@Invesquotes Copart management walked-the-walk with their own money. There's a lesson in that. That $10mm in foregone compensation is now worth $1.7 billion.

https://t.co/VFNsVzoOxt

In Apr 2009, $CPRT's CEO Willis Johnson and Pres Jayson Adair each agreed to forgo their next 5 yrs of comp in exchange for 2mm options. A bold proposal to say the least.

3 splits later that $10mm in forgone comp is now 16mm shares valued at over $1.3 billion. Not a bad trade!

@Billhuang1223@ttril22 I think they have a lot of pricing power. They've had no issue increasing prices in the past.

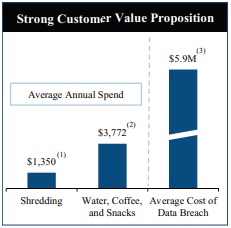

Document destruction is a very low cost service w/ high value. Most businesses take info security seriously and wont price shop to save a few dollars a month.

https://t.co/8ke7jMp8vB

Redishred $KUT.v just released FY24 targets: $9mm in FCF, up from $7mm last yr.

Current market cap is $52mm, bringing the valuation down to 5.8x FCF.

Strong growth outlook too. 6% shred comps in Q1 + atypically large ~6% pricing increase in Q2 should help drive FY25 FCF.

@ttril22 In this case I think value will be its own catalyst.

Other potential catalysts, however, include: pricing increases driving margin expansion, M&A, higher paper prices, a sale of Shred-It that highlights private market value, share repurchases, a sale of the business, etc.

@bsg_cap Family controlled and family “doesn’t care about shareholders”, stock hasn’t gone anywhere for years and won’t until they start returning capital, “dependent” on backlog, lumpy revenues, if the multiple is so low the market must know the business is about to collapse, etc etc.

With $DRX.to at $17.70, this is now an 11-bagger from $1.60 back in Oct 2021.

It's slightly amusing to remember that ALL of the feedback I received then was how terrible the investment idea was too.

Dance to the beat of your own drum. Most of the chirping on here is noise IMO.

ADF Group $DRX.to is a leading steel fabricator with a focus on complex projects and is one of the most undervalued $50+ million market cap companies IMO. Trades for 2.9x EV/EBITDA, 4x FCF, 52% of tangible book value.

With $IBT.v being acquired at a 2.6x premium to when this growth trio was declared, we were left with only two constituents. Let's restore the trinity, there's lots of opportunity out there.

The Holy Trinity of Microcap Growth v2

$KUT.v 6x FCF 15% TTM growth

$DRX.to 9x FCF 32% TTM growth

$PHA.v 3x FCF 48% TTM growth

All attractive niche businesses with exciting growth prospects. Canadian microcap is such a weird and wonderful pond to fish in.

The Holy Trinity of Microcap Growth?

$KUT.v 7x FCF 64% TTM growth

$DRX.to 4x FCF 40% TTM growth

$IBT.v 3x FCF 33% TTM growth

All attractive niche businesses with exciting growth prospects.

Canadian microcap is such a weird and wonderful pond to fish in.

Now I take any five year forecast with a grain of salt, but $DRX.to mgmt made it very clear on the call that in addition to a bullish FY25 forecast, the longer-term outlook looks strong to them as well.

ADF's $DRX.to CEO joined the CC to curb stomp the bear thesis:

"...we see a lot of work for the next 3 to 5 years. okay? A lot of work, a lot of battery plants, a lot of airports, a lot of bridge. So I would say for the next 3 to 5 years, market is going to be very, very good."

ADF Group $DRX.to results out on Thu.

I find it particularly interesting that the CEO will be co-hosting the CC.

CEO usually has the CFO host all CCs and only joined for the breakout Q1 CC. Hard to imagine he would go out of his way to host the CC for a disappointing qtr IMO.

You can listen to the whole interview with $DRX.to here.

The CFO also addresses the growing backlog and capital allocation, among other topics.

https://t.co/waqKTYKggN

ADF Group $DRX.to published an excellent mgmt interview in Feb 2024.

The section on margins was particularly bullish IMO, with mgmt stating:

"The margin we've been able to produce... we should be able to keep them in the same range, hopefully increase them in coming quarters"