TAX BILLS 2026/27:

State Minister for General Duties @henrymusasizi1 has said @GovUganda projects to generate UGX 1,741 billion in FY 2026/27 from the tax policy proposals contained in the bills and UGX 3,164 billion from URA administration measures, which contributes to the projected revenue effort of 15.5% of GDP, representing a growth of 0.6 percentage points .

The Minister made the remarks while presenting the

the Tax Bills for FY 2026/27 to the Finance Committee of @Parliament_Ug

TAX BILLS:

✅️The Income Tax (Amendment) Bill, 2026;

✅️The Excise Duty (Amendment) Bill, 2026;

✅️The Value Added Tax (Amendment) Bill, 2026;

✅️The Tax Procedures Code (Amendment) Bill, 2026;

✅️The Stamp Duty (Amendment) Bill, 2026;

✅️The External Trade (Amendment) Bill, 2026;

✅️The Lotteries and Gaming (Amendment) Bill, 2026; and

✅️The Traffic and Road Safety (Amendment) Bill, 2026.

"The Bills are meant to raise revenue, foster compliance and assist @URAuganda in its work," said the Minister adding that revenue mobilization plays a critical role in financing Government priorities for socio-economic transformation.

@henrymusasizi1 also said the proposed amendments are complemented by the improvements in tax compliance,adding that the compliance strategies are designed to expand the tax base by bringing on board persons currently outside the tax net.

TAX POLICY PROPOSALS:

INCOME TAX:

➡️An option for taxpayers to pay rental income tax monthly.

➡️Introduce a withholding tax of 10% on commissions paid to data and voice bundle distribution agents.

➡️Introduce an Alternative Minimum Tax of 0.5% for businesses which carry forward losses beyond 7 consecutive years.

➡️Introduce 6% final witholding tax on non business assets.

➡️Introduce a withholding tax of 6% on public entertainers.

VAT:

➡️Increase the VAT Threshold from UGX. 150 million to UGX 250 million.

➡️Clarification of the taxation of imported software.

STAMP DUTY:

➡️Increase the stamp duty on land transfers from 1.5% to 3%.

➡️Introduce Stamp duty on motor vehicle and Motorcycle registration both at first registration and on transfer as follows: Motor vehicle registration at UGX. 100,000 for regular vehicles and UGX. 200,000 for commercial motor vehicles and motorcycles at UGX. 50,000.

EXCISE DUTY:

➡️Increase excise duty on diesel and petrol by UGX. 200 per litre.

➡️Increase the specific excise duty rate on any other un-denatured spirits of alcoholic strength by volume of less than 80% from UGX 1700/litre to UGX 3500/litre.

➡️Increase excise duty at first registration on motorcycles from UGX. 200,000 to UGX. 500,000.

➡️Extend excise duty to apply on all single use plastics and increase the rate from 2.5% or USD 70 per ton whichever is higher to 25% or USD 1,500 per ton whichever is higher.

➡️Increase excise duty on cement from UGX. 500 to UGX. 1,000 per 50 kg.

➡️Increase excise duty rate for sugar from Shs. 100 per Kg to Shs. 300 per Kg.

➡️Introduce excise on cooking fat and fatty acids at UGX. 500 per liter/ Kg.

➡️Increase excise duty on cooking oil from UGX. 200 to UGX. 400 per litre.

TRAFFIC AND ROAD SAFETY ACT:

➡️Reduce the age of acceptable cars from 15 years to 13 years from the date of manufacturing. Introduce a graduated scale of environmental levy on imported used motor vehicles.

𝟐𝟎𝟐𝟓 𝐓𝐚𝐱 𝐋𝐚𝐰 𝐒𝐲𝐦𝐩𝐨𝐬𝐢𝐮𝐦 | 𝐔𝐠𝐚𝐧𝐝𝐚 𝐋𝐚𝐰 𝐒𝐨𝐜𝐢𝐞𝐭𝐲

The 2025 Tax Law Symposium organized by the Uganda Law Society - LAP, brings together leading tax experts, policymakers, and legal practitioners to discuss the evolving tax landscape in Uganda.

Our very own @EdwardBalaba Partner – Tax will be among the key speakers, unpacking the latest trends, substantive changes, and procedural developments shaping tax practice and compliance.

📅 Date: Tomorrow, 29th August 2025

📍 Venue & Participation Details: See flyer below

Don’t miss this opportunity to gain expert perspectives on critical tax developments that impact businesses and professionals alike.

#MMAKSTaxPractice #TaxCompliance

Valuation of firm depends on stage in its life cycle and the purpose of valuation.

I tell my clients: tell the reason you need valuation I’ll give you approach.

Look at full perspective:

There are 6 stages:

1. Starup

2. Young growth

3. High growth

4. Mature growth

5. Mature stabile

6. Decline

Before valuation it is useful to determine which stage company belongs in.

For example, if the company is in mature growth stage then:

• Source of Value is stabile earning potential

• DCF is applicable

• Relative valuation is applicable too

• Pricing measure are : Revenues, Earnings, Growth rate, FCF

• Valuation ratios could be : PE to Growth rate, P/E, EV/FCF

• Preferable method:

👉 DCF

👉 𝘈𝘭𝘵𝘦𝘳𝘯𝘢𝘵𝘪𝘷𝘦 𝘰𝘳 𝘥𝘰𝘶𝘣𝘭𝘦 𝘤𝘩𝘦𝘤𝘬:

• Comparable companies (P/E)

• Comparable transactions – EBITDA multiple

The success of valuation lays in how well you create a projection of each important financial categories

Look the other stages a well.

Want this poster in high-res PDF? Drop a comment and I will send you a file (important note: follow me so I can DM you)

Everyone wants to build muscle…

But no one builds their brain.

You’ll notice it only when it starts to fail:

Brain fog. Anxiety. Mood swings.

Here’s how to heal and protect the organ that controls everything in your life 🧵

The increased government borrowing is attributed to slow growth in tax revenues and a surge in government expenditure driven by supplementary budget requests #MonitorUpdates https://t.co/wyiib33QVJ

🎙️ EPISODE 6 of the Tax Hub Podcast is dropping this week.

📺 We are excited to share a teaser of the in-depth discussion that EPISODE 6 brings.

🔔 The full discususon will be uploaded on our YouTube channel.

@MMAKS_Advocates@EYnews@AFMpangaUG@URAuganda

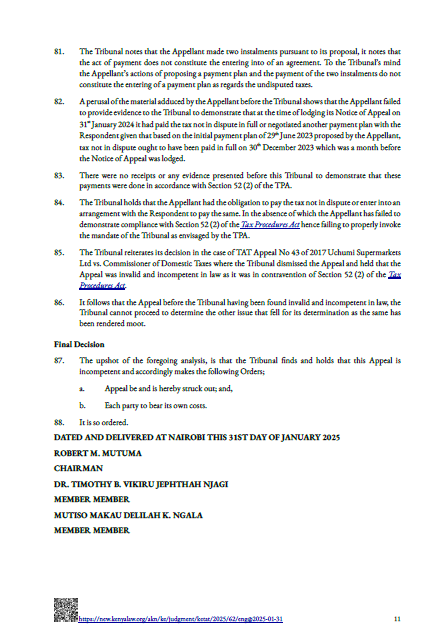

I once stopped for coffee with a young Ugandan lawyer, Edward Balaba studying at Kings College London and missed not one but two buses, but still made it on time to Gatwick.

https://t.co/HMntvjqctw

#MonitorUpdates

The Notes app on your iPhone is one of the most powerful tools available.

But 99% of people don’t know its true potential.

Here are 15 amazing features you must know:

Taxpayers must settle undisputed tax amounts or negotiate a payment plan before lodging an appeal as required under Section 52(2) of the Tax Procedures Act (TPA)

https://t.co/A8OmCu4dYw