I built my own context engine that is so much faster/deeper than the “memory” function in Claude and it’s amazing. Bc it’s MCP you can literally connect the same context to both a ChatGPT and Claude session at the same time with additive writes/reads. Not bound to any provider. You can just do things.

22. THE HOHN-STYLE DILIGENCE WORKFLOW

A practical Hohn-style research process should follow a disciplined sequence.

Step 1: Write the 3-sentence business-quality thesis

Before building a model, answer:

* What does the company do?

* Why is it hard to compete with or replace?

* Why should it be more valuable in 10 years?

If this cannot be stated clearly, the idea is not ready.

Step 2: Map the industry profit pool

Identify:

* Total industry revenue

* Total profit pool

* Profit share by competitor

* Historical returns on capital

* Market share trends

* Pricing history

* Customer concentration

* Supplier power

* Regulatory constraints

* New entrant history

* Failed entrant history

The goal is to determine whether the industry allows owners to earn excess returns.

Step 3: Identify the moat and test it adversarially

Classify the moat:

* Physical asset

* IP/engineering complexity

* Network effect

* Switching cost

* Installed base

* Bundle/distribution

* Brand

* Scale

* Regulation/concession

Then disprove it:

* Who has tried to enter?

* Why did they fail?

* What would change that?

* What technology could substitute it?

* What regulatory action could weaken it?

* What customer behavior could undermine it?

Step 4: Conduct reference checks

Hohn emphasizes speaking with relevant people. A proper process includes:

* Customers

* Former executives

* Competitors

* Suppliers

* Regulators where possible

* Industry consultants

* Former employees

* Distributors

* Buyers who switched away

* Buyers who refused to switch

* Technical experts

Reference checks should focus on what matters:

* Would customers leave after a price increase?

* Is the product mission-critical?

* Is the competitor credible?

* What is the company’s real reputation?

* What are the technical failure modes?

* What does management misunderstand?

* What is the industry’s dirty secret?

Step 5: Build the financial model after the moat work

The model should not be an accounting exercise. It should translate the business-quality thesis into financial outputs.

Model explicitly:

* Price growth

* Volume growth

* Mix

* Margin bridge

* Maintenance capex

* Growth capex

* Working capital

* Incremental ROIC

* Free cash flow conversion

* Buybacks/dividends

* Leverage

* Regulatory resets

* Downside scenarios

Step 6: Build the bear case

The bear case must be serious and specific.

Questions:

* What if the moat is weaker than believed?

* What if pricing power disappears?

* What if regulation caps returns?

* What if AI changes distribution?

* What if management makes a bad acquisition?

* What if normalized margins are lower?

* What if growth requires more capital?

* What if customers are more price-sensitive?

* What if the terminal multiple is lower?

* What if the market is correctly discounting something?

Step 7: Define the 3 variables that matter

A Hohn-style investor must reduce noise.

Examples:

* For an airport: tariff framework, passenger volume, commercial revenue per passenger.

* For an aircraft engine company: installed base growth, aftermarket margin, reliability.

* For a rating agency: debt issuance cycle, pricing power, regulatory risk.

* For a payment network: volume growth, take rate durability, regulatory fee pressure.

* For enterprise software: retention, seat expansion, AI substitution risk.

* For a railroad: pricing, volume mix, operating ratio, regulatory/labor risk.

The investment should not depend on 25 variables being right.

Step 8: Define engagement optionality

For each holding, assess:

* Is management excellent, acceptable, or problematic?

* Are there capital-allocation changes that could improve value?

* Is there a governance issue?

* Are shareholder rights usable?

* Is public activism needed or would private dialogue work?

* What is the escalation ladder?

* What is the value of intervention?

Step 9: Determine position size

Sizing should reflect:

* Business quality

* Conviction

* Downside risk

* Liquidity

* Correlation

* Regulatory exposure

* Volatility tolerance

* Opportunity cost

* Ability to add on weakness

* Need for activism

Step 10: Monitor thesis, not price

Ongoing monitoring should focus on:

* Moat strength

* Pricing behavior

* Customer retention

* Competitive entry

* Regulation

* Capital allocation

* Free cash flow

* Balance sheet

* Management incentives

* Disruption risk

* Long-term intrinsic value growth

The stock price is information, but not the thesis.

23. HOHN-STYLE SCORING SYSTEM

This is a practical codification, not a disclosed TCI system.

A company should be scored out of 100.

Business quality and moat: 25 points

* 0-5: no durable moat

* 6-10: weak or unproven moat

* 11-15: decent moat but vulnerable

* 16-20: strong moat

* 21-25: multiple reinforcing moats with low substitution risk

Essentiality and demand durability: 15 points

* 0-5: discretionary demand

* 6-10: useful but deferrable/substitutable

* 11-15: essential, recurring or ultimately unavoidable demand

Pricing power: 15 points

* 0-5: price taker

* 6-10: inflation pass-through only

* 11-15: proven ability to price above inflation without volume loss

Financial quality: 15 points

* 0-5: poor cash conversion, leverage, cyclicality

* 6-10: acceptable but inconsistent cash flow

* 11-15: high FCF conversion, high ROIC, resilient balance sheet

Management and governance: 10 points

* 0-3: value-destructive or misaligned

* 4-7: acceptable

* 8-10: strong capital allocation and shareholder alignment

Regulation and disruption risk: 10 points

* 0-3: high risk of confiscation or substitution

* 4-7: manageable risk

* 8-10: stable framework and low disruption risk

Valuation and expected return: 10 points

* 0-3: quality fully priced or overvalued

* 4-7: reasonable expected return

* 8-10: high-quality business mispriced due to temporary, misunderstood, or fixable issue

Scoring interpretation

* 85-100: potential core Hohn-style compounder

* 75-84: investable if valuation is attractive and risks are understood

* 65-74: watchlist or smaller position

* 50-64: likely not good enough unless special situation

* Below 50: reject

A concentrated portfolio should mostly consist of companies scoring above 80, with the highest position sizes reserved for those above 85.

24. MASTER CHECKLIST FOR ANALYZING A COMPANY LIKE CHRIS HOHN

Business quality

* Is this a genuinely high-quality business?

* Is the business structurally better than the average public company?

* Does it earn returns above cost of capital?

* Are those returns durable?

* Is the business simple enough to understand at the level of the true value drivers?

* Is the company likely to be larger, stronger, and more profitable in 10 years?

Industry structure

* Is the industry consolidated?

* Are competitors rational?

* Does demand growth translate into profit growth?

* Are profits competed away?

* Has the industry historically created shareholder value?

* Are there failed entrants that prove barriers are real?

* Are customers fragmented or concentrated?

* Are suppliers powerful?

* Are employees or unions able to capture economics?

* Is regulation stable?

Moat

* What is the moat?

* Is it physical, legal, technological, network-based, behavioral, or economic?

* Is there more than 1 moat?

* Is the moat strengthening or weakening?

* Can a competitor replicate the product?

* Can a customer substitute the product?

* Can technology bypass the company?

* Can regulation force the moat open?

* Is the moat visible in margins, ROIC, retention, or pricing?

Essentiality

* Is the product essential?

* Is demand recurring, unavoidable, or mission-critical?

* Is the product required by regulation, financing, safety, or workflow?

* Can customers defer purchases?

* If deferred, does demand return later?

* Is the customer’s cost small relative to the value delivered?

Pricing power

* Can the company price above inflation?

* What is the evidence?

* Did volumes hold after price increases?

* Are competitors rational on price?

* Does price growth drop through to profit?

* Could regulators or customers push back?

* Is pricing power cyclical or structural?

Growth

* Is growth price, volume, mix, M&A, or FX?

* Is volume growth value-accretive?

* Does growth require capital?

* Is growth profitable?

* Is incremental ROIC attractive?

* Is the runway long enough to matter?

* Does growth increase the moat?

Financials

* Does accounting convert to cash?

* What is normalized free cash flow?

* What is true maintenance capex?

* What is working capital intensity?

* Are margins sustainable?

* Is leverage conservative?

* Is the company financially resilient in downturns?

* Are there off-balance-sheet liabilities?

* Are pensions, leases, guarantees, or legal liabilities material?

Management and governance

* Is management aligned?

* Does management allocate capital rationally?

* Has management avoided value-destructive M&A?

* Is the board competent?

* Are incentives based on ROIC and FCF or growth and adjusted EBITDA?

* Is there governance risk that the market over-discounts?

* Is activism or engagement possible?

* Is management focused on the core business?

Regulation and politics

* Does regulation protect or threaten the economics?

* Are returns socially acceptable?

* Is the company over-earning?

* Is there risk of price caps, fee limits, breakups, forced access, or concession changes?

* Is the regulator independent?

* Is the state a customer, regulator, or shareholder?

* Could political pressure change the rules?

Disruption

* What can kill the business?

* What can substitute the product?

* Does AI lower entry barriers?

* Does AI change customer behavior?

* Does AI commoditize the service?

* Could a large incumbent bundle a competing product?

* Could a small innovator attack the most profitable segment?

* Is the business more like Microsoft or more like Yellow Pages?

Valuation

* What is normalized owner earnings?

* What is conservative intrinsic value?

* What is the downside value?

* What is the long-term compounding rate?

* What does the market imply?

* Is the market underestimating duration?

* Is the market over-discounting governance risk?

* What multiple is justified by the moat?

* What expected return is available at today’s price?

* What return remains if the exit multiple compresses?

Position sizing

* Is this good enough to be a top 10 position?

* What is the permanent capital loss risk?

* Can the position be held through volatility?

* Is there enough liquidity?

* Is the position correlated with existing holdings?

* Is the thesis dependent on macro?

* Is the thesis dependent on regulation?

* Is the idea better than current holdings?

Sell discipline

* Has intrinsic value been reached?

* Has expected return fallen below alternatives?

* Has conviction declined?

* Has the moat weakened?

* Has management changed behavior?

* Has capital allocation deteriorated?

* Has regulation changed?

* Has AI or technology changed the terminal value?

* Is the stock now pricing in too much perfection?

25. HOW TO WRITE A HOHN-STYLE INVESTMENT MEMO

A high-quality memo should be short on noise and deep on the few variables that matter.

Recommended memo structure

1. Thesis in 5 bullets

* What the company does

* Why it is a great business

* Why the moat is durable

* Why the market is wrong

* Expected return and downside

2. Industry structure

* Profit pool

* Competitors

* Customer power

* Supplier power

* Entry barriers

* Substitution risk

* Regulatory framework

3. Moat evidence

* Pricing history

* ROIC history

* Market share

* Failed entrants

* Customer retention

* Technical barriers

* Network effects

* Switching costs

4. Financial model

* Normalized FCF

* Revenue growth split

* Margin bridge

* Capex

* Incremental ROIC

* Capital returns

* Balance sheet

* Scenarios

5. Valuation

* Base case

* Bear case

* Bull case

* Implied market expectations

* Expected IRR

* Downside risk

* Required margin of safety

6. Governance and engagement

* Management quality

* Board quality

* Incentives

* Capital allocation

* Potential engagement topics

* Escalation path

7. Red-team case

* The strongest reasons not to invest

* What would prove the thesis wrong

* What must be monitored

* Kill criteria

8. Position size recommendation

* Initial size

* Add levels

* Maximum size

* Risk limits

* Correlation

* Liquidity

* Monitoring plan

26. THE PRACTICAL HOHN TEST

A company is likely Hohn-style investable only if most of the following statements are true:

* The company operates in an industry where shareholders can retain economic surplus.

* The business has high and sustainable barriers to entry.

* The product or service is essential.

* The company can price above inflation or protect real economics.

* The business has low substitution risk.

* The company has strong free cash flow conversion.

* Growth is capital-light or earns attractive incremental returns.

* Management is at least rational and not value-destructive.

* Governance issues are either absent or fixable.

* Regulation is understood and not likely to confiscate economics.

* The company can be owned for 10 years.

* The market is underestimating durability, pricing power, governance improvement, or long-term cash-flow growth.

* The valuation allows attractive returns even without heroic assumptions.

* The downside is mostly temporary mark-to-market volatility, not permanent impairment.

* The idea is good enough to displace capital from an existing holding.

FINAL SYNTHESIS

Chris Hohn’s methodology is a search for long-duration, protected economic rents. The framework deliberately avoids most companies because most companies cannot defend profits for long periods. The process starts with moat durability, not valuation; with essentiality, not growth; with pricing power, not revenue momentum; with intrinsic value compounding, not catalysts; and with conviction, not diversification.

The practical discipline is severe: reject structurally bad industries, avoid false precision, distrust profitless growth, test every moat for competition and substitution, separate price growth from volume growth, treat regulation as both shield and sword, and concentrate only where the business is exceptional and the downside is underwritten.

The highest-quality Hohn-style investments are companies that can be held through multiple market cycles because the fundamental business is becoming more valuable over time. The ideal outcome is not a quick re-rating. The ideal outcome is ownership of a scarce, essential, cash-generative asset whose intrinsic value compounds for longer than the market is willing to discount.

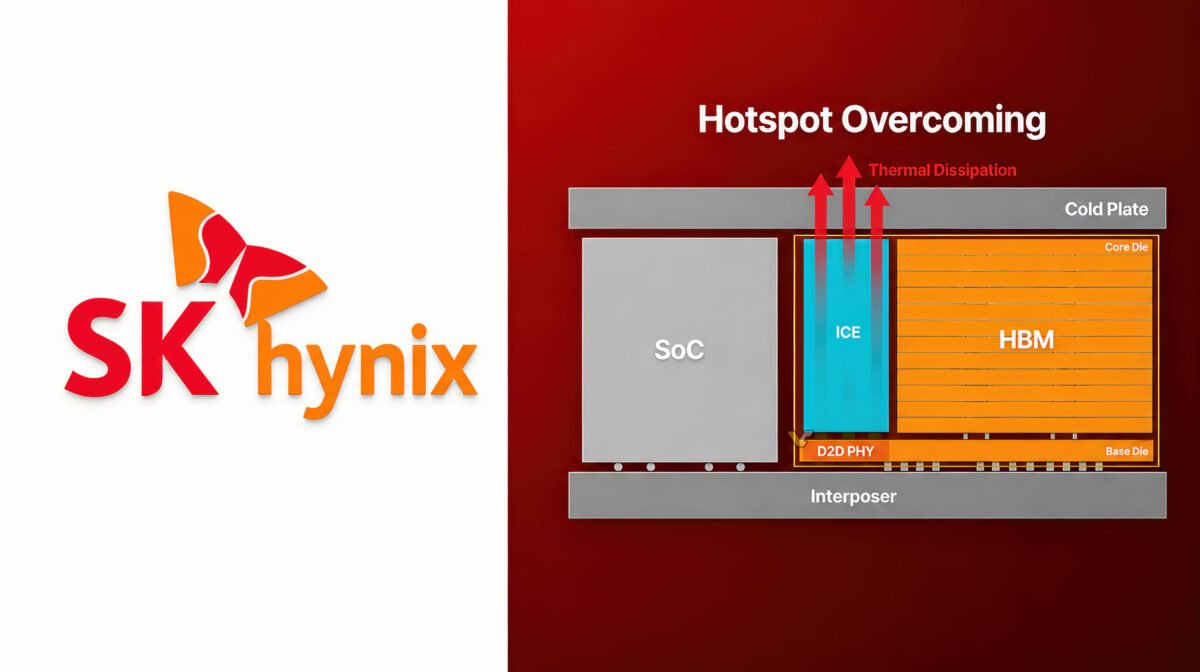

SK HYNIX INTRODUCES INTEGRATED COOLING FOR NEXT-GEN HBM

SK Hynix launched iHBM, a thermal management solution for future high-bandwidth memory chips.

Instead of relying only on indirect cooling through the core die, iHBM embeds cooling elements inside the HBM package where heat concentration is highest.

The company says the technology reduces thermal resistance by 30%.

It is designed for next-generation HBM products, including HBM5.

SK Hynix says iHBM can operate stably under high-temperature and high-pressure conditions.

The technology is also compatible with existing System-in-Package architectures, meaning customers can adopt it with limited design changes.

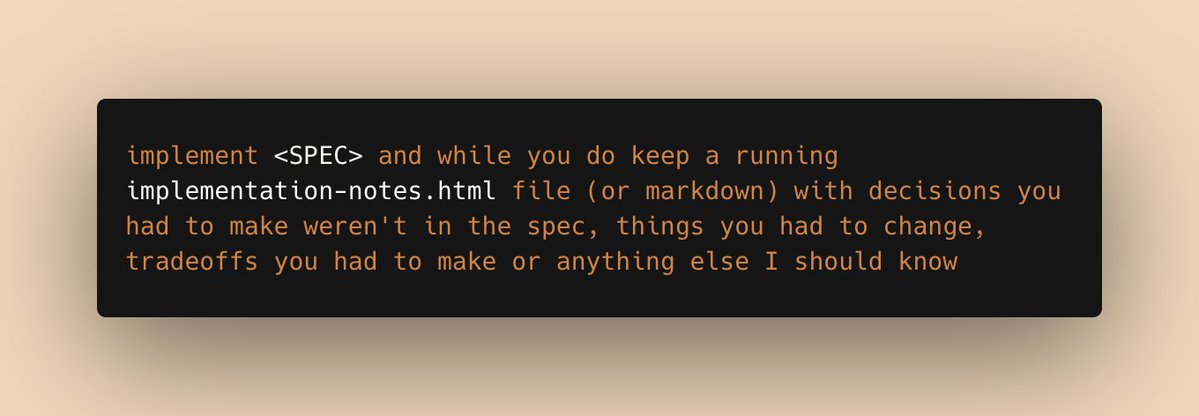

a prompt I've been using a lot recently:

implement <SPEC> and while you do, keep a running implementation-notes.html file (or markdown) with decisions you had to make weren't in the spec, things you had to change, tradeoffs you had to make or anything else I should know

Introducing Beautiful HTML Templates:

I made some stunning HTML slide templates & open-sourced them

If you use this template system, it will literally be impossible for your agent to produce something ugly

Link below

$NVDA $MU $SNDK $LITE The Economics of Frontier AI Inference and Hardware Bottlenecks

Frontier AI inference is constrained primarily by memory bandwidth and rack-scale integration, not raw compute. Sequential token generation creates a fundamental bottleneck where KV-cache movement and hardware utilization determine throughput economics more than peak FLOPS.

First-principles modeling confirms that Mixture-of-Experts architectures and high-speed interconnects are structural responses to this constraint, enabling practical cost management at scale. API pricing from OpenAI, Google, and other providers directly reflects these physical limitations, with long-context tasks and sequential decoding imposing disproportionate cost penalties tied to the memory wall.

This dynamic reshapes where investment value accrues across the AI hardware stack. Individual component specifications matter less than full-stack system efficiency, including memory hierarchy, interconnect bandwidth, and workload-aware scheduling. Hardware incumbents and chip startups alike face strategic roadmaps dictated by the same physics. The companies that solve rack-scale memory movement most efficiently will capture outsized value, while those optimizing for compute alone risk building capacity the inference bottleneck cannot fully exploit.

My Trading Manifesto:

Embrace risk.

Accomplishment and fulfillment in any endeavor requires facing the unknown head on, placing your bet, and accepting the consequence.

You can't control what cards life deals, but you can control when to shove your chips in the middle. Focus on that part.

Bet size matters too. Balance your aggression. Size relative to the opportunity.

Study each situation with as little ego as possible. Prioritize truth over preconceived notions. Many an "expert" has been taken out to the woodshed because they couldn't let go of their grand theory.

Don't hesitate to build your understanding of things from the ground up again and again. That keeps you closer to the truth and further from outdated or tainted knowledge.

Hold feedback in high value. Use feedback as a compass to adjust strategy and make a better bet on the next try. There's nothing more valuable than ex-post information. It's the primary tool of improvement. It's how you move from a poor risk-taker to an exceptional risk-taker. It's how you develop killer instinct.

Again, keep ego out of the process. If contradictory evidence comes back, don't dismiss it. Update your views and approach. The desire to "be right" must never overpower the objective search for truth and results.

Finally, keep self-preservation top of mind. Earn the right to bet big as your knowledge progresses, but only to a limit. Never put yourself in a situation where a negative outcome means complete destruction. Preserve your seat in the game. Without a seat at the table, killer instinct will decay.

You will experience exhilarating wins and bone crushing defeats regardless. No amount of preparation or strategy can eliminate uncertainty, so hold your head high in the tough times and remain humble in victory.

Luck's a fickle beast after all…

Welcome to all my new connections on X — all 22.6K of you. The reach here is powerful.

For those new: my work is focused exclusively on the intersection of TMT and power within the generative AI (GAI) infrastructure buildout. This is a multi-year, likely multi-decade capex regime. The approach is sector-first and systems-level, with investment horizons in sync with the duration and scale of this buildout regime — not quarter-to-quarter noise.

Over the past year, a core part of the process has been creating a full suite of equal-weight GAI sector indices from scratch — defining sectors, selecting constituents, and tracking capital flows across the stack. That exercise clarified where the true bottlenecks are — and where the highest probability alpha resides. It has been one of the highest signal inputs in the entire framework.

The detail feeds directly into the Custom GAI Index Dashboard, which is monitored throughout the trading day. It serves as a real-time view into where capital is actually moving — not where narratives suggest it should.

At the center of the portfolio are the “GAI TMT 4 Horsemen” — $NVDA $MU $SNDK $LITE . These represent my largest delta-dollar exposures and, more importantly, sit directly on the critical and required path of GAI infrastructure buildout.

An equal-weight index of these names is up 104.6% YTD — the strongest performance across any segment tracked.

For those interested in a deeper dive, an X subscription is available, offering more granular trade-level views, positioning, and direct Q&A. It’s priced at a nominal $1/month — deliberately low to maintain signal integrity and filter noise.

Inbound DM volume is high. If a message is missed, follow up or post publicly on my timeline.

This buildout is still in the early innings. The opportunity set remains asymmetric for those positioned with the right framework in place.

Stay disciplined. Stay focused.

$AAOI short-term, maybe they get some downside and an opportunity to cover. 24+ months hold, I absolutely would not be short $AAOI . The market doesn't seem to care about the @CitronResearch report.

I think this is a useful teaching moment, so I’ll try to expand on it a bit.

Over the last few weeks, I’ve heard a lot of statements like “most participants are short,” “everyone is hedged,” and “the pain trade is up.” But when you hear things like that, you really have to step back and ask: who exactly is doing what, and what evidence do I actually have to support it?

At a high level, markets can be broken down into a few key groups of participants:

Large tactical end users;

These are primarily hedge funds and active managers. They are trading to generate returns, and their flows are large, fast-moving, and opportunistic. Like the hedge funds listed in the original post below.

Small tactical end users;

This includes smaller RIAs and retail traders. The flows are smaller, but still active and reactive, often moving quickly in and out of positions.

Large passive end users;

These are large RIAs, retirement programs, insurance-linked mandates, and ETF issuers. They represent massive pools of capital, but their activity is slower and typically rules-based.

Small passive end users;

Your typical buy-and-hold retail accounts. Smaller in size individually, but collectively meaningful. Their behavior is generally steady and long-term oriented.

Non-tactical end users;

Sovereign wealth funds and very slow-moving pension or retirement programs that require 5 year long approval cycles. These are enormous in size but extremely slow to adjust positioning.

Now, if you think about how markets actually move, most short-term price action is driven by large and small tactical players, along with large passive flows. That is where the velocity comes from.

So if “everyone is short” and “the pain trade is up,” you have to reconcile that with reality. If that were true, why did so many of those players (like the hedge funds in the original post) lose money during a market decline? Why did large RIAs wealth programs lose money? Why did a broad set of passive products also take losses?

Once you look at actual performance across the street, the list of possible explanations narrows quickly.

Are pensions broadly positioned for equities to fall? No.

Are sovereign wealth funds leaning short equities? Also no.

Are buy-and-hold retail investors positioned for downside? Definitely not.

What people usually mean when they say “the pain trade” is that large and small tactical players are positioned in a way that would lose money if a certain outcome occurs. But when data objectively shows us the opposite, we have to accept that information.

It might sound elegant to frame things as some kind of 4D chess, but in reality, markets are often much simpler. Most of the time, when it comes to U.S. equities and larger drawdowns, the real pain trade is lower. It continues to seem like that is the case at this moment.

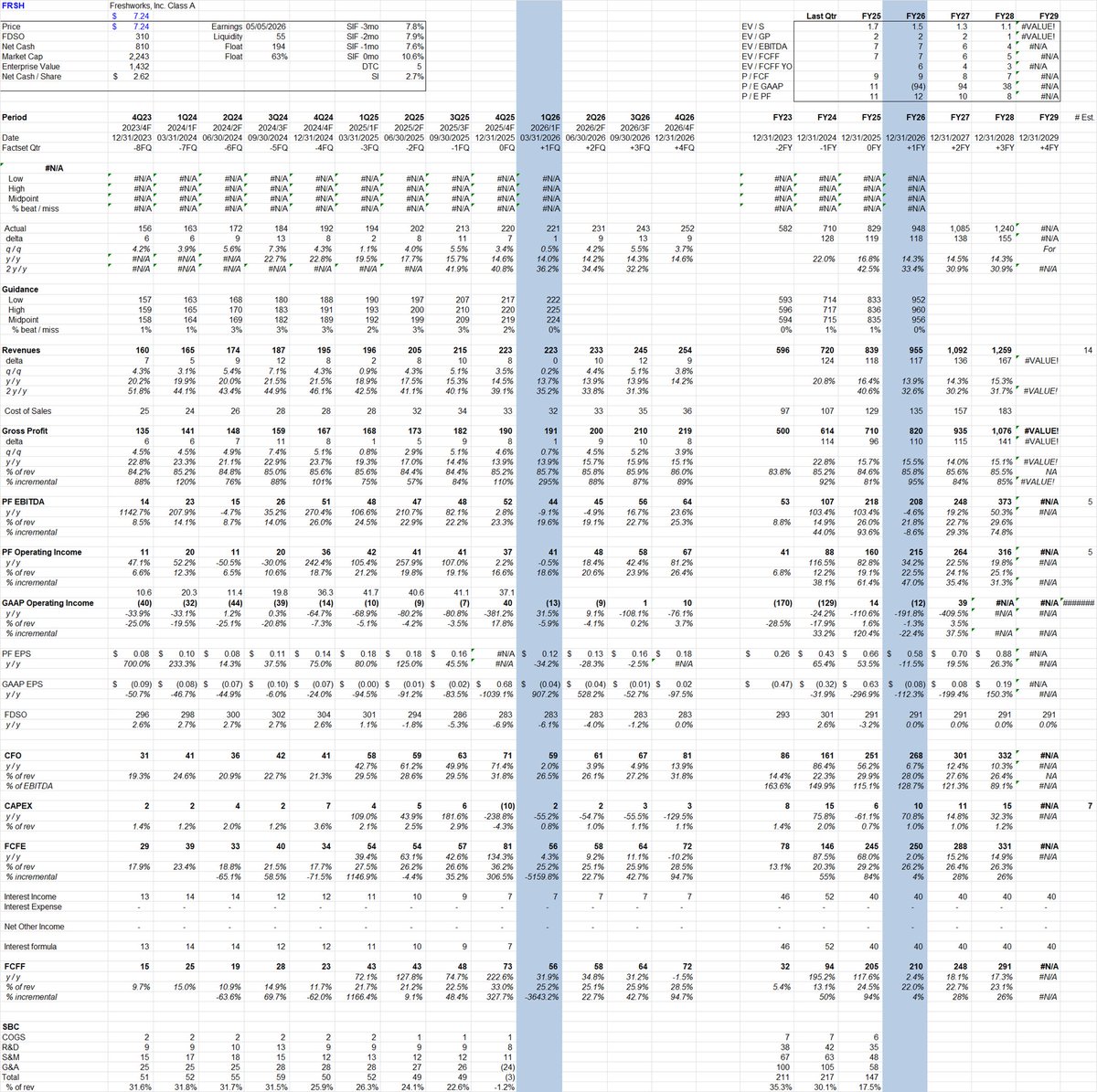

$FRSH reported a decent Q4.

Punchline is stock is just way too cheap.

Company has generic workflow software for customer / IT support. They did 840m in rev last year growing 16% yy and did 227m in Q4 growing 13% yy cc so slowing.

Highlights

-92k total customers and 8k have bought AI functionality which is at 25m ARR or 3% of total revenue

-AI customer cohort has a dollar net retention of 116% in Q4 up from 112% in Q3 .

-Took per interaction pricing up from 10c to 50c and no pushback from customers. This will flow through model going forward.

-50% of new customer wins taking AI functionality.

-Seat reductions not an issue because company is a share gainer and sees seat expansion. Pipeline great at high-end.

-Guidance embeds an expectation for a slight ACCELERATION.

-Will be GAAP profitable by end of 2026.

My take

So company has respected mgmt team improving capital allocation, is seeing reasonable traction with AI and accelerating and is profitable.

Using fully-diluted shares (including anti-dilutive ones), market cap is 2.2b w/ 0.8b in cash - so 1.4b EV.

Company generated 180m of unlevered FCF in 2025 so trading at 7.8x trailing FCF which will grow from here.

They guided to 250m in FCF for 2026. So P/FCF here so trading at 9x 2026 FCF, and EV/FCF of ~5.5x.

...for a growing, profitable business that is accelerating on the back of AI product adoption.

Like I said, I don't love the company but this is $TLEO level too cheap (see my last post).

I listened to the call replay while driving out to go skiing.

Pulled over to check financials and stock price, and couldn't help myself from buying some.

-11% downside to 8x 2026 street FCF

+93% upside to 15x 2027 street FCF ($14 - where stock was 2 mo ago).

Canonical AI Agent Coding Use (What I've Learned so Far)

Everyone has their own agent guide. I generally like reading other people's. I will try and provide mine succinctly

The loop that works:

Ideate → Design → Plan → Execute → Test → Use → Optimize Back End / Performance → Refactor → Track / Analyze → Return to ideate

Concretely:

1) Write a long product document that incorporates all your features and desired functionality

2) Go into Claude and ask it to split it into screens. Each screen should have a user story (I am a person logging into this app and I need to create a wallet)

3) Once user stories are done for each screen, create UX mocks for every single screen in Claude (it's fast and more responsive)

4) When a UX mock looks like shit use Gemini Pro to generate an image that would look better and feed back into Claude

5) Create a milestones folder

6) Take the output of #1 (your product doc) and all your user stories – feed that into Claude and make a normalized output (your project plan)

7) Instruct Claude or Codex to make a series of milestones folders. This will often be like 10-15 milestones

8) The milestones should explicitly link to your project_plan (alternately called a burndown list). The agents should understand that the project plan is always updated after a milestone is completed

9) Explicitly map milestones to appropriate UX elements. Instruct the agent to reference JSX or HTML/CSS designs and not to redo them unless necessary (you already did all that UX mocking)

10) Milestones have a https://t.co/eFkg5pFgoG, a completion_report.md, a code_review.md

11) Make sure your first milestones are actual app login so you're working against a live version of the app at all times

12) Each code review should identify security problems and P0s and be separate from implementation. Code reviews are actioned -- after you have tested a feature to make sure it basically works you pass it to make sure it's secure

13) After you implement all your P0 and P1 fixes you need to make sure and test your app (or figure out some way to have Claude Cowork do this for you. I've found this is not really a thing yet but some others have had success with it)

14) Periodically refactor (find long files, poor code design etc and refactor to be readable and maintainable). A good tell that you need to refactor is that there are 2000 line monster functions

15) Use your app repeatedly in new contexts. Start with fresh machines. Make sure to have deployment logic (local docker → staging fly → prod fly). Different apps have different deployment phases

16) Chances are at this point you have some kind of back end architecture. Databases of users etc. Once your app is kind of a thing and is running this is when you should do back end design. This is counterintuitive. Some chads will just do all of this up front with a perfect spec doc. For back end design tell the agent to be minimalist (use Postgres extensively, less managed services where possible, prefer open source). These agents love proposing overkill solutions and this pattern will only get worse as the agents are monetized via advertising to propose premium db solutions etc

17) Get your back end in order, re-test whole app

18) Do a full refactor after proper back end is up (this normally would be super expensive in terms of dev time). This means "make it extremely maintainable". have the agent define what the proper refactor would entail

19) When doing things like massive refactors encourage the agent to create a burn down list as they are context hogs

20) In Claude Code extensively use "planning mode" if you must use Claude Code. I prefer using Codex. Claude code is better for making documentation.

21) This is the right point to add tracking tooling. That could be uptime metrics, user tracking, prompt tracking (langfuse), Google Analytics etc. Tracking lets you know what is working and what is not working

22) Python based tests. Make sure that you can interact with different parts of your app using python scripts (get this set of users and tell which 10 are most active). etc. This stress tests your back end / makes sure it lines up with common sense

23) do your docs. make the docs not too wordy so they dont blow out LLM context

In terms of meta programming you need to impart some version of this process to https://t.co/g1Z7VtYYXl and https://t.co/GvybLnHPD5 (for Codex). Have it write what a good code review would be in the context of your repo.

Simple flow is: always have plan → milestones link to plan → milestones require code review → get milestone done → periodically refactor → track → alter plan

I am not yet at the point where I have orchestrators. Trying to get there. I am finally at the point where I'm building custom tooling which means that the labs will launch the exact tooling I'm building in 2-3 weeks. Whatever, AI is the jam.

There's a reason I've been preaching these plays. $FLNC $LAC $LAR for energy. $TGT $EBAY $FRPT for staples. $USAR for materials. Throw in some $SMR for nuclear. Boring trades aren't bad trades, they can do some crazy numbers in these conditions. Great time to buy value stocks.

Iran Clock Is Ticking - How To Profit

The U.S. is starting to escalate things with Iran, and if something is going to happen, it will likely take time before it actually does. These situations usually involve positioning, signaling, and buildup before any real action takes place.

Iran is a fundamentally religious regime, and that matters. When a regime believes its time may be limited, the range of actions it considers acceptable widens dramatically. There is no rational way for Iran to retaliate directly against the United States, so the remaining options are indirect.

One of the few levers Iran still has is destabilizing the oil markets. This is why I think Iran is far more likely to strike its neighbors rather than the U.S. directly. The analogy is simple. When you are a kid and someone much bigger is coming to beat you up and you know you cannot fight back, you do not go after them. You go after their younger brother or sister. Not because they did anything, but because hurting them hurts the person you actually want to get back at. That is the same logic here. Iran cannot hit the United States, so it may hit nearby countries or infrastructure to create maximum disruption.

This is also why I believe there is a connection between what is happening with Iran and what has already happened in Venezuela. The U.S. needed to stabilize the oil market somewhere else before risking instability in the Middle East. Securing Venezuelan oil supply helps keep a lid on prices in case Iran later tries to disrupt infrastructure or supply routes in the region.

If escalation occurs, oil is likely to react first and most violently. Equities would also come under pressure even without a direct link. I expect the Nasdaq to sell off, but not in a catastrophic way.

There are three ways to play this.

The first is long crude exposure through oil call options or $XLE. This is the most direct way to express geopolitical and supply risk.

The second, and what I am currently doing, is $QQQ put ratio spreads. I am buying one in the money put and selling three puts well below the money. I expect markets to remain relatively strong overall, and there is no reason for the Nasdaq to collapse purely because of Iran. But I do expect downside pressure. This structure benefits from time passing if nothing happens.

The third option is $VIX, but this is the most problematic way to play it. Contango in $VIX futures is very high right now. If nothing happens, long $VIX futures positions can lose a lot of money purely because of the structure of the curve. $VIX options may work in specific cases, but $VIX futures are not an attractive risk reward.

For me, the cleanest way to express this environment remains long oil options or $XLE, combined with $QQQ ratio put spreads. I do not need to be right on timing. I just need time not to work against me while waiting for volatility.