Top Osimertinib Resistance Expert Dr. Zofia Piotrowska Strengthens Credibility of Nuvectis Pharma's NXP900 Combo Study

$NVCT $AZN $JNJ

https://t.co/x1M4d8uHl8

The NXP900–osimertinib combination trial was posted Friday on https://t.co/MsoF3ttsMV The most noteworthy detail was the listing of Dr. Zofia Piotrowska at Massachusetts General Hospital (MGH) as Principal Investigator.

It is rare for a clinician of Piotrowska’s stature to lead a microcap-sponsored early combination study unless the biology is compelling and the study is designed with real translational intent. MGH physicians operate under some of the industry’s most stringent institutional oversight regarding industry interactions. Their leadership in a trial is a form of scientific “institutional vetting” that signifies that the protocol has passed a gauntlet of internal reviews and that the PI views the drug as a legitimate potential successor to the current standard of care.

Dr. Piotrowska is widely regarded as one of the field’s leading experts on EGFR-mutant NSCLC and was an investigator in AstraZeneca’s landmark FLAURA program. She has since been a definitive voice in mapping the post-FLAURA landscape: a reality where resistance is no longer a simple “on-target” mutation, but a complex web of heterogeneous bypass signaling.

This framing is directly relevant here. While Tagrisso (osimertinib) is a ~$7.5B global franchise, nearly all patients eventually progress. Many of these tumors retain EGFR lineage dependence but sustain survival through bypass circuits, including SRC/YES1-mediated signaling. This circuit can stabilize EGFR and maintain downstream survival pathways like SRC–FAK–YAP1 even with ongoing osimertinib exposure. NXP900 is designed to shut down this “bypass hub,” a node active in roughly 80–85% of resistance cases, to restore sensitivity to EGFR blockade.

Just as important, this is not a generic all-comers combo. The trial is being genomically enriched by excluding tumors with established non-SRC bypass mechanisms, tightening eligibility around settings where SRC/YES1 biology is most likely to matter. At a site like MGH, where patients are routinely re-biopsied at progression, this improves molecular matching and increases the odds of a clean signal.

$ABVX

STIL here is making another highly relevant point - What he is referring to here is basically the "latency" point. It basically goes like this:

"A cancer signal seen so early is likely not a real cancer signal because cancer doesn't "develop" that fast. What you are actually seeing is "latent" cancer that was there but undetectable at baseline."

This is also why it is important that...they've had >100 patients on the drug for ***5-7 YEARS WITH ZERO CANCERS***. If it was a "super mega carcinogen" you'd now from the extremely long phase 2 study!

How could it be possible that the drug somehow causes cancer in a few weeks after NOT causing it in 5-7 YEARS? The answer is *IT DOESN'T* - what we saw in those 2 cases in the P3 is just statistical NOISE!

I expect sharper minds to look at these facts and come to the same conclusion tomorrow.

I keep hearing people referring to "7" cases of cancer in the high dose arm for $ABVX. I get it - that's what they technically showed in the table, but in observing a lot of conversation about this I gather that people don't actually realize what really matters there. I am strongly of the opinion that there are really only 2 malignancy cases that matter for adjudication - the prostate cancer and breast cancer cases.

I initially started talking about these cases as "the 2" cases from the very beginning because I assumed that everyone would be on the same page that these were the only 2 that mattered...but I've found that people really are considering this as a case of *7* full blown malignancies in the 50mg arm...This is just not correct.

Let's break this down.

First of all, they're counting "colonic dysplasia" in this table as one of the "malignancies". I cannot stress this enough: Colonic dysplasia is, by definition, LITERALLY not cancer. This is actually an unequivocal point that I don't understand how it could even be up for debate.

"Dysplasia" is a "precancerous" lesion. Cervical dysplasia, colonic dysplasia, melanocyte dysplasia. Terms exist for these PREcancerous findings because they are, by definition NOT CANCER (otherwise, if they were cancer, we'd call them cervical cancer, colon cancer, and melanoma)...

Dysplastic lesions, not being cancer, often regress on their own or simply never evolve into cancer, staying in the "dysplastic" state until death. However, if they *do* become cancer, they do so through a process that is called "malignant transformation". Literally, something that is NOT malignant TRANSFORMS into something that is.

Why did the ABVX management team include this in the list of "malignancies"? Honestly, I don't know. I think it is an evident mistake, and a strong piece of evidence that they didn't think they'd actually have to explain away a "cancer signal" in this dataset because their analysis of the data told them that there isn't one. If they were worried that the market was going to interpret these data as a catastrophic malignancy risk (which, make no mistake, is what the current low $70s price tag is assuming), they would've likely adjudicated this more thoroughly and left the "malignancy" that is by definition NOT malignancy off of the "malignancy" table...

So that is tossed out easily IMO. 6 cases left now. 4 of those are NMSC (non-melanoma skin cancer). I gather that people are dramatically overestimating what a diagnosis of NMSC means. Far be it from me to minimize NMSC (since it is what I treat for a living as a dermatologist), but guys....this is NOT in the same category as ANY other malignancies. NMSC is a milder category of its own, and I don't mean that as a matter of opinion. Literally, "non-NMSC malignancies" is a distinct endpoint used to gauge risk of "serious" malignancies in clinical trials. NMSCs are left out of that category because they almost never are "serious" - certainly almost never life threatening.

Here's an exercise anyone can do to drive this point home. Google, or ask an LLM "what are the 10 most common cancers in the United States?". They are all going to give you the same answer: Breast & prostate will be the top 2 at slightly >300,000 cases/year.

So breast and prostate are the #1 and #2 most common cancers according to every source...except, those sources either ignore completely or footnote at the bottom that there is a type of cancer 15x more common...NMSC!!!

The point? Ubiquitously, NMSC isn't even included on the list of "most common cancers" because they're frankly in a separate category altogether from cancers like breast and prostate. It actually is controversial whether or not it is even possible for basal cell carcinoma to metastasize, and (aside from transplant patients), CSCC is almost never fatal unless left ignored/untreated for years (people ignoring a giant bleeding skin cancer is perhaps more common than you'd think, but not happening in any clinical trial patients).

These 4 50mg NMSC cases (vs 1 in the placebo group) are a not representative of serious malignancy risk even if the market is acting as if they are...they are absolutely in milder a category all their own, and lumping these all together is a mistake.

Again, if people think these 4 NMSC cases are some scary life threatening event, they're just flat out wrong. There are >15x more cases of NMSC than breast cancer in the US/year, yet >10x more breast cancer deaths occur in the US per year.

Again, not to minimize my own career too greatly, but almost *always* NMSC are removed by VERY simple, ~10 minute procedures under local anesthesia. Cutting out (or scraping away) the lesion typically takes me around 60 seconds, and the bulk of the procedure is actually spent stitching the patient back up. Drive yourself to the office, drive yourself home, local anesthesia, under an hour, you're cured. Hell, in many places in Europe it is actually standard practice to not even "treat" a basal cell carcinoma! On many body locations they are simply biopsied, and once diagnosed they are considered cured by the biopsy itself!

It has become very clear to me that people are thinking that these NMSC cases are highly relevant cases of severe, potentially fatal cancer. They simply are not. There are *millions* of these in the US per year and most are treated with <15 minute procedures. These are in a TOTALLY different, far less serious category of "cancer".

So again, why wasn't $ABVX prepared to discuss/explain this? I legitimately think they did not expect to need to. They may have overestimated the market's knowledge here and underestimated its potential for a knee-jerk reaction to the "C-Word". It's a mistake, yes, but it ultimately doesn't change the profile of the drug.

So, I think we have compelling cases to write off the colonic dysplasia (literally not cancer) and NMSC cases, as I have usually found to be standard in these situations.

That leaves the breast and prostate cancer cases. Again, the otherwise #1 and #2 most common cancer types...funny how that worked out! I sincerely do not believe that these two cases alone represent a signal against 0 in the placebo arm. This is textbook small sample statistical noise, ESPECIALLY for a drug with no mutagenic risk AND no immunosuppression (literally, HOW would this drug even be causing cancer then???).

However, clearly the market will want more info here on these two cases.

Hopefully the market will wake up to the points above (that $ABVX and I mistakenly thought were obvious) highlighting that the colonic dysplasia and NMSC cases can be almost completely written off. After that, hopefully $ABVX can give us more info on these two "legit" cancer cases (breast and prostate).

Yes, they should've been ready to do so on the call. they messed up, but let's see what the details show. Some are saying we will see updates sooner than the October conference like they initially guided for on the call (at which point they clearly did not expect the market to be freaking out at all).

After that, we also need to see the data from the 50mg "escape/placebo" arm that was not part of the primary efficacy analysis. That's is own topic of conversation, but that could significantly rewrite the narrative (now that $ABVX is aware a narrative needs to be rewritten after it got away from them).

I think the market thinks they are hiding these "escape/placebo" arm 50mg patients' data. I believe they were just totally caught off guard by the market's reaction to the "cancer signal" here and didn't think they'd need to have that dataset ready to prove there's no cancer risk (they thought the initial dataset spoke for itself...I agree, but so far the market clearly doesn't).

There should be several hundred patients worth of extra 50mg patients in that group. Ideally they can move up the release of that dataset to help qualm the market's fears and try to prove they aren't trying to hide anything there. Depending on the sample size there, we should very likely expect a few "cases" there too, but if the rate comes in lower than the original 50mg data we got, this narrative could snap back rapidly. Let's hope!

There are going to be case studies written about this initial $ABVX reaction, and (if we can get it) the subsequent rapid snap back ( 🤞🏻 ).

My HEAVILY BIASED opinion is that if the market comes to its senses and realizes this thing is not getting a black box warning we are going to >$150 in no time.

In reality if the “malignancy overhang” can be completely dispelled, there’s no reason we couldn’t see it go back to the brief initial market reaction of ~$180. Personally I’m already convinced that the malignancy stuff is statistical noise, but let’s see what the company can show the market about these cases and the extra data to convince people. This could’ve been upfront if they were just ready to explain what they already had, but oh well.

Once this black box warning stuff is put to bed, I can’t emphasize enough that the efficacy results here were at a level I literally didn’t even model for. Those endoscopic remission rates in particular are at levels I didn’t even think were possible for a single drug to produce.

With a clean label and a hit in crohn’s (which is now much more likely given the *extreme* efficacy in UC), this is an $8-$10B/year peak sales drug...pick your multiple on that…🤷🏻♂️

Again, I’m heavily biased and there’s no such thing as a guarantee, but this all seems very clear to me already. Unfortunately it’s not my opinion that matters! Let’s see what Mr. Market has in store.

$SYRE market cap at $79 now is roughly equal to $ABVX market cap at $96 now.

This is the most absurd valuation juxtaposition I have ever seen, full stop.

Doesn’t get more insane than this.

$ABVX thoughts:

The Phase 3 maintenance data showed strong efficacy, with results comparable to best-in-class JAK inhibitors.

The market's sell-off has been driven by cancer-related safety concerns. These events were concentrated in the 50 mg arm (n=6), with one case each in the 25 mg arm (n=1) and placebo arm (n=1). Reported malignancies included one prostate cancer, one breast cancer, one case of colonic dysplasia, and four non-melanoma skin cancers (NMSCs).

As others have pointed out, the solid tumors are likely incidental rather than drug-related. The latency is too short, the tumor types are not those typically associated with immunomodulatory therapies, background incidence rates appear plausible, and the dataset includes up to 7 years of exposure alongside a clean DSMB review. That leaves the dose-dependent NMSC imbalance as the only potentially meaningful safety signal.

It's also worth highlighting the 25 mg arm. Despite years of accumulated exposure, there has been no emergence of the major safety signals that ultimately drove boxed warnings across the JAK class. While the dataset is not large enough to conclusively rule out future risk, the evidence at 25 mg remains remarkably clean. If regulators ultimately view the 50 mg findings as dose-related, there is a plausible path where 25 mg becomes the preferred commercial dose, preserving much of the drug's value proposition.

Importantly, NMSCs alone are unlikely to result in a boxed warning. That would be consistent with the broader JAK class, where NMSCs were explicitly excluded from boxed-warning language.

The issue, however, is not necessarily the magnitude of the risk but the change in perception. The drug has gone from having "no safety footprint" to having "some safety footprint." Once that happens, investors no longer need to prove harm; the company needs to prove its absence.

That question cannot be answered by re-analyzing existing data. It likely remains an overhang until the label decision in 2027 and more definitive long term data.

From a valuation perspective, this matters more than the absolute risk itself. The bull case depended on a pristine safety profile justifying a premium to upadacitinib. "Almost clean" does not command the same premium as "clean."

$CNTX data on June TCE targeting claudin 6 ( with high specificity vs other Claudins ) in ovarian ca. Co reported a PR at cohort 3 ( low effective dose ) and low CRS due to gentle use of steroids.

CAR T cell targeting claudin 6 by $BNTX reported high RR .. but toxicity and durability ?

$CNTX referenced possibility of beating 30% RR in heavily pretreated OC including ADC from $ABBV

Data in June. Very interesting set up with CEO benchmarking 30% RR which is much better than 5-10% with standard chemotherapy

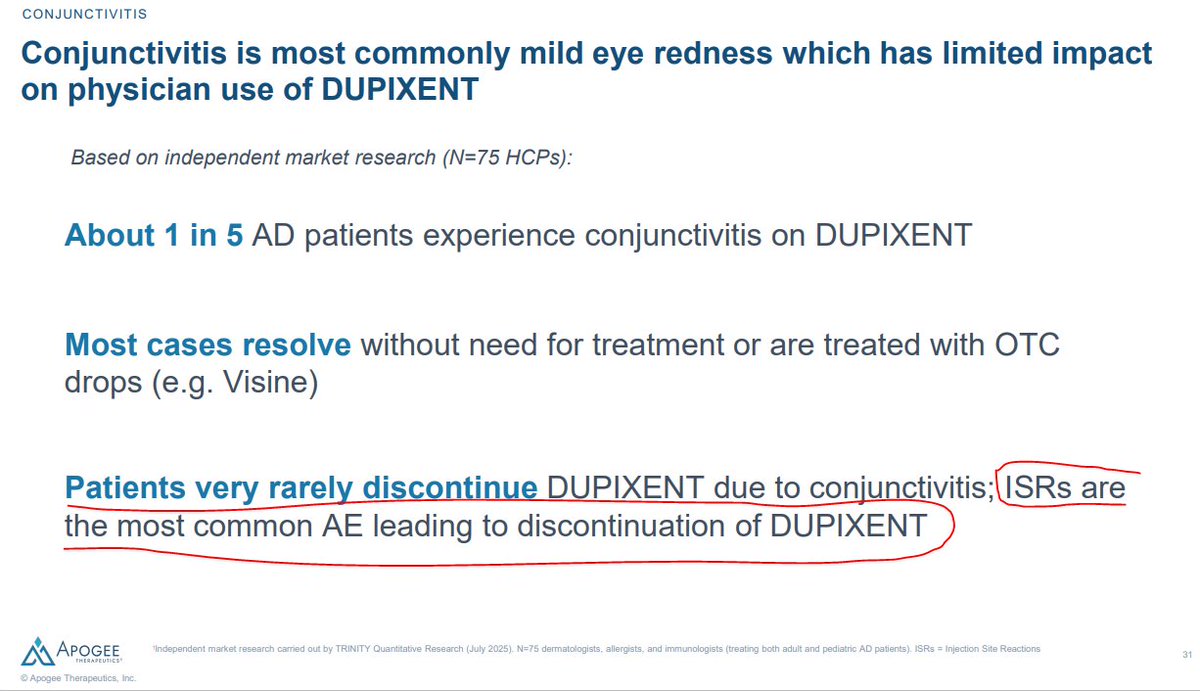

I've got to complain about $APGE again. You're welcome to take my opinion with a grain of salt since I've disclosed that I am short, but IMO they are spewing absolutely *blatant* bullshit about ISRs (add them to the LLY legal team!).

I heard them in 2 recent calls saying that "the most common reason for discontinuing Dupixent is ISRs". Huh? What?! ISRs are the most common cause of stopping Dupi???

That is absolutely INSANE to me, because I have treated hundreds of patient with Dupixent and LITERALLY NOT EVER (NOT ONCE) HAVE I HAD TO DISCONTINUE A PATIENT'S DUPIXENT BECAUSE OF ISRs. In fact, I've never even had to go as far as giving them advice on how to mitigate ISRs, such as treating the injection site with a cold compress. Literally: Nothing. Ever. In hundreds of patients.

I *have* discontinued patients due to conjunctivitis. If we are talking AEs, the most common causes for discontinuation in *my* experience are

1) Conjunctivitis

2) Facial erythema (some derms believe this to be psoriasis caused by the drug)

***gap***

3) Joint pain (rare)

Again, I can't even rank ISRs on that list at all because *LITERALLY* this has never ever happened with any of my patients.

So, that is *my* clinical experience, which goes directly in the face of what $APGE is claiming. I say that I've literally never even seen it happen, yet $APGE says that ISRs are the literal top cause of dupixent discontinuations...Sure, I'm biased, but so are they.

They want to convince you that conjunctivitis is not a big deal because they've seen higher rates of that side effect than dupixent/ebglyss so far. Instead, they want to create a strawman side effect that they can point at and say...

"Hey, we caused more conjunctivitis so far, but it's actually ISRs that are the problem!"

So, if we are both biased, what can we do to resolve the discrepancy? Look at the actual clinical data! In clinical trials, were patients more likely to discontinue from conjunctivitis, or from ISRs? Let's look at the actual data!

P3 5-year extension trials (n~2700):

-> 14 patients discontinued due to conjunctivitis

-> Zero (?) patients discontinuing due to ISRs? ISR is not even listed as a reason for discontinuation in the publication.

Real world dataset from the Netherlands (n~1300):

-> 38 patients discontinued due to conjunctivitis...the most common cause of AE-related discontinuation in the study *by far*

-> 2nd place for discontinuations was muscle/joint pain

-> Yet again...***ZERO*** cases of discontinuation due to ISR. None. ZERO!

So, $APGE is going out on these roadshows and repeatedly telling everyone that ISRs are literally the single most common cause of dupixent discontinuation, yet with only a few minutes of research you can get to a sample size of ~4,000 patients treated with dupixent for multiple years showing DOZENS of cases of discontinuation due to ISRs and LITERALLY NOT ONE SINGLE CASE of discontinuation from ISRs...Again, this matches my clinical experience precisely, where conjunctivitis is the most common cause and I've *never* seen ISRs drive discontinuation once.

So WTF is $APGE talking about? How are they making this bold claim that goes directly in the face of the entire body of medical evidence?

Well, if you read the tiny footnote in this slide from their corporate deck, this bold claim is apparently coming from "independent market research" via some sort of physician survey...

...ok. Well, hopefully I don't have to convince people that you can design a survey such that it gives you almost any result you want. IDK how this internal dataset looks, how it was collected, etc etc, so I can't tell you exactly what's wrong with it. But, I can tell you that across my own clinical experience and literally THOUSANDS of patients in the literature, I cannot find a SINGLE case of discontinuation due to ISR, whereas there are DOZENS of confirmed cases due to conjunctivitis.

Yet here is $APGE going around and repeatedly spreading the same ISR FUD that the $LLY legal team has tried to invent in order to screw over $NKTR. You can take my biased word that this is absolute bullshit if you want, but fortunately thousands of patients worth of objective clinical data happen to be on my side here.

I think $APGE is absolutely *Full*. *Of*. *Shit*. with this ISR vs conjunctivitis nonsense.

Fortunately for me, the publicly available data unequivocally agree.

Let's just look at their Ph2 data at face values

$IMRX Ate + Chemo 1L PDAC PFS: 9.6m

$RVMD 6236 MONO 2L PDAC PFS: 8.1m

How much impacts on PFS in 1L vs 2L? Let's learn from Tagrisso...

2L PFS (AURA3, Tagrisso mono): 10.1m

1L PFS (FLAURA, Tagrisso mono): 18.9m

But hey what about adding chemo to 1L?

1L PFS (FLAURA2, Tagrisso + chemo): 25.5m

So PFS increased 152% from Tagrisso mono 2L to Tagrisso + chemo 1L

And people are welcome to dream $IMRX has a path to 1L PDAC...

$qure $clpt Matt spoke today, my connection got completely jacked up, going to work on trying to get a transcript. This is the rough notes on what my sources believed they heard this morning so take it for what you will. Could have missed some stuff or taken stuff as different context, it’s hard with no transcript or replay.

Leadership mostly focused on 1 year results with pre-bla and type A meeting. Like I said, Prasad really focused on the 1 year data.

The type a meeting focused on pre-specification, which he answered by saying in 2018 it would have been next to impossible to prespecify, but at 1 and 2 year data they worked with the fda before locking it in to account for that. and the other thing at the type a meeting was the 1 year data and kaputsa said any HD KOL would be able to explain that in early symptomatic patients it would be impossible to have 1 year data show anything due to the slow progression of the disease.

He was asked if he expected the 4 year data to follow what they had seen, with each year getting better then previous. and he said that is what they are hoping to expect.

thought big thing is he said potential for gap between treated and untreated patients to become even more meaningful

The big takeaway was that Kaputsa seemed to be calling out the fda: said the MHRA understood the significant unmet medical need of HD, they had regulatory flexibility, and it was very clear to the MHRA that the 3 year evidence was worth a review.

He also said there were 10s of thousands of patients in the UK/Gulf/common wealth and Latin america that would be in TAM.

It sounds like they arent going to engage with the fda on an rct because they have other opportunities.

It sounds like strategy was going to be put pressure on FDA to see if there really is change at leaderhsip level.

This is exactly what I would do if I was Uniqure, say look, we will be releasing the 4 year data soon, happy to lock in the data beforehand , we spoke with many KOL’s, neurologists and the HD community, we do not believe it is ethically right to do a rct phase 3. We believe and many other regulators believe the data we have shown has shown an early signal that amt 130 is working, we are happy to work with the US and would love to come with a mutually beneficial agreement that makes sense for both parties. I’m very happy that it seems Uniqure might not be putting up with the phase 3 rct idea.

FDA has lost 50% of its oncology review staff since 2/13/25 h/t ex FDA Commish Gottlieb's comments on Face the Nation on 5/10. Pancreatic cancer patients shouldn't be punished because of HHS's staffing & hiring problems. #pancsm $RVMD $XBI $IBB $BBC

This is a huge statement from the JPM 26 conference from the new acting director of CBER. It bodes well for @uniQure_NV $QURE AMT130. How can they move the goalposts and expect any company to spend the money required to bring treatments to market as they did with AMT130?

I don't know if @US_FDA will approve AMT-130 but in my book the brand equity of $QURE and $CLPT and a few others has gone up huge. If approves, everyone eligible will go on it. Minimal marketing spent

After months of exhaustion, heartbreak, and feeling like our community was screaming into the void, with today’s news, I’m allowing myself to feel something I haven’t felt in a while: HOPE.

There is still a tremendous amount of work ahead. Huntington’s disease doesn’t pause while leadership changes. Families are still losing time. Patients are still waiting.

And yes, we may be starting over in some ways. Re-educating. Rebuilding awareness. Explaining, again, what Huntington’s disease is, what urgency looks like, and why patients deserve scientifically sound pathways forward. However, I would rather start there - with education, transparency, and honest dialogue - than continue trying to navigate leadership that felt dismissive, politically driven, or unwilling to truly hear the rare disease community.

That said, I also want to acknowledge the people who did listen. Leaders in the Huntington’s disease community like Katie Jackson, Jenna Heilman and others who have worked tirelessly to speak truth, push for accountability, and refuse to let patients be ignored. And the congressional leaders and advocates behind the scenes who were willing to ask hard questions, investigate concerns, and use their voices when so many stayed silent.

Advocacy is exhausting. This fight has taken a real toll on me, but we are still here, and if this creates an opening for better leadership, better science, and a renewed commitment to patients, then we keep going.

Huntington’s disease doesn’t wait.

And neither can we.

#HuntingtonsDisease #RareDisease #StandUpSpeakUp4HD #TimeMatters #DelayStealsTime

@RepAuchincloss@SenRonJohnson@SenRickScott@SenateAging@SenGillibrand@realDonaldTrump@POTUS@WhiteHouse@BeckyQuick@adamfeuerstein@Christina4HD@rachelreising96@JRenz0418@houmanhemmati@hthurgood@Help4HDI@HDYOFeed