Jerome Powell just said US debt "will not end well" if nothing changes.

He is right because he has been saying this for years and nothing has changed.

The debt itself is not the immediate crisis but the path it is on is.

Federal debt is growing faster than the entire US economy every single year.

Interest payments alone now exceed $1 trillion annually more than the entire Medicare budget.

The Congressional Budget Office projects debt hitting 120% of GDP by 2036, and some independent models put it far worse than that.

Powell was clear that fixing this is not the Fed's job, Congress controls spending, the Fed controls rates, and Congress keeps spending.

His exact words on the matter: "I pretty much limit myself to those high level points which essentially everyone ignores."

The most powerful central banker on Earth is openly telling you that lawmakers know about this problem and are choosing to do nothing about it.

If interest rates stay elevated and deficits keep compounding, the government eventually faces a forced choice, slash spending, raise taxes dramatically, inflate the debt away, or default on its obligations.

There is no fifth option.

BREAKING: PRESIDENT TRUMP JUST ISSUED A 10 DAY DEADLINE TO IRAN

Trump says the U.S. has to make a meaningful deal with Iran and that we’ll find out in about 10 days.

He warned the U.S. may have to take it a step further if talks fail and Iran needs to make a deal or bad things will happen.

Trump also said Iran cannot have a nuclear weapon and claims that the Middle East is currently at peace.

CPI is at 8 month low.

Core CPI is almost at 5-year low.

Job market is cooked.

Bankruptcies are rising.

Credit card delinquencies are going up.

Housing market is in trouble.

And still, Powell is acting like the economy is stronger than ever and only concern is the inflation.

Powell already made a horrible mistake by continuing QE for longer in 2021, which destroyed the markets in 2022.

He is doing something similar again by being hawkish for longer than needed.

🚨THIS IS REALLY DISAPPOINTING

In the past 5 years, here are the returns of top assets:

Silver: +180%

Gold: +171%

S&P 500: +74%

Nasdaq: +61%

BTC: +35%

ETH: +7%

We took more risks, had the biggest regulatory developments and institutional adoption, and yet underperformed every asset class over the half-decade.

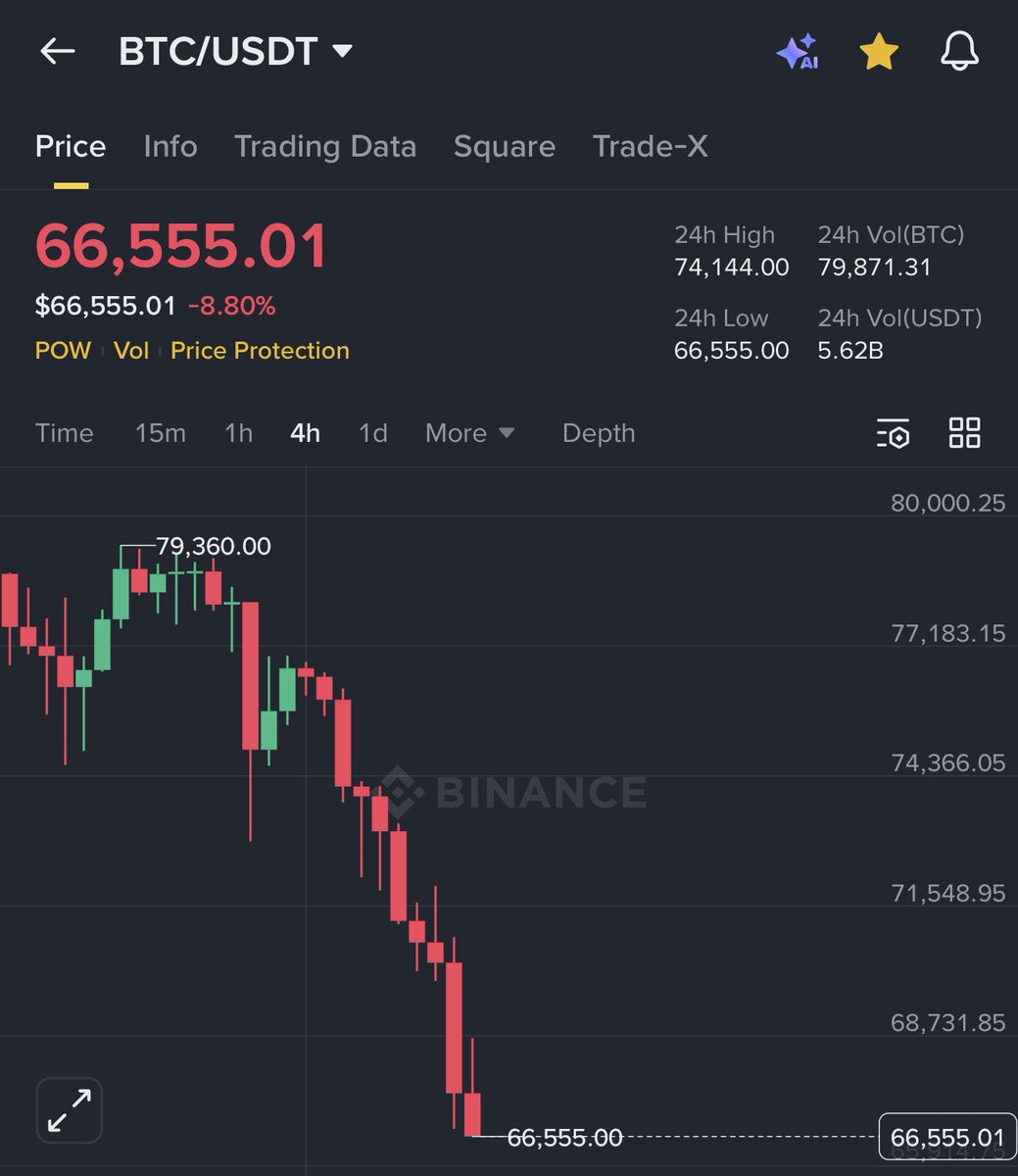

This was the highest volume day on $IBIT, ever, by a factor of nearly 2x, trading $10.7B today. Additionally, roughly $900M in options premiums were traded today, also the highest ever for IBIT. Given these facts and the way $BTC and $SOL traded down in lockstep today (normally SOL trades with beta) + the relatively lower liquidations on CeFi exchanges, this leads me to believe that the nexus of the problem lies with a large IBIT holder. IBIT has become the #1 venue for BTC options trading, so my guess is that a hedge fund trading IBIT options is the culprit.

If you look at the 13F filings for IBIT (I like whalewisdom dot com), you'll find a number of interesting names that have the majority of their fund in IBIT. In fact, there are a few in there (not naming names) that have 100% of their fund in IBIT, which likely means no cross margin. In fact, the biggest reason to set up a fund to hold a single asset would be to isolate margin, so that if the trade blew up, the brokers wouldn't have claim to any other assets.

Interestingly, most of these giant, single asset funds are based in HK.

We know that Asian traders, particularly in China, have been deeply involved in the Silver and Gold trade. Silver was down 20% today, which was the 2nd largest 1 day move in a very long time (largest on Jan 30). We also know that the JPY carry trade has been unwinding at an increasingly rapid pace.

This leads me to think that the culprit for the IBIT blowup today was 1 or more HK-based non-crypto hedge funds. As @FranklinBi pointed out, the fund(s) being non-crypto would explain why no one sniffed them out. They would likely have few/no crypto counterparties, meaning complete isolation from CT.

The last small piece of evidence I have is that I personally know a number of HK-based hedge funds that are holders of $DFDV, which had the worst single down day ever, with a meaningful mNAV decline. The mNAV had been holding steady surprisingly well throughout this pull back until today. One of these fund(s) could have been connected to the IBIT culprit, as I highly doubt a fund taking that large of a position in IBIT and using a single entity structure would only have the one fund.

Now, I could easily see how the fund(s) could have been running a levered options trade on IBIT (think way OTM calls = ultra high gamma) with borrowed capital in JPY. Oct 10th could very well have blown a hole in their balance sheet, that they tried to win back by adding leverage waiting for the "obvious" rebound. As that led to increased losses, coupled with increased funding costs in JPY, I could see how the fund(s) would have gotten more desperate and hopped on the Silver trade. When that blew up, things got dire and this last push in BTC finished them off.

I have no hard evidence here, just some hunches and bread crumbs, but it does seem very plausible. Let's see if some more concrete evidence floats to the surface here soon. The smoking gun will be a large fund fitting this profile filing a 13F showing a giant IBIT holding going to zero. Unfortunately, if a fund had their IBIT position liquidated today, they wouldn't have to disclose the position change until 45 days after the quarter end, so we'd be looking at mid May for the smoking gun from 13F filings most likely.

Hopefully some of you out there with too much time on your hands this weekend can snoop around more. My guess is that word will start to get out, because something of this size is just too hard to hide. Additionally, if the broker was not able to liquidate the fund in time, the broker may have a hole in their balance sheet, which would be even more difficult to hide.

This was the highest volume day on $IBIT, ever, by a factor of nearly 2x, trading $10.7B today. Additionally, roughly $900M in options premiums were traded today, also the highest ever for IBIT. Given these facts and the way $BTC and $SOL traded down in lockstep today (normally SOL trades with beta) + the relatively lower liquidations on CeFi exchanges, this leads me to believe that the nexus of the problem lies with a large IBIT holder. IBIT has become the #1 venue for BTC options trading, so my guess is that a hedge fund trading IBIT options is the culprit.

If you look at the 13F filings for IBIT (I like whalewisdom dot com), you'll find a number of interesting names that have the majority of their fund in IBIT. In fact, there are a few in there (not naming names) that have 100% of their fund in IBIT, which likely means no cross margin. In fact, the biggest reason to set up a fund to hold a single asset would be to isolate margin, so that if the trade blew up, the brokers wouldn't have claim to any other assets.

Interestingly, most of these giant, single asset funds are based in HK.

We know that Asian traders, particularly in China, have been deeply involved in the Silver and Gold trade. Silver was down 20% today, which was the 2nd largest 1 day move in a very long time (largest on Jan 30). We also know that the JPY carry trade has been unwinding at an increasingly rapid pace.

This leads me to think that the culprit for the IBIT blowup today was 1 or more HK-based non-crypto hedge funds. As @FranklinBi pointed out, the fund(s) being non-crypto would explain why no one sniffed them out. They would likely have few/no crypto counterparties, meaning complete isolation from CT.

The last small piece of evidence I have is that I personally know a number of HK-based hedge funds that are holders of $DFDV, which had the worst single down day ever, with a meaningful mNAV decline. The mNAV had been holding steady surprisingly well throughout this pull back until today. One of these fund(s) could have been connected to the IBIT culprit, as I highly doubt a fund taking that large of a position in IBIT and using a single entity structure would only have the one fund.

Now, I could easily see how the fund(s) could have been running a levered options trade on IBIT (think way OTM calls = ultra high gamma) with borrowed capital in JPY. Oct 10th could very well have blown a hole in their balance sheet, that they tried to win back by adding leverage waiting for the "obvious" rebound. As that led to increased losses, coupled with increased funding costs in JPY, I could see how the fund(s) would have gotten more desperate and hopped on the Silver trade. When that blew up, things got dire and this last push in BTC finished them off.

I have no hard evidence here, just some hunches and bread crumbs, but it does seem very plausible. Let's see if some more concrete evidence floats to the surface here soon. The smoking gun will be a large fund fitting this profile filing a 13F showing a giant IBIT holding going to zero. Unfortunately, if a fund had their IBIT position liquidated today, they wouldn't have to disclose the position change until 45 days after the quarter end, so we'd be looking at mid May for the smoking gun from 13F filings most likely.

Hopefully some of you out there with too much time on your hands this weekend can snoop around more. My guess is that word will start to get out, because something of this size is just too hard to hide. Additionally, if the broker was not able to liquidate the fund in time, the broker may have a hole in their balance sheet, which would be even more difficult to hide.

BREAKING: Bitcoin has erased the entire gain it made since Trump won the election.

BTC pumped 78% after Trump became president and is now back at the same level as November 2024.

If GOP passed the clarity bill in Dec/Jan all this mess would not be there at all !! They love to help institutions not crypto community who voted them. 😡 @DavidSacks@JDVance@saylor