The $GFL / $SES.TO merger getting this contentious wasn't on my bingo card.

My position is unchanged: this isn't the optimal outcome for either party. That said, $SES.TO shareholders are getting a good price today. At 11x forward (announced price) or ~10.5x using current $GFL price, investors should take their ball and go home. For continued energy beta via OFS, I'd point you to $CEU.TO, a best-in-class specialty chemicals biz trading at 9.5x that's tied to production (vs. drilling activity), much like $SES.TO's base biz.

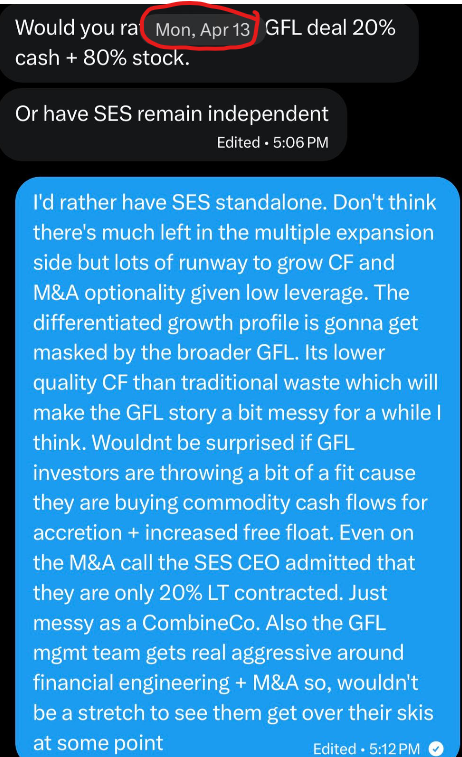

My comment below on preferring $SES.TO standalone is b/c a combo with $GFL is sub-optimal for both sides.

$GFL shareholders want truly non-cyclical CFs. Adding OFS pressures the multiple by muddying the story and weakens $GFL's ability to do accretive SW M&A, especially opportunistic M&A in economic downcycles.

For $SES.TO shareholders, the standalone growth profile gets watered down by the broader $GFL. That's not to say $SES.TO is a "waste" biz whose chart will grind up and to the right, as many suggest. When the next energy downcycle hits (and it will), the multiple will compress dramatically. But $SES.TO holders should be given the chance to trade around that growth profile and energy cycle volatility.

My near-term view on $SES.TO is positive: the Iran situation should inject a geopolitical risk premium into oil that we haven't seen in a decade+. Layer on renewed focus on security of supply, which will point major crude and products buyers to NAM. $SES.TO's core business will benefit because it supports Canada's long-life resource base and an oil price anywhere close to US$80 is great for basin-wide profitability and will support healthy activity levels.

If $SES.TO's multiple keeps grinding higher as generalists conflate commodity CFs in a constructive oil price environment with business quality, this opens the door to accretive M&A of actual waste assets and a longer-term pivot. That's the additional optionality in the $SES.TO thesis, but it requires that the oil price remains high enough for long enough. Once again, this highlights $SES.TO's exposure to energy beta.

Are you serious? I don’t know your CAGR and you don’t know mine — nor do I care. You could be -99% or +9,999% on the year and I’d still engage because this is my sector.

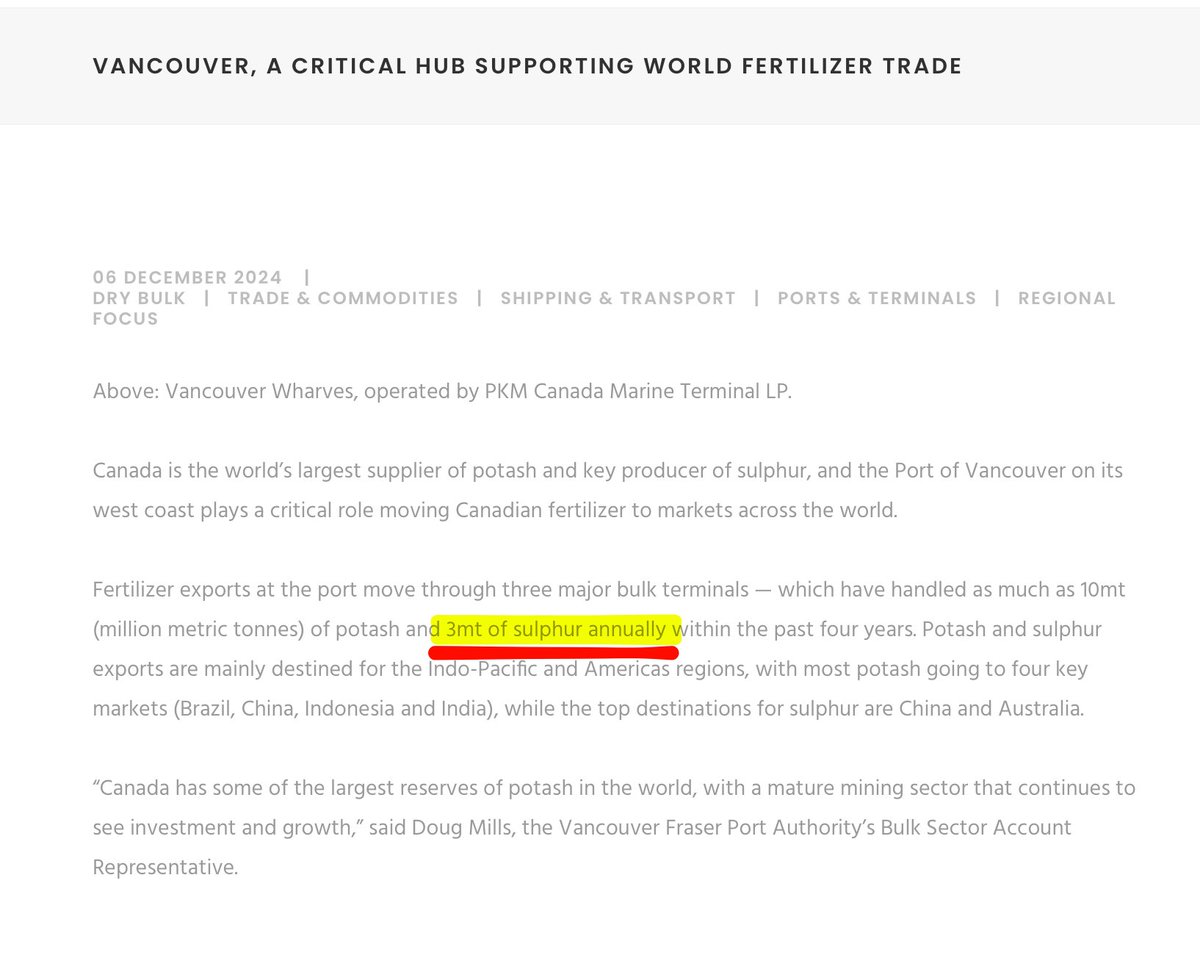

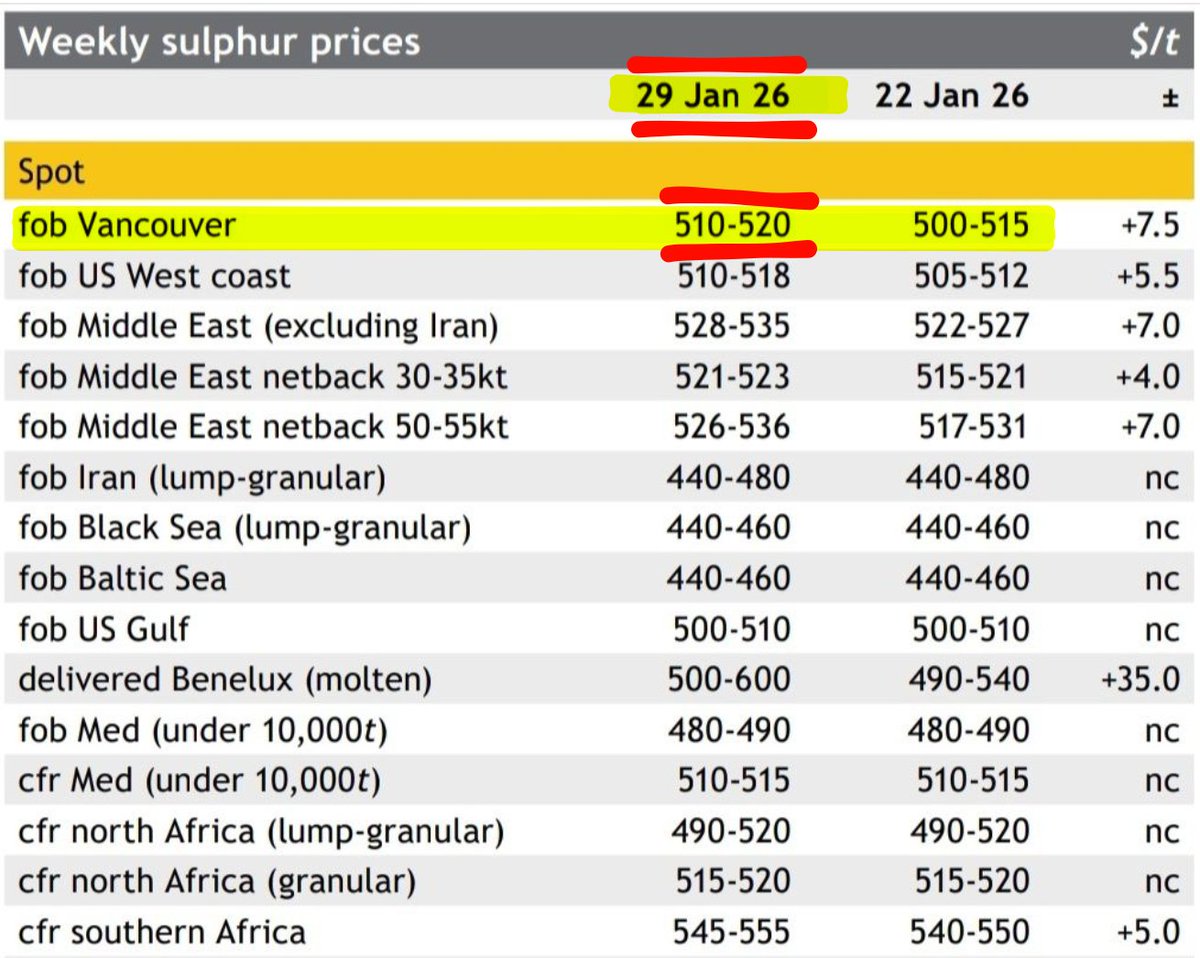

Why not take a minute to wonder why it's just accumulating there? In January of 2026, FOB Vancouver pricing was ~$500/t, that 10 million tonne pile would be $5 billion! So why weren't they selling it then?

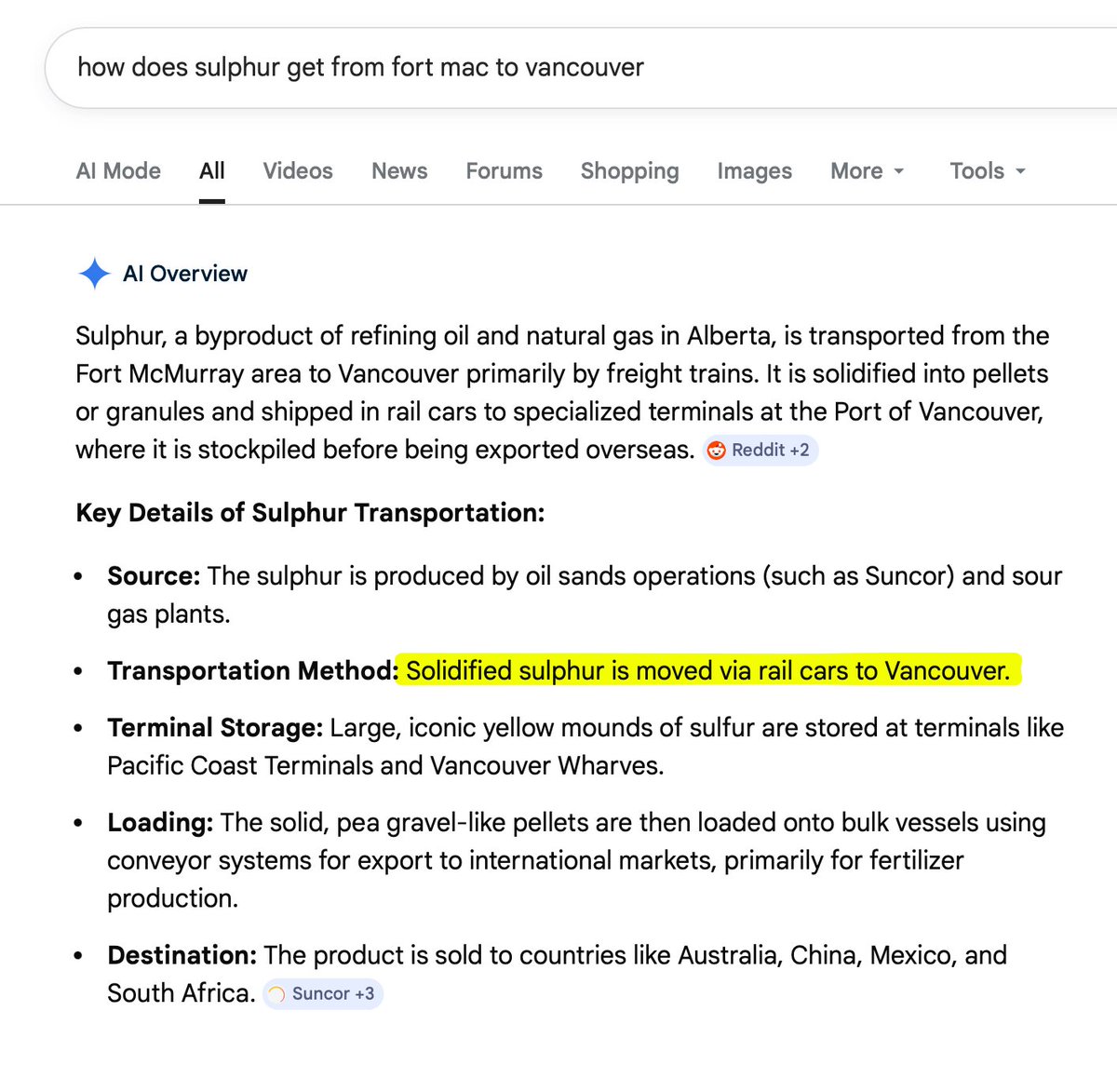

There’s a reason that it sits there; because you transport sulphur via rail to Vancouver, and then you need space at a dry bulk terminal. The Port of Vancouver can handle 3 million tonnes a year of sulphur exports. At that rate, if *just* Suncor owned the terminal (they don't), it would have >3 years to export their Suplhur.

But, Suncor isn't the only Sulphur exporter from Vancouver; and they're not the only oil sands mine in Fort Mac. In terms of free terminal space, there's ~2,000 tonnes a day of export capacity, if you're lucky, or 0.73mt/yr, so at that rate it'd take Suncor almost 15 years to sell their Fort Mac inventory.

But Suncor isn't the only Oil Sands mine with Sulphur, nor the only Sulphur producer in Alberta! So they're competing with everyone else for that terminal space.

And to even get to the Vancouver terminal; you need to rail your Sulphur. So you have 3 bottlenecks to get your Sulphur from Fort Mac to the Port of Vancouver; your rail terminal/transloading capacity, your ability to book rail cars, and your actual dry bulk terminal capacity in Vancouver.

And every single Sulphur producer in the province (i.e. everyone with an oil sands mine, refinery, or sour gas plant), is trying to export their Sulphur.

So you end up with highly depressed local prices for Sulphur (why Cavvy/Pieridae did their infamously poor deal with Shell) -- much like AECO gas, it's trapped in the province. You're effectively using TTF pricing to mark AECO reserves in the ground with no ability to land that gas in Europe. It's ridiculous and a fundamental misunderstanding of commodity markets.

Again, I don't know your returns, nor do I care; but if you're going to be so freaking cocky about a claim so bold, and tell me to "google it" -- at least make sure you're right, and have done at least one second-order google search yourself.

Trying to implement AI at a big bureaucratic organization:

Me: Copilot is useless, can we get Claude instead?

IT: No.

Me: but we could cut so many people if you let us use Claude.

IT: No. Case resolved. Ticket closed.

IT email: Please complete this short survey.

Please for the love of everything holy if you are an E&P do not do anything stupid.

Do not buy back your shares after running your cashflow at $110/bbl WTI. No they're not cheap. The time to buy back stock was every day over the last year.

Do not buy new assets. The time to buy new assets was every day over the last year.

Do not grow. If you couldn't grow over the last year economically, you are almost certainly not going to be able to maintain your new-found production levels when the market reverts. You are not the low cost producer.