(1/9) Keeta and ASK Group @askgroupae, a UAE-based investment group led by His Highness Sheikh Ahmed bin Sultan bin Khalifa bin Zayed Al Nahyan @asknahyan, have created a joint venture aiming to tokenize tens of billions of dollars of commodities and modernize cross-border payments in the Gulf Cooperation Council (GCC) region and beyond, contributing to the UAE's vision and commitment to growth as a global leader in digital finance and real-world asset infrastructure.

Mastercard just announced stablecoin settlement. Big move. But most people don't understand where this sits in the payments stack or why it's still only half the answer.

Let me break down how a £3 coffee actually settles across three systems.

1/Today, when you tap your card, your bank authorises instantly but nothing actually settles. Mastercard batches everything end of day. Your coffee shop's bank receives funds 1 to 2 business days later.

Banks carry overnight risk on every single transaction. Weekends and holidays make it worse. This model is 30 years old and hasn't fundamentally changed.

2/What Mastercard just announced changes the interbank settlement layer, not the consumer experience.

Instead of batch clearing, your bank converts GBP to USDC on chain. USDC moves between banks near instantly via blockchain. The coffee shop's bank converts back to GBP.

Faster. Works 24/7. A genuine step forward.

3/But here's what nobody is talking about.

Both banks now have to trust Circle, the company behind USDC, to sit in the middle of every single transaction on the planet.

That's not decentralisation. That's replacing one intermediary with another. A faster one, yes. But still a third party with counterparty risk baked in.

4/This is where the architecture of tokenised fiat matters.

Instead of converting to a stablecoin issued by a third party, you tokenise the fiat itself. GBP stays GBP. It moves on chain represented as a token backed 1:1 by real reserves held in a regulated account.

No conversion. No Circle. No issuer risk.

5/For this to work at scale you need a network where:

Banks are verified participants with compliance baked in at the network layer, not bolted on afterwards.

Value moves anchor to anchor, each bank operating as a tokenised fiat anchor on the network.

Settlement is instant and final, not probabilistic, not batched, not dependent on a third party redeeming your stablecoin.

6/This is exactly the architecture Keeta Network is building.

Keeta isn't trying to replace Mastercard. It's building the settlement infrastructure that makes the next generation of payments actually work, for institutions, for cross border flows, and for any network that wants to settle value without a third party sitting in the middle.

7/Mastercard choosing stablecoins tells you the industry knows batch clearing is broken.

What it doesn't solve is the issuer dependency problem.

Tokenised fiat on a purpose built settlement network does.

The rails matter as much as the asset.

$KTA @KeetaNetwork@schenkty

Keeta Personal is live.

I have been watching this network for months. I have traced the on-chain activity, read the whitepaper, decoded the GitHub. And I am telling you now. This is the moment the thesis becomes real.

Most people manage money across systems that were never built to talk to each other. A bank on one side. A crypto wallet on the other. A separate platform for investments. Every move between them costs you a fee, a delay, or another app to log into.

Keeta Personal deletes that entire problem.

One account. Your bank, your crypto, your investments, in the same place.

Here is what that actually means.

You get a US routing number and a European IBAN built in. Real banking details. Your salary can land straight into it. You can hold it as USD or convert it to USDC on the spot. No second app. No off-ramp.

It plugs into every rail that matters. Wire. ACH. ACH Debit. SWIFT. SEPA. PIX. Faster Payments. Interac. Visa Direct. Outbound payments to over 160 countries. Sending money across the world starts to feel like sending it across the street.

Bills get paid directly from your balance. No cashing out first. Your tokenised fiat is fully backed and held at regulated partners, so rent, subscriptions, autopay all come straight off your account.

Underneath it is a full crypto wallet. Hold, swap and send across Keeta, Ethereum and Base. Your everyday cash and your digital assets finally sitting in the same room.

And this is just what is live today.

What is coming. Physical and virtual spending cards. Native iOS and Android apps. Stock and T-bill investing from the same account. Savings and shared accounts. Instant funding and withdrawals via debit card. Real-time tokenised fiat transfers between Keeta users. Tools to create and manage your own tokens.

Then there is the part most people are sleeping on. Keeta Personal runs on open infrastructure. The same rails, the same multi-currency accounts, the same real-time settlement powering the app are available to builders through one SDK. Every product built on top makes your account reach further without you doing anything.

This is not a wallet. This is not another neobank. It is the moment banking and crypto stop being two separate worlds.

The product is live. The receipts are on-chain. Go and verify it yourself.

https://t.co/ju5Z8gHnbg

$KTA @schenkty@gabe_schenk@Syno_0x@xescure@Brown_Thunder76@KeetaNetwork

@KeetaNetwork@schenkty $KTA

Keeta can also go parabolic just like LAB (I own both), once Keeta Personal mobile App becomes available on iOS & Android and I believe we are getting very close. Just my humble opinion. Good luck to those who are patiently holding.

(1/7) Keeta Personal is live!

Built to bring everyday banking, payments, and digital asset management into one application.

Users can now hold, manage, and move crypto, fiat, and other investments from a single platform.

"@KeetaNetwork is the missing link that enables all existing Web3 and TradFi systems to communicate with one another seamlessly."

We spoke with CEO @schenkty about cross-border payments, compliance and shared rails.

Read more 👇https://t.co/qdPma3SjhE

$KTA

@KeetaNetwork@schenkty

keeta:native

26 May 2026

Pump up the volume.

Let's celebrate 'coz

It's TIME!

Keeta Network getting PERSONAL!

From fiat to crypto, investments that shine,

One account to connect the whole world online!

Multi-currency flowin', USD to yen,

ACH debit payin' bills again and again!

Visa Direct sendin' cash across the globe,

Stablecoins swappin', no fees overload!

Hold your USDC, earn that sweet yield,

T-Bills and stocks on-chain, that's the real deal!

160+ countries, come join the fun,

Keeta Personal – the revolution's begun!

Bank transfers instant, crypto in sync,

Global moves faster than you can think!

Compliance on point, privacy sealed tight,

This is the future, shinin' so bright!

KEETA PERSONAL, IT'S TIME!

Payments, crypto, investments— all mine!

Move that money, spin it around,

Keeta Network liftin' us off the ground!

KEETA PERSONAL, IT'S TIME!

Day One for Keeta Personal today.

Is the Bank acquisition approval also close?

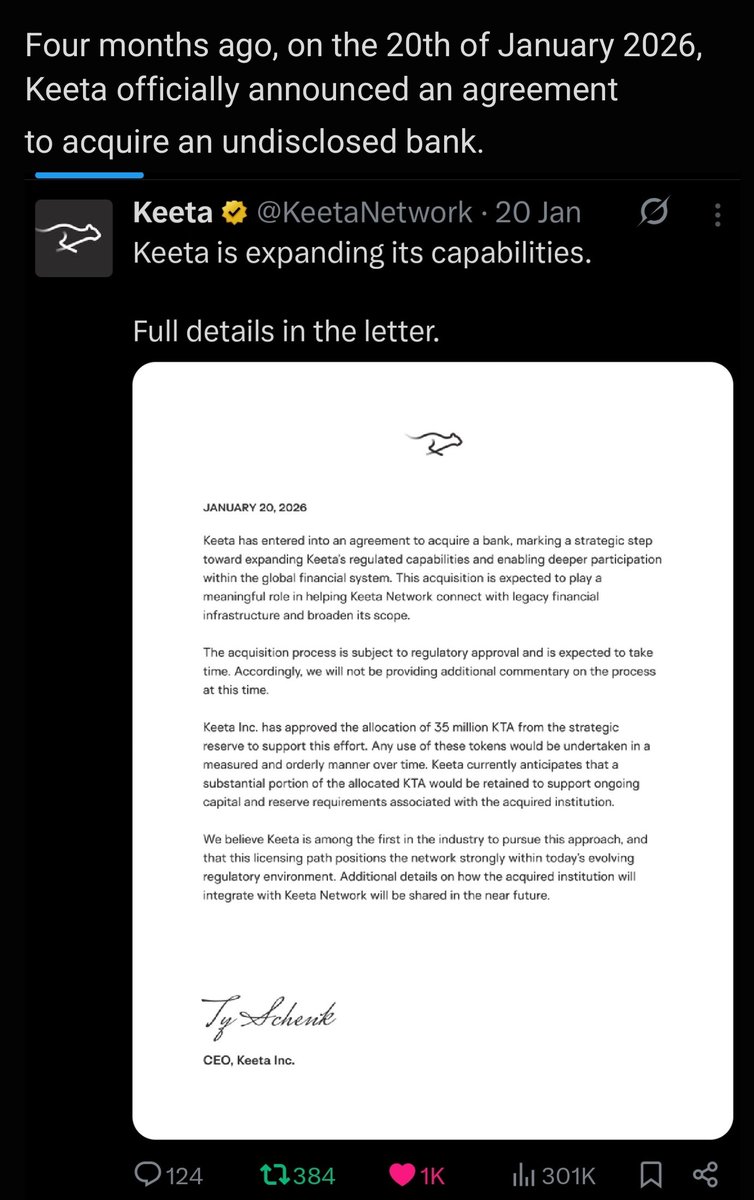

Four months ago, on the 20th of January 2026, Keeta officially announced an agreement

to acquire an undisclosed bank.

On May 19th 2026,

President Donald Trump signed a major

executive order directing federal

agencies to streamline and fast-track the

licensing and regulatory approval

processes for cryptocurrency and fintech

firms.

Google and AI says that the average time for bank acquisition approval is 4 months.

So, Keeta's bank acquisition approval could be close. Check out $KTA and pay close attention 'coz Keeta is about to take off.

@KeetaNetwork

@NicoNIMH@schenkty@KeetaNetwork I know it's on the 22nd of May. But some sources are also picking up May 15th. We don't want to have frustrated people complaining tomorrow. AMBCrypto is not AI but they also picked up May 15 as the launch date. https://t.co/QMdDDn1N9Y

@schenkty@KeetaNetwork $KTA

@KeetaNetwork@schenkty

Can't wait to send money across the world in milliseconds with Keeta Personal. Accumulate $KTA now and retire early. (NFA-Not Financial Advice). ❤️ $$$