion capex needed for next 2-3 years

Can source extra capacity via job work if needed

Retail Expansion Plans

Ahmedabad store (pilot): 500–600 kg capacity

New stores planned:

Surat (90% complete) – 400 kg

Rajkot (70%) – 300 kg

4 total stores planned in 2 years (Ahmedabad, Surat, Rajkot, Vadodara)

Timeline: One store to open in Q4 FY26, another in Q1 FY27

Funding: From retained earnings (₹39 Cr PAT last year, ₹45 Cr targeted this year)

Some debt funding also planned

Revenue & PAT Guidance

FY26:

🔸 Revenue: ₹700 Cr

🔸 PAT: ₹45 Cr

FY27 Target:

🔸 Revenue: ₹1,000 Cr

🔸 PAT: ₹55 Cr

Retail margins > Wholesale/Job Work

Q1 Degrowth vs Peers?

Other players showed strong growth due to being pure retail

RBZ had preponed festive sales into Q4, esp. Akshaya Tritiya

RBZ is 65% occasion wear, demand was postponed due to gold price spike

Daily wear remained stable

Product Mix: Occasion vs Daily Wear

Focus remains on occasion wear (core)

Developing daily wear in-house, but still in pilot phase

No plans yet to wholesale or mass manufacture daily wear this year

Geography: Gujarat First

Pilot success in Ahmedabad = scaling within Gujarat

4 target cities = 50% of Gujarat GDP

Long-term plan to expand beyond Gujarat, but not immediate

Regulatory & Other Updates

IT Notice (pre-IPO, bonus share related): Under appeal. No merit.

Gold price volatility affects buying behaviour "demand is postponed, not lost"

Security: Full showroom insurance, strong precautions in place

Stock Liquidity & Face Value Split?

Investor concern on low trading volume

No face value split planned, but management will explore investor feedback

🧾 CFO Position

Mr. Harit Zaveri will continue as interim CFO

Internal promotion planned; grooming talent from within

RBZ Jewelers is in a transition phase, shifting from a B2B-focused business to a high-margin, retail-led growth engine.

Retail expansion, strong balance sheet, manufacturing advantage, and unique brand positioning in bridal jewellery give it an edge.

Watch for strong H2 and upcoming store launches.

#RBZJewelers #EarningsCall #SmallCapStocks #Q1Results #GoldJewellery #RetailExpansion #InvestSmart @sriranganek@anupammahor@AmannaPrerana@tsatwork@deepak4748

EFC Awarded with Interior and Fit-out Contract worth INR 57 Crore

Pune, June 27, 2025 – EFC is pleased to announce that it has been awarded an Interior and Fit-out

Contract worth ₹57 crore from a leading MNC.

#SME#LAWSIKHO#AddictiveLearning#AddictiveLearningTechnology

Addictive Learning Technology FY25 Concall Highlights:

👉FY 2026 & Future Outlook :

▫️ Revenue target of 50-60cr for the next six months (Jun-Dec);

💠Current monthly revenue is around 6cr, with confidence in scaling to 10cr/monthly in the next two to three months, driven by improved sales team efficiency via AI tools

💠No full FY26 revenue guidance was given

▫️No specific margin percentage was provided, but the focus is on cash flow positivity and profitability, with AI as a key driver. Management was reluctant to give precise guidance, noting the business’s inherent uncertainty

▫️Margin compression occurred in FY25 due to lower sales, but this is expected to reverse as sales scale without significant cost increases

▫️Open to monthly / quarterly calls based on feedback and internal discussions

👉Current order book and pipeline:

▫️Current projects:

����Course Sales: Selling approximately 1,000 to 1,200 courses monthly, with average costs of 58,000 INR for law courses and 68,000-69,000 INR for skill arbitrage courses

💠Services Revenue: Current services generate 25 lakh per month

▫️Product Launches: Over 40 products launched;

💠Global academic writing and research services (targeting an $8 billion industry, used by professors and researchers worldwide)

💠Pro courses in sales leadership, AI analytics, US and Indian patent agent exams, strategic operations, AI transformation, medical writing, and US accounting ( CPA, ACCA, enrolled agent for IRS)

▫️NALSA Tie-Up: Already in place, with courses initially sold to existing students for high profitability and low sales cost

▫️Community Leads: Over 30% of revenue now comes from community-driven leads

▫️Pipeline:

▫️US University:

💠Setting up a for-profit university in the US (likely Florida or Texas) within 8-12 months, targeting Dec'25 or Jan'26

💠Will offer an AI and data science-focused MBA, priced at $13,000 (vs. $5,000 currently), with access to 28 US states, UK, Canada, and beyond

▫️Low-Ticket Courses:

💠For India (3,000-10,000 INR) and for the US ($100-200) target microlearning markets, currently experimental with 2% of revenue

💠Successful pilot in UK solicitor qualification exam (5-10 lakh revenue, low delivery cost)

💠Manpower export via AI matching (writers, virtual assistants) planned for the next year

💠Future AI applications to train students on 1,000+ parameters (for judiciary, UPSC exams), analyze classes, and optimize webinars / boot camps

👉 Others :

▫️Challenges:

💠Sales Team: Scaling failed due to low productivity and a negative sales organization mindset; AI tools resolved 80% of this, with 20% left to address in three months

💠Defamation: A lost defamation case and social media attacks caused temporary booking declines, refunds, and fear, but the impact has faded by May-Jun'25; amplified unfairly; pursuing legal action

💠US/UK/Canada Setback: Trump’s removal of the Central American Board of Education led financing partner to withdraw, halting international growth; addressed via the US university plan

▫️Share Price and Promoter Actions:

💠Share price fell due to pre-IPO lock-in ending, a promoter selling shares, defamation case, and social media attacks

💠Promoters bought shares, with no plans to sell; no recovery timeline given for share price, focus is on long-term business growth

💠Defended promoter presence on social media for narrative control and personal freedom, asking investors to factor this into risk

▫️ AI Transformation:

💠Investment: ~4cr spent in the last six months, current spend ~50 lakh/month, with 200-250 of 600-700 staff working on AI aspects

▫️Claims to outperform competitors (e.g., The Legal School, Miles Education, KPMG, UpGrad) in most domains, emerging as the primary choice, often with little competition

▫️Improved branding via unpaid success stories on YouTube; showcase real impact, like a student earning 6 lakh/month

▫️ 33% increase in other expenses were for community, tech, and US university; 27cr of 58cr IPO funds unutilized, to be used for US university or AI; focus on cash flow positivity, no equity dilution planned

▫️600-700 employees and consultants on payroll, considered lean, with no major layoffs planned; staff support AI development and training

▫️AI prevents mis-selling; goal is for students to earn back course fees in 3-4 months, driving referrals and satisfaction

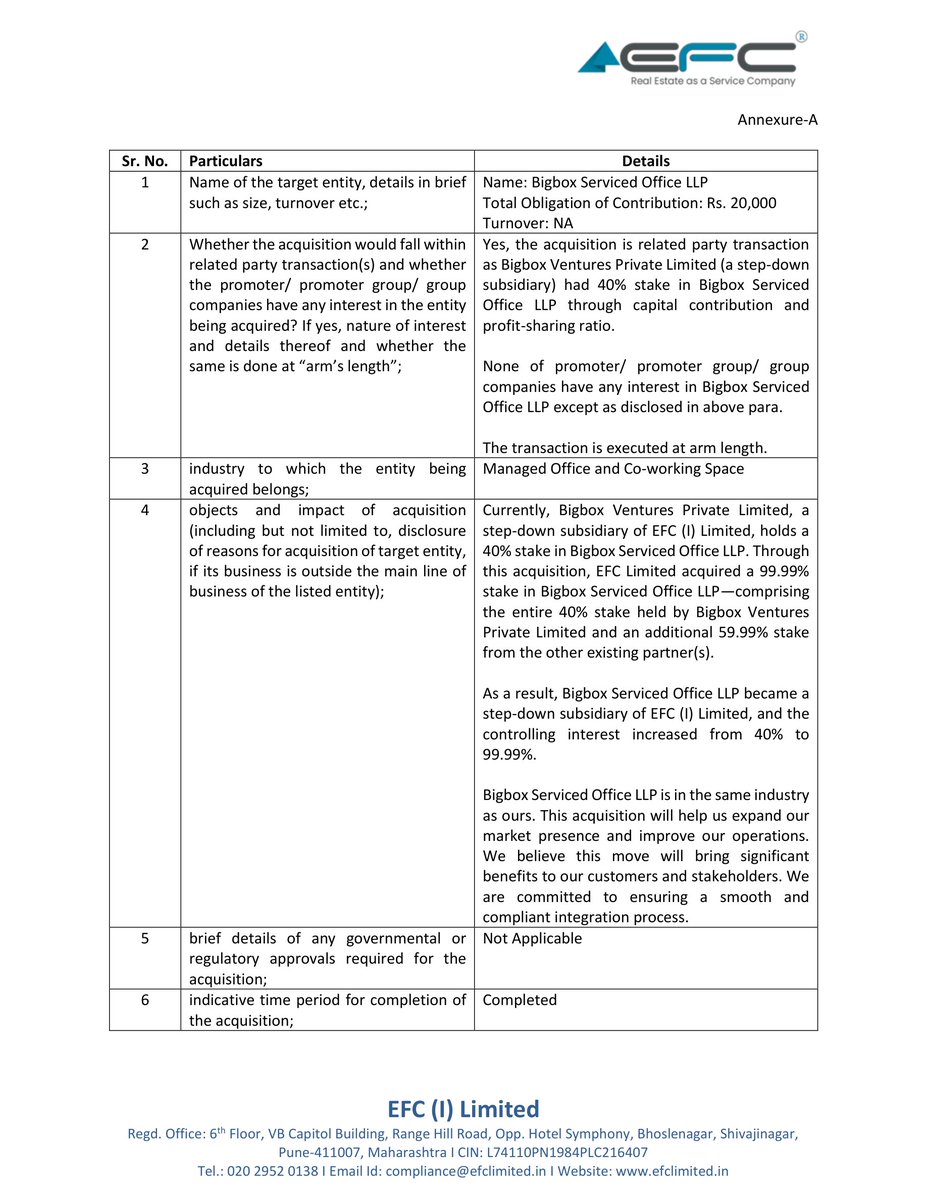

🚀 EFC (I) Ltd Expands into Co-working Space with Bigbox Acquisition | MCap 3,397.76 Cr

- EFC Limited (wholly owned by EFC (I) Ltd) acquired a 99.99% stake in Bigbox Serviced Office LLP.

- Total capital contribution for the acquisition: ₹20,000.

- Bigbox operates in India’s Managed Office & Co-working Space sector (incorporated on 17-10-2023).

- Related-party transaction: Bigbox Ventures (EFC step-down subsidiary) previously held 40% stake.

- Arm’s-length deal—no other promoter/group company interests involved.

- Strategic goal: Expand market presence in EFC’s core industry.

- Acquisition already completed; no regulatory approvals needed.

- No turnover data available for Bigbox (newly incorporated).

Disc: Information provided in this tweet can be inaccurate, verify through the source before making any investment decision.

EFC (I) Ltd Q4FY25 CONCALL HIGHLIGHTS

Payment Structure & Credit Period:

oPayments are generally received on a milestone basis.

oCertain percentages are received as advances.

oDepending on contract size, performance guarantees (5% to 10%) may need to be provided.

oMilestone-based payments are released throughout the project.

oA retention amount (5% to 10%) is retained by the customer until snags are removed and expectations are met before complete handover.

oThe typical credit period in this segment ranges from 45 to 60 days, which the company aims to achieve and adhere to by selecting suitable clients. The company has been improving this credit period, aiming not to cross beyond 45-60 standard days, which is reflected in trade receivables being not beyond 15% of total turnover. This improvement helps improve cash flow.

Margins:

oOverall margins in the design and build segment average between 17% to 22%.

oMargins depend on the nature of the contract, including the percentage of design/intellectual activity involved (more services/intellectual activity leads to improved margins) and the complexities involved (e.g., specialized jobs like R&D centers or laboratories allow for better margins compared to simple office infrastructure development).

oIn the pure leasing business, EBITDA margins are around 30%.

oIf the property is owned, the margin could increase significantly to approximately 75% to 80% because the rental payments to a landlord (which are 45-50% of revenue in the leasing model) are not required.

Order Book:

oAs of the first quarter of the new financial year, the company has confirmed orders of 200 cr plus.

oThis includes a large contract of 183 cr from an MNC client, as announced previously, and other secured contracts.

oThis order book will be executed over the period, with the large contract taking time to get fully executed during the year. The entire amount may not be accounted for in the first quarter but will be spread across the year.

Capex Requirements:

oLeasing Business: Capex is largely required for interior design and fit-out activities. Most leases involve landlords financing the fit-out, making the capex insignificant for the company. On average, the capex is about 50,000 rupees per seat, with the company investing about 10% of that, primarily when there is long visibility on the customer end. For an annual leasing target of 20-25,000 sq ft), the capex outlay is estimated at around 12.5 cr (calculated as 25,000 seats * 10% * 50,000/seat) for the financial year.

oDesign and Build: As a contracting business, there is hardly any capex investment, as no plant and machinery are required.

oFurniture Business: Substantial investment in machinery and equipment has already been made. The total capex invested in the furniture division is about 15 to 20 cr for setting up the plant and machineries and ensuring compliance. No major further investment is planned for the current financial year, although some minor machinery might be needed for specific client requirements.

Growth Targets/Guidelines for FY25-26:

oLeasing: Target is to add 20 to 25,000 seats at an average rental rate of 6,500 to 7,000 rupees, while maintaining 90% occupancy.

oDesign and Build: With a current order book of 200 cr, they expect to grow by at least 60% to 70% year-on-year and are confident of outgrowing expectations.

oFurniture: Target is to achieve 50% to 60% capacity utilization this financial year, with the total capacity being 275 to 300 cr in value terms.

#INOXWIND

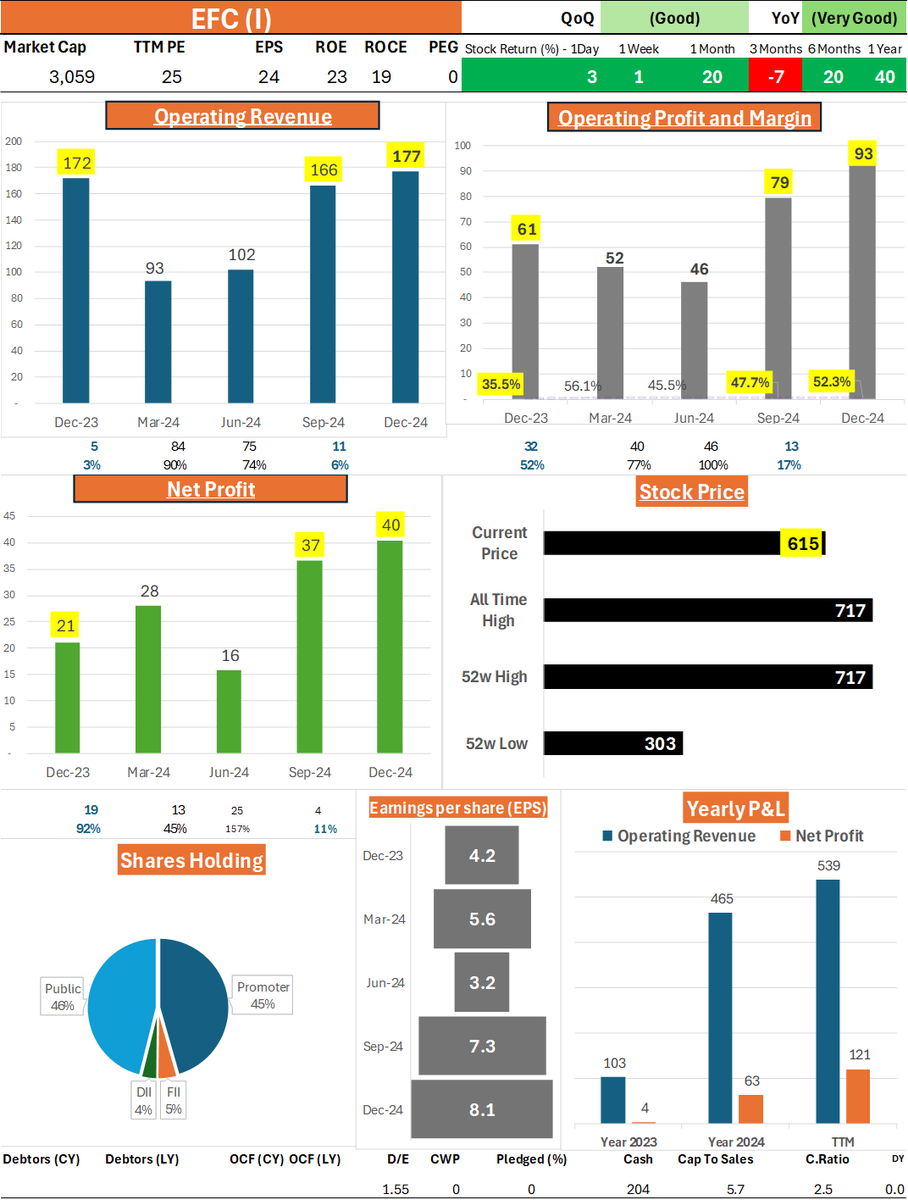

**EFC (I) Ltd.: Powering India’s Workspace & Logistics Boom** 🚀

*CMP: ₹310 | Market Cap: ₹3,000 Cr | P/E: 28*

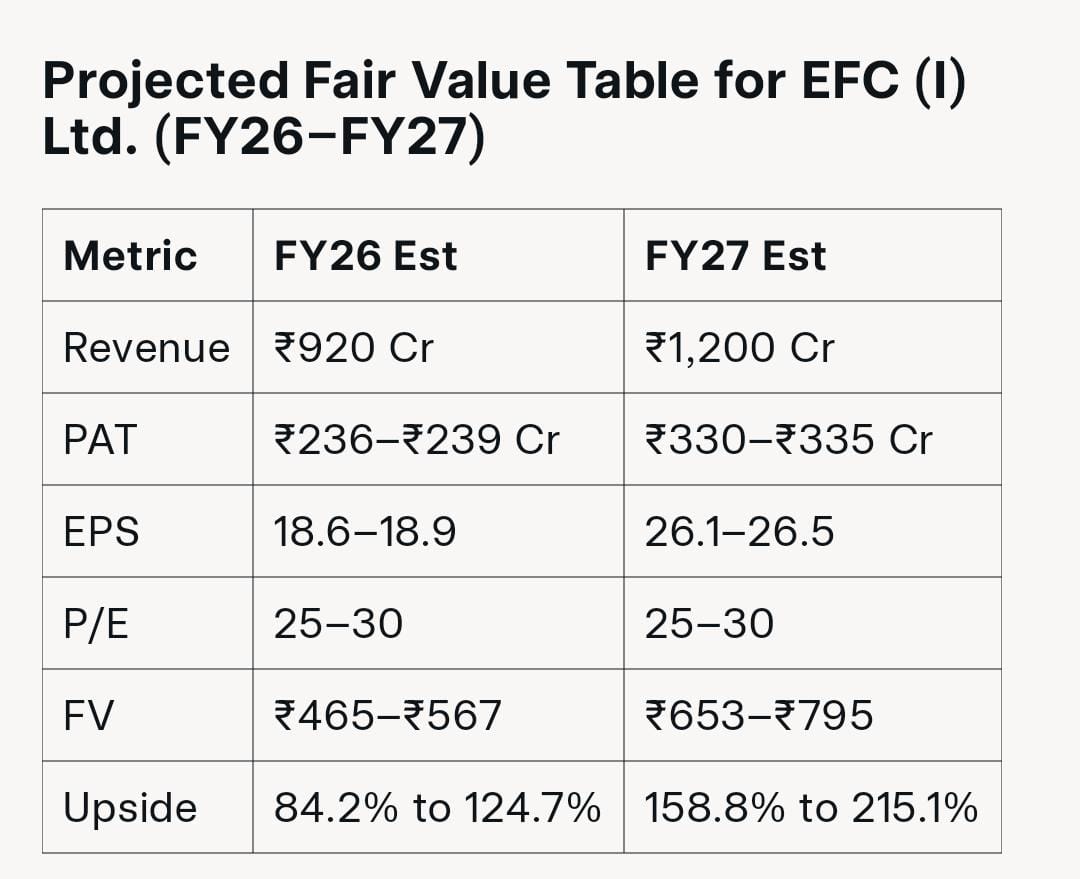

EFC (I) Ltd. is riding a wave of growth 🌊, fueled by its expansion into co-working spaces 🏢 and warehousing 📦, capitalizing on India’s booming demand for flexible office solutions and logistics infrastructure. With a 56.6% YoY revenue jump to ₹657 Cr in FY25 📈 and a 126.4% YoY increase in Q4 FY25 to ₹211 Cr 💰, the company is scaling rapidly by operating 79 centers with over 60,000 seats across 9 cities in 7 states, serving 600+ corporates. Strategic acquisitions like Bigbox Ventures 🤝 and a focus on ESG initiatives 🌱 further boost its appeal. EFC’s product portfolio centers on providing premium co-working spaces, warehousing solutions, and interior and furniture design/build services, targeting a diverse customer base of corporates, startups, and logistics firms seeking modern, scalable workspaces and storage solutions in prime locations.

The company’s cash flow remains robust 💪, with operating cash flow (OCF) soaring to ₹133 Cr in FY25 from ₹10 Cr the previous year, reflecting strong collections despite rapid growth. Management guidance is bullish, targeting 65,000–70,000 seats by FY25-end 🎯 (up from 47,000 in Q1 FY25), with an average of 55,000 operational seats generating ₹350 Cr in revenue from the office space segment alone. They project a 2x YoY growth in the design/build segment, driving overall revenue to ₹920 Cr in FY26 (40% growth) and ₹1,200 Cr in FY27 (30% growth), with PAT expected to rise 50% to ₹236–₹239 Cr in FY26 and 40% to ₹330–₹335 Cr in FY27, positioning EFC to leverage India’s real estate and digital transformation trends 🌟.

Here's my estimated fair value for efc

#EFC #CoWorking #Warehousing #IndiaGrowth #InvestSmart

🏢 EFC Group Expands with New Pune Office Space | MCap 2,066.23 Cr

EFC Group boosts its presence in Pune with a 26,500 sq. ft. office space, adding 600+ seats to its portfolio. 🌟

📌 Key Points:

- EFC Group acquires 26,500 sq. ft. of commercial office space in Pune.

- The new space spans two floors and can accommodate over 600 seats.

- This move aligns with EFC’s strategy to expand its serviced office portfolio.

- The company operates 70+ centers with 56,000+ seats across 9 cities in 7 states.

- EFC serves 570+ corporate clients, including Indian and global companies.

🔹Company Profile:

Name: EFC (I) Ltd

Symbol: EFCIL, BSE:512008

Sector: Realty - Real Estate related services

What do you think about EFC’s expansion strategy? Could this be a game-changer in the managed office sector? 💭

Follow us for more realtime updates!

🕒 This update of EFC (I) Ltd was announced at March 17, 2025, 01:52 PM

Disc: Information provided in this tweet can be inaccurate, verify through the source before making any investment decision.

MPS LTD

MPS is a B2B learning and platform solutions company powering education, and research for corporates.

Market Cap-3,690 Cr.

Current Price-2,157

Stock P/E-30.8

Dividend Yield-3.47 %

ROCE-35.6 %

ROE-26.5 %

Posted Good result Q2 FY25

Invested

📊 MPS Ltd (#MPS) Q3 Earnings

🔝 Net Profit:- ₹40.7 Cr (YoY 🔼 36.9%)

💹 EBITDA:- ₹60.3 Cr (YoY 🔼 35.2%)

📝 Result Analysis:-

MPS delivered a strong Q3 performance with impressive YoY growth in profitability and operational efficiency. Robust execution and cost control have driven both Net Profit and EBITDA higher, beating expectations on YoY and QoQ metrics!

↪️Follow Me For Real-time Updates About Stock Market 👉 @Yuvraj_77

MPS Ltd Q3 Results:-

Revenue 186.36 cr vs 133.81 cr grew by 39.2% YoY & up 4.8% QoQ

PAT 40.71 cr vs 29.73 cr grew by 36.9% YoY & up 15.5% QoQ

Decent trading at 30 PE

Stock up 8% post results