Investors believed factories and physical assets were the best inflation hedge.

They had it backwards.

Asset-light businesses with strong franchises keep most of their earnings. Asset-heavy ones must reinvest constantly just to stay in place.

— Warren Buffett (1983 letter)

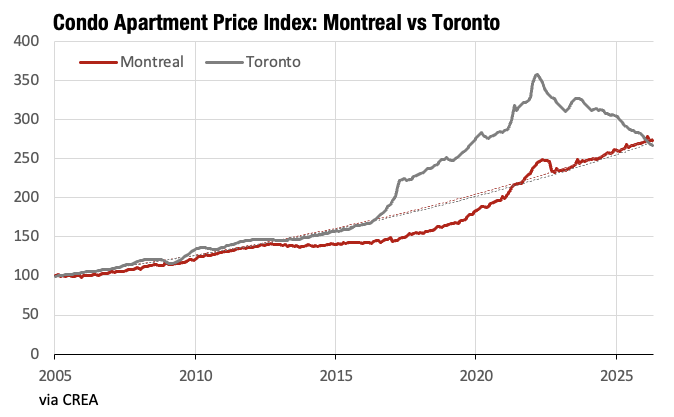

If you purchased a condo in Montreal in 2005, you are now outperforming your friends in Toronto who did the same.

But there was a 20+ year period when the Montrealer was envying Toronto's relative outperformance.

What happened here?

This can be a very aggressive portfolio for many investors.

The 90/10 rule is a model for investors who can tolerate volatility and have long term horizons (10+ years).

BMV Group $BOLSA.MX

- Operates Mexico's only stock exchange

- Zero debt, large cash position (~20% of market cap)

- 20%+ ROE & ROIC

- Increase from 3M to 25M retail investment accounts in Mexico

- Repurchasing shares

- Trades at 12x 2026 EPS

- 6% dividend, 70% payout ratio

Bill Ackman (All-In Podcast interview):

“Look, when you're a concentrated investor, or investor generally, and you're a long-term investor, the most important and most challenging thing to do is determine what's the risk of disruption.”

Suppose you make 20 or 30 real long-term bets over the course of your investing lifetime. If you are successful in making sure that your potential downside over the long-term for every one of them is either nothing or very small, what are you left with?

What you have is a collection of bets where all that's left is potential upside. Maybe some work out very well, and maybe some don't. But your starting point is one where you won't lose money. That's an extremely constructive starting point.

Spend 85% of your research time thinking about the downside. Moat, competition, runway, valuation, disruption, risk of the business model itself, the balance sheet. Spend almost all of your time on these things.

BERKSHIRE HATHAWAY'S VERDICT ON THE CONSUMER: 16 Full Exits, Zero Exceptions & What the Sell List Tells Us About the Consumer Meltdown and the Policy Response That Follows! https://t.co/RzMqRPERQJ

The latest quarterly results from my pick showed broad-based growth across all key metrics — and meaningful market share gains in dollars and volumes.

Management has cleaned up the balance sheet and is in a position to restart aggressive share buybacks soon — while the rest of the sector is forced to protect dividends they realistically should cut.

I don`t know why Fundsmith initially invested in

$OTIS but selling the shares at these prices/valuation doesn`t make a lot of sense with service revs and fcf highly likely moving up HSD going forward?!

*BERKSHIRE TO ACQUIRE TAYLOR MORRISON FOR $72.50 A SHARE IN CASH

First $BRK.B acquisition in forever - buying $TMHC for $8.5B all in, or $72.5 / share all cash

Most investors are aware of Akre's home run with American Tower.

In 2002, he bought $AMT shares as low as $0.79 per share. These shares were worth close to 50x their cost within only 5 years and close to 100x within a decade.

But Akre didn't start buying $AMT in 2002. He started in 1998, buying shares at a cost basis of $22. This means that $AMT plunged 98% between 98 and 02.

Both the $0.79 and $22 purchases would beat the S&P over a long period of time.

Investing is fascinating.