Benoît van den Hove, CEO van Euronext die ik erg waardeer, waarschuwt voor de opdrogende liquiditeit van Belgische smallcaps. De schuldige is mede de meerwaardetaks. Te lezen https://t.co/BarAz7YcP1

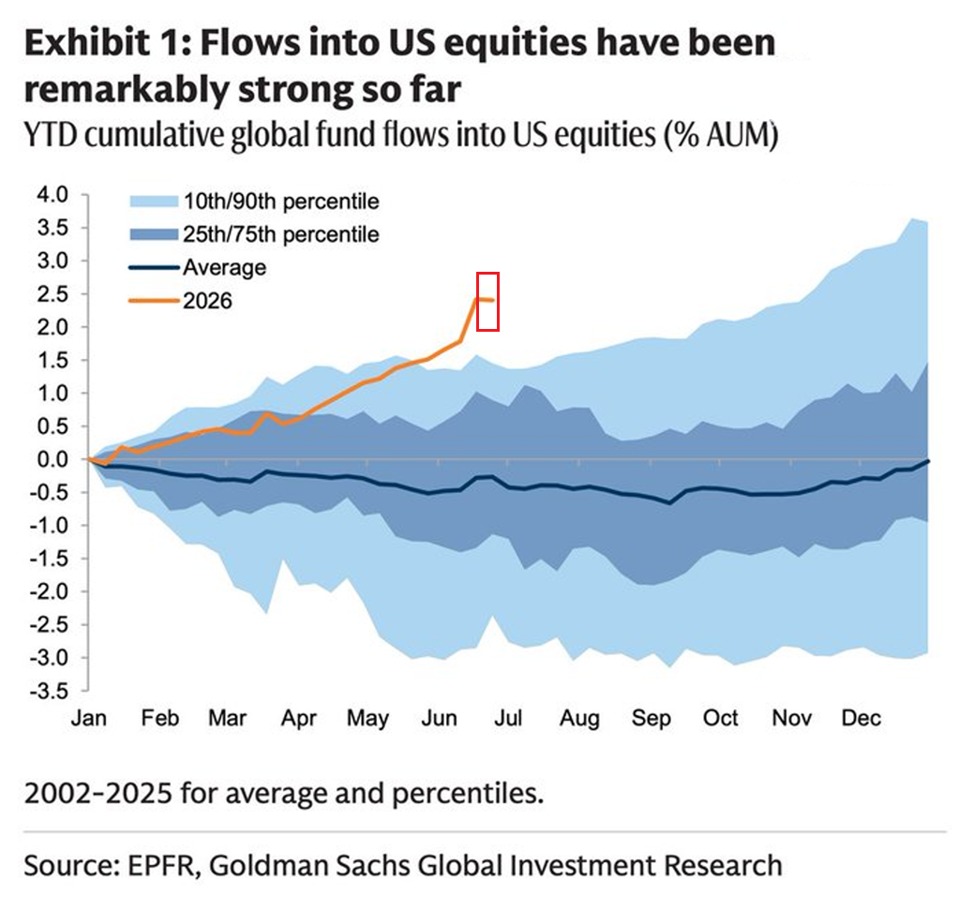

Foreign investors are piling into US equities at a record pace:

Cumulative year-to-date inflows from global investment funds into US equities are up to ~2.5% of their total assets under management.

This percentage has more than DOUBLED since May alone.

This is also significantly above the 2002-2025 average of -0.3% in outflows for this point in the year.

By comparison, excluding the top 10% with the largest inflows and the bottom 10% with the largest outflows of the 2002-2025 period, global fund inflows averaged just ~1.5% by this point in the year.

The YTD pace has already exceeded the full-year total recorded in the middle 50% of years since 2002.

Current demand for US equities is unprecedented.

Er is in Vlaanderen amper publiek debat over de invoering van de digitale euro. Dat is zeer bizar. De gevaren zijn gigantisch. In het Europees Parlement klonk enkel groot applaus van klassieke partijen.

De VRT nam bijna klakkeloos de communicatie van Europese Commissie over. Alle - nochtans zeer terechte- bezorgdheden en gevaren worden wel besproken. Maar dan onder de noemer "complottheoriën".

Dat is onbegrijpelijk. Dit is de grootste verandering van ons geldstelsel sinds de afschaffing van de goudstandaard. Mensen gaan voor het eerst geld aanhouden bij de overheid in plaats van banken.

Het is echt niet zo denkbeeldig dat de overheid daar in de toekomst willekeurig gaat in sturen. Academici als Koen Schoors pleiten nu al om geldbestedingen te controleren, zoals "bijvoorbeeld enkel in groene investeringen".

En ja, er zijn daar safe-guards in voorzien in de huidige voorstellen. Maar wie zegt dat die later niet aangepast zullen worden? Zo is het vrij aannemelijk dat overheden gaan beslissen om enkel nog betalingen voor overheidsopdrachten of fiscale zaken via de digitale euro te aanvaarden. Dat kan daarna stap voor stap uitgebreid worden.

Er is een reden waarom gelddeposito's tot nu toe niet onder controle van de overheid staan. Sterker nog: het banksysteem is ontstaan uit een fundamenteel wantrouwen tegenover de overheid.

Geen enkel groot publiek debat over. Bezorgde tegenstemmen worden afgedaan als complotdenkers. Foute boel.

In januari 2018 schreef de onnavolgbare Kaaiman ( Koen Meulenaere) in @tijd één van zijn vele pareltjes. Meer dan 8 jaar na datum ( en elfendertig extra taksen later) nog altijd brandend actueel.

of hoe extra belastingen, je groei helemaal kapot dreigen te maken

Rijkentaks ontploft in gezicht van Les Engagés: Odoo-topman dreigt België te verlaten https://t.co/lnrcPXmpcn

Last week I published "The Fatal Conceit, Renewed." Today I publish its companion: a catalogue of the methodological errors in the work of Thomas Piketty and Mariana Mazzucato.

The errors are not peripheral. They are devastating — and they all lean in the same direction. In econometrics, we have a name for an estimator whose errors all point one way: biased. In politics, we also use the same name.

Why spend the effort taking these two apart? Because they are dangerous. Piketty and Mazzucato are the intellectual darlings of today's left. They supply a veneer of scholarly respectability to what the left is forever seeking: a justification for higher taxes and more state intervention. The oldest idea in politics — that a few enlightened people know better than the rest of us what to do with our money.

The fame is real. The findings are not. Here is the audit.

Over de centenindex en het alternatieve voorstel van de sociale partners: jammer dat alles in één geheel wordt bekeken. Het zijn eigenlijk twee verschillende discussies.

Een draadje 🧵

@NunoGalo In Belgium we did not realy observe this after the last ECB rate hikes in 2022-2023. Interest rate margins and RoE of banks increased, though admittedly less than in other countries, as bankdeposit rates did not rise that much. What am I overlooking?

We zijn een low-risk, low-return-maatschappij die de voorkeur geeft aan vrije tijd boven werkuren.

Aan herverdeling boven disruptieve groei.

Aan stabiliteit boven dynamiek.

Dat kan legitiem zijn. Maar dan moeten we ook durven uit te leggen wat de gevolgen zijn. Minder economische groei. Minder grote bedrijven. Minder technologische doorbraken. Minder economische dynamiek. Langzame geopolitieke irrelevantie. Een passieve toeschouwer van wat in de wereld gebeurt.

Europeanen zien succes vaker als een kwestie van geluk of een inherent oneerlijk systeem.

Wie gelooft dat het systeem oneerlijk is, wil herverdeling.

Wie meer herverdeelt, moet meer belasten en betonneert zwakkere economische groei in het systeem.

👉 @PeterDeKeyzer in @trendsbelgie. Lees zijn tweewekelijkse columns hier 👉 https://t.co/DbATVWMGta

We stopped everything to write an answer (link below) to Paul Krugman's two posts of today (one informal, one with a simple model) arguing that Europe is broadly not falling behind the United States.

The change measured by the Draghi report, he argues, is mostly due to growth in the technology industry, which has distorted GDP numbers without actually leading to higher standards of living. We should believe our eyes when we walk around France and walk around Mississippi.

Krugman is wrong. The measures he uses understate European stagnation. This matters enormously. Divergence with the United States is the strongest evidence for reform in Europe.

1. The growth numbers

Krugman compares the United States, France, and Germany at purchasing power parity in current prices. On that measure, France's and Germany's position relative to America has been roughly constant since 2000.

But current price comparisons miss productivity gains in sectors where prices fall. If America produces twice as much software while the price of each unit halves, the value of American software output looks unchanged even though the volume has doubled.

Most economists therefore use constant prices, which fix the base-year PPP level and apply each country's real output growth on top of it. American output growth has concentrated in tech, where prices have fallen tremendously as productivity rises. In terms of the volume of things produced, America has pulled away from Europe.

2. Is it all the tech industry?

Krugman concedes this tech divergence but says it is not welfare-relevant. The American growth lead is an accounting artefact of measuring more iPhones at base-year prices, not a sign that Americans are actually richer, because Europeans buy the same iPhones at the same world prices.

This is not the right way to think about the world today, as an earlier Paul Krugman would have argued.

His model assumes tradable goods, interchangeable workers, marginal-cost pricing, and no profits. Each assumption fails.

Most of what households buy is non-tradable: housing, healthcare, childcare, education. When American tech firms bid workers from haircutting to coding, American haircut wages rise. Germany has no growing tech sector to do the bidding, so German wages stay flat.

Technology is not priced at marginal cost. Apple's margins are around 40 percent. Anthropic's inference margins are at 70 percent. The major platforms enjoy network effects, switching costs, and lock-in that hold prices well above what a competitive market would deliver. A large share of the productivity gains in technology stays as profit.

A lot of the value of American technology dominance shows up in equity, not in wages. Apple, Microsoft, Nvidia, Alphabet, Meta, and Amazon together are worth $21 trillion, more than the entire combined stock market value of all European stock markets. Around 60 percent of US equity is held by American households. The median French or Spanish household holds almost no equity.

The median employee at Meta, a company with almost 80,000 employees, earned $388,000 in 2025.

This advantage is not going to go away. Krugman's own 1991 paper, cited in his Nobel prize, showed that comparative advantage in modern industries is produced by increasing returns to scale, specialized labor markets, supplier networks and the agglomeration of suppliers, workers, and ideas in particular places. Once an industry concentrates somewhere, the concentration is self-reinforcing. Europe is being pushed away from the next round of technology industries (AI!).

3. What about inequality?

Another retort is that GDP per capita hides substantial inequality, and so even if America is rich on average, this is mostly due to the super wealthy.

But despite the US's high pre-tax income inequality, it also achieves higher median incomes than Europe, in part because of such a high base, and in part because it actually redistributes more than many European countries.

The cleanest comparison is median equivalised disposable household income: income after cash taxes and transfers, adjusted for household size and purchasing power. According to the OECD's 2021 numbers, the median American earns 30 percent more than the median Dutchman, about 31 percent more than the median German, and about 52 percent more than the median Frenchman.

4. What about hours worked?

Krugman points out that while American GDP per person is higher, most of this is because Americans work more. For this divergence to be an hours worked story, Americans must work more relative to Europeans now than they did in 2000.

The opposite has happened. Birinci, Karabarbounis, and See in a 2026 NBER paper show that about half of the American-European hours gap that existed in the 1990s has reversed by the end of the 2010s. Americans work fewer hours per person than they did in 2000, while most Europeans work more.

5. Is America not a bad place to live?

Walk around Alabama and France: surely the former cannot be substantially richer than the latter?

American cities often have poorer centres and richer suburbs or exurbs. European cities preserve richer and more attractive historic cores. A visit to a city as a tourist in America compared with a city in France will leave one having seen different spots on the income distribution. Americans in Europe go to the nicest and richest European cities.

Rather than a walking around test, do a driving around test. Go to the periphery of any modern American city and see a level of new-built material wealth that is extremely uncommon in Europe, with thousands of enormous four- or five-bedroom homes. In the South, in places like Nashville and Austin, drive around the downtowns to see hundreds of luxury apartment buildings springing from the ground. This construction boom is replicated virtually nowhere in Europe today.

The other question is generational. Housing often costs more in Europe than in the United States, despite the quality of the housing stock generally being much better. Europe has nice city cores but these are inaccessible to young Europeans.

Consider the salaries available to entry-level workers. The starting pay for a London police officer is $57,000. In Washington, DC, $75,000. The entry-level Deloitte consultant job in Madrid pays around €28,000, roughly $33,000 per year. In Charlotte, the entry-level Deloitte job pays $63,000.

There are many things to dislike about life in America. But relative to 25 years ago, the gap in material wealth has shifted dramatically in America's favor.

https://t.co/VOpQ32R5tg

Overseas investors are piling into US stocks:

Foreign investors now allocate a record 63% of their US financial assets to equities.

This percentage has more than DOUBLED since the 2008 Financial Crisis.

This also surpasses the 2000 Dot-Com Bubble peak by ~10 percentage points.

By comparison, the long-term average allocation is ~40%.

As a result, foreign investors now own a record $21.3 trillion in US stocks and equity funds, surging +170% since 2020.

Foreign investors are doubling down on US markets.

Omdat #1mei elk jaar leidt tot Trumpiaans fake news: de 10% hoogste inkomens betalen 46% van alle personenbelasting. De hoogste helft betaalt 93%. De rest dus bijna niks. Wie solidariteit belangrijk vindt ontkent best niet het bestaan ervan, uit respect voor wie het feest betaalt

Vandenbroucke 'vergeet' iets belangrijk in dit gesprek.

🤫

Hij weet namelijk al 5 jaar dat het weghalen van controle-artsen bij de ziekenfondsen een realistische piste is. Sterker, hij heeft daarover een advies op zijn kabinet liggen.

Het is o.m. getekend door... artsen van ziekenfondsen.

👇

Het advies is eind 2020 opgemaakt door een aantal professoren, oud-ambtenaren en arts-directeurs van de mutualiteiten en was het resultaat van een denkoefening die ex-minister Maggie De Block in gang heeft gezet in 2018.

Daarin staat letterlijk:

"We stellen voor om voor alle verzekeringsartsen één enkel agentschap op te richten dat de enige werkgever zal zijn."

"Dit systeem zal aanzienlijke schaalvoordelen mogelijk maken en de onafhankelijkheid waarborgen bij het nemen van beslissingen."

Die laatste twee punten zijn cruciaal.

Het betekent namelijk dat het huidige systeem volgens die werkgroep duidelijk onvoldoende efficiënt is en te weinig garantie biedt op onafhankelijke medische beslissingen over arbeidsongeschiktheid.

Exact wat de laatste maanden - op verschillende manieren - pijnlijk duidelijk is geworden.

Maar met het advies is nooit iets gedaan. De minister heeft het aan de kant gelegd.

Dat is zijn recht.

Maar kom dan 5 jaar later niet voor de camera zeggen: "We kunnen geen nieuwe boot bouwen, want dat duurt te lang."

Hij heeft 5 jaar de tijd gehad om aan de 'nieuwe boot' te beginnen, maar heeft dat bewust niet gedaan.

Ondanks een duidelijk advies dat zo'n 'nieuwe boot' nuttig kan zijn.

Die beslissing kost de sociale zekerheid helaas veel geld.

1) You might have missed it but the EU just published the CMDI package – one of the most consequential pieces of bank regulation. It fixes something that has been really embarrassing about European banking regulation for more than a decade. And the impacts are huge.

Een duidelijk signaal dat we moeten kiezen voor duidelijke en transparante hervormingen.

Niet voor steekvlam- en symboolpolitiek.

Politici dragen hier een verpletterende verantwoordelijkheid.

Slechte begroting levert België nieuwe ratingverlaging op https://t.co/bRKS2ZAATA

- nieuwe ratingverlaging

- volgens IMF op weg naar 2e hoogste tekort onder de industrielanden in 2031

- oplopende overheidsschuld niet onder controle

Ondertussen gaat de discussie over brede energiesteun en stond in de kranten hoeveel de belastingverlaging zal opleveren

#lalaland

Wekenlang discussiëren over (overbodige) energiesteun om de achterban te paaien, terwijl het nieuws verschijnt dat België de slechtste begroting heeft van de eurozone én nu ook nog een kredietverlaging.

Neem uw verantwoordelijkheid, en trim de uitgaven!

https://t.co/naEGKuD09b

Deze aflevering van @vrtpano was onmogelijk om helemaal uit te kijken.

Quasi elk argument kon ik weerleggen. Amateurisme troef.

Ik was te lui om het op Twitter te weerleggen, maar zal toch een paar dingen zeggen.

Disclaimer: ik ben geen expert. Mij verbeteren mag.

🧵