You may want to check out the newly launched Journal of Privat Markets Investing. The lastest journal launched by the original Institutional Investors Journals (now @PM_Research_), JPMI will quickly become THE resourse for best investment practices within the 'Alts' space. It's a spin-off from II/PMR's Journal of Portfolio Management, Edited since '86 by Frank Fabozzi, and will be Edited by Mr. Fabozzi's protege (my observation) - Prof. Michael Imerman.

I would suggest we need natural leaders, courageous leaders, principled leaders. Not self-appointed ones. Those that lived their principles. First principles. Timeless principles.

America needs a natural aristocracy.

Aristocracy just means “rule by the best” and Joe Lonsdale argues that it is an idea that is unduly demonized. Artificial, hereditary aristocracies are indeed a corrupting force, but to reject the idea that the most competent should rule is equally dangerous. By rejecting Aristocracy altogether, we don’t unleash democracy we get bureaucracy: a geriatric slop that will suffocate a civilization if not eradicated. This is what is plaguing America today.

@JTLonsdale is the closest thing you’ll find to a Roman senator, someone who acts courageously in politics, commerce, and the military informed by a classical understanding of virtue. And this interview will tease out Lonsdale’s political philosophy that underlies all of his ventures: Palantir, UATX, Cicero and 8VC.

Timestamps:

1:50 Change Requires a Demanding Philosophy

3:17 America’s Problem: No Aristocracy

8:34 In a World of Machiavellis, Be a Cyrus

10:51 The World Can’t Afford Our Absence

21:43 Democracy Dies in Bureaucracy

30:48 How Cicero Institute Writes Philosophy Into Bills

32:38 Measuring Who Gets Help First

44:04 When Buyers Become Too Powerful

50:04 The Philosophy Behind Palantir

This is really important, and why diversification and staging your investments over multiple rounds is so important not only to manage the downside, but to capture and lean into the upside.

Venture doesn't run on leverage.

It's asymmetric: you can only lose 1x, but you can potentially make 1,000x.

In the math, overwhelmingly the error that matters is the error of omission.

There’s also evidence of “widespread misbehavior” as well!

"This is the first study that seeks to document the downside of the current pattern of VC contracting, where VCs receive very large amount of discretion in exchange for a mere promise not to misbehave. We cannot measure the extent of VC misbehavior itself, but we can study the tip of the iceberg – litigation – showing allegations of widespread VC misbehavior."

https://t.co/hY5XHqty0v

“This place seems like exactly the kind of learning place that Charlie Kirk was trying to turn every American campus into.” — @SteveDoocy@foxandfriends

How about you just bundle all that into 'lack of professionalism and/or professional standards & practices'. That should do it... After all, there are no professional standards & practices in the venture industry. No training required. No certification (that can be pulled) if there was unprofessional behavior. There is no training required. No body of knowledge to study to understand how to manage risk better, or how to define an objective, data-driven investment process that avoids FOMO.

If we want freedom to remain the world’s dominant operating system, we should fund it like our lives depend on it.

Government programs and frameworks (like ESG) can’t solve problems that are really about our ability to build and compete. Capitalism can.

Investors have the long-term orientation and risk appetite needed to rebuild our industrial base, strengthen our supply chains, and scale the technologies that matter.

Here’s why we need a new lens:

- We once led in 60 of 64 critical technologies. Now China leads in 57.

- We rely on fragile or adversarial regions for critical materials and manufacturing.

- ESG isn’t enough. We need GCI. We need capital that plays offense.

- Venture can lead but pension funds, endowments and other large capital pools must follow.

VC is the only job I know where you "do" mostly nothing for years, are wrong on most of things you do actually do, and can then return hundreds of millions of dollars seemingly by accident.

venture capital went from weirdos at the fringes of society investing in semiconductors to harvard educated spreadsheet jockeys doing occult excel macros to value brick and mortar private equity rollups at software multiples because the deck said "ai" 25 times.

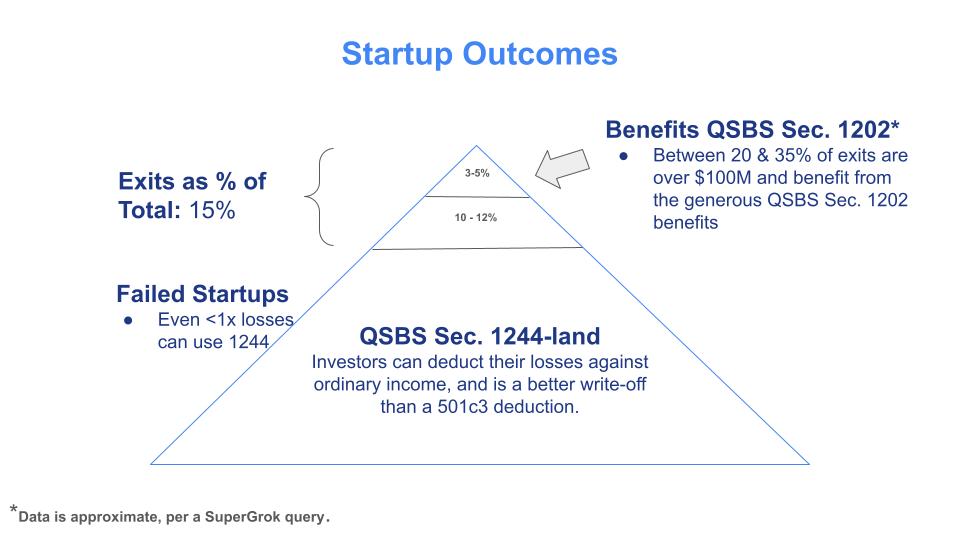

@harris ....and show how act 1 investment $s can be de-risked via QSBS Sec. 1244 (losses can be written off against taxable income for the first $1M of investors' $s.

@lukefischer Don't overlook the original QSBS incentive - QSBS Sec. 1244 - which de-risks early stage investing by allowing losses to be written off against ordinary income, while Sec. 1202 impact maybe 2% of investors.

@cartainc Don't overlook the original QSBS incentive - QSBS Sec. 1244 - which de-risks early stage investing by allowing losses to be written off against ordinary income, while Sec. 1202 impact maybe 2% of investors.