* 99% of the biggest winning stocks were above their 200 day moving average when they made their big moves.

* And 96% above their 50 day moving average.

I have no desire to fish anywhere else.

From Trade Like a Stock Market Wizard @markminervini

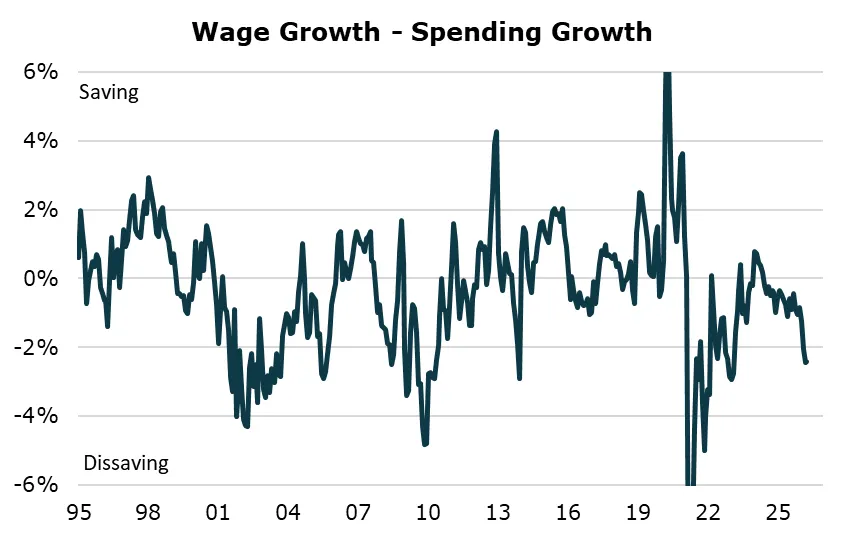

Households on A Knife's Edge

Real incomes are now contracting, but households have kept up spending so far. Without income or price relief, their choice of whether to keep dissaving will define the US economy in 2H26.

https://t.co/yj7U3lcam7

The Economist on the U.S. economy’s consistent growth outperformance relative to other advanced countries:

“America’s outperformance began decades ago, but in the 2020s it has become vast. And it is likely to last. The latest IMF forecasts show American growth besting the rest all the way to 2030 and beyond….

Many of America’s advantages are hard to emulate. The country’s continental scale, single language, natural-resource wealth and the fiscal space that comes from issuing the world’s safe asset give it a unique economic advantage over Europe…

But America also shows just how much other rich countries are failing to live up to their economic potential.”

#economy @EconUS@TheEconomist

⚡️U.S. outperformance is real, durable, and more structurally important than most people want to admit.

America is winning because it can metabolize chaos faster than everyone else.

That is the whole secret.

Europe is optimized for preservation.

America is optimized for mutation.

Europe protects the existing social model. America lets capital, talent, fraud, ambition, violence, speculation, startups, monopolies, bubbles, immigrants, engineers, universities, military spending, energy production, and financial markets collide until something enormous breaks through.

That produces ugliness. It also produces scale.

The U.S. can create OpenAI, Nvidia, SpaceX, Tesla, Palantir, Anduril, Apple, Amazon, Microsoft, Google, Meta, BlackRock, shale, Bitcoin infrastructure, venture capital networks, and world-dominating financial markets in the same civilizational machine. Europe can produce excellent engineers, beautiful cities, strong welfare states, industrial champions, and high living standards. But it struggles to create world-eating firms in the new layers of power.

That is the gap.

The Economist is late because this was visible years ago. The 2020s did not create U.S. dominance. They exposed the compounding. AI, cloud, energy, defense tech, capital markets, reserve currency privilege, fiscal capacity, demographic absorption, and China’s slowdown all pushed the world’s marginal capital back toward America.

The biggest structural advantage is the dollar. The U.S. issues the asset the world needs in crisis, then uses that privilege to finance deficits, defense, liquidity, innovation, and consumption. Everyone complains about U.S. excess. Then they buy U.S. assets when the world gets dangerous.

That is empire mechanics.

Europe’s problem is deeper than weak growth. It has lost speed. Too much regulation, too little risk, aging populations, expensive energy, fragmented capital markets, weak tech platforms, defense dependence, demographic tension, and political systems designed to block extremes rather than produce new engines. Europe is not dead. But it is increasingly downstream of American tech, American defense, American liquidity, and American risk appetite.

America’s contradiction is brutal: the system is globally dominant while many households feel poorer, angrier, and less secure.

That is why people miss the signal. They look at broken housing, debt, health care, crime anxiety, inflation, political dysfunction, and conclude America is failing. At the household layer, many things are degrading. At the system-power layer, America is pulling further ahead.

Both are true.

Markets care more about the system-power layer until social breakdown starts impairing earnings, labor, politics, or bond confidence.

So the real investment implication is clear: U.S. assets keep attracting global capital because the U.S. still owns the future-facing engines. AI, defense, energy, software, capital markets, and hard-asset monetary escape routes remain American-centered.

Europe can rally cyclically.

America owns the structural premium.

Why SPY feels unstoppable as of early 2026 -

70M US active 401(k) participants =

• $10.1 trillion in 401(k) plans

• $19.2 trillion in IRAs

• $49.1 trillion total US retirement assets

• Foreign ownership of US equities: ~18-20% (pensions & institutions worldwide buy S&P

This is the Revenge of the Old Economy in real time.

A super cycle already underway before Hormuz closed.

Brent will break out. The security premium is not transitory.

Three drivers. Not fading. Intensifying.

Deglobalization. Electrification. Redistribution.

All three turbo-charged versus our 2020 super cycle call.

We are still in the bottom of the first inning. None of the imbalances have been resolved. They grow by the day.

Own the grains/softs. Own the metals. Own the molecules.

Remember, you cannot print molecules https://t.co/XQpR4p4HPL.

10/10

Pettis’ point is that global imbalances are a system. One country’s surplus is another country’s deficit. So the fix cannot be “America borrows less” while China, Germany, Japan, or other surplus blocs keep suppressing domestic demand and exporting excess savings.

1. Surplus countries must raise domestic demand

China’s surplus exists because domestic consumption is too weak relative to production. That is usually caused by households receiving too small a share of national income, while the state, firms, banks, and local governments control too much of the surplus.

So China needs to shift income toward households through higher wages, stronger social safety nets, less reliance on property and infrastructure investment, and less financial repression.

In plain terms: Chinese workers need to consume more of what China produces.

Without that, China keeps exporting its imbalance abroad.

2. Deficit countries must stop absorbing the surplus passively

The US cannot keep acting as the global balance sheet that receives everyone else’s excess savings.

That means the US has to reduce the attractiveness of pure financial inflows that inflate assets without building productive capacity. Capital entering the country should be pushed toward productive investment, infrastructure, industrial capacity, energy systems, advanced manufacturing, and tradable sectors.

Fiscal tightening without industrial rebuilding just crushes demand while leaving the productive deficit intact.

3. Capital inflows need to be filtered

The issue is what kind of capital enters and what it does once it arrives.

Capital that builds factories, ports, energy systems, mineral processing, chip capacity, rail, grid infrastructure, and productive supply chains helps resolve the imbalance.

Capital that buys existing assets, Treasuries, housing, equities, private credit, and speculative claims deepens the trap.

So the resolution is a capital-allocation regime that favours productive capital over balance-sheet inflation.

4. Trade adjustment must rebuild production, not just punish imports

Tariffs alone are too blunt. Sure they are leverage but they don’t rebuild domestic adjustment you need to combine tariffs or import discipline with:

domestic procurement rules, industrial credit, energy cost reduction, skills formation, tax incentives for tradable investment, supply-chain mapping, and public-private coordination around strategic sectors. Which we are seeing

Otherwise tariffs just raise prices while the industrial base remains too weak to respond.

5. The monetary framework must stop privileging asset stability over productive capacity

If the central bank and financial system keep rewarding asset protection, low consumer inflation, cheap imports, and liquidity expansion, while ignoring industrial complexity, external dependency, and productive investment, then the imbalance recreates itself.

So the deeper resolution is institutional: monetary and financial policy must measure whether credit is expanding productive capacity or merely inflating claims on existing assets.

China has to consume more. America has to build more. Capital has to be redirected from claims on production into production itself.

This is politically difficult because both sides have powerful domestic winners from the current system.

In China, the winners are exporters, state firms, local governments, banks, and investment-heavy sectors.

In the US, the winners are finance, asset owners, import-dependent corporations, consumers of cheap goods, and the Treasury market itself. The FOMC in its bid to financialize everything has selected for state vassalage . Instead of dying of shame Powell is so clueless about what he’s led the Republic into he wants to stay on

So the imbalance resolves either through deliberate restructuring or through crisis: protectionism, defaults, currency stress, debt deflation, unemployment, and political rupture. My guess is war.

For the record.

Iran’s Historic Mistake

Carl von Clausewitz wrote that war is “the continuation of politics by other means.” President Trump grasped this from the start: Operation Epic Fury exists to stop Iran’s nuclear march and restore deterrence, not to pursue the familiar neocon fantasy of occupation and nation-building. Epic Fury is peace through strength in action: credible force applied decisively when adversaries mistake restraint for weakness.

By weaponizing the Strait of Hormuz, Iran committed a strategic blunder of historic proportions.

Tehran meant to punish America. Instead, it exposed every power built on imported energy, vulnerable sea lanes, and the delusion that globalization repealed geography. China is exposed. Europe is exposed. Britain is exposed. Iran has created a world where hard resource power decides outcomes.

Start with China. Beijing’s industrial machine depends on imported oil and gas moving through vulnerable maritime chokepoints, the old Malacca dilemma in modern form. A great power reliant on long, exposed sea lines cannot be secure, regardless of economic scale. The Hormuz shock forced China to scramble for alternatives, proving that size is not resilience.

Europe and Britain face the same problem. After escaping Russian dependency, they traded one vulnerability for another, leaning on imported LNG and maritime flows exposed to coercion. When chokepoints tighten, they absorb shocks rather than project strength. European criticism says less about American failure than about discomfort with a world where hard power still matters.

Iran’s mistake is that once Hormuz becomes structurally unreliable, the world builds around it. That means bypass corridors, revived pipeline politics, and urgent planning for routes linking Aqaba to Mediterranean outlets near Gaza and the long-stalled Basra-to-Aqaba pipeline. The old energy order is cracking. The UAE’s OPEC exit signals cartel discipline giving way to national advantage under pressure.

Trump deserves credit, not European scolding. Operation Epic Fury struck thousands of targets, degraded Iran’s offensive capabilities, and shattered assumptions that the West would absorb escalation without response. The administration acted while others lectured. It restored deterrence in the only language Tehran understands.

The larger lesson matters more. Secure natural-resource hard power is what the Western Hemisphere possesses in abundance. The United States, Canada, and the Americas command hydrocarbons, LNG, farmland, freshwater, critical minerals, and strategic depth on a scale import-dependent Europe and Asia cannot match. This crisis clarified, not weakened, the Americas structural position.

The financial dimension reinforces the point. Demand for Federal Reserve swap lines during crisis proves King Dollar remains supreme. When stress hits, governments run toward dollar liquidity, not away from it. Hard resource power and monetary power reinforce one another, and the United States sits at the center of both.

That is Epic Fury’s real significance. Clausewitz wrote that “the political view is the object, war is the means.” Trump understood that. Iran tried to weaponize geography, Trump turned the confrontation into a demonstration of who is exposed and who is not.

The Trump administration deserves far more praise than it has received, and history will likely judge that Iran’s greatest miscalculation was not merely closing Hormuz, but revealing which powers still command the real sources of strength.

Central Bankers they don’t serve capitalism. They serve their own interests.

If capitalism were their aim, we would have built stronger industries, deeper productive capacity, and a broader class of owners, makers, engineers, farmers, builders and manufacturers.

Instead, the system was selected for deindustrialisation. It rewarded financial extraction over production, asset inflation over wages, imports over national capability, and dependence over sovereignty.

In the 17th century, a serf might work three days for the manor house. Today, many workers spend a similar portion of their lives working for the bank.

The name and firm have changed, but the system is familiar. The modern worker is chained to his shelter by debt, rent, mortgages, fees, inflation and financial claims created by institutions that contribute little to the real economy.

In a systemic sense, they are patristic; sure, they provide capital, though in this cycle, they provided capital to financialise the systems indentured workers.

The banks don't support the economy. Too often, they sit above it. They create credit, expand asset prices, collect interest, and then claim they are the indispensable engine of prosperity.

But when finance grows too large, it stops funding production and starts feeding on it. We stopped funding production decades ago.

Which is the cycle? Every time banks and financial interests overstep, they become too greedy. Every time they become too greedy, they distort the economy. Every time they distort the economy, the political class eventually protects them instead of the public. Then the technocratic class arrives to justify the arrangement with complicated language, models, forecasts and moral lectures.

But the outcome is fewer real industries, fewer independent producers, fewer competitive markets, and more dependence on a narrow class of financial and technological gatekeepers.

Hamilton understood the importance of productive industry. Eisenhower warned against concentrated power and the military-industrial machine. Robert Menzies understood that national strength required more than consumption and financial speculation.

Leaders of the past, whatever their flaws, often understood something many modern leaders have forgotten: liberty is not built on debt, dependence and imports. Freedom rests on the ability of a people to make things, defend themselves, feed themselves, power themselves and not be permanently beholden to foreign suppliers or domestic financiers.

A nation that cannot produce is not truly sovereign. A nation that cannot manufacture becomes strategically weak. A nation that sells off its productive base and calls the result “efficiency” is not modernising, it is dismantling its own state.

When production and finance fall out of balance, rivalry becomes inevitable. Nations that lose their industrial base become insecure. Nations that dominate supply chains become aggressive. Financial elites profit from instability, while ordinary people pay the price through inflation, unemployment, debt and war.

Central banks and financial institutions may not print ammunition directly, but they create the conditions that make conflict more likely. They inflate assets, punish workers, reward speculation, and push nations into dependency. Then, when the imbalance becomes dangerous, the same class that caused the instability presents itself as the only class capable of managing it.

Real capitalism requires competition, productive investment, broad ownership, failure for the incompetent, reward for the capable, and markets that are not permanently rigged in favour of insiders. But most of the modern economy is not that. It is dominated by duopolies, monopolies, cartels, too-big-to-fail banks, captured regulators, and technology platforms that behave more like private governments than companies.

Capitalism exists as an ideal, and at certain points in the economic cycle, it briefly appears. But it rarely remains pure for long. Power concentrates. Finance captures politics. Corporations eliminate competitors. Banks socialise losses and privatise gains. The productive economy gets hollowed out while everyone is told this is progress.

A free society cannot survive on financial engineering, imported goods, inflated property values and digital monopolies. It needs productive strength. It needs industry. It needs skilled workers. It needs competition. It needs national independence. Above all, it needs a system where money serves the real economy, not the other way around.

Once finance becomes the master rather than the servant, liberty begins to disappear. And once a nation forgets how to make things, it eventually forgets how to defend itself.

With $40 trillion in debt, a war in the Middle East and rising inflation, the market should've crashed by now.

And if it did, your retirement account would drop 30-40% like it did in 2008.

But 4 forces built into the system prevent this from happening.

Each one explained:🧵

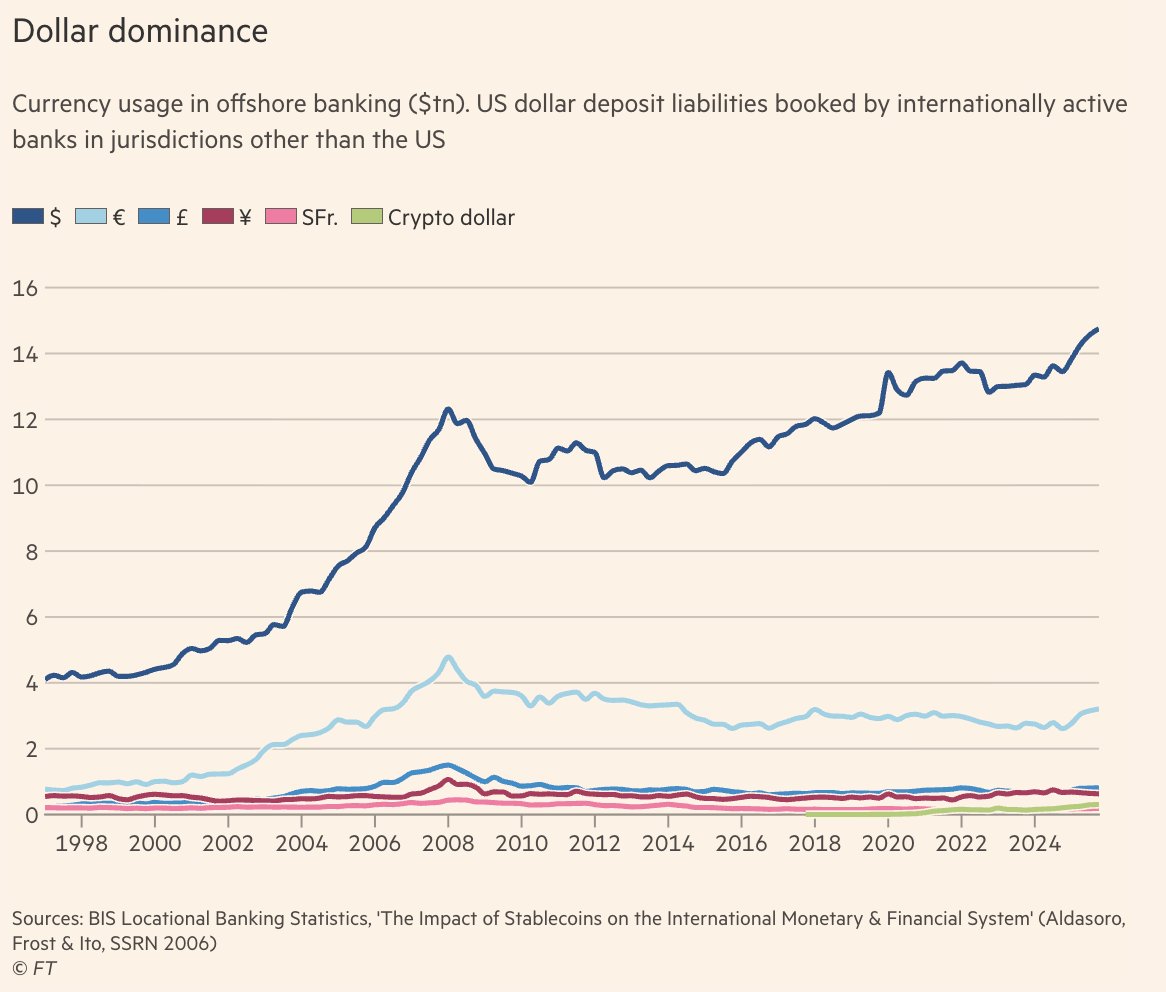

There has been too much talk of petrodollars.

And not enough talk of Chinese dollars

China isn't really de-dollarizing. Rather the contrary.

A new blog

1/

https://t.co/6NT3Onlp9U

Despite all the noise about de-dollarization, the FT reports that offshore dollar deposits just SURPASSED 14 TRILLION DOLLARS.

The dollar is FAR AHEAD of any rival and its lead is INCREASING.

KING DOLLAR = REIGNS SUPREME.

Food for thought.

The age of cartel scarcity is ending

The United Arab Emirates’ decision to leave OPEC is not just another quarrel inside an oil cartel. It is a move in the New Great Game taking shape across energy, trade routes and strategic commodities.

For years, Abu Dhabi accepted the logic of collective restraint. Saudi Arabia would lead, Russia would amplify, and other producers would sacrifice volume for price. That bargain worked while members shared the same goal: defend oil prices without destroying demand.

The UAE no longer fits the model. It has invested heavily to expand capacity, while OPEC+ quotas have limited its ability to monetise those barrels. ADNOC has targeted crude production capacity of 5mn barrels a day by 2027, while UAE production has often been restrained by OPEC+ agreements (EIA). Abu Dhabi wants to convert oil in the ground into sovereign wealth while demand still has value. The cartel wants patience. The UAE wants velocity.

That is the structural shift. The oil market is moving from price defence to market-share capture. The UAE is not leaving OPEC because it has lost faith in oil. It is leaving because it wants to sell more of it while the world still needs it.

Investors should separate the shock from the regime. In the short term, the Iran conflict drives prices because it determines whether barrels can move through Hormuz. If tankers cannot sail, spare capacity is theoretical. War risk, insurance costs and inventories set the front-month price.

But Iran does not define the long-term price structure. Wars create spikes; structures determine regimes. The structural story is bearish: OPEC is less cohesive, the UAE is more willing to chase volume, and the US is now the resource superpower OPEC once feared. The US became the world’s top crude producer in 2018 and produced a record 13.2mn barrels a day in 2024 (EIA).

For Donald Trump, the rupture is useful. A weaker OPEC means Saudi Arabia and Russia have less ability to manage prices. Lower oil is a tax cut for US households and a weapon against inflation. But Hormuz limits the victory lap. Trump can pressure cartels; he cannot repeal geography.

China sees the same map differently. It remains exposed to Gulf flows and needs reliable suppliers. Beijing has relied on discounted Iranian and Venezuelan barrels, but those supplies carry sanctions, shipping and insurance risk. A freer UAE can offer something more valuable than cheap crude: reliability.

This is the New Great Game in energy form. The US wants lower cartel power. China wants secure supply. The UAE wants autonomy and relevance in both capitals. Saudi Arabia wants to preserve cartel authority. Russia wants disruption to keep energy geopolitics in play.

The age of cartel scarcity is giving way to the age of market-share oil. The marginal barrel is no longer merely an economic unit. It is a geopolitical instrument.

Tariffs ended the old System.

The US/Middle East deals set template for the New System

OPEC ending + swap lines ramping are confirming signposts for the thesis laid out a year ago:

Technology

- The US provides allies with access to leading-edge Technology - the AI Tech Stack - which serves as the new defense and security umbrella.

- This mutually beneficial Technology sharing accelerates the growth of a secure, expanding "Western" ecosystem and prevents adversaries from accessing these critical tools.

Energy

- The Middle East provides the cheap and abundant energy required to power massive, energy-intensive AI infrastructure and data centers.

- This reliable supply of energy supports lower global prices, which helps streamline US reindustrialization and the reshoring of critical production.

Money

- The Middle East directs its capital surpluses to directly fund physical AI infrastructure and Critical Product manufacturing in both their region and the US.

- This system fundamentally shifts money flows away from unproductive financial assets toward productive physical capacity and labor

Confluence

- The unification of the separate Pillars establishes a balanced, non-zero-sum template for the New System that is focused on free trade, fair burden-sharing, and addressing each nation's unique deficits and surpluses.

- This synergy brings seemingly disparate strategic goals together, simultaneously boosting national security and expanding physical productive capacity across the globe

The Pillars of Power in action

Paul Tudor Jones says the US is more dependent on equity prices than ever, and explains what a 35% correction would trigger in the economy:

"We're 252% of stock market cap to GDP. In 1929 we were 65%. In 1987 we got to ~85-90%. In 2000, 170%.

If you think about the periodicity of significant bear markets. Since 1970, we get a mean reversion about every 10 years.

Let's say mean revert to the past 25 or 30-year PE. That would be a 30, 35% decline. Well, 35% on 250% of GDP is 80, 90% of GDP.

10% of our tax revenues are capital gains, they go to zero. So you can see the budget deficit blowing up. You can see the bond market getting smoked. You can see this kind of negative self-reinforcing effect.

In the stock market, we're over-equitized as a country. We have the highest individual equity weightings in the history of the country.

And then the real problem is if you look at private equity in 2007-2008, that was about 7% of institutional portfolios. Now it's about 16% of the institutional portfolios. We're so much more illiquid than we were in 2008.

The problem is that if you buy the S&P at this current valuation, the 10-year forward return is negative when you buy the S&P with a PE of 22. That's what history shows.

So yes, the S&P is spectacular long-term, if you have a hundred-year view. But that's because that's an average of a hundred years, including times when the S&P 500 PE was 6, 7 and 8, or one third of what it is right now.

Valuation matters a lot, and the stock market's really high and it's gonna be really hard to make money from here with any kind of long-term view."

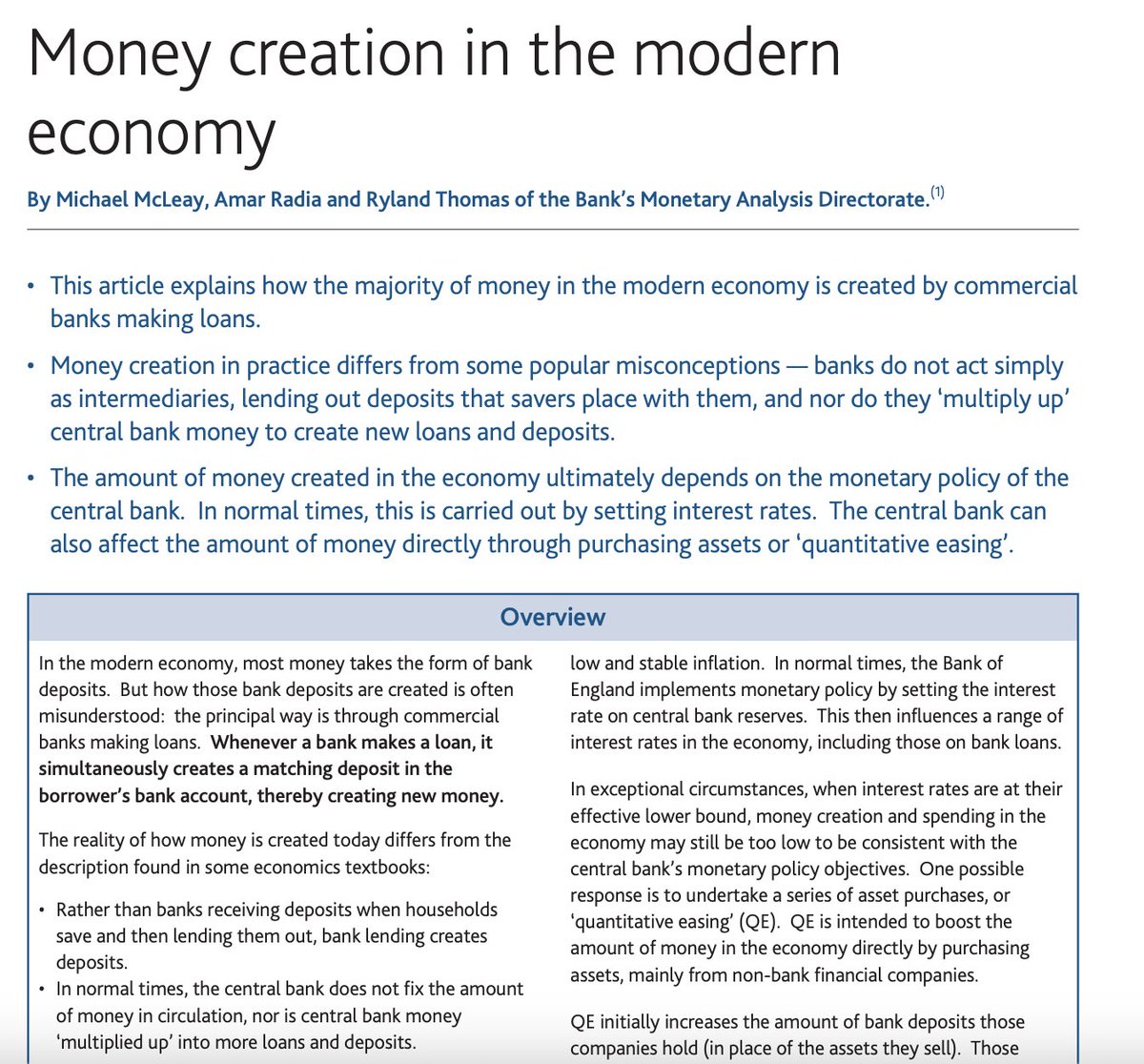

Just got off a zoom call catching up with a friend of mine from the Boy Scouts who is now a bank manager.

Told him that inflation has to be constant because loans create new money with interest and that interest has to be paid off somehow.

explained that even the bank of england has written papers describing exactly this process. they all admit this openly.

He was literally stunned and almost fell out of his chair.

"You mean money is lent into existence? every time a customer draws a line of credit they just print it? and the money supply is constantly increasing?!"

this is a guy who is a math major and works at a major bank.

even the people running the system don't know how it works.

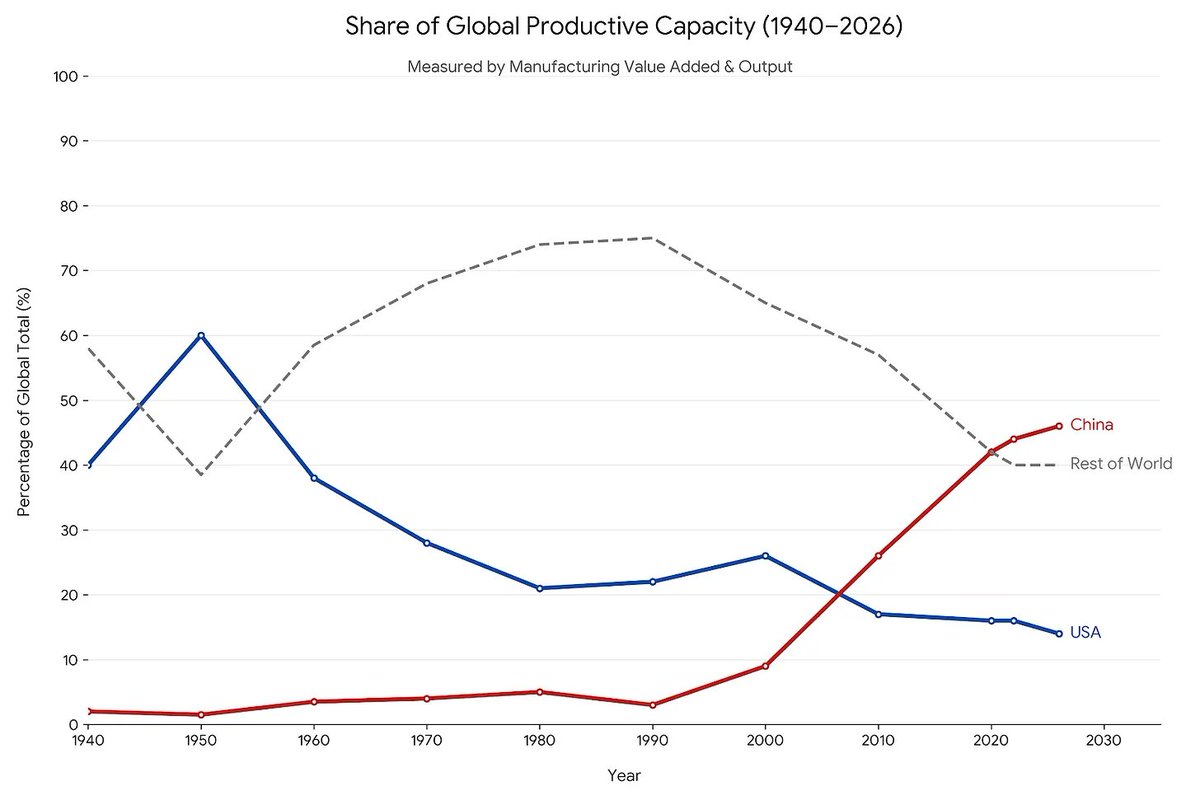

1/15 The greatest geopolitical shift of the last 25 years was a quiet transfer of physical reality.

To cut costs & boost margins, US Corporates sent their Productive Labor & Capacity overseas to China.

The West optimized for short-term efficiency, sacrificing long-term resilience

أعلى مستوى في التاريخ!

مع إغلاق مضيق هرمز:

🎯ارتفعت صادرات الولايات المتحدة من المنتجات النفطية إلى أعلى مستوى لها في التاريخ! (أنظر الرسم البياني أدناه)

🎯وارتفعت صادرات النافثا الأميركية إلى أعلى مستوى لها في الناريخ!

🎯وارتفعت صادرات الغاز المسال الأميركي إلى أعلى مستوى له في التاريخ

🎯وصادرات فنزويلا ترتفع إلى أعلى مستوى لها في 6 سنوات،

🎯وأسعار النفط الأميركي ترتفع بعد خطاب ترمب بشكل كبير، ويتجاوز سعر خام برنت، وهذه حالة نادرة!

إسمع:

الولايات المتحدة أكبر منتج للهليوم في العالم وتستعد الآن للتعويض عن كل الهليوم المصدّر من الخليج!