$KEEL just announced a $350M convertible notes offering. Here’s the full picture.

Up to $408M with the greenshoe. Matures 2032. Conversion triggers at ~$11.40 - roughly double today’s price.

The bull case:

Capped calls offset dilution up to the conversion price. Proceeds go to long-lead equipment deposits and letters of credit - you don’t order gear speculatively. This is construction acceleration capital. Same playbook as October 2025. Raise cheap debt when momentum is strong, not when you’re desperate.

Total war chest after this raise: ~$883M.

The honest bear case:

This stock went from $0.70 to $6.60 in 12 months. If three leases sign and the stock re-rates toward peers - $11.40 (estimate on todays price) is reachable. At that point dilution kicks in. The greenshoe adds another $58M of exposure on top.

Today’s sell-off is also partly mechanical - convertible arb traders short the stock and buy the notes simultaneously. That’s standard, not fundamental.

My issue:

On the Q1 earnings call Ben was asked directly about equity issuance. His answer:

“We have no reason or no need to issue equity right now. We’ve got everything that we need.”

Convertible notes aren’t equity today - but they become equity if the stock doubles. That’s a meaningful caveat that wasn’t communicated clearly on the call. I don’t love the sway from that statement three weeks later. Retail investors deserved more transparency on this possibility.

Management has earned trust through execution. But trust cuts both ways - and this one warrants watching closely.

The bottom line:

Minimal dilution below $11.40. Real dilution above it. Proceeds accelerating construction is genuinely bullish. The timing of the communication is not.

$KEEL 🏗️⚡

DYOR. NFA.

Why $KEEL Is Now My Largest AI Infrastructure Bet (see article)

The bull-case spread is still wide. If KEEL secures a meaningful backstop, guarantee, or strong credit structure, the upside could exceed the ranges shown in my bracket tables. I cover that possibility in the report, but kept the main assumptions more measured.

Dilution is difficult to model. They will likely need significant capex, but that does not automatically mean ugly dilution. If leases are signed first, KEEL may be able to raise capital into strength, use project-level/non-recourse financing, or bring in strategic partners. Overall, I think the estimates are reasonable.

LEAPS still look relatively cheap to me. A potential 10x move in the equity could translate into a much larger return through options leverage, potentially closer to a 30x outcome, 3000% within 2 years. Obviously, that leverage cuts both ways.

This is a high-conviction, high-risk position, not financial advice. Read the report, stress test the assumptions, and do your own research.

And if you find the report useful, please consider following my account and sharing it. I’m very close to 1,000 followers, and my brain is refusing to let that number sit unfinished 😅

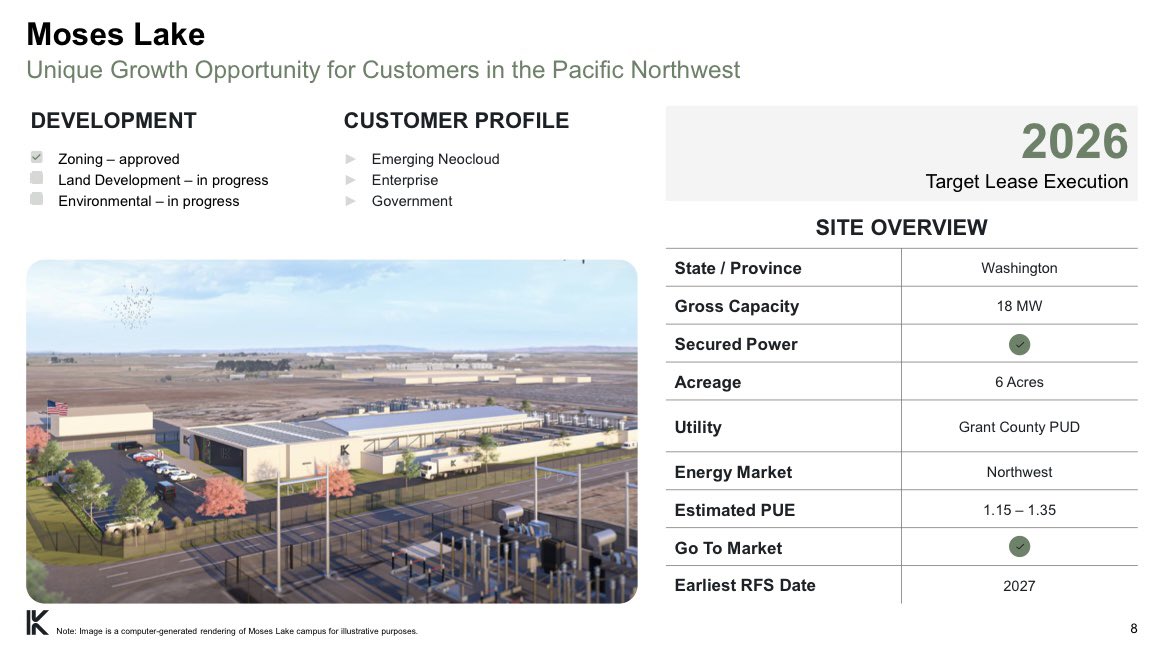

$KEEL Infrastructure targets three sites for lease executions in 2026 ⚡️

Sharon

• First Keel site to be ready in Pennsylvania

• 110 MW

Panther Creek:

• Flagship hyperscale campus

• 350 MW

Moses Lake:

• Pacific Northwest

• 18 MW

BREAKING $KEEL EARNINGS🚨⁉️

$KEEL just completed its transformation into a pure-play North American HPC/AI infrastructure play.

Q1 2026 highlights:

• Rebranded to Keel Infrastructure

• Fully exited Latin America exposure

• Focus now entirely on high-demand AI data center markets

• Panther Creek, Sharon & Moses Lake all advancing with zoning/site development underway

• $533M liquidity runway through lease execution + Moses Lake construction start

Financials:

• Revenue: $37M, down 23% YoY

• Operating loss: $98M vs. $35M last year

• Net loss from continuing operations: $128M vs. $38M YoY

• Adjusted EBITDA: -$17M vs. +$7M YoY

The losses were largely driven by restructuring costs, $BTC fair value losses, debt extinguishment costs, and investments into development.

The bigger picture:

$KEEL is positioning itself early for the AI infrastructure buildout in supply-constrained North American markets.

This is no longer just a Bitcoin mining story. It’s becoming an AI infrastructure development platform.

Currently down -9% premarket.

$BE - from Brookfield ($BAM) call ongoing:

"We are already in conversations to expand our $5 Billion partnership [with Bloom]. Not by percentages, but by multiples."

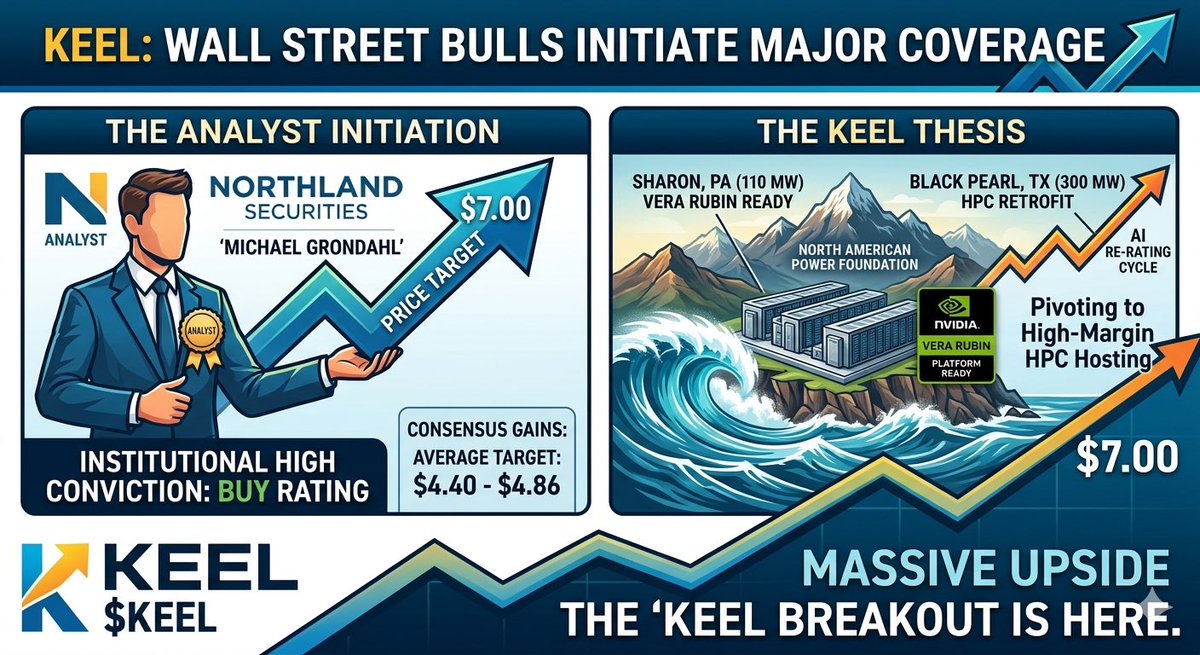

Northland Securities issues Major Price Target for $KEEL! ⚓️🎯

The institutional momentum for Keel Infrastructure ($KEEL) just hit another level. Northland Securities has officially initiated coverage, and the outlook is overwhelmingly bullish.

The Breakdown:

• Rating: BUY

• Price Target: $7.00

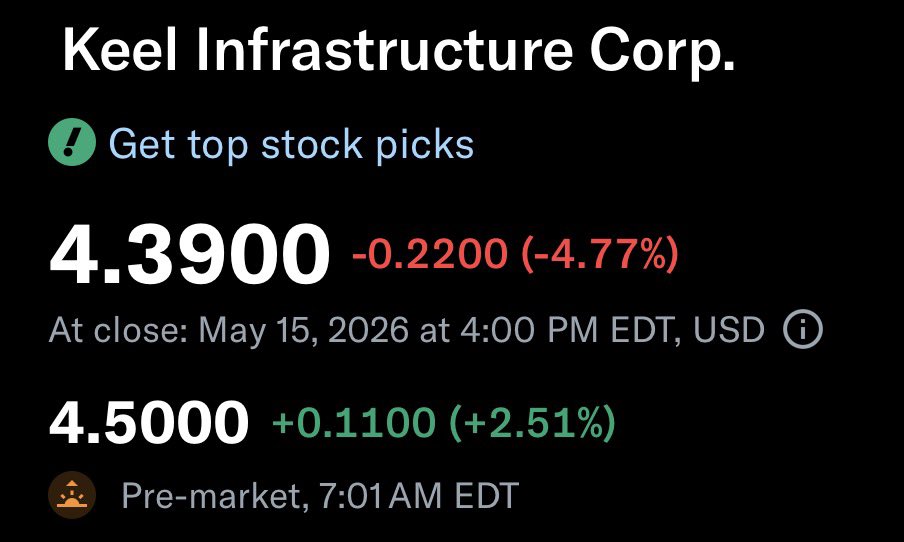

• Upside: This new target represents a massive potential gain from current trading levels (~$2.89).

• The Thesis: Analyst Michael Grondahl is signaling high conviction in KEEL’s strategic pivot toward high-margin North American AI infrastructure.

Why it matters:

Northland joins a growing chorus of Wall Street firms re-rating $KEEL as a premier infrastructure play.

With a $7.00 target now on the board, the gap between "miner" valuation and "AI data center" valuation is closing fast.

The "Keel" is set for a major breakout. 🏗️🌊🚀

$IREN $CIFR $WULF $ORCL $NUAI $SLNH $HIVE.V $NBIS

🚨 @keelinfra_ scores a key regulatory win in Sharon, Pennsylvania 🚨

⚡ Zoning board of Sharon, PA approves planned 110 MW data center expansion on 18 acres of former Westinghouse Electric industrial land

⚡ Currently operating 30 MW at the Clark Street site — two 80 MW substations targeted for completion by end of 2026

⚡ Once complete, $KEEL plans to deploy @nvidia Vera Rubin hardware at the facility — next-gen AI GPU infrastructure from day one

⚡ Brownfield redevelopment — former industrial eyesore converted into state-of-the-art digital infrastructure — strong community narrative

⚡ Next steps: Mercer County Regional Planning Commission → Sharon Planning Commission → City Council final approval

⚡ If approved, construction and hiring begin before end of 2026

Filter by company to see every CORZ deal with CoreWeave, or every WULF deal with FluidStack.

Filter by client to see who Microsoft, AWS, and CoreWeave are actually signing with.

Sort by size, revenue, duration, or revenue per MW.

BIRD gets $50M in predatory financing to chase GPU business with zero infra or expertise. Stock +582%.

HIVE announces $75M, 0% convert to buy NVDA B200s & scale HPC toward $140M+ ARR, following record $93M rev qtr & actual Tier III data centers. Stock down.

JPM High Yield Credit Research initiates $CIFR $WULF $APLD bonds with very bullish note.

"The hardest thing to explain is the glaringly evident which everybody has decided not to see. The world is dramatically short on compute."

"From a market structure standpoint, we are highly confident in the market’s ability and appetite to absorb high yield (and eventually Leveraged Loan) data center risk. Virtually every deal that has been brought to market has been upsized and/or tightened, and essentially all have traded well."

Team likes the $CIFR (Barber Lake & Black Pearl) most, then $APLD Polaris Forge bonds.

Great conversation between Morgan Stanley analysts Jim Faucette and Stephen Byrd on an in-house podcast. Some notes:

"When we look at the Bitcoin/AI miners, if anything the fundamentals have gotten better. The value paid by the AI community and hyperscalers is very high compared to the value implied in these stocks. Many of the Bitcoin stocks trade at EV/watt of $2-7/watt. The high-water mark was in December where a deal generated $18/watt. We think the new normal is $13-15/watt. That's a lot more than $2! If you're a stock trading at $2 and deals are happening at $13, that's an obvious reason to be excited...

...The power demand growth for AI in our model is around 30% per annum. The compute demand growth in our projected numbers is around 200%. There are now many data points suggesting that these compute numbers is way too low (Google internal projections are 3x MS numbers; token usage up 2200% y/y despite no 10x improvement in efficiency).

...Cipher is down YTD, which really doesn't make sense in that context.

So why are some of these stocks down? They are high vol stocks and Bitcoin stocks are often the first on the list to sell. The more nuanced questions we are getting from clients are really interesting: Is there enough funding for this capex? If Middle Eastern funding dries up, what happens to the available cash? Can these small Bitcoin companies really build these multi-billion-dollar datacenters. I respect that question, it's absolutely possible some of the companies will run into execution challenges. The good Bitcoin teams are bringing in FLR/JEC to manage these projects, that's a positive. And we are getting questions about private market funding...

...The Bitcoin players have the advantage of irrevocable grid access agreements. That's like the keys to the kingdom! We need all of the Bitcoin power for AI. All of it. We'll still be short. We need Bloom to dramatically increase their capacity... This power problem is going to get worse, not better."

(Interesting call-out on improvements at $MARA, sounds like an upgrade from their current UNDERWEIGHT rating maybe in the works.)

![matthew_sigel's tweet photo. $BE - from Brookfield ($BAM) call ongoing:

"We are already in conversations to expand our $5 Billion partnership [with Bloom]. Not by percentages, but by multiples." https://t.co/E0vaaTHPIs](https://pbs.twimg.com/media/HHzl9ZyWgAUQbEb.jpg)