$HIMS keeps executing. The more value it offers, the more it becomes a must have subscription similar to $AMZN. Obviously it has a long way to go, but Dudum knows where to invest to make this a must have subscription- including services previously only available for the elite. All for a tiny $5.5b market cap. See you at $100.

$HIMS is now a $5B company, trading at a P/S ratio of 2.5x.

The company expects to surpass $6.5B in revenue by 2030 and has a strong track record of beating expectations by wide margins.

Hims has also exponentially increased the pace of new vertical launches: Labs, HRT treatments, and now longevity and peptides — areas expected to become mainstream by 2026.

This is what an asymmetric bet looks like.

$AMD was HATED at $84, now $247

$BABA was HATED at $80, now $174

$RKLB was HATED at $14, now $85

$BIDU was HATED at $75, now $156

Currently HATED:

$JD $29

$UNH $291

$NIO $4

$HIMS $29

$OSCR $14

“Be fearful when others are greedy, and greedy when others are fearful.”

Bookmark this. Revisit in 1 year.

NFA

$HIMS IS APPROACHING HUGE SUPPORT AND LOOKS PRIMMED FOR A BIG RECOVERY IN 2026 🚨📈

Ive broken down a very simple monthly time frame here for $HIMS.

Hims has really struggled since it peaked out in early October at $65 a share with a fake breakout.

Retail has abandoned the stock, whilst institutions continue to accumulate.

There is bullish divergence which hints to accumulation, the recent selling has also been done on very weak volume that suggests that there is not that much conviction in this recent sell off in $HIMS.

The stock is now approaching a very large support area and providing $HIMS stays above $23 a share, the next target remains $137 for wave 3 🎯

Follow my full analysis and every move for $HIMS by joining my group for FREE - https://t.co/jUU7An5iAK

Gavin Newsom, with ZERO fucks to give, telling the European press in Davos how European leaders need to deal with America's bullying psychotic shitstain. 🙌💪👏✊👇

$HIMS remains a very compelling company.

But the market rushed to price perfection into a still very young company operating in a highly regulated and competitive environment.

In my view, that optimism got ahead of reality, and that mispricing is now being corrected.

This process takes time. But if you have the discipline to wait for the alignment, this year could be the defining one for your portfolio.

The recent stock drop reflects a market focused on short-term "shortage" dynamics of weight-loss drugs. But for those looking at the 2030 horizon, where Hims & Hers has projected $6.5 billion in revenue, the company is no longer just a "telehealth" app. It is becoming a personalized health infrastructure.

The current volatility isn't the end of the story, it's the beginning of the transformation.

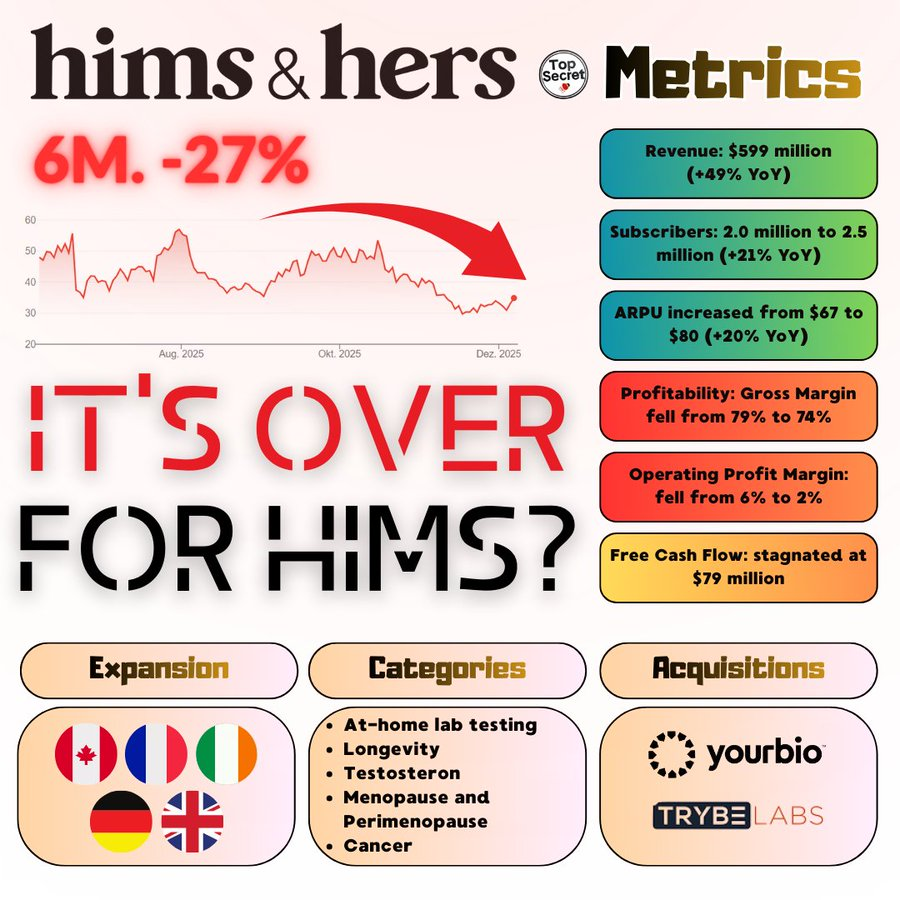

Conclusion: On the surface, the top-line growth is undeniable: Revenue is up 49% YoY to $599M, subscribers have swelled to 2.5 million, and ARPU has climbed to $80. The demand is clearly there. However, the stock is down 27% over the last 6 months for a reason: Profitability is taking a hit. Gross margins dropped to 74% and operating margins shrank to a razor-thin 2%. Why? Because the company is aggressively reinvesting. They aren't just selling pills anymore; they are pivoting into complex "hard health" categories like cancer, longevity, and at-home lab testing via acquisitions like YourBio and Trybe Labs. Add to that a massive geographic expansion across Europe (UK, Germany, France, etc.), and Canada. The market is punishing the margin compression BUT the data suggests they are simply building a much bigger, more medical infrastructure for the future.

What are your toughts?

In 1999, $AMZN was in the phase of a fundamental transformation. $HIMS is facing a remarkably similar narrative. While the stock has seen massive volatility recently, largely due to fears around the GLP-1 (weight loss drug) shortage ending and competitive moves from Amazon Pharmacy, Ro and $NVO, the company is undergoing a fundamental transformation. It is moving from a "lifestyle pill" company into a vertically integrated, data-driven healthcare giant.

Just as Amazon moved from books to music, then to electronics, and eventually to the cloud (AWS), Hims & Hers is aggressively expanding its verticals. The goal is to own the entire "patient journey" through a subscription-based model that prioritizes longevity and preventative care. 👇

$HIMS is down 55% from its February highs.

Meanwhile:

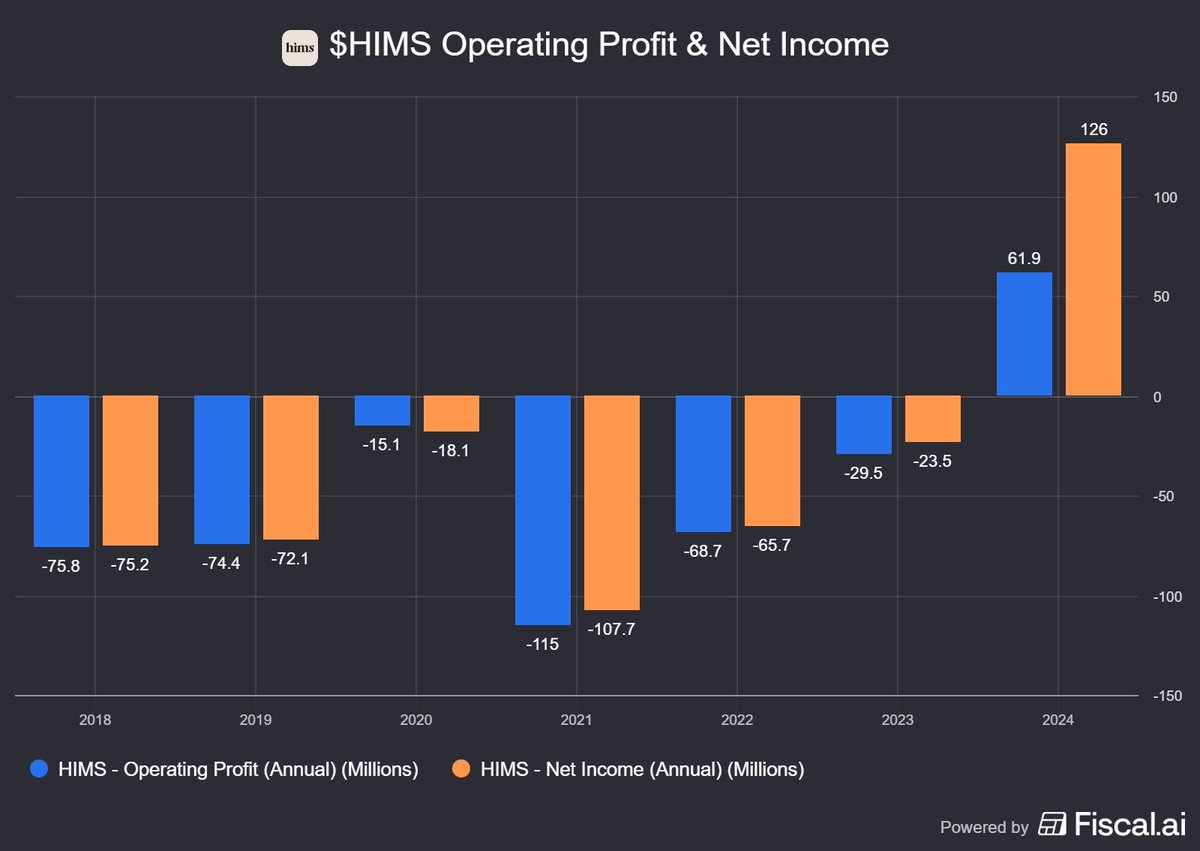

• In Q3 it posted $600M in revenue, an all-time record

• It launched the HRT vertical and Labs

• It began international expansion in Europe with ZAVA and in Canada with Livewell

Sentiment around $HIMS is at the lows, but only because sentiment follows price. Fundamentals are extremely strong.

We saw the exact same thing with $AMD in 2025. When the stock was at $80, people called it “Advanced Money Destroyer” even though the business kept growing. A few months later, the stock was up +250% and sentiment completely flipped.

The same will happen with $HIMS. Buying in the low $30s could be life-changing.

If your $HIMS avg is in the teens, you're likely sitting on a 10X in the next 5 years

20's? You're likely sitting on a 5X in the next 5 years

Buying in the 30's can still 4X in that time

The trick is to expand your horizons further than the next 3 months

My 2030 price target: $140

@TheProfInvestor Hims is a healthcare disruptor. Volatility expected. Long term it's quality will show. Meta, Google amd, all of them took a 50% drawdown in the past few years. It's path of the course 🤷🏻♂️