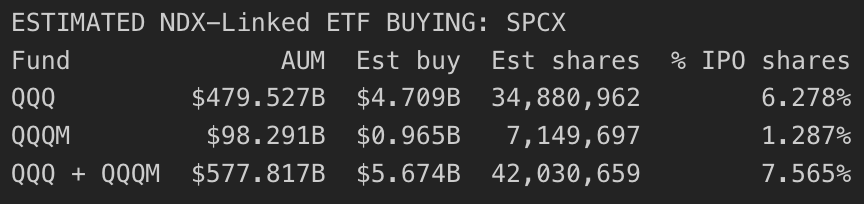

$SPCX could force $5.6B of day-one buying from QQQ and QQQM alone:

The IPO filing points to 555.6mm shares at $135.00, or $75.0B of IPO value.

Using the IPO shares as the free float input, the low-float 3x cap would put the NDX weighting value at $225.018B.Against the current NDX base, that maps to an estimated 0.985% weight, ranking ~25th in the index.

For QQQ, with roughly $473.3B of AUM, that implies about $4.7B of $SPCX buying, or 34.5mm shares. QQQM adds another ~$968mm of estimated buying, or 7.2mm shares.

Combined QQQ + QQQM demand would be about $5.6B, or 41.7mm shares, equal to 7.51% of the IPO shares available.

That’s just on day one from two funds.Of course, this is subject to change.

Actual demand will mostly depend on where $SPCX trades when Nasdaq evaluates it for inclusion, likely around its 7th trading day under the new fast entry rules.

People don't have to own. Make salaries low for export, and they live in social housing like cattle.

We're gonna own factories and nice living.)) Losers. God bless eu

socialistic social housing projects have a common lifespan of around 100 years (feels like) in the east. pragmatists and architects united and build thousands of these type of housing. not pretty, but modern. and they still around everywhere.

🚀 European credit funds saw €1.9bn of net inflows last week

The breakdown (week ending 13 May):

🔵 EUR IG: €711mm

🔵 EUR HY: €1.02bn (!!)

🔵 Strategic: €236mm

🔴 GBP IG: flat at £16mm

HY leading the charge at 1% of AUM in a single week. That's the strongest weekly flow since early 2024.

Are you positioned for spread compression or sitting this one out?

#CreditStrategy #BondFlows

What we’ve been seeing over the last seven months is not a pure discretionary “rotation” story, as much as a mechanically driven movement of risk tied to factor exposures across active managers and systematic strategies.

The apparent liquidity "hot potato" is really capital being forced to migrate as institutional portfolios (multistrat and equity) rebalance around factor constraints (growth, momentum, sector, quality, duration, beta, countless others) under conditions of declining macro liquidity. Capital mechanically sloshing around in a leaking pool.

As flows concentrate in a given factor (eg, mega-cap growth early on), crowding increases, correlations tighten, and marginal returns compress. When that factor stalls or volatility rises, risk models, VaR constraints, and performance pressures force managers to rotate exposure elsewhere. The new destination is not necessarily "fundamentally better", it is just the next available bucket with capacity and some upside sensitivity / marginal trend.

This is why the progression has followed such a structured liquidity-driven path. From Mag 7 (pure growth + duration) in Sept 2025 , to financials (rate sensitivity), to defensives (low volatility / quality / yield proxies), to cyclicals and real assets, and now into semiconductors. Each move was a shift in factor expressions hidden by meme of sector rotation. We've done the full tour.

These moves have been amplified by thinning macro liquidity since q3 2025, and the square root law of market impact. This allows smaller reallocations across factors to create disproportionately large price moves, reinforcing momentum and drawing in additional systematic and other benchmark-driven capital. This creates the illusion of strong conviction, when in reality it is reflexive positioning driven by portfolio construction constraints.

The “hot potato” effect emerges because no manager can afford to be early in de-risking while performance (and high water mark / compensation) benchmarks are still being driven by whichever factor is currently in favor. Capital is effectively forced to chase the marginal winner, even as the underlying macro backdrop weakens. This keeps flows moving, but with diminishing breadth and increasing fragility.

That flow is now concentrated into semiconductors.

What you are seeing is not clean exposure to "innovation", but the final concentration of multiple crowded factors (eps growth, momentum, capex beta, AI meme) all layered on top of each other. This is the heart of the AI trade. There is no “bigger” conceptual trade available. This is the defining expression of the entire market zeitgeist.

That’s what makes this stage particularly unstable in my view.

If semiconductors begin to roll over after collecting all this flow, it represents the simultaneous unwind across the most crowded and defining macro factors in the market.

When that happens, the same mechanisms that forced capital into the trade will force capital out of it, and there is no obvious alternative factor(s) left within equities to absorb that flow.

At that point, it is plausible the hot potato leaves the equity complex altogether and rotates into duration, volatility, or uncorrelated defensives, likely in a far more disorderly fashion due to the thin liquidity backdrop.

In some ways this marks the final battleground of State vs Capital.