imagine lending to a normal defi money market with 15k+ assets with capital equally distributed across each

even if 100 assets experience tail risk and go to zero (as commonly seen in defi), the overall pool remains healthy due to the level of diversification

in a similar manner, 15k+ consumer installment loans significantly compresses tail risk to a point where senior tranche only has impairment if we hit 2008 crisis levels of defaults

Great to see a solid team like @3janexyz thinking very differently from the 2022 cohort, where mostly all died the same way: concentrated single-name loans, originator marking its own book, and a thin or correlated loss waterfall (or none at all).

"Real world yield" that was just unsecured trust in a structured-credit costume.

Been spending time on 3Jane's ABF risk work and had a few back-and-forths with the team (s/o @wumpycrypto & @uhr3al). It's one of the more solid frameworks I've seen onchain.

And it starts from the failure modes, not the yield (altho yield is pretty juicy as well).

First, let's get into the core insight:

1) Consumer/SMB ABF isn't a credit-quality bet, it's a diversification one.

2) The ~18% gross on the underlying is mostly a complexity premium, not a credit premium.

3) Small borrowers pay it because banks abandoned small-ticket, short-duration lending after 2008, so their real alternative is a 24%+ card, not an 8% loan.

And the loss math is the part most onchain credit never had.

1) Spread the lending across thousands of tiny borrowers and the random blowups cancel out, go from 30 borrowers to 3,000 and the swing in pool losses drops from ~2% to ~0.2%.

2) The book they lend against loses ~1% to defaults over time; its worst-ever batch lost ~4.5%.

3) Senior holders don't lose a cent until losses hit ~19% of the pool.

4) And even modeled at 2008-level stress, the 1-in-100 bad year only reaches ~19.9%, right at that line.

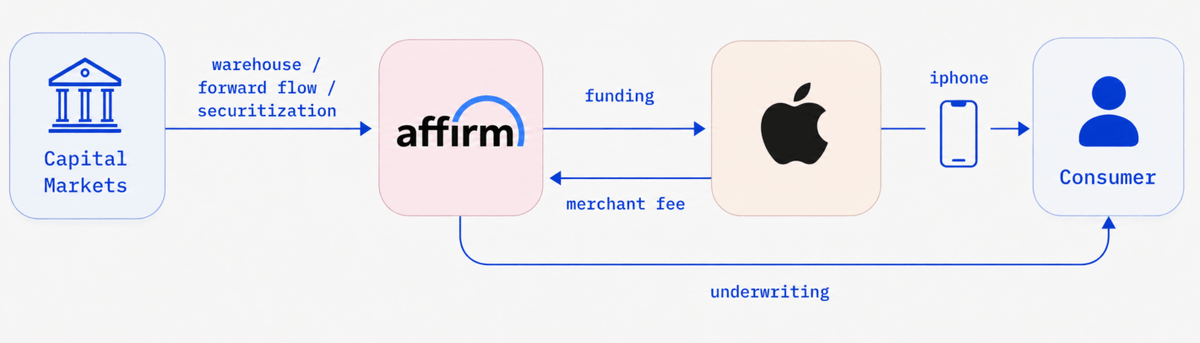

This is the same kind of paper the bond market already rates investment-grade (think Affirm).

And today, they shipped the first live one. A $10M senior warehouse facility with LendSwift, a US consumer lender:

1) ~15,000 short-duration installment loans, ~16% APR underlying, 15% coupon

2) $3.33M first-loss equity from LendSwift (25% of stack), 75% advance rate

3) sUSD3 junior absorbs next: ~32% APY, ~11%

4) USD3 senior paid first: ~13.1% APY, ~64%, behind ~36% of the stack

5) blended ~16% net APY to suppliers, 12mo revolving / 6mo amortization

Two structural pieces seal it.

1) The loans sit in an SPV bankruptcy-remote from LendSwift's corporate entity. Lender blows up, collateral's still walled off and yours.

2) And repayments are swept into a DACA-controlled account, not the originator's. The structural control against diverting or commingling collections, one of the cleaner failure points in off-chain credit.

This is what real-world yield onchain should actually look like.

Not a wrapped T-bill.

Cryptonative dollars funding real US consumer credit through real securitization plumbing.

Compressing the bank-warehouse => forward-flow => ABS gauntlet into one programmable conduit.

Pretty sick.

Still a few things I want to work through with them, and will. But structurally, this is the most serious onchain credit I've seen in a while.

Crypto private credit never had a yield problem. It had a structure problem. Someone's finally building it.

3Jane has executed a $10M senior warehouse facility with LendSwift, a U.S. fintech consumer lender, to scale its loan portfolio

Funded by USD3/sUSD3 at a 15% coupon and secured by ~15,000 short-duration installment loans

Cryptonative capital now funds mainstream consumer credit

1/ Aave v3 mainnet, DeFi's largest lending mkt, has ~20k stablecoin borrowers

A credit card ABS can have up to 750x (~15m) the number of borrowers, enabling AAA credit ratings from agencies

A primer on USD3 & the law of large numbers as we deploy our first credit facilities

with current metrics, they’re giving away 2% of their TTS over the next 90 days to $1.2m excluding any rewards from their points campaign

one thing to note is that their token supply is completely unlocked at launch

with this in mind, even @ $10m FDV -> 66.6% APY from $TAN

with underlying yield from curve pool likely somewhere 10-30% APY

looks juicy, but i have to price risk of new CDP protocol & performance of $TAN to get risk-adjusted before deploying

The Pre-Deposit campaign ends on Monday.

More than $3.2M were deposited in $USDC & $frxUSD.

Of these deposits, $1.8M are eligible for $TAN rewards, as the rest were deposited directly via Curve.

Ineligible LPs: withdraw and redeposit via our UI to become eligible. Withdrawals and redeposits must be one-sided.

Link below 👇

Private credit is usually shown as one clean RWA category. In practice, it is a mix of very different credit risks 📊

A 72-hour settlement liquidity facility is not the same thing as a 3-year corporate loan.

Invoice financing, receivables, SME working capital, trade finance, consumer credit. All of them sit under the same label, but they behave differently under stress.

This is why structure matters so much in tokenized credit.

Duration, repayment source, seniority, first-loss capital, and who controls the cash flow usually tell you more than the asset name.

"receivables financing is a tangible use case for defi to step in"

at 3jane, we're taking the first steps towards bringing receivables financing on-chain in a transparent manner.

through granular loan data & programmatic tranching, 3jane will disrupt capital markets

It’s been a little less than a month since my official start at @aave. A few quick observations:

1. DeFi is the use case for blockchains and is much more welcomed among institutions and fintechs than I even expected.

2. QC backed lending will provide the next growth spurt for DeFi lending - Aave will win here.

3. The old game that chains played for logo slapping is now happening to DeFi protocols. Astute players will price deals wisely and have a way to monetize or just watch their token go into oblivion. Lot of smoke and mirrors here.

4. Receivables financing is a tangible use case for DeFi to step in, really helps if the player is willing to put the full dataset on chain

5. DeFi lending will essentially redefine how prime brokerage works ($25B revenue industry)

6. Aave has work to do on BD side. It’s getting fixed and will be a sight to see.

7. @StaniKulechov is actually a beast - impressive ability to grind.

a defi lending equivalent of asset-backed financing:

traditional unsecured corporate debt -> lending to a pool of 5 collateral assets on an overcollateralized money market. one asset experiencing losses (or in defi, experiencing an exploit) suddenly means a large % of the pool is exposed to a distressed asset. recovery depends on bailouts / discounted value of assets (ex: resolv/stream/kelp). this is similar to a company defaulting on their unsecured corporate loan, where recovery is now contingent upon a discounted sale based on enterprise value.

even in money markets exposed to a wide variety of collateral (30+ assets) - tail risk is wide and heavily correlated.

asset-backed financing -> lending to a pool of 1,000 collateral assets on an overcollateralized money market with:

- concentration limits (X% collateral assets cannot be correlated in losses / come from same issuer)

- performance triggers (Y% drop in price triggers early repayments from borrowers)

- eligibility requirements (what collateral is actually accepted)

one asset experiencing losses represents a smaller % of the pool, meaning tail risk compresses. recovery depends not on bailouts / discounted value of assets once losses already hit. instead, lenders are protected from underperforming assets BEFORE losses hit through early amortization (borrowers getting too close to LLTV), claims on cash flows from collateral assets (yield-bearing tokens have yield routed to repaying loan), and interest from the remaining pool.

tldr;

asset-backed finance equivalent in defi lending is:

- lending to 1,000+ collateral assets (reduces tail risk)

- lending protected by performance triggers (underperforming collateral has exposure lowered)

Structured financing for fintech lenders (ABF) is a $100B+ asset class with virtually no history of being exported into crypto markets, despite consistently generating 10%+ returns.

Releasing a deeper analysis ahead of public launch:

➝ ELI5 warehouse loans & forward-flows

➝ Where the yield comes from

➝ Structured credit risk profile & loss distribution

Full post below.

tvl as a metric penalizes the capital efficiency of unsecured lending protocols

3jane is able to drive higher credit spreads through extending unsecured lines of credit - yet tvl may appear 2-3x lower than an overcollat. lending protocol despite being able to support greater economic productivity

from current data:

3jane

tvl: $600k

outstanding credit: $18.8m (incl. asset-backed finance staging & cryptonative unsecured)

curvance

tvl: $64.5m

outstanding credit: $23.5m

despite similar amounts of outstanding credit, curvance looks like 100x bigger protocol than 3jane when using tvl as the metric for measurement.

as paper states, total assets is a better measurement than tvl when evaluating lending protocols.

i think a better measurement would be fees per $ in total deposits - in essence, how much $$$ is a lending protocol able to drive from a users deposit?

protocols with high fees per $ in total deposits means borrowers are willing to pay a higher borrow rate (likely due to being able to borrow against novel asset classes) & lenders feel they are being properly compensated for their credit exposure.

rerunning the numbers:

3jane

fees: $1.8m (assuming ~ 10% on-credit apy)

total deposits: $19.6m

fees / deposit: $0.09

curvance

fees: $2m

total deposits: $64.5m

fees / deposit: $0.03

this flips the tvl metric upside down, showing how showcasing the capital efficiency of each lending protocol. the main thing its missing is accounting for scalability of a lending model imo.

p.s. i just took curvance as an example b/c its a pretty good, generic overcollateralized lending protocol

I’ll go further and say TVL has always been a poorly defined metric, and is mostly a technical measurement vs a financial measurement, since it just measures tokens in a location.

Let’s imagine three lending protocols. Both receive 100 USDC in deposits.

Protocol A lends 50 USDC out unsecured. TVL is now 50 (100 deposits - 50 lent USDC).

Protocol B lends 50 USDC out against $100 in ETH. TVL is now 150 (100 deposits + 100 collateral - 50 lent USDC).

Protocol C fails to originate any debt at all. TVL is 100 (100 deposits).

What useful information is TVL giving us here? Not much. All three protocols were equally successful in attracting 100 USDC in deposits, but the TVL doesn’t tell that story, and standard practice is to count it as three completely different values.

For lending protocols, this mostly comes from TVL being a poor substitute for proper accounting. If these protocols were lending companies, they would probably be measured by total assets instead of TVL:

Protocol A lends 50 USDC out unsecured. Total Assets is now 100 (100 deposits - 50 lent USDC + 50 loan).

Protocol B lends 50 USDC out against $100 in ETH. Total Assets is now 100 (100 deposits - 50 lent USDC + 50 loan).

Protocol C fails to originate any debt at all. Total Assets is 100 (100 deposits).

What’s different? Well, the collateral is not the property of Protocol B, so you don’t count that. Also, both Protocols A and B made a 50 USDC loan. That lowers their assets by 50. HOWEVER, they have less USDC because they made a loan. That loan is an asset, and would typically be carried at the value of the amount lent.

Total assets is useful here because it accurately reflects that the assets inside each protocol sums up to $100.

Alternatively, the next most common method is to measure total deposits. This is a simple measure of how much money customers deposited, and does not account for loans or other assets. For our example, it would also show 100 for all protocols. To the extent that a protocol primarily finances all lending from deposits, the total deposits method would generally follow the total assets method, with the main difference being the exclusion of any protocol equity.

One could also use net income. In an onchain environment where things like emissions and revenue collection can be scattered across a sprawling set of smart contracts, this is probably quite hard to collect without standardized disclosure and reporting practices.

In general, TVL is more of a technical metric than a financial one - it measures tokens within an affiliated set of smart contracts.

It only loosely reflects actual financial value, and I think its persistence as a key metric has more to do with DeFi participants being naive of standard accounting practices than anything else.

people are starting to wake up to money market lending just being a senior tranche wrapped under the guise of risk curation.

people get paid some benchmark rate set by a utilization curve, borrowers are the junior tranche which keep residual.

imo, these money markets are one of the key features in defi. lots of curators end up catching heat following lots of recent exploits, but they do serve a crucial role in serving as an unbiased (hopefully) third-party to underwrite risk. they allow each holder of an asset to choose their specific leverage through money markets, creating a continuous spectrum of synthetic mezz/junior tranches.

however, there are several issues:

- lenders lending to assets with lots of on-chain dependencies end up taking tail risk, which is near impossible to underwrite (or at least for right now, while DPRK goes crazy). lots of these tail risk events can result in assets being marked down to near zero (look at stream, resolv rlp, etc.), in which case it would actually be +ev to leverage on the underlying asset, since a loss would likely result in being zero'd in junior/senior.

- senior tranche is not correctly paid for lower coverage ratio. a position sitting 0.5% away from LLTV is inherently more risky then a position with a 10% buffer. the residual rate earned by the junior is decreased, yet the senior tranche remains at a constant rate set by the utilization curve. $1 borrowed is indifferent to the coverage ratio.

at 3jane, we're looking to solve this issue on several fronts:

- unsecured lines of credit are priced dynamically by LTV; higher LTVs = higher APY to lenders

- tranching at the protocol level creates a clearly defined capital waterfall while minimizing third-party dependencies

- unsecured lines of credit & asset-backed financing allows for risk curators & 3jane depositors to better underwrite risk as risk becomes dominated by credit exposure, not on-chain tail events

at 3jane, we're tapping into a new asset class previously unavailable to defi: offchain creditworthiness & future productivity

with our unsecured cryptonative lines, we showed our underwriting system can extend unsecured credit lines at scale to cryptonative borrowers

now, we're leveraging fintech lenders to originate loans to hundreds/thousands of businesses utilizing bnpl in their workflow to free capital.

$AFRM originated ~$36B of BNPL purchases in 2025.

Every consumer purchase is funded by a web of bank warehouse lines, forward flows, and securitizations under the hood.

3Jane x BNPL yield, coming soon ✨

@3janexyz -> tranches asset-backed financing and unsecured cryptonative borrowing into a junior & senior tranche

unsecured loans have variable rate based on LTV (what @LotusFi_ does)

Tranching is actually a more adjacent primitive to fixed-rate in this thesis than most think.

Both solve the same institutional problem from different axes; flat pool defi is unallocatable on a risk committee because there's no defined position in the capital stack.

1) Fixed-rate solves it on the rate axis (know what you earn, over what duration).

2) Tranching solves it on the loss axis (know where you sit in the waterfall if losses occur).

Together they reproduce tradfi level structured credit toolkit for onchian capital markets.

What's interesting is the wave is on its third real attempt, and the timing finally fits:

1 (2020–22): @BarnBridgeDAO shipped SMART Yield in 2020 = Senior bonds + Junior tokens tranched from Aave/Compound yield. @idlefinance followed with Perpetual Yield Tranches (epoch-free, novel design).

Both hit ~$80M TVL peaks, both effectively dead now. Right idea, four years early.

2 (2023–24): @StructFinance ported the model to @avax on GLP yield. Idle then pivoted into @paretocredit, recognizing tranching alone doesn't capture value, but tranching inside an institutional credit product (@RockawayX + @FalconXGlobal + @Maven11Capital) does.

Now upwards of $50M+ in structured credit facilities.

3 (2025–26): purpose-built for the moment (and honestly the most interesting one)

@roycoprotocol dawn -> universal yield-source tranching, continuously-priced Senior/Junior split, observation period before Junior absorbs losses. Dialectic curating.

@0xKnoxFi -> 3-tranche model (Senior / Spectrum / Junior) with Surplus Participation. The Spectrum tranche is the under-appreciated bit — DeFi's first real mezzanine layer. In TradFi, mezzanine is where most institutional allocators actually sit. Two-tranche models reproduce only Senior + Equity; three-tranche unlocks the middle.

@LotusFi_ -> tranching within a lending market via LLTV tiers. Different surface, same idea.

@mezzanine_fi -> tranching applied to peg arbitrage + crosschain stables.

Why i think this wave works (and will be bigger than ever) when the previous ones didn't:

1) mature variable-rate base layer (30+ @Morpho curators, @pendle_fi PTs, sUSDe, syrupUSDC)

2) the substrate is finally rich enough to tranche meaningfully

3) institutional buyer is actually here (Pareto's pivot is the proof that risk committees can't allocate to flat pools)

4) curator/structurer role separation now exists for structured products, not just lending

5) fixed-rate origination is shipping alongside, so the full toolkit closes

Defined positions in the capital stack by rate and by loss.

But i believe ideally both is what unlocks the next wave of institutional DeFi.

This will be the next thing i dive deeper into after fixed-rates. Builders in this lane, would love to trade notes.

@3f_xyz bridging time gaps is a great example of how cryptonative rails can revolutionize RWAs

- programmatic, transparent prime broker auctions ensure the best rates for borrowers

- lenders can view real-time loan health

- borrowers are no longer bound by T+X RWA cycles

- each borrower can specifically choose their preferred leverage instead of a blanketly applied fund level leverage

From last week's deposits for @3f_xyz private beta:

⬛️ $7.1 million of total exposure in @centrifuge $JAAA from LPs who are earning yields from leveraging the real world!

🟧 10x leverage on JAAA = ~39.4% APY

🟦 Bridge Facilitator overnight liquidity = 9.1% APR

🟩 wJAAA Morpho lender = 3.7% APY

Few realize there's a $15M @AerodromeFi fuelled heist going on in the form of @overnight_fi ... if you farmed aero in the early days I'm sure you've seen them.

- They raised $850k in pre seed from some good funds

- The product was basically a PoL aero farm. They put up liquidity and bribed their pool, extracted more than their bribes, repeat.

- They were early to this and it worked well, earning them millions and filling up a fat treasury to $15M including their veNFT

- To entice buyers they always said OVN was backed and the treasury would buyback whenever it fell below treasury value... and it should be valued for its PoL and the business itself

- That day came as OVN sold off... but the founders promises didn't come to fruition. OVN has traded down only for a long time.

- In response, the holders put up a vote to distribute the treasury assets back to them

- 1 day later... he's attempting to take the entire treasury for himself and disguising it as a 'token migration'. Every holder will be diluted 1:1000 and get locked tokens

- On top of this he tries to claim protocol owned wallets are suddenly his own... Trying to comingle and mix funds to hide the treasury.

- It's such nasty work, even their lead VCs have started selling at cents on the dollar despite holding until now

Guess the only thing that was overnight about this was how fast the treasury disappeared

note: dcf cap holds OVN (from a long time ago). Thankfully a small bag, but enough to pay attention.

1/ DoorDash just reported 933M orders and $31.6B GOV in Q1.

In 2025 they added Klarna BNPL at checkout to drive growth. Most consumers still don't know who fronts the cash.

The capital markets rabbithole on how your burrito gets financed at 0% APR

1/ Since the 2010s, fintechs made origination software-native. Crypto's one redeeming quality is that it has the capacity to turn capital markets into software when nobody else can.

Both worlds are converging. To accelerate that vision we're introducing fintech credit conduits.

3Jane began as a credit-based money market extending lines of credit to cryptonatives.

Today we're evolving into programmable credit facilities via warehouse loans & forward-flows to power the next generation of fintech originators across a $100B opportunity.

Full post below.

![HarryTran_RWA's tweet photo. I found early RWA projects weekly so you don’t have to PT.17

@Credit_Markets - Tokenized LATAM Private Credit

@higrowfi - Tokenized Agricultural

@fractionaxapp - Tokenized Real Estate

@officialpanora - Tokenized Agricultural

@you_canton - RWA Perps on Canton Network

@ChainBNBapp - Tokenized Real Estate

@ammomarkets - Tokenized Ammunition

@TravessiaCredit - Tokenized Commodities

@satscapital_ - RWA Infrastructure

@GENPowered - Tokenized Green Energy

@deadstock_app - Tokenized TCG

@OnchainEstate - Tokenized Real Estate

[ Bookmark for later read🔖 ]](https://pbs.twimg.com/media/HIQ09BZaIAEvu2Z.jpg)