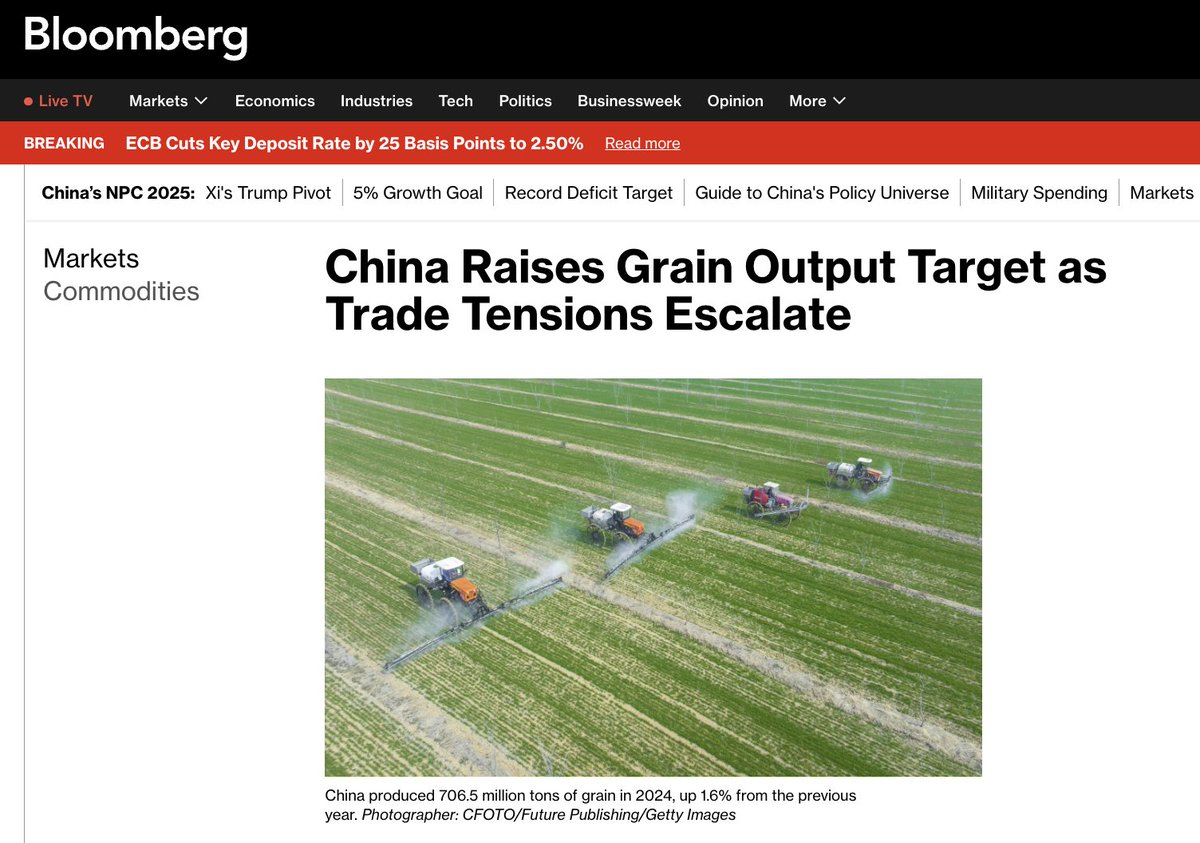

🇨🇳 Forget #tradewars—this is a way bigger long-term bearish story for ags.

1️⃣ #China is doubling down on domestic crops production.

2️⃣ Population is flat/declining.

3️⃣ Aging population → lower per capita meat consumption → less feed demand.

Beijing wants 50 MMT more grain by 2030. That’s a structural shift, not just a trade war reaction.

#oatt #grains #china #agriculture #soybeans #corn

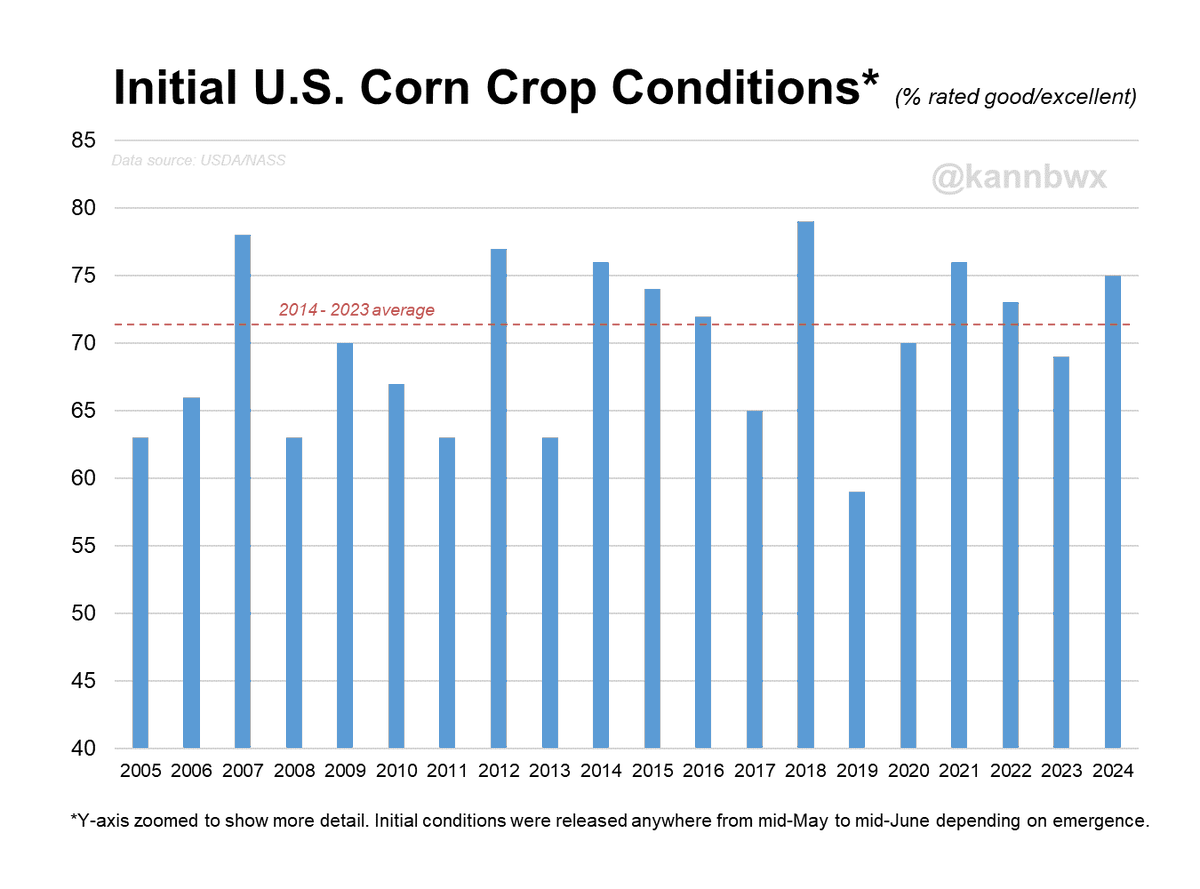

🌽U.S. #corn starting at 75% good-to-excellent is the 6th best start of the last 20 years and the best since 2021.

People always point out 2012's great start - yes, things can certainly turn. In the nearer term, a quarter of the crop has yet to emerge. Let's see how that looks.

🚘 HOW ‘BOUT THAT RIDE IN? 🚘

“If you look around your circle & you’re not inspired… you’re not in a circle, you’re in a cage!” - RIP Nippsy

Facts.

Sit with winners. You’ll notice that the conversation is different… now set up shop there!

⚡️ Positive Vibes Only!

#👊

@ScottFranklinJr@kannbwx Good question. I’m honestly not sure. Have not heard of anything major other than I think they got hit with some pretty heavy rains over the last couple weeks. Unless flooding occurred, I can’t imagine rain hurting the crop this time of year.

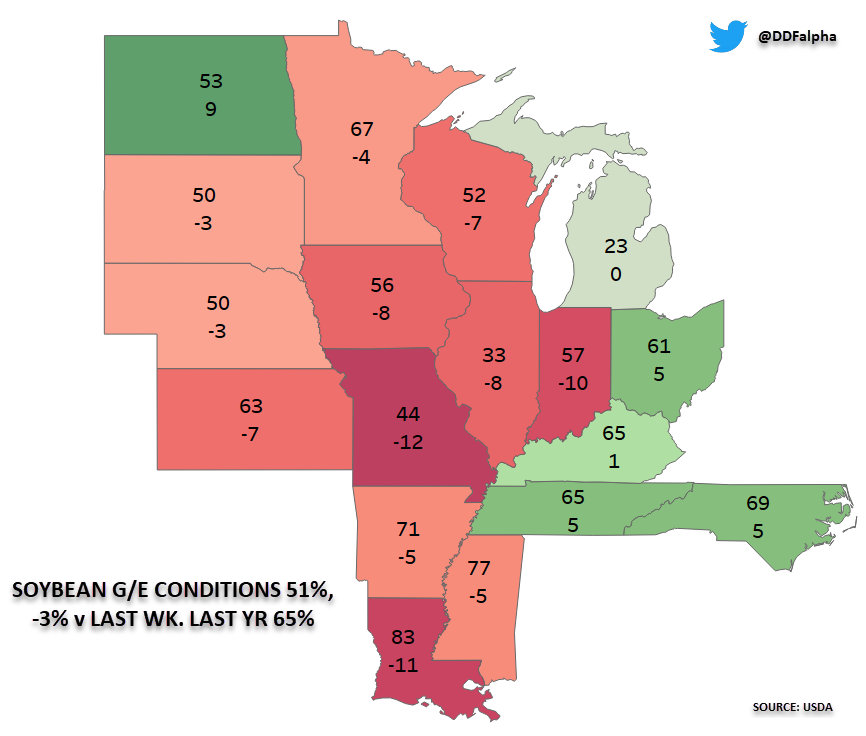

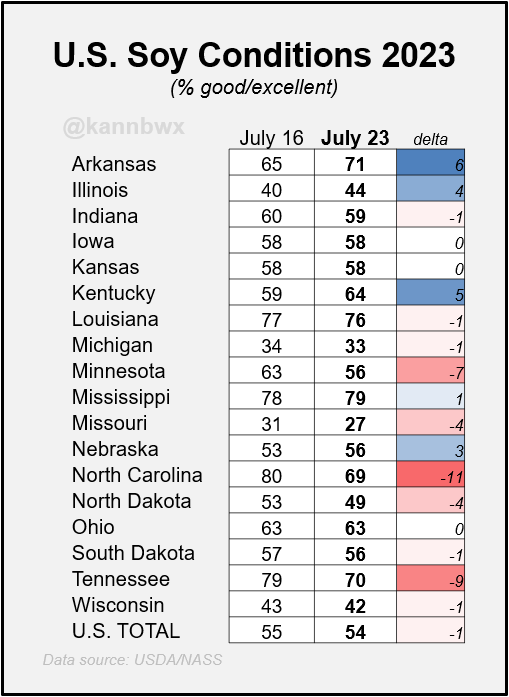

#Soybeans declined 1 pt to 54% good/excellent despite expectations for steady. Many of the same offsetting state changes as in corn. Illinois beans are 44% good/exc, off from the low of 25% four weeks ago.

🇺🇸U.S. #corn conditions are unchanged at 57% good/excellent, against the expectation for +1pt. Strong improvements in Illinois, Kansas, Kentucky were offset by declines in many other states including Minnesota, Ohio, Missouri & the Dakotas.

So many wrong takes on the Black Sea #graindeal. Here’s what you need to know if you trade #wheat (and #corn) as of today:

* Odesa shipments are over. The chance was high that the Kremlin would stop the grain deal and show everyone that they should stay away from Odesa. We gave a heads-up about such a scenario last week after the first light attack on Odesa and Putin’s angry interview (the market/media missed that – everyone was watching the NATO forum).

* Despite what the media/politicians are telling you, Odesa shipments are not a game-changer now. Ukraine can ship 40+ mmt of grain via other routes, and that more or less matches their 23/24 export potential.

* Other export routes are the Danube and via land to the EU. The almost-forgotten Danube has been expanding rapidly since the start of the war. In recent weeks for the first time, they loaded two handysize ships (17K)

* Is the Danube safe? We don’t know. Russia threatened all vessels in the Black Sea going to Ukrainian terminals, so that could potentially include ships going to the river. Some vessel owners are cautious and prefer not to send ships there currently, but overall the navigation is still active, and local traders are actively buying at CPT Reni/Izmail/Kilia.

* Potential attack on the Danube terminals could be a game-changer. Watch this carefully. Is it likely to happen? The chance is not negligible but low, the Kremlin clearly doesn’t want to mess with NATO, and Romania is very close. What is concerning is that Russian propagandists, who were happy about the Odesa attacks, are now starting to talk about the Danube…

* Potential escalation could come from the Ukrainian side. We do doubt that they would openly attack vessels going to Russian ports, but some attempts to disrupt the shipments are possible (ie more attacks on the Crimean bridge impacting Russian shipments from Azov…or Novorossiysk). If something big happens here, we could see a rally similar to Feb-Mar 2022….Russia has almost 50mmt+ of wheat to ship.

* A potential path to de-escalation? It also exists….we will be watching Erdogan. We do believe that Moscow and Ankara discussed the end of the grain deal some time ago – Ankara clearly wasn’t surprised. We also know that Erdogan still likes the deal and has a lot of leverage over Moscow.

* Trade / hedge accordingly.

* Support by reshare & follow and check what we offer at https://t.co/8gTnMNZzdZ.

#oatt

usda has not lowered yield in july since new methodology in 2013. the only times they lowered yields in may or june were in 2013, 2019, and 2022 all due to planting delays (which has clear impact on yields). yet ill bet trade guess is looking for material change next week.....

G/E Conditions v Last Wk for #Corn & #Soybeans: Declines continue across the corn belt as dryness continues to hamper progress. Notable declines seen across key growing region of IL with corn DOWN another 10% with soybeans DOWN another 8%. Not looking for much improvement this wk

Quick thoughts regarding today’s crop progress numbers. I was, like many, surprised just how quickly IA & IL conditions have fallen v LW. If this were 3-4 wks from now during pollination the impacts would have dramatic implications on US production. However, forecast remains dry, conditions will decline this wk, materialized rains are what market is wanting now. The market has priced in a substantial amount of risk premium in this market especially for #soybeans, but even for #corn this has been impressive. Regardless how competitive we are right now, this is about money flow & momentum, one MUST respect that or get ran over in near term. Adjust and adjust quickly in this environment but stay disciplined & keep emotions in check. Option vol at these levels WILL NOT perform like you think higher or lower (if long only) without substantial moves. There is a lot of risk in options right now if structured wrongly. #TuesdayThoughts

🇺🇸I was curious how often dry Junes in the U.S. Midwest precede dry Julys - mixed results. I was also interested how #corn yield turns out in those years. Here's what I found:

⚫️Yield within a couple % of trend or above

🔴Yield more than a couple % below trend

Prevent plant discussions are on the rise with the slow planting pace in the northwest U.S. #Corn Belt. Good to know what that means and how to interpret. Farmers can collect insurance when crops cannot be planted by a certain date. 2019 & 2020 were big PP years.

Back from a week on the beach with the kids and time for an oil macro update. Where do things stand now and where are we headed? First, our compass...global oil inventories continue to plummet and the "gap to normal levels" continues to widen = bullish.