All studies have limitations, but some studies are like power plants that don't produce power, with the engineers explaining, "Like other power plants, ours has limitations . . ."

Not about that ideology per se because but about argumentativeness, stupid concern for nuance and vocab, etc. She agreed its become like a sociology journal reviewer. Also complained that even GPT gives her more guff than before, but still her preferred model

The year is 1945, you have an R&R pending for more than a year because the editor is prisoner of the Nazis. The decision letter comes: reject, the topic is not general interest anymore.

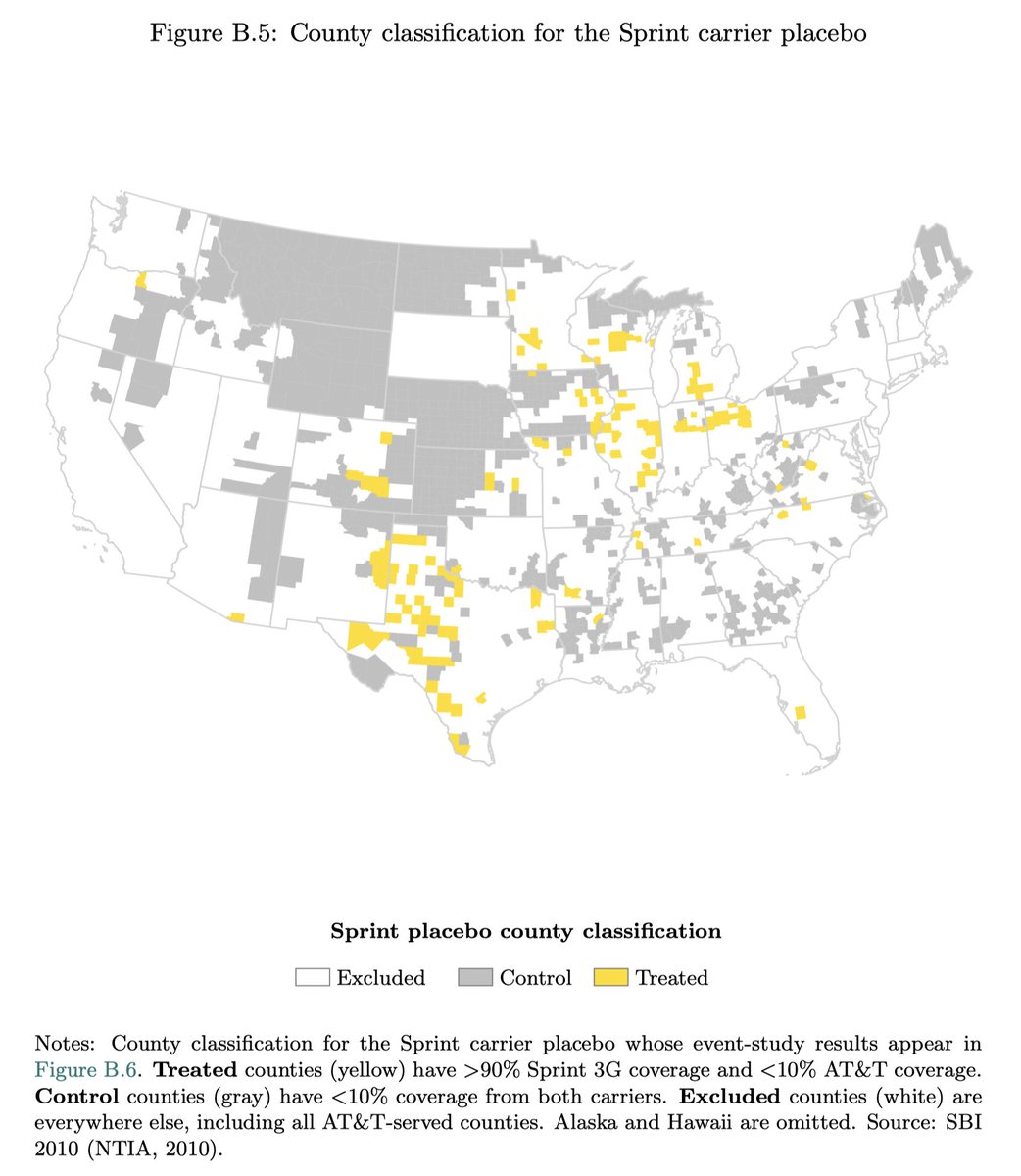

I fear that the new cellphones-cause-low-fertility NBER working paper has found a potentially genuine divergence between the fertility rate in rural and urban counties in the US, then labelled it "iPhone."

The problem is that AT&T coverage was heavily urban, resulting in an imbalance between the control and treated group.

The matched Poisson regression is supposed to address that by overweighting the small number of notionally urban counties that did not have iPhone coverage. But I believe that by "urban," they mean counties in which just 33% or more of the population were in towns of 2,500+ people. It would therefore included a lot of places that are, in fact, rural.

To me, it seems like there's a failure of identification.

Hence, the SDiD result could reflect iPhones or a differential effect of the Panic of 2007 on rural and urban areas. We don't know.

The other-carrier placebos are also uninformative because they are structurally incapable of reproducing the urban-rural confound, given how they are mapped.

The paper is here: https://t.co/IXXlro3fUn.

"Something … predicted but hasn’t happened yet was a revolt of the youth against the baby boomers’ requests. It didn’t happen simply because young voters … believe that protecting the claims of their parents and grand parents will protect their own. As if there was a secret infinite source of funding."

The theory that Google selling tons of their own stock is to suck capital out of the AI-related market so there's less left for the three large IPOs this year.

https://t.co/zzA86Js0NG

Here's something many people don't know about me -

Before I publicly dissected the long list of problems in the 1619 Project, I contacted the New York Times through their official channels to request a series of corrections to unambiguous factual errors in its content. The editor - Jake Silverstein - brushed me off and refused any correction - a pattern he also exhibited toward other critics from across the spectrum.

Before I publicly broke the story about Kevin Kruse's plagiarism in Reason, I contacted Princeton's academic integrity officer and alerted him to the problems I had found, giving them a chance to respond and address it internally. They ignored my email and later claimed to have lost my email after I went public.

Before I published my findings on Quinn Slobodian's habitual manipulation of source materials to alter its plain meaning through misquotation, I submitted an article to Contemporary European History (the journal where the worst examples appeared), highlighting the problems with the passages and asking for a correction through their official process. They desk-rejected it, brushed me off, and falsely claimed that Slobodian's piece had been thoroughly vetted in peer review. In fact, one of their own referees had flagged the same problems over a year earlier and recommended rejection of the article.

Before I published an expose on Nancy MacLean & Sandy Darity's similar manipulation of W.H. Hutt quotations in their article for History of Economics Review, I (along with 2 coauthors) submitted a response comment to this journal asking for a correction through its official processes. The editor gave us a complete runaround where he imposed an arbitrary length limit requiring us to cut the content, sent the trimmed version to a referee, then rejected the piece because the referee said we didn't sufficiently address the very same things we were forced by the editor to cut. When I then asked the editor to issue a simple corrigendum to the most egregious misquotation (one that transformed Hutt's explicit attack on the racism of white Afrikaners into a defense of Apartheid), he refused and tried to pass it off as a difference of "interpretation."

Before I published an expose of a leading covid masking model in the Wall Street Journal, I sent a comment to the medical journal that published it alerting them to a math error that changed their entire set of results. The journal acknowledged the error was real but refused to publish my piece on the grounds that the "next release" of the model would be updated to reflect it - even as politicians up to and including Joe Biden were trumpeting the erroneous results all over the news.

Apple now trades at 10.36x sales. The highest valuation in its history.

Remember Scott McNealy's warning about 10x sales? Apple just crossed it.

But here's the part that should stop you.

McNealy was describing a hypergrowth company. Apple is not. Apple's annual revenue:

– 2022: $394 billion

– 2023: $383 billion (its first decline since 2019)

– 2024: $391 billion

– 2025: roughly $415 billion

Four years. Less than 2% growth a year. Essentially flat.

Yet over those same four years, the stock soared and the price-to-sales multiple nearly doubled.

Read that again.

The revenue barely moved. The valuation exploded. Every dollar of the gain came not from Apple selling more, but from investors agreeing to pay more for the same sales.

That is multiple expansion. It feels like growth. It is not growth. It is sentiment.

Apple's long-term average price-to-sales ratio is 3.6x. It now sits at 10.4x. Nearly three times its own historical norm.

For the math to work from here, one of two things has to happen. Either Apple suddenly reaccelerates revenue growth after years of stagnation. Or the multiple holds at the highest level in company history. Forever.

History says multiples revert. They always do. The only question is whether earnings grow fast enough to cushion the fall.

This is the quiet danger hiding in the "safest" stock in the world.

Nobody worries about Apple. The ultimate quality compounder. A Buffett favorite. A permanent holding.

All of that can be true.

And you can still lose money for a decade if you buy a flat-growth business at three times its normal price.

Great company. Demanding price.

They have never been the same thing.

@ed_hagen@danwilliamsphil Daily is wrong about this, and his empirical papers on the matter are shoddy. Excellent predictor within US is percent Black.

@mattyglesias It's one thing to predict a bubble bursting, it's another to get the timing right. If you cannot do both, you may lose a lot of money despite being directionally right.

@GarettJones But wouldn't you want the information in terms of density (e.g., per square mile)? (Also, probably heavily driven by people's tendency to complain, so hard to interpret.)

@yzilber@Uber Not sure about that. IIRC, drivers are in trouble if the average drops below 4.7 or so, so a single one-star rating can do a lot of work. If multiple people do it, even better. But I'm not against an "infectious" button.