We are about to experience a massive end-of-Q2 rebalancing period:

Institutional investors are estimated to sell up to $165 billion in equities and purchase an equivalent amount of bonds by quarter-end, the highest in at least 4 years, according to JPMorgan.

Japan's Government Pension Investment Fund (GPIF), with ~$1.9 trillion in assets, is estimated to sell ~$60 billion in equities, while Norway's Norges Bank, managing a ~$2.1 trillion sovereign wealth fund, is expected to sell ~$40 billion.

At the same time, US defined benefit pension funds, managing ~$9.6 trillion in assets, could account for another ~$55 billion in equity sales.

The Swiss National Bank is estimated to sell ~$25 billion, though this figure could fall to ~$8 billion if its equity allocation rises to 30% from the current 28%.

Meanwhile, balanced mutual funds, managing ~$4.0 trillion in assets, are estimated to purchase ~$15 billion in equities.

A massive quarter-end rebalancing wave is about to hit global markets.

The new Fed chairman’s first press conference was rather hawkish.

He came off as articulate and prepared, but tightly-phrased on most things (ie not giving a whole lot away) which is a style he previously foreshadowed.

Bit of a hit to rate-sensitive assets, which makes sense.

Interesting. The Trump SPR drawdown is sharp, but small compared to Biden's...

(As always, more interesting charts in the Wolf Street article, linked in reply below so X won't hide this post.)

🚨 Anthropic just showed a 27-minute workshop on how to actually do prompts for Claude.

Taught by the people who built it.

Free. No registration. No paywall.

I've seen $300 courses that don't cover what they teach in the first 8 minutes.

Watch it and bookmark it now.

My op-ed published in MoneyWeek today on helium. The commodity nobody talks about is quietly underpinning the space race, AI chips and the NHS. One third of global supply was wiped out overnight when Iranian strikes shut Ras Laffan. Spot prices doubled. SpaceX’s own S-1 doesn’t even mention it as a risk, despite Musk admitting there isn’t enough helium on Earth for his Starship ambitions. The UK has no domestic production, no reserve, and no critical minerals designation. That gap won’t stay invisible much longer.

https://t.co/eW9Q4KA1iQ

#SENTIMENT CAPITULATION

The Gold Miners Bullish Percent Index just hit 7.69. March was the only other time we saw a reading this washed out, and that marked a major sentiment reset in the miners. In simple English, most people have given up again. This is exactly what full capitulation feels like. Weak hands get forced out, sentiment gets cleansed, and the sector starts setting up for the next turn higher. These are never comfortable spots in real time, but historically this is the kind of panic zone where the best opportunities begin to form. @WSBGold

U.S. COMMERCIAL CRUDE oil inventories at refineries and tank farms along the Gulf Coast (PADD 3) have depleted by 20 million barrels since the middle of April compared with an average draw down of less than 3 million barrels over the previous ten years. The Gulf Coast is the country’s largest refining region and the most integrated with global seaborne crude markets. It is the most exposed to the global loss of supplies resulting from closure of the Strait of Hormuz. Inventories were exactly in line with the ten-year seasonal average on May 29 wiping out a surplus of 17 million barrels (+7% or +0.86 standard deviations) on April 17:

China cut raw dysprosium and terbium to Japan, It did not cut finished magnets - Read that again.

Japan can still buy the finished product from Chinese factories but cannot buy the raw material to make its own.

That trains Japanese manufacturers to stop making magnets and start buying them, Every month Shin Etsu does not get raw dysprosium is a month its customers switch to Chinese finished magnets.

The ban is not punishing Japan, It is converting Japan from a competitor into a customer.

Takaichi said in Diet that a Chinese attack on Taiwan would be a survival threatening situation for Japan. That was one sentence in one committee hearing.

Within two months China banned dual use exports, blacklisted 20 defense entities, and stopped shipping dysprosium, terbium, gallium, and yttrium. The chart goes from 200k kg bars to flat zero.

Every Indo Pacific government considering a public Taiwan position now has a cost model in front of it

Everyone focuses on dysprosium and terbium. Gallium is the harder problem. It is not mined directly. It comes as a byproduct of aluminium smelting.

China runs 90% of global gallium supply because it runs 60% of global aluminium. You cannot build a gallium mine, You need an entire aluminium smelting industry first.

Japan has neither, The chart shows gallium going to zero alongside the rare earths.

🚨 THE ENTIRE AI BOOM MIGHT BE BUILT ON FAKE REVENUE.

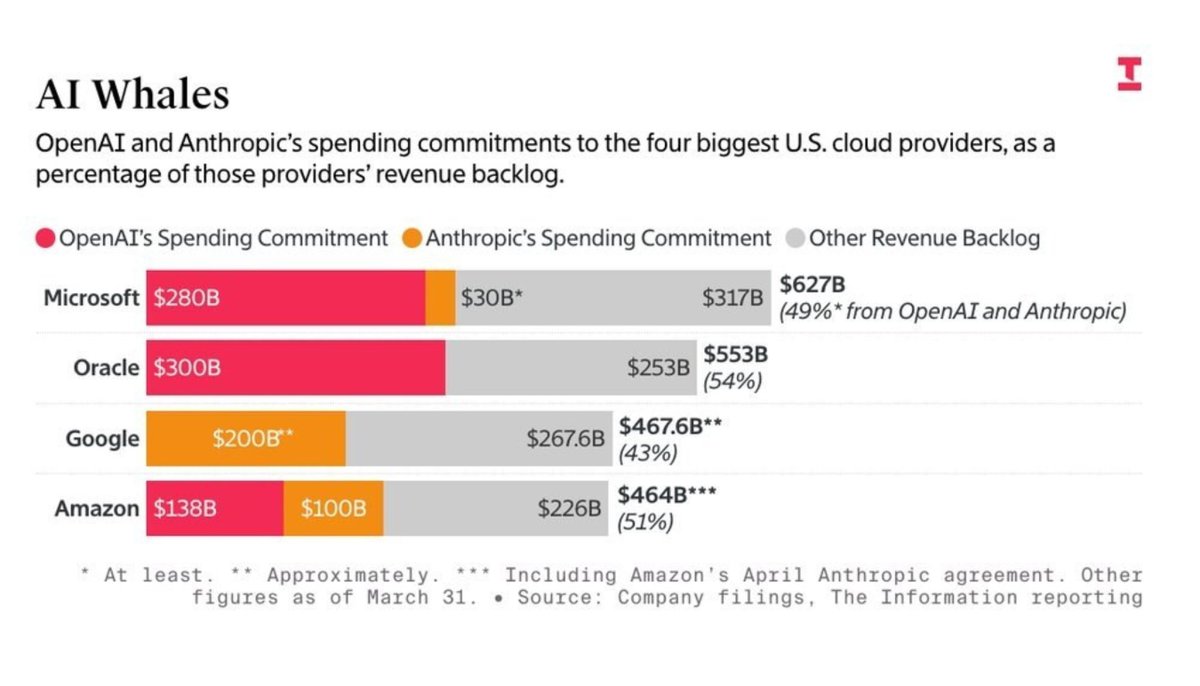

Latest corporate filings show that OpenAI and Anthropic alone make up over half of the entire $2 trillion future cloud backlog held by Microsoft, Oracle, Google, and Amazon.

This massive pipeline is actually being created through a circular accounting trick called a round trip revenue loop.

But how it works ?

A tech giant gives billions of dollars to an AI startup as an "investment". But hidden in the contract is a strict rule forcing the startup to hand that exact same money straight back to the tech giant to rent their computer servers.

Look at the documented case of Microsoft and OpenAI.

When Microsoft invested $13 billion into OpenAI, it didn't just give them cash; it gave them "cloud credits" to use Microsoft servers. OpenAI used those exact credits to train its AI models, and Microsoft then turned around and recorded that server usage as brand new "cloud revenue" from a customer.

The tech giant is literally paying itself with its own money and calling it a sale.

This is why OpenAI’s annual cloud bill has ballooned to over $60 billion, double its actual revenue of $25 billion, kept alive solely by this recycled funding loop.

Anthropic runs the exact same play, spending $2.66 billion on Amazon Web Services in just nine months, which was basically 100% of all the money it earned at the time.

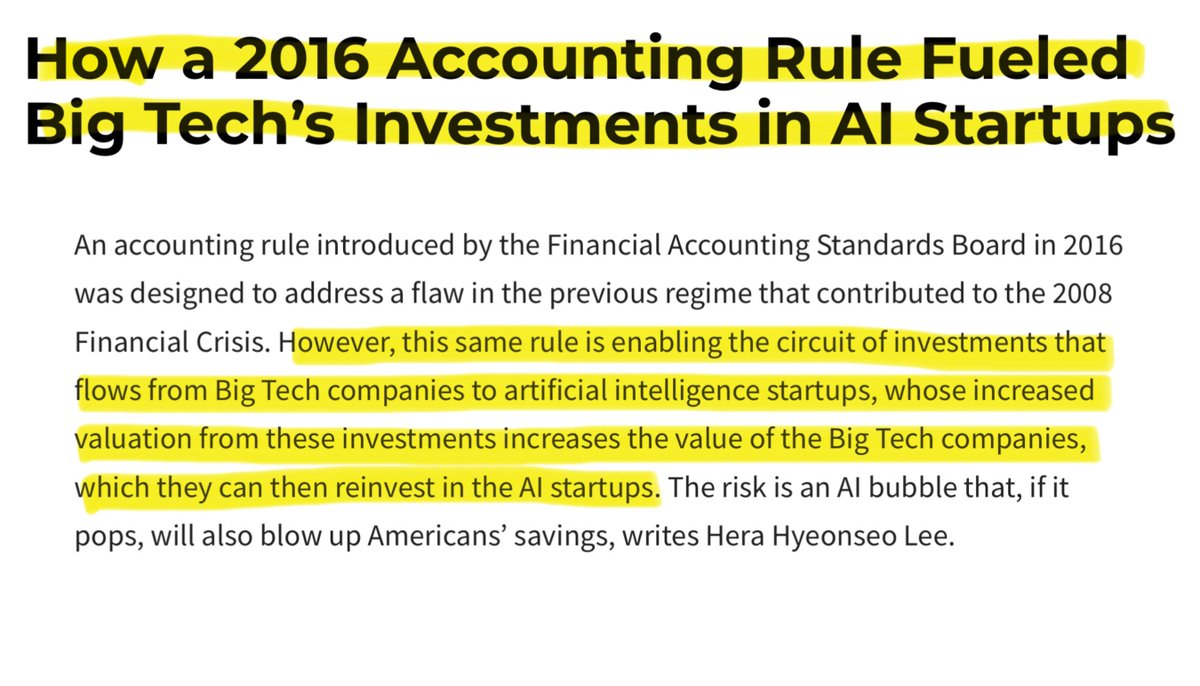

This manufactured demand triggers a second accounting trick where tech giants book massive paper profits. Every time a startup gets a higher value from a new funding round, the tech giant updates the value of its investment on its books and counts that unearned paper gain as direct profit.

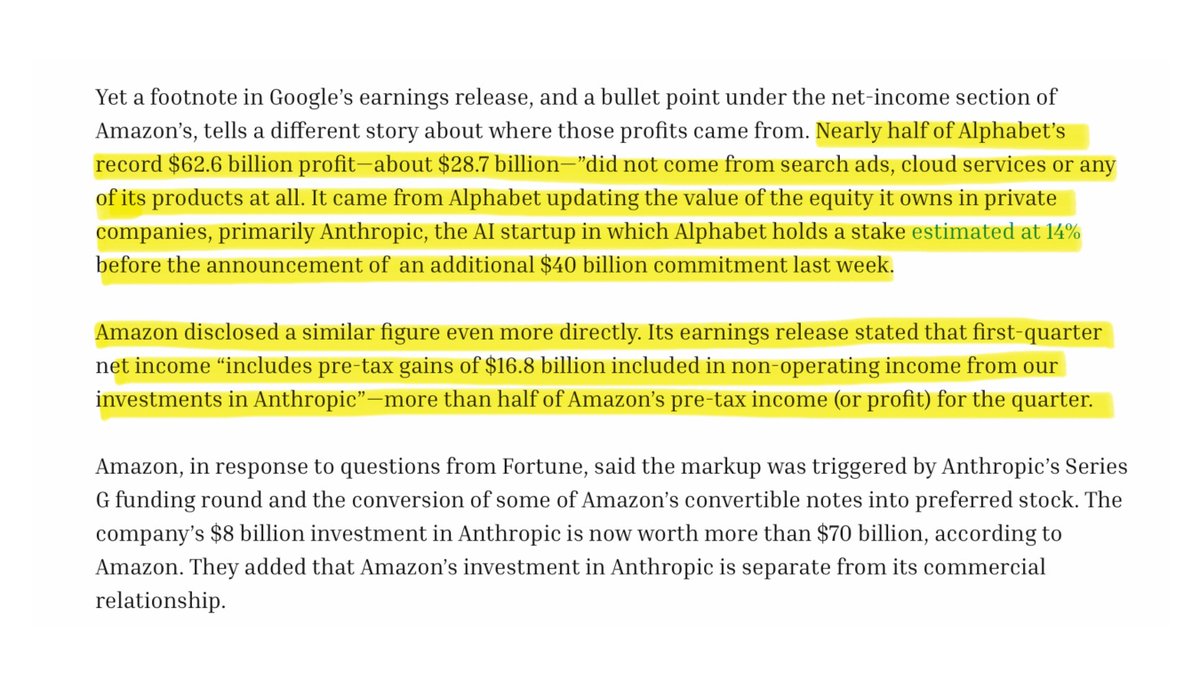

In Q1 2026, Alphabet reported a record $62.6 billion profit, but $28.7 billion nearly half, was just a paper markup on its Anthropic investment. In the same quarter, Amazon reported $30.3 billion in profit, but $16.8 billion of it was just an Anthropic paper gain.

While Amazon reported record profits, its actual free cash flow collapsed 95% to just $1.2 billion because it had to spend $44.2 billion in real cash to build physical data centers.

This has created a massive danger where these giant companies rely heavily on just one or two unstable startups. Microsoft has 49% of its $627 billion future backlog tied to OpenAI, while Oracle has an incredible 54% of its entire $553 billion pipeline relying on OpenAI alone.

This perfectly mirrors the 2001 dot-com crash when Global Crossing and Qwest Communications swapped identical fiber-optic network capacity with each other just to book fake sales.

Qwest had to erase $1.4 billion in fake income, and Global Crossing went completely bankrupt.

The only difference is that the dot-com swaps were illegal, but today's AI loop is fully legal under current accounting rules.

This legal loop inflates tech company stock prices, forcing automatic retirement accounts and index funds to buy even more of these tech stocks. It is a self feeding loop where investments, sales, and stock prices all go up on paper without the AI technology ever making real cash profits.