Me crucé con esto, Messi está casi 6 desviaciones estándar por encima de la media de delanteros de grandes ligas en cuanto a goles y asistencias en 90 minutos. Estadísticamente es prácticamente imposible que vivas para ver a alguien así

In einer grossen Studie wurde untersucht, wie sich die Leistung von über 26'000 Schülern in China während 30 Monaten veränderte, wenn sie anfingen, KI-Chatbots zu nutzen.

Ihre Hausaufgaben wurden rund 20% besser.

Sie benötigten für die Hausaufgaben rund 20% weniger Zeit.

Das ist super.

Aber: Bei Prüfungen (wo KI verboten ist) wurden sie rund 20% *schlechter*. Das ist eine massive Verschlechterung.

KI kann Denkkompetenz aufbauen, wenn sie als eine Art Tutor eingesetzt wird. Dann spricht man von kognitivem Scaffolding.

Die Realität ist aber, dass die Strategie des kognitiven Offloading der Weg des geringsten Widerstands ist: Denkarbeit an Chatbots auszulagern, ist instrumentell gesehen rational. Ein Fehlanreiz.

Diese Entwicklung ruiniert Bildung. Und sie ist ein systemisches Risiko: Was passiert, wenn eine ganze Generation noch weniger als frühere Generationen lernt, eigenständig zu denken?

Die letzte Folge der Anstalt war ein Meisterstück. Die berühmte Tafel hat KathErina (das E steht für EON) Reiche kompakt demaskiert was wir schon alle wussten. Nicht nur als Lobbyistin, sondern als das was sie Habeck immer vorgeworfen hat:

Ideologin

Sollte JEDER gesehen haben👇

200 Quadratmeilen Wüste. 15.000 Arbeiter. Eine eigene Entsalzungsanlage, ein eigenes Glasfasernetz, Roboter, die zweimal am Tag staubfrei wischen. Und Solarmodule, so weit das Auge reicht.

Willkommen im Khavda Renewable Energy Park in Indien. Dem größten Kraftwerk, das die Menschheit je gebaut hat.

30 Gigawatt. Solar und Wind kombiniert, auf einer Salzwüste in Gujarat, betrieben vom Adani-Konzern. 13 Gigawatt sind bereits am Netz. Das allein wäre schon mehr als die gesamte installierte Solarleistung mancher europäischer Länder.

Aber es wird noch verrückter. Weil tagsüber mehr Strom produziert wurde als verkauft werden konnte, hat Adani in neun Monaten die vermutlich größte Netzbatterie der Welt gebaut. 1,1 Gigawatt Leistung, 3,5 Gigawattstunden Kapazität. Offiziell in Betrieb seit diesem Monat. Bis April 2027 sollen weitere 10 Gigawattstunden dazukommen. 13,5 Gigawattstunden Batteriespeicher an einem einzigen Standort.

Der Grund für die Batterie: Tagsüber ist der Strom billig, weil die Sonne scheint und alle Solaranlagen gleichzeitig liefern. Abends wird der Strom teuer, weil die Nachfrage steigt und Solar wegfällt. Adani speichert jetzt den billigen Tagesstrom und verkauft ihn abends zu Marktpreisen. Das ist kein Subventionsmodell. Das ist ein Geschäftsmodell.

Adani-Nachhaltigkeitschef Arun Sharma sagt es so: "Wir machen nichts auf Megawatt-Ebene. Auch nicht auf Hunderte-Megawatt-Ebene. Wenn es nicht Gigawatt ist, haben unsere CEOs nicht die Aufmerksamkeitsspanne dafür."

Und Khavda ist nicht allein. In der chinesischen Provinz Qinghai, auf dem Tibetischen Plateau in 3.000 Metern Höhe, steht der Talatan-Solarpark. Über 17 Gigawatt, auf einer Fläche von sieben Manhattan. Die Höhe ist kein Nachteil, sondern ein Vorteil: Die Sonne strahlt intensiver als auf Meereshöhe, und die kalte Luft macht die Solarmodule effizienter. Unter den Modulen grasen Schafe.

In Kalifornien plant der Westlands Water District einen 21-Gigawatt-Solarpark auf brachliegenden Agrarflächen im Central Valley, deren Wasser versiegt ist. Aus einem Wasserproblem wird ein Energieprojekt.

Stellt euch das vor: 30 Gigawatt Erzeugung plus 13,5 Gigawattstunden Speicher an einem einzigen Standort in Indien. 17 Gigawatt auf dem Dach der Welt in China. 21 Gigawatt auf ehemaligem Farmland in Kalifornien. Vor fünf Jahren galten Projekte mit einigen hundert Megawatt als Rekorde.

Die Solarenergie hat die Gigawatt-Schwelle durchbrochen. Und sie kommt nicht wieder zurück.

Quellen: Canary Media / New York Times / Adani Green Energy / https://t.co/kMQChukfVD

Today at #GoogleIO, I shared how we’ve been laying the building blocks for the future of agentic commerce with Universal Commerce Protocol (UCP), Agent Payments Protocol (AP2), and our new Universal Cart.

Am 22. September verspricht Kasachstans Präsident dem US-Präsidenten eine Wolfram-Mine.

36 Tage später kaufen Trumps Söhne Anteile an der Firma, die sie bekommen wird.

9 Tage später wird der Deal mit 1,6 Milliarden Dollar Steuergeld offiziell.

Drei Mal innerhalb eines Jahres dasselbe Muster: Söhne kaufen ein, Vater liefert den Auftrag.

Im August 2025 steigen Donald Trump Jr. und Eric Trump bei einer kleinen New Yorker Baufirma namens Skyline Builders ein. Sie kaufen über ein Vehikel mit dem Namen American Ventures, einer Tochter von Dominari Securities. Dominari hat die Trump-Söhne Ende 2024 in seinen Beirat geholt. Sie halten dort auch einen Anteil am Mutterkonzern.

Skyline ist zu diesem Zeitpunkt eine unauffällige Holding für asiatisches Baugeschäft. Niemand schreibt darüber.

Am 22. September trifft Kasachstans Präsident Tokayev Donald Trump und sagt ihm zu: Eine US-Investmentgruppe namens Cove Kaz wird das größte unentwickelte Wolfram-Vorkommen der Welt bekommen. Cove Kaz hatte gegen chinesische und russische Bieter konkurriert. Tokayev entscheidet sich für die Amerikaner.

Diese Zusage ist informell. Kein Vertrag, kein offizieller Beschluss. Nur ein Versprechen zwischen zwei Präsidenten.

Am 21. Oktober berichtet die Presse erstmals über diese Vereinbarung.

Sieben Tage danach, am 28. Oktober, schießen die Trump-Söhne weiteres Geld in Skyline nach. Im Rahmen einer Kapitalerhöhung von knapp 24 Millionen Dollar.

Drei Tage später, am 31. Oktober, kauft Skyline für 20 Millionen Dollar einen 20-Prozent-Anteil an einer Firma mit, Zitat aus dem Filing, "bedeutenden Beständen an kritischen Mineralien in Asien". Diese Firma ist Kaz Resources, die Tochter von Cove Capital, die das Wolfram-Projekt entwickeln wird.

Am 6. November verkünden Cove Kaz und Kasachstan den Deal offiziell. 70 Prozent der Mine gehören Cove. 30 Prozent dem kasachischen Staat. Geplante Investitionssumme: 1,1 Milliarden Dollar.

Die US-Regierung steigt mit ein. Die staatliche US-Exportbank gibt eine Zusage über bis zu 900 Millionen Dollar Projektfinanzierung. Die staatliche US-Entwicklungsbank ergänzt das mit bis zu 700 Millionen Dollar. Macht zusammen bis zu 1,6 Milliarden Dollar Steuergeld.

Am 30. April 2026 fusionieren Skyline und Cove Kaz. Das fusionierte Unternehmen geht an die Nasdaq. Geplanter Ticker: KAZR.

Auf keiner einzigen Pressemitteilung tauchen die Namen der Trump-Söhne auf.

Warum Wolfram?

Wolfram ist das Metall mit dem höchsten Schmelzpunkt der Welt. Es steckt in panzerbrechender Munition. In kinetischen Abfangkörpern für Raketenabwehr. In Hyperschallwaffen. In jedem Halbleiter. In F-35-Triebwerken. Christopher Ecclestone, Bergbau-Stratege bei Hallgarten in London, sagt: Das Pentagon will Wolfram um jeden Preis.

China kontrolliert über 80 Prozent der weltweiten Wolfram-Produktion. Im Februar 2025 verhängt Peking Exportbeschränkungen. Die Preise für Ammoniumparawolframat, der internationale Benchmark für Wolfram, springen seitdem um über 40 Prozent.

Die USA haben 2015 die letzte eigene Wolfram-Mine geschlossen. Wer eine neue, verlässliche Quelle anzapfen kann, sitzt auf einer goldenen Ader.

Genau diese Ader bekommen die Söhne des US-Präsidenten. Mitfinanziert mit Steuergeld.

Der Geschäftsführer von Cove Capital, Pini Althaus, sagt der Financial Times wörtlich: Cove habe "direkte Unterstützung von Präsident Trump, Außenminister Marco Rubio und Handelsminister Howard Lutnick" erhalten, um die Mine zu sichern.

Lutnick selbst hat einen persönlichen Brief an den kasachischen Präsidenten geschickt, um den Deal zu unterstützen. Das geht aus einer Investorenpräsentation hervor, die Skyline bei der US-Börsenaufsicht eingereicht hat.

Pini Althaus hat übrigens vor Cove eine andere Mineralienfirma gegründet: USA Rare Earths. Auch sie hat Mitte 2025 über 1,5 Milliarden Dollar an konditionaler US-Staatsförderung erhalten.

Das ist der Hintergrund. Jetzt zum Muster.

Im August 2025 steigt eine Risikokapitalfirma namens 1789 Capital bei einem Startup namens Vulcan Elements ein. Donald Trump Jr. ist dort Partner. Vulcan stellt Magnete aus Seltenen Erden her.

Drei Monate später, im Dezember 2025, bekommt Vulcan einen Pentagon-Kredit über 620 Millionen Dollar. Plus 50 Millionen Dollar als Eigenkapitalbeteiligung der US-Regierung. Es ist der größte Kredit, den das zuständige Pentagon-Büro für strategisches Kapital je vergeben hat. Trumps Executive Order 14241 hatte zuvor die Pflicht zur unabhängigen technischen Prüfung solcher Vergaben aufgehoben.

Im März 2026 steigen die Trump-Söhne bei einem Drohnenhersteller namens Powerus ein. Lieutenant General Keith Kellogg, ehemaliger Sicherheitsberater des Vizepräsidenten, sitzt im Beirat. Wenige Wochen später startet die US-Regierung ein Drohnenprogramm mit einem Budget von 1,1 Milliarden Dollar. Powerus will Aufträge daraus ziehen. Der geplante Börsenticker der Firma: PUSA.

Jetzt Cove Kaz. KAZR. 1,6 Milliarden Dollar Steuergeld.

Drei Fälle. Zwölf Monate. Dasselbe Muster.

Das Wall Street Journal hat die Trump-Familien-Geschäfte seit der Wiederwahl auf insgesamt mindestens vier Milliarden Dollar Erlöse und Papiervermögen geschätzt. Krypto, Drohnen, Seltene Erden, Wolfram, Bitcoin Mining, Prediction Markets. Eric Trump hat in einem Interview gesagt, sie hätten in der ersten Amtszeit "keinen Dank für ihre Zurückhaltung bekommen". Diesmal halten sie sich nicht zurück.

Im März 2026 versuchen Demokraten im Kongress, Donald Trump Jr. per gerichtlicher Vorladung zu zwingen, unter Eid zum Vulcan-Deal auszusagen. Republikaner blockieren die Abstimmung im Ausschuss.

Die rechtliche Bewertung dessen wird Jahre dauern. Zwei Dinge stehen aber jetzt schon fest.

Erstens: Wer in den USA steuerpflichtig ist, finanziert über Mehrheitsstrukturen einen Bergbau-Deal in Kasachstan, an dem die Söhne des Präsidenten beteiligt sind. Ohne dass diese Beteiligung in den offiziellen Pressemitteilungen erwähnt wird.

Zweitens: Wenn dasselbe Muster in einem Jahr drei Mal auftritt, ist es kein Zufall. Es ist eine Methode.

Wenn dich solche Makro Insights interessieren und dir helfen, interagiere gerne mit dem Post. 🧡

Everyone's been waiting for "the European Amazon" for 20 years.

Turns out it might be a discount grocery chain.

Dutch Central Bank just picked Lidl as its cloud provider. Not AWS. Not Google. Not Microsoft. Lidl.

The reason: trust in US tech is eroding across European institutions. Data sovereignty rulings, the political climate, tariff drama. Every quarter the case for sitting on top of US infrastructure gets harder to defend.

So Europe is decoupling. Quietly. Contract by contract. While everyone watches the political theatre.

Lidl pulled in nearly €2B from cloud last year. All infrastructure built inside the EU.

The "European alternative" people have been waiting for?

Turns out it's a grocery chain that's been quietly investing for years.

If a discount supermarket can win central bank cloud contracts, is US big tech's moat in Europe thinner than anyone admits?

Last place anyone was looking. First to deliver.

Bugatti just lost its all-time speed record. To the Chinese EV in this video. 308 mph at Papenburg, on a battery.

The Chiron Super Sport had held the record for six years. 1,600 hp, 8.0L W16, four turbochargers. Bugatti needed every horse of that to hit 304 mph. BYD's Yangwang U9 Xtreme did 308 with four electric motors and a battery pack.

Marc Basseng, the driver, won the Nürburgring 24 Hours. He said the run was "technically not possible with a combustion engine." He's right.

A combustion engine produces a power curve that peaks at a specific RPM and falls off either side. Past 9,000 RPM the valves float, the connecting rods stretch, the pistons can't reverse direction fast enough. The W16 is the absolute thermodynamic ceiling of 100 years of internal combustion. Every mph past 290 cost exponentially more engineering for diminishing returns.

The U9 Xtreme uses four electric motors. Each produces 744 hp. Each spins to 30,000 RPM. No valves. No pistons. No connecting rods. Total system output is 2,978 hp, almost double Bugatti's W16. Power-to-weight is 1,217 hp per tonne.

The motors were never the hard part. Mate Rimac said this years ago. The constraint was always the battery, because to deliver 2,978 hp into four wheels you have to discharge faster than any production EV ever has.

BYD built the world's first 1,200-volt production car. Everyone else uses 800V. The Blade Battery runs lithium iron phosphate cells with a 30C discharge rate, ten times what a conventional EV battery handles. Heat generation falls 67% versus 800V at matching output.

That last number is the whole game. Heat is what kills high-power EV runs. Other automakers derate within seconds at full power because the battery cooks itself. BYD's architecture lets the Xtreme hold maximum discharge long enough to actually approach the aerodynamic limit of the chassis.

Bugatti spent 20 years engineering the W16 to its physical ceiling. BYD spent 18 months building the architecture that cleared it.

They're making 30 of them.

The crown for fastest production car on Earth has belonged to Bugatti, Koenigsegg, Hennessey, SSC. All combustion, all European or American. The crown is Chinese now, and it runs on a battery.

The Universal Commerce Protocol is taking a major step in building the future of agentic commerce with the expansion of its Tech Council. Welcome to @Amazon, @Meta, @Microsoft, @Salesforce and @Stripe.

The success of UCP is an industry-wide effort that requires a true ecosystem approach. Welcome to the new partners joining us to build the future of agentic commerce! 💪

☠️ ANTHROPIC HAT GERADE EBAY ERLEDIGT!

Das ist der Chart von $EBAY. Minus 5,3 Prozent. An einem Tag. Von $103,40 runter auf $97,94. Kein Earnings. Kein Skandal. Kein Insider-Verkauf. Nur ein Forschungs-Paper von Anthropic.

"Project Deal" heißt das Ding.

Anthropic hat in seinem San-Francisco-Büro einen Marktplatz für die eigenen Mitarbeiter gebaut. 69 Leute. Je 100 Dollar Budget. Klassisches Craigslist-Setup. Nur mit einem Twist: Die Verhandlungen führt Anthropic. Nicht der Mensch. Die KI kauft, verkauft, dealt für dich. 186 Transaktionen in einer Woche, über 4.000 Dollar Volumen.

Und ein interessantes Detail aus dem Paper: Wer einen schwächeres Modell bekam, machte nachweislich schlechtere Deals. Hat es aber selbst nicht gemerkt.

Klingt nach Büro-Spielerei. Ist es nicht.

Es ist ein Proof of Concept dafür, dass jeder Marktplatz im Netz austauschbar ist. eBay verdient Geld weil Menschen eBay brauchen, um zu handeln. Was, wenn Menschen nichts mehr machen müssen?

Wall Street hat verstanden. Sofort.

Alles, was Marktplatz ist betroffen. Salesforce ist seit Januar 33 Prozent runter, weil "Claude Cowork" die ganze CRM-Industrie in Frage gestellt hat. Adobe minus 36. ServiceNow gerade von UBS auf Neutral runtergestuft. Der Software-Index IGV ist 35 Prozent unter seinem Hoch.

Eine ganze Branche wird vor unseren Augen umgeschrieben.

Wall Street hat dafür schon einen Namen. SaaSpocalypse. Seit Januar 2026 sind ungefähr 2 Billionen US-Dollar aus der Software-Wirtschaft verdampft. Zwei Billionen. Und das Spiel fängt grade erst an.

Was Wall Street gerade einpreist: Pro-Seat-Lizenzen verlieren ihren Sinn, wenn ein Agent eine ganze Abteilung ersetzt. Plattform-Take-Rates kollabieren, sobald Agenten direkt mit Agenten verhandeln. Werbung verliert ihre Logik in einem Markt ohne menschliche Klicker. Was bleibt sind Infrastruktur-Anbieter, Daten-Besitzer und die Modell-Hersteller selbst.

Und genau da kommt der nächste Schlag.

Anthropic hat letzte Woche Opus 4.7 vorgestellt. Sonnet 5 ist seit Anfang April live. Das Roadmap-Leak von vor zwei Monaten zeigt interne Referenzen auf Sonnet 4.8 und Claude 5 - geplant für den Sommer. Google hat parallel angekündigt, bis zu 40 Milliarden Dollar in Anthropic zu investieren. Das ist ein All-In auf die Disruption der eigenen Cloud-Kunden.

Bei OpenAI läuft das gleiche Spiel, nur lauter. Sam Altman hat im März bei BlackRock öffentlich gesagt, sie trainieren in Abilene, Texas, das nach eigener Einschätzung beste Modell der Welt. Übersetzt: GPT-6. Release-Fenster: Ende Mai. Was die Modelle laut Roadmap können sollen? Selbstständige Workflows. Bezahlsysteme. Buchungen. Verhandlungen. Komplexe Transaktionsketten ohne menschliche Aufsicht. OpenAI hat parallel mit Etsy und Shopify die ersten Pilot-Integrationen für agentic shopping gestartet. Du sagst ChatGPT was du brauchst, ChatGPT kauft. Ohne Klick auf Etsy.

Und du musst dir die Frage stellen, welches Geschäftsmodell das überlebt.

Marktplätze überleben so nicht. Wenn ein Agent für mich kauft, brauche ich keine Plattform mit Suchfunktion und Verkäufer-Reviews. SaaS-Lizenzen pro Sitzplatz fallen genauso. Wenn 10 Agenten die Arbeit von 100 Sales-Reps erledigen, braucht keiner mehr 100 Salesforce-Logins. Werbung wird ein Nullsummenspiel. Agenten klicken keine Anzeigen.

Wie schnell diese Unternehmen sterben, ist die einzige offene Frage.

Ich sehe drei Szenarien.

⚠️ Erstens: Die Plattformen integrieren die Agenten und werden selbst zur Infrastruktur. eBay wird zum reinen Settlement-Layer für Claude und GPT. Möglich. Aber die Margen brechen weg.

⚠️ Zweitens: Die Plattformen sterben langsam und Anthropic plus OpenAI werden selbst zum neuen Marktplatz. Wahrscheinlich. Wer die Schnittstelle besitzt, besitzt den Kunden. Und die zwei sammeln gerade die Schnittstellen ein.

⚠️ Drittens: Eine ganz neue Asset-Klasse setzt sich durch. On-Chain. Programmierbar. Permissionless. Wo Agenten ohne Custodian und ohne Plattform handeln können. Krypto war von Anfang an für eine Welt gebaut, in der Maschinen Geld bewegen. Keine andere Schiene kann das aktuell.

Ich bin etwas besorgt 🫠.

https://t.co/no3JK9V7iH

NEW: Astronaut Reid Wiseman shares a video of ‘Earthset’ that was taken with his iPhone

“This is uncropped, uncut with 8x zoom which is quite comparable to the view of the human eye…” Wiseman said.

This has to be the greatest iPhone video of all time.

Every day for the next long while, I'm going to tear down a new public software company and highlight the AI risks/opportunities around it- products launched to date, top startups, key quotes from earnings calls, etc.

Long one for the weekend!

Day twenty-four: Salesforce $CRM

Peak share price: $361.99

Share price today: $182.14

EV today: $157bn

ARR today: $44.8bn

NRR: Undisclosed

EV/ARR: 3.5x

GAAP Operating Margin: 17%

EV/Run-rate GAAP EBIT: 21x (!!)

Headcount: 87,042 (+10% Y/y)

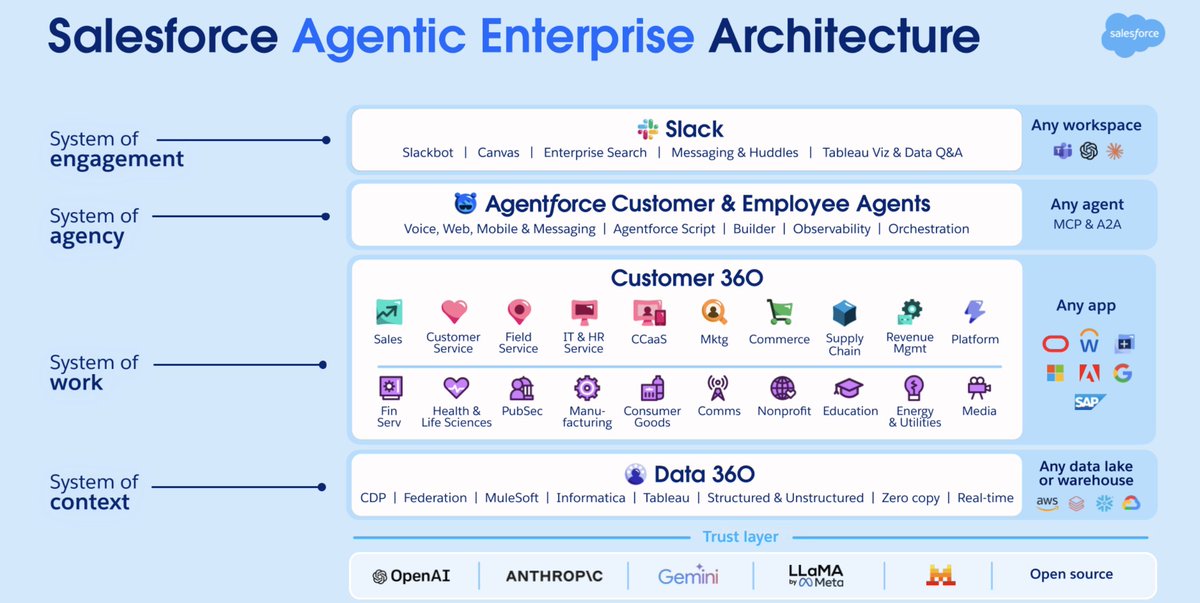

What Salesforce does:

It may surprise casual observers, but Salesforce's "CRM" business is only 20% of revenue today, with the rest scattered amongst customer service software (22%), the Frankenstein segment called "Agentforce 360, Slack and Other" (24%), e-commerce and marketing (12.5%) and Mulesoft+Tableau (16%).

In short, Salesforce has to be analyzed as a diversified conglomerate of quite disparate business units, and AI impacts will be particularly difficult to measure. Much of the business outside of sales/service was built inorganically, with notable acquisitions including:

Slack - $27.7bn - Chat for business

Mulesoft - $6.5bn - API management/iPaaS

Tableau - $15.7bn - BI/analytics

ExactTarget - $2.5bn - Email marketing

Demandware - $2.8bn - E-Commerce Software

Informatica - $8bn - Legacy Mulesoft (!!)

and literally dozens of smaller ones.

Incredibly, Salesforce spent 40% of today's enterprise value on just those six acquisitions enumerated above.

AI bear case:

Given the complexity of evaluating so many independent business lines, the overarching bear case for Salesforce is actually more cultural than product-specific. While some Salesforce products seem remarkably well-positioned for the AI age (i.e. Slack), and others perhaps more challenged (i.e. Tableau), the toughest aspect of Salesforce is the cultural headwinds associated with being a massive conglomerate of different businesses and frankly ham-handed marketing and execution to date. Renaming each business line "Agentforce X" is one of the most hilariously corporate things I've seen a software company do in the AI age. Considering the pace of change and the assorted fears about SaaS, Salesforce seems uniquely challenging to manage/steer through this world, and frankly, some of the business lines (looking at you, Demandware/ExactTarget/Tableau) were already challenged even before AI.

AI bull case:

Cultural challenges aside, Salesforce has deep relationships with many of the world's largest enterprises and a clear #1 position in enterprise "front office" software (i.e. CRM) which is perhaps more insulated from AI than "back office" software that is associated with cost-centers (a la ServicenNow). Though it will of course move slower, there will still be plenty of time before any of its core businesses are truly under threat, and relative to the software titans of yore (i.e. Oracle/SAP), its software is mostly cloud-native and can be updated over the air, making it easier to catch up.

Finally, Slack looks like a tour-de-force acquisition in a world where chatting with AI becomes a key part of enterprise workflows- Salesforce may be able to turn it into a key insertion point, at least for the set of companies that use it over Microsoft teams.

AI traction:

Salesforce reported Agentforce ARR of $800, up 169% Y/y. I'll note that AI revenue is fairly easy to overstate for a company as large as Salesforce, since large enterprise customers may view spend fungibly and be happy to shift it into the "good" back in exchange for discounts, etc. This was endemic when Oracle/Microsoft were transitioning to "cloud," for instance- even though both efforts were ultimately successful.

Adjacent AI-native startup summary:

This is a truly intimidating section considering the breath of Salesforce's portfolio, and true no AI native company has expressed a vision that would lead to it duplicating Salesforce's various business lines over time.

It remains true that there is no one scaled startup on a trajectory to displace Salesforce in CRM. @attio is perhaps the buzziest CRM startup and a great company, but with 169 employees growing 67%, it remains small in absolute terms and @HubSpot is likely the real competitor to watch, at least in the mid-market.

In CX, the picture is muddier with various AI native starts like @SierraPlatform, @parloa_ai, @DecagonAI, @intercom (yes, now AI native) etc. all growing nicely. My sense is that their combined AI revenue is still smaller than reported Agentforce revenue, though they may have more "real" revenue in production as a group. This is certainly the category to watch as the AI native vendor threat is most acute.

Elsewhere- Tableau is under clear direct threat from @sigmacomputing, @_hex_tech and @omni, and some have longer term fears about what AI means for BI/analytics as categories.

Management Quotes:

"We're using our remarkable cash flows to take advantage. This is not our first SaaSpocalypse. We have been through many SaaSpocalypses. I remember the horrible SaaSpocalypse of 2020 when not only the software industry was dying, but we were all dying, but we made it through that. And now everyone is back, doing great. So we're so grateful to make it through that, and we're going to make it through this one as well. And it's just in a great marketing opportunity and a great buying opportunity, and that's why we are doing this incredible repurchase authorization of $50 billion."

"If you haven't seen the new Agentforce, you haven't seen Agentforce, the level of determinism, the voice capabilities, Agentforce Studio, Agentforce Builder. We are spending a huge amount of time on Agentforce. I just saw the new Agentforce demos from our team. It was incredible. We even have Agentforce running in Slack. We have Agentforce Builder running in Slack. We have amazing things happening."

"Introduced Agentic Work Units (“AWUs”) to measures tasks accomplished by an AI Agent, with 2.4 billion AWUs delivered to date across Agentforce and Slack, growing 57% quarter-over-quarter ("Q/q")"

"Salesforce has processed more than 19 trillion tokens to date, up 5x Y/y"

"Agentforce accounts in production increased nearly 50% Q/q"

"And the third way is for customer-facing agentic use cases, agents, which sell fuel, the credits, Flex Credits. And companies, if you look at the bookings of Agentforce in Q4, 50% were credits, Flex Credits, fuel; and 50% were higher SKUs."

Commentary:

There are three ways for things to play out for Salesforce. In one scenario, AI native startups (along with nimbler incumbents) come out like piranhas and take chunks out of each of its core businesses. Though there is business-by-business nuance and much can change with time, so far this seems to be a threat only to the CX business.

In the second scenario, Salesforce executes modestly well and muddles through- not leading the way but also taking smart steps, eventually figuring out Agentforce and investing in AI where it is working.

In the third scenario, Salesforce pulls something special off and proves to be more than the sum of the parts in an AI-native world, building a full agentic architecture for the enterprise.

In honesty, I see long odds of the third outcome and little evidence for it to date. Unfortunately, Salesforce's acquisitions have been very mixed in quality and remain quite disjointed today, making a cohesive vision hard to see or build. It would arguably be better for the company to jettison certain products (Tableau, Demandware) and refocus on the AI, advantaged ones (Slack, perhaps CX/CRM, etc.).

So the question for Salesforce is whether scenario #1 or #2 plays out- my gut is that #2 should be achievable, but that there is risk of misexecution creating #1. The bottom line is that big enterprise system-of-record businesses do have time to react to the new world, and so, to some degree, their destinies are in their hands.

Welcome Salesforce Headless 360: No Browser Required! Our API is the UI. Entire Salesforce & Agentforce & Slack platforms are now exposed as APIs, MCP, & CLI. All AI agents can access data, workflows, and tasks directly in Slack, Voice, or anywhere else with Salesforce Headless 360. Faster builds, agentic everything. 🚀

#Salesforce #Agentforce #AI

https://t.co/mxySdJS7HR

Map of Chongqing's metro system in 3D.

Chongqing is called the "mountain city". Building metro here is more difficult than in plain cities.

Chongqing’s metro total length ranks 7th in the world, with over 550 km.