I let my son (7) pack his bag for our flight this afternoon. Went to check it before we left and found eight baseballs, an entire pouch filled with legos, and three pocket knives stuffed in various pockets.

@Mr_Neutral_Man@rhunterh And what happens in the days between IPO and when index funds must buy them. Seems like an obvious front-running opportunity. And that’s sadly where the world is at today. Completely divorced from intrinsic value.

Doing the same. I took notes and had a few calls with MMYT back in ‘23 but it ran up before I could ever gain conviction. Have been following and waiting for another chance to DD them in earnest.

They’re super attractive because while Europe is fragmented, India is even more so. And while $BKNG has something like 55-60% of trips originating in-app, $MMYT had 80%+ three years ago. It’s remarkable.

@finphysnerd Just asked my wife about this one. She, and just about all of her friends prefer Nuuly, owned by $URBN, on the idea that they get to make their own selections. The stylists at $SFIX never get it right apparently.

Many of these Hikari holdings go nowhere until Hikari acquires a controlling share. They then sit down with management and give them three options. 1) pay out all of your cash via special dividend 2) opt for MBO 3) become our subsidiary. In either case Hikari benefits but not in every case do you, as a shareholder of that business benefit. When the third option is selected (as is done commonly) Hikari acquires complete control of the business and that cash accrues to their balance sheet.

Ipso facto, you're better off owning Hikari if this is your sole criteria.

I keep tracking the stuff Hikari is buying - hundreds of stocks in their portfolio - and it's basically always good and obvious. Plus, they essentially act as an activist for you... with no management or performance fee.

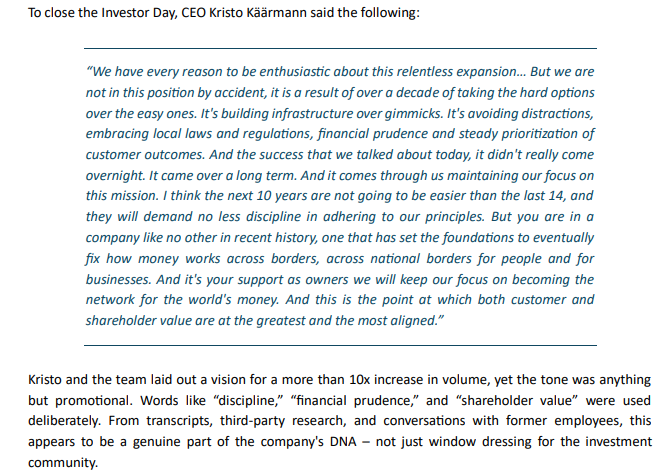

I think that's the big point although I see a few more takeaways as well.

BBY won through the 80s and 90s on a superior value proposition (Lower prices, greater assortment, more convenience, etc) but lost in subsequent decades because Amazon outcompeted them on those very same vectors. Even with Circuit City going BK in '08 and BBY officially 'winning' the big box electronics war, they never picked up incremental market share because Amazon gobbled it all up.

Also, while BBY net income hasn't changed much (inflation unadjusted) on a $ basis from '05 to '25, share count is down 58%. This has accounted for essentially all of the EPS growth over the last 20 years. Without the share buyback in place, there would be effectively a 0% return over 20 years.

Despite being in a -45% 5-year drawdown and currently trading at <10x P/E, $BBY has still compounded at 12.5% p/yr for 40 years! There is a lesson somewhere in here about the LT compounding of businesses with a unique value proposition (which was then the big box retail format)