DigiTimes published a report on TSMC's packaging this morning, and there's a lot of alpha in it.

To summarize:

1. TSMC is significantly expanding SoIC capacity in 2027 (from 10K wafers/month to 50K wafers/month), with NVIDIA locking up most of this SoIC capacity. Only 10% will be allocated to CPO.

-> Positive for BESI. More hybrid bonding tool orders should follow.

2. CoPoS is delayed… first product shipment expected in Q4 2030.

CoWoS's lifespan is now expected to be longer than previously anticipated. CoPoS is just too difficult to push through. According to DigiTimes, with large orders pouring in not only from NVIDIA and AMD but also from ASIC customers, TSMC's CoWoS capacity for the next two years is already fully booked. CoPoS was originally expected to take the baton with mass production in 2028, but per the latest schedule:

Q3 2026: R&D equipment move-in begins. R&D line buildout takes about 1 year.

Q3 2027: Pilot line equipment orders placed. Equipment lead time of about 3 quarters.

Q2 2028: Pilot tools moved into the Chiayi P7 fab. Validation and fine-tuning needed for about 1 year afterward.

Mid-to-late 2029: Mass production equipment finalized, supply chain orders placed. Lead time of 3 quarters.

Q1 2030: Mass production equipment move-in. First packaging product shipment possible 6 months to 1 year later, in Q4 2030.

In particular, "uniformity" and "warpage" are reportedly causing significant difficulties in implementing CoPoS.

-> Negative for the CoPoS supply chain. TSMC is reportedly even imposing a policy that anyone joining the CoPoS development effort will be barred from selling externally.

3. Lastly, the CoWoP project led by NVIDIA and SPIL (矽品) is reportedly facing a potential suspension. Because of the higher technical difficulty and elevated cost, SPIL and Taiwanese PCB vendors are showing low willingness to participate, and only Chinese PCB vendors are showing intent to continue R&D.

-> Those who were pushing CoWoP should be ashamed of themselves. The ones who were pumping mainland Chinese names...

Post JPM note, the thesis that Solana is set to dominate in 2026–2027 become quite clear

1/The CLARITY Act is narrowing disputes, and both crypto and banks signal support. Solana stands to capture the first wave of institutional stablecoin adoption.

2/ Long-term legal certainty favors networks built for scale. The GENIUS Act shows bipartisan crypto legislation works. Solana’s high-throughput, low-cost, and fast-finality design positions it perfectly.

3/ Timing matters. If CLARITY passes before the midterms, Solana gains a clear regulatory runway while competitors scramble to adjust.

4/ Institutions want efficiency, liquidity, and scalability—not hype. Solana delivers:

<400ms settlement/65k TPS/~$0.00025/tx

This makes it institution-ready, from payments to tokenized assets.

5/ DeFi is maturing. The market is shifting from speculative NFTs/gaming to real-world assets (RWA) and tokenization. Solana hosts ~$6B in DeFi—perfectly positioned to lead this trend.

The Fan-Out Effect: What Happens Between a Query and a Citation - From a research developed by @Kevin_Indig & @AirOpsHQ analyzing 16,851 queries and +353K pages across ChatGPT's full retrieval pipeline:

* Retrieval rank is the #1 signal. A page at position 1 in ChatGPT's retrieval results has a 58% citation rate vs. 14% at position 10 — a 4x gap that no amount of content quality alone won't close. Great SEO is your advantage in AI search.

* Your headings are what get you cited. Pages with headings that closely match the user's query are cited 41% of the time vs. 29% for weak matches. Heading structure is the primary on-page lever for AI citation — more impactful than word count, topical breadth, or body copy.

* Domain authority doesn't translate. DA and backlinks show no positive correlation with AI citation — and are slightly inversely correlated. ChatGPT evaluates content directly based on relevance and structure, not authority signals.

Read more: https://t.co/4ZrPdOZ0Zs

New Report: Neoclouds and the Three Business Models

The market still talks about “Neoclouds” as if they are one category. They are not.

What is emerging are three different businesses: full-stack AI platforms, bare-metal GPU clouds, and what I think of as Power Landlords.

They all monetize the same AI demand, but through very different economics, very different risk retention, and very different claims on durability. The debate is increasingly shifting from who has the most GPUs to who can convert scarce, deliverable power into the most durable revenue and cash flow per energized MW.

https://t.co/oq7K0EP1lf

I knew the popularity of Agentic AI had led to a surge in demand for server CPUs, but I didn't expect TrendForce to provide such a ratio (CPU:GPU = 1:1).) $AMD $INTC $NVDA $ARM

真没想到trendforce会将服务器CPU与GPU的比例上调到1:1这个程度。

Reuters: In addition to one fab scheduled for completion this year, YMTC plans to build two more, and once all three fabs are operational, its production capacity will more than double.

Reuters: One of YMTC’s soon-to-be-completed fabs sourced more than 50% of its equipment from domestic Chinese companies, including key tools used for vertically stacking chip layers.

Reuters: Two sources said all three of YMTC’s new fabs will allocate a certain amount of capacity to DRAM production, though the exact output will depend on the progress of the company’s DRAM chip development.

$SNDK

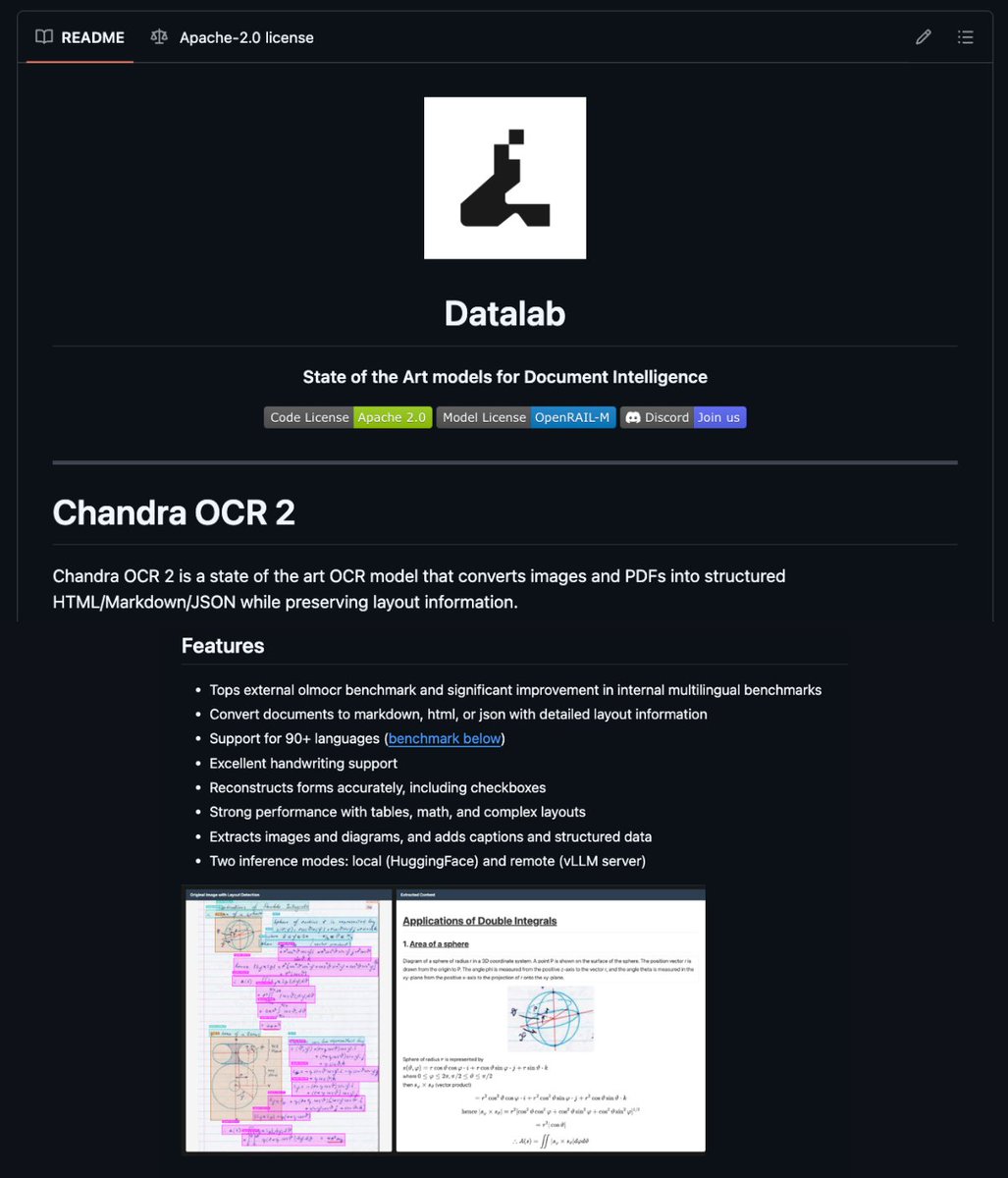

I found a GitHub repo that reads doctor handwriting.

It's called Chandra. It handles forms, tables, math equations and cursive documents that have defeated OCR for 30 years.

One command. Full layout preserved.

→ Reads handwriting, cursive, and messy print with full accuracy

→ Reconstructs merged table cells including colspan and rowspan

→ Renders inline math and block equations as LaTeX automatically

→ Extracts checkboxes, radio buttons, and form fields with their values

→ Outputs Markdown, HTML, or JSON with bounding box coordinates for every element

→ Supports 40+ languages out of the box

→ Runs locally via HuggingFace or on a vLLM server for production throughput

Tested on 10K financial filings, medical forms, LA Times newspapers, and college worksheets.

It beats every baseline on the OLMOCr benchmark.

100% Open Source. Apache 2.0. 4.8K stars.

Repo: https://t.co/nrCGKxLCC9

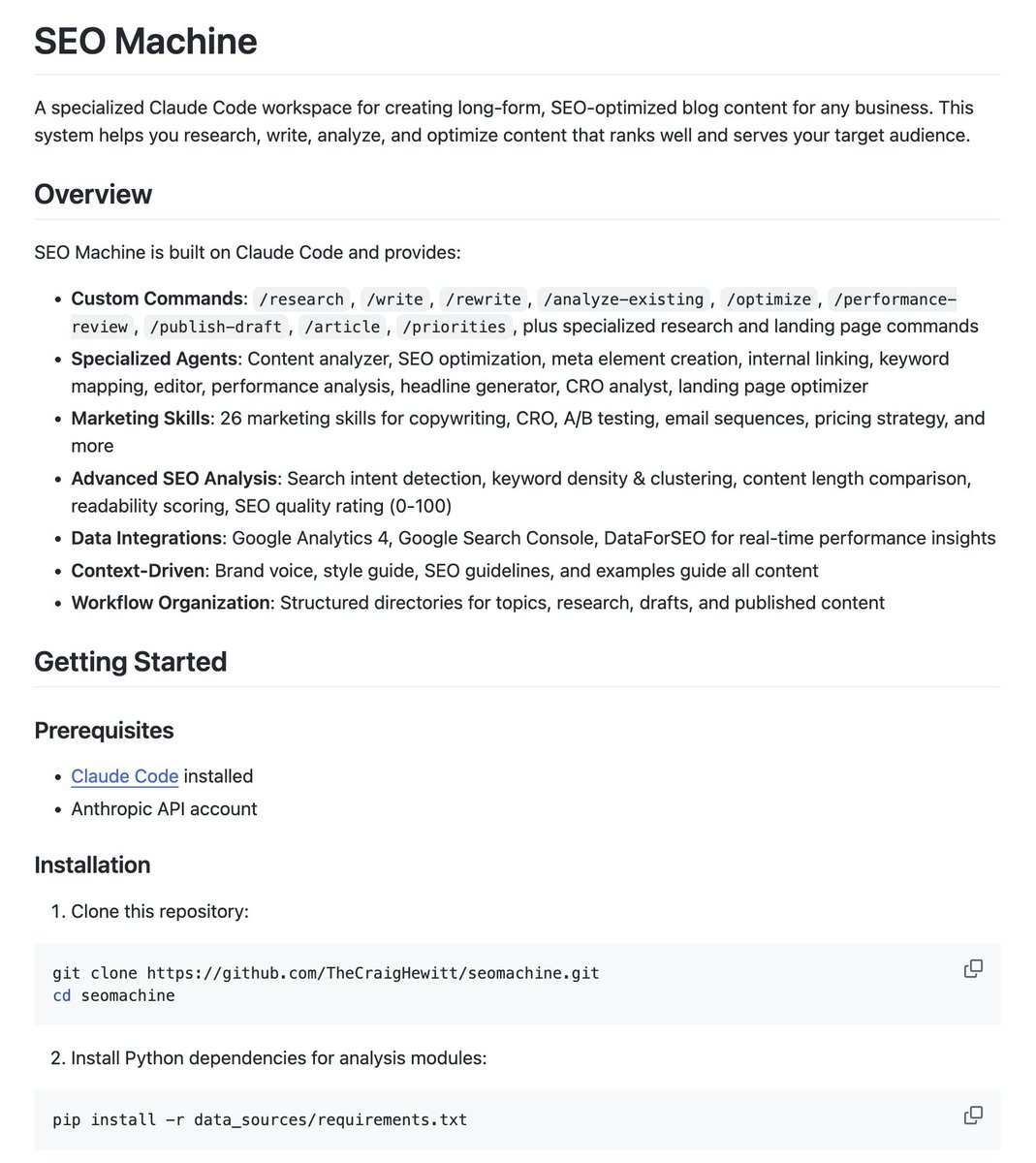

🚨 Someone open sourced a Claude Code workspace that writes, researches, and optimizes long-form SEO blog posts automatically.

It's called seomachine.

+2,548 stars this week.

Why it's great:

Hiring an SEO content agency costs $3,000 to $8,000 per month. A single optimized post from a freelancer runs $300 to $800.

Seomachine gives you a Claude Code workspace pre-wired for keyword research, content structure, competitive analysis, and readability scoring.

Most teams ship 2 posts a month. This runs the full pipeline end to end.

How to use it:

Clone the repo and drop it into Claude Code as your workspace. Feed it your business, your target keywords, and your audience.

It researches, writes, analyzes, and optimizes in one session. No prompting from scratch. No formatting cleanup.

Just point it at a topic and ship.

Deep|AI Infra 2026: Shifting from "Brain Power" Competition to "Whole-Body" Evolution

This is one of our most important reports this year, and our entire team invested a significant amount of time and effort into it.

We observed that the OCS ratio in Scale Up scenarios is still rising rapidly, and we also found that $MRVL is involved not only in TPU but also in LPU.

In 2026, the focus of AI development has pivoted from chasing high benchmark scores to pursuing AI Agents capable of multi-step reasoning and autonomous action. This infrastructure arms race is undergoing a transformation akin to biological evolution. If an AI system is viewed as an evolving organism: the GPU/TPU represents the calculating brain; Memory and Storage serve as the memory carriers for experience and context; the CPU acts as the hands coordinating tasks; while Optics and Networking function as the limbs supporting systemic data flow and response sensitivity. Under the framework of the Agent Scaling Law, the core bottleneck is no longer just the FLOPS of a single chip (brain power), but rather the communication efficiency (limbs), the memory wall (memory), and the Total Cost of Ownership (TCO).

The “Brain” Idle Crisis: Even with the most powerful compute cores, if the “limbs” (communication) are underdeveloped, chips will sit idle for over 1/3 of the time waiting for data.

The “Memory” Retrieval Bottleneck: Long-sequence reasoning for Agents imposes rigorous demands on KV Cache management; the performance of memory and storage components has become the deciding factor for an Agent’s logical depth.

Dimensional Evolution of “Limbs”: To overcome the communication bottlenecks inherent in MoE architectures, infrastructure is moving from 3D Torus toward high-dimensional topologies (up to 10D). Networking investment weight is now matching or even surpassing that of compute chips.

This report outlines the bottlenecks facing AI Agents and recent TPU progress, specifically exploring how Google TPU optimizes “whole-body” coordination through vertical integration. We argue that:

Networking is the new core battlefield: To solve MoE All-to-All bottlenecks, Google is significantly expanding scale-out bandwidth and shifting from 3D Torus to higher dimensions.

Unlocking TCO and Allocation Efficiency: Through proprietary architecture and vertical integration, the TPU v7 rack cost is significantly lower than the NVIDIA GB200. This efficiency gain frees up CapEx for growth in optical communications and memory. $LITE $NOK $CRDO

Detailed Report

https://t.co/o4KXldnP5G

Linux is free

Docker is free

Kubernetes is free

Git is free

GitHub is free

Python is free

Node.js is free

Go is free

PostgreSQL is free

MySQL is free

MongoDB is free

Redis is free

Terraform is free

Ansible is free

Jenkins is free

Prometheus is free

Grafana is free

NGINX is free

Apache is free

VS Code is free

Postman is free

Figma is free

Vercel is free

Netlify is free

Azure is free tier

ChatGPT is free

Claude is free

Gemini is free

Perplexity is free

What’s stopping you to build and ship?

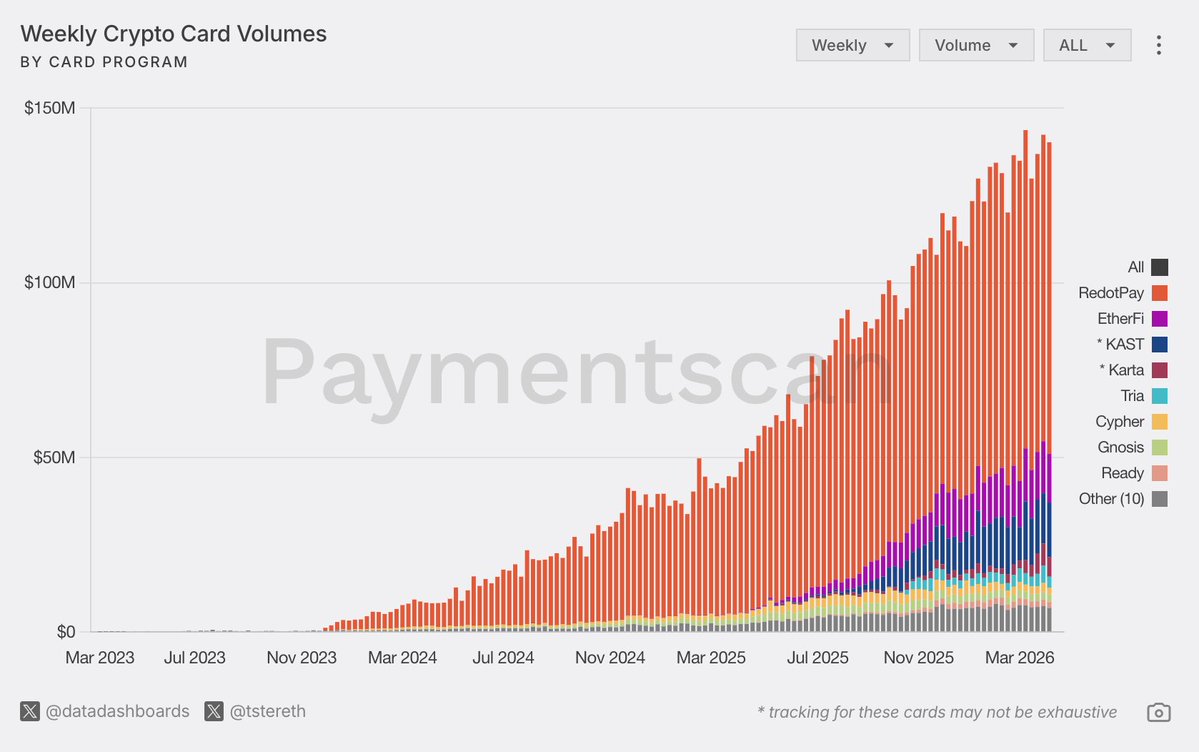

Crypto Cards Weekly Digest: April 6-April 12

Volume:

RedotPay: $89.22M

KAST: $15.64M

EtherFi: $13.95M

Karta: $5.59M

Tria: $3.17M

Gnosis: $2.14M

Cypher: $1.94M

Ready: $1.68M

Other (10): $6.9M

Total: $140.3M (-1.5% WoW)

Transactions:

EtherFi: 188,791

RedotPay: 113,321

Bitget Wallet: 96,095

BFinance: 48,279

Gnosis: 45,756

Safepal: 42,838

Avici: 27,552

MetaMask: 22,927

Other (10): 47,034

Total: 632,593 (+0.1% WoW)

Weekly Crypto Card Users

RedotPay: 62,310

EtherFi: 19,496

Bitget Wallet: 13,750

BFinance: 13,015

Safepal: 6,404

Tria: 5,879

Gnosis: 5,278

Ready: 4,244

Other (10): 8,785

Total: 139,161 (+1% WoW)

Some interesting stats:

Despite total card volume falling slightly, RedotPay still grew volume from $87.76M to $89.22M.

KAST was the biggest volume gainer, its volume rose from $14.35M to $15.64M, about +9% WoW.

Tria was the biggest loser this week, with its volume down by -35.7% WoW.

Hope you enjoyed this post and found some new VALUABLE information.

If you wanna support me, I'd appreciate a like, reply, and RT <3

🇹🇼 Taiwan - Heart of Photonics and Optical Components

Taiwan currently holds the strongest integrated growth potential in the global Photonics and Optical Components industry, particularly for AI data center applications. Below a list of tickers that focus in this field.

Epitaxy (LandMark e IntelliEPI) is leading in YTD% because the biggest current bottleneck in AI optics is the capacity for InP/GaAs epitaxial growth. Whoever masters this has a structural advantage.