Phenomenal crowd at Basis Northwest, the preeminent event for all things taxable investment management, hosted by @TaxAlphaInsider

I really enjoyed presenting to my fellow tax nerds on the dominant theme in taxable wealth management today.

Every advisor thinks deeply about what’s in their Tech Stack. We’re building the leading TAX STACK to help advisors with the dominant shift from pre-tax product to after-tax implementation platforms.

Clients won’t tolerate packaged product. They demand portfolios bent around their objectives. They want customized Tax Design - the deliborate coordination of tax lots, cash flows, gifting, and tax loss harvesting across the household balance sheet - to maximize after-tax wealth.

We help advisors automate and coordinate this complex problem through our Canvas Custom Indexing platform.

@FTI_US@OSAMResearch

For any financial advisor or allocator interested in the tax management strategies, Direct/Custom Index, tax-aware long-short, 351, exchange funds, etc… follow Brent!

Schwab announced new limits on long/short SMAs today: 30% of adviser book, max leverage, min account size.

This is structurally different from Fidelity's recent moves, but perhaps has the same root cause.

Schwab's announcement mentions short security availability and pricing as an explanation.

These changes are frustrating to those I've spoken with, but I think the operational reality is that sourcing shorts is more fragmented and challenging than many initially anticipated and the custodian/brokers are adjusting to accommodate that reality.

DMs open if anyone has additional context.

May I offer a different perspective on the whole transatlantic family feud brewing over NATO.

Europeans are furious at what they call American unilateralism and "wars of choice," while Americans are done subsidizing allies who won't lift a finger when Washington actually needs them. Given all the sentimentality and historical baggage, there’s been a lot of bad blood and high grade insults thrown both ways.

A lot of pride here is at stake. But given that I am not American or European, what I can provide is an Asian perspective. The whole thing looks very different as there are no blood ties or cultural nostalgia to pull me either way. Because of distance, the default Asian lens on America has always been colder, clearer, and far more pragmatic than the European one.

Asians have never lived under the illusion that their relationship to the US is one based on shared values. If they ever did, the illusion was shattered during the Cold War. Instead, Asian nations saw the relationship to America as a cold, interest-driven bargain in a dangerous neighborhood full of communists, insurgents, and bigger powers.

Fast forward to today, and this lesson still holds. Japan, South Korea, the Philippines, Vietnam, Singapore and Indonesia all partner with America because their interests (not values) align - especially when it comes to countering China.

These nations have reasons to be alarmed about Beijing's ambitions in the South China Sea, around Taiwan, and across the Indo-Pacific. They don't need lectures about democracy or liberal international order to see the value in US forward presence, intelligence sharing, tech transfers, and security guarantees. It's a straight-up transactional deal: the US keeps the sea lanes open and the PLA at bay. Meanwhile, Asian nations host your bases, buy your weapons, and join your alliances (Quad, AUKUS, etc.). When interests diverge, they adjust pragmatically, without the drama and meltdown.

Probably not many in the West know this, but one of the forces that shaped this attitude was the US pullout of Vietnam and the rest of America’s Cold War shenanigans. Lee Kuan Yew was one of America’s loudest cheerleaders in Southeast Asia. In 1967 he flew to Washington, testified to Congress, and begged Lyndon Johnson (and later Nixon) not to cut and run in Vietnam. He warned that a hasty US exit would trigger the dominoes - Vietnam, Cambodia, Laos, and then pressure on the rest of Southeast Asia.

Singapore became a logistical hub, providing a haven for US troops on R&R, oil refineries supplying the American war machine, and Lockheed servicing aircraft. At one point, US military-related spending made up 15% of Singapore’s entire GDP. Singapore didn’t support the war because it loved American democracy but because it kept the communists tied up and bought Southeast Asia time to build up its own economy and military.

Then came the pullout - the Paris Accords in 1973 and then Saigon falls in 1975. Despite all the lobbying, despite the blood and resources America had spent, domestic politics in the US (the anti-war movement, Congress, Vietnam syndrome etc.) ended it. LKY watched in disbelief as the superpower that had promised to hold the line simply walked away.

The lesson was that American commitments are real only as long as they serve American interests and American voters don’t get tired. It’s a brutal one to internalize. LKY was disappointed and noted American “unreliability” but Singapore didn’t collapse into panic or anti-Americanism. They just recalibrated and kept pursuing pragmatism by building its own deterrent, diversifying partners, and later offered the US naval logistics access (Sembawang port) when the Philippines kicked them out of Subic Bay in the early 1990s.

Malaysia drew the same conclusion. The Tunku was pro-Western and anti-communist early on, but Malaysia never joined SEATO and pushed ZOPFAN (Zone of Peace, Freedom and Neutrality) instead. When the British announced their East-of-Suez withdrawal in 1968 and Nixon’s Doctrine (1969) told Asians “you defend yourselves first, we’ll just help,” Kuala Lumpur accelerated its neutralist tilt.

The message was clear - don’t count on Washington to bleed indefinitely for distant allies.

South Korea is similarly pragmatic but it operates under far higher stakes due to baggage from the Korean War and the ongoing North Korean threat. American intervention literally saved the South from conquest, resulting in a bond that is forged in blood. While South Korea had to learn the same lessons - that the American umbrella isn’t permanent, sharing a border with a nuclear-armed adversary forces tighter coupling with Washington.

The reverberations of Nixon’s 1973 opening to Beijing cannot be understated. It shocked the entire region that America, the great anti-communist crusader, suddenly would cozy up to Mao to counter the Soviets. If Washington could flip on core principles when interests demanded it, why should smaller states pretend the relationship was about anything deeper?

The core Asian critique of the European approach to dealing with America is that it is entirely bound up in moral values and civilizational kinship. This means that every disagreement feels like a betrayal and breeds resentment on both sides.

Because Europe is so hyped up on abstract values, it makes NATO feel like a sacred club that America is disrespecting. Asia's interest-based lens sees alliances as tools - useful until they're not. Maybe Europe thinks the Asian approach is cynical but the irony is that this is actually what keeps Indo-Pacific partners far more reliable counterweights to China than many NATO members ever were against Russia.

With both sides now coming to the negotiating table, we could see volatility calm down as we move into Spring... HOWEVER... the WH will likely continue to apply kinetic pressure to facilitate negotiations with China (and Iran via proxy) on a path forward.

It will take some time for the world to parse through the economic impact of intensified global competition, which will almost certainly impact supply chains, trade, and the global security apparatus.

In 2026, we have seen two dramatic security shifts - a reincarnation of the Monroe doctrine with VZ in the Western Hemisphere, and a rewriting of the status quo in the Middle East with Iran. A third will manifest at some point. With Japan set to re-militarize and US-Sino negotiations set to begin, expect a reset in Asia as well, though hopefully much more subtle!

While volatility may decline, one can argue it will settle in at either a higher absolute level or with greater dispersion within equity indexes until a clearer path is well-established.

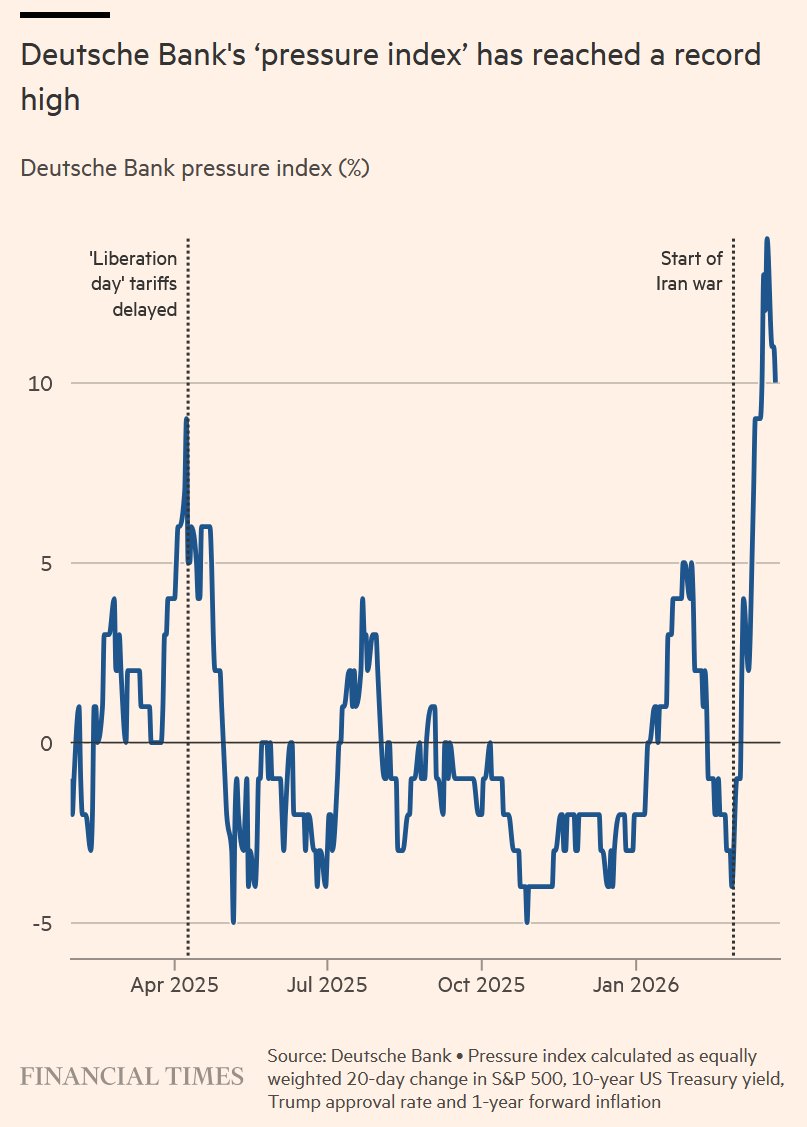

This is Wild.

Deutsche Bank has developed an index that helps to predict the next TACO by Trump.

It has proven effective in previous big Trump pivots.

The "Pressure index" combines one-month change in approval ratings, one-year inflation expectations and performance of the S&P 500 & t-bill yields.

The higher it goes, the greater the chances of 🌮

With both sides now coming to the negotiating table, we could see volatility calm down as we move into Spring... HOWEVER... the WH will likely continue to apply kinetic pressure to facilitate negotiations with China (and Iran via proxy) on a path forward.

It will take some time for the world to parse through the economic impact of intensified global competition, which will almost certainly impact supply chains, trade, and the global security apparatus.

In 2026, we have seen two dramatic security shifts - a reincarnation of the Monroe doctrine with VZ in the Western Hemisphere, and a rewriting of the status quo in the Middle East with Iran. A third will manifest at some point. With Japan set to re-militarize and US-Sino negotiations set to begin, expect a reset in Asia as well, though hopefully much more subtle!

While volatility may decline, one can argue it will settle in at either a higher absolute level or with greater dispersion within equity indexes until a clearer path is well-established.

The most challenging thing about this market environment is that global macro factor correlations are trending towards 1, which means portfolio diversification is disappearing beneath the risk models.

Look at a chart of stocks, gold, silver, bonds. It’s all correlated since the conflict in Iran broke out.

Oil is the only diversifier, and as we saw yesterday, that has its own risks.

Really tough time to allocate with conviction.

The most challenging thing about this market environment is that global macro factor correlations are trending towards 1, which means portfolio diversification is disappearing beneath the risk models.

Look at a chart of stocks, gold, silver, bonds. It’s all correlated since the conflict in Iran broke out.

Oil is the only diversifier, and as we saw yesterday, that has its own risks.

Really tough time to allocate with conviction.

Volatility set to continue this week as:

1. Despite the President's Friday tweet, kinetic actions are likely accelerating.

2. Degrossing and repositioning is rampant across asset classes.

3. Markets struggle to price in both an economic growth shock (recession) and an energy supply shock - obviously inter-related.

4. Equities are waking up to the possibility of a prolonged impaired growth trajectory.

5. Rates actually matter now to bellwethers given AI-related debt issuance.

There is currently an asymmetric downside to being early back into risk assets. Important to note in this regime that bonds are no longer risk-free given inflation risks. We've been discussing this structural shift for a few years with clients.

There will be an entry point, but it probably won't be a flash point as has existed in previous crises with the Fed swooping in to the rescue. They are hamstrung here in what I call Policymaker Purgatory.

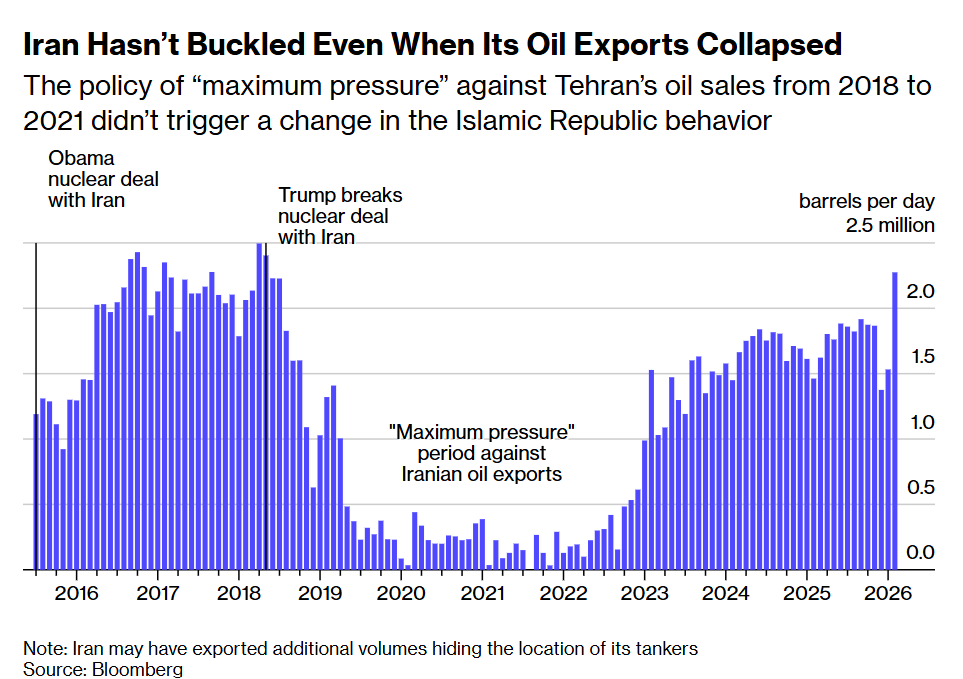

But Iran has weathered long periods of ultra-low oil exports. Back in 2020-22, Iran endured American "maximum pressure" on its petroleum industry, with exports at times down 90% from today's levels. And Iran didn't buckle then. Thus, it's unlikely to do so now.

🧵9/10

Volatility set to continue this week as:

1. Despite the President's Friday tweet, kinetic actions are likely accelerating.

2. Degrossing and repositioning is rampant across asset classes.

3. Markets struggle to price in both an economic growth shock (recession) and an energy supply shock - obviously inter-related.

4. Equities are waking up to the possibility of a prolonged impaired growth trajectory.

5. Rates actually matter now to bellwethers given AI-related debt issuance.

There is currently an asymmetric downside to being early back into risk assets. Important to note in this regime that bonds are no longer risk-free given inflation risks. We've been discussing this structural shift for a few years with clients.

There will be an entry point, but it probably won't be a flash point as has existed in previous crises with the Fed swooping in to the rescue. They are hamstrung here in what I call Policymaker Purgatory.

This is going to be a challenging week in financial markets ahead.

Investors will be forced to reconcile with either prolonged conflict or prolonged disruption in the flow of critical commodities.

Either gets you to the same place, some version of extreme risk: existential (the Gulf States raison d’etre), economic (everyone loses during kinetic conflict), and inflation (lock in of critical energy, AI, and agricultural commodities).

This conflict too shall pass, but on what timeline and what long-term impact to financial markets, nobody knows.

The WH thought Epic Fury would be as easy as Absolute Resolve (VZ).

Trump wants out, like yesterday.

As long as the surviving Iranian regime agrees to keep oil flowing and leave Israel alone, a deal can be done.

If so, there are two huge new massive suppliers of oil to the global market at a couple mb/d in the next few years,

Oil vol crushed, global oil supply glut.

One of the key challenges for the near-term was pointed out in @BobEUnlimited morning note, that wars are political, which is to say that the actions of the key players over the next few weeks may or may not be rational.

You have a series of actors in a conflict for which some face economic hardship, some economic demise, and others existential risk. The decision matrices don't align right now.

The reaction of market participants to whatever results will more likely be driven by their portfolio positioning, leverage, and realized volatility than their true view.

Take a low conviction approach and position for the range of possibilities. Whatever level of conviction you think you have, cut it in half, then in half again, and position accordingly.

This is going to be a challenging week in financial markets ahead.

Investors will be forced to reconcile with either prolonged conflict or prolonged disruption in the flow of critical commodities.

Either gets you to the same place, some version of extreme risk: existential (the Gulf States raison d’etre), economic (everyone loses during kinetic conflict), and inflation (lock in of critical energy, AI, and agricultural commodities).

This conflict too shall pass, but on what timeline and what long-term impact to financial markets, nobody knows.

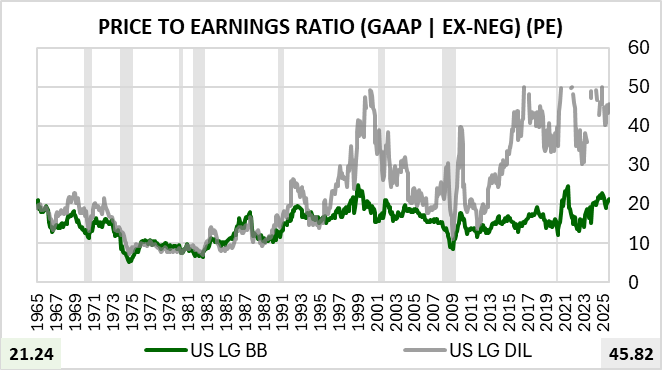

@dampedspring it is empirically true that stocks with high buybacks are on average priced cheaper and have better fundamental growth than high dilution stocks

chart below US LG BB = US Large Cap High Buybacks, US LG DIL = US Large Cap High Dilution

The Federal Reserve received grand jury subpoenas from the Justice Department on Friday that threaten a criminal indictment relating to Chair Jerome Powell’s testimony last summer about the central bank’s building renovation project

Powell statement: https://t.co/qDMqOngobs

@BradHuston Bob has been a gold bull for years. Why is it unreasonable to change one’s opinion after a 100% run in an asset class and a 12% depreciation in USD?

There is a rhythmic life cycle of personalities on this app. It’s a shame because many get ridiculed unfairly. It’s usually the ones that grow their followers the fastest that succumb because they get lured into the sense that it’s a “community”. Somewhere along the way, the algo turns. People pile on. It’s sad.