Between 2017-18 & 2025 more Indians sought pvt hospitalisation, perhaps a result of more Indians having health insurance thanks to govt sponsored programmes, & yet they paid more than inflation indexed costs even after deducting insurance reimbursements.

@naalmot story

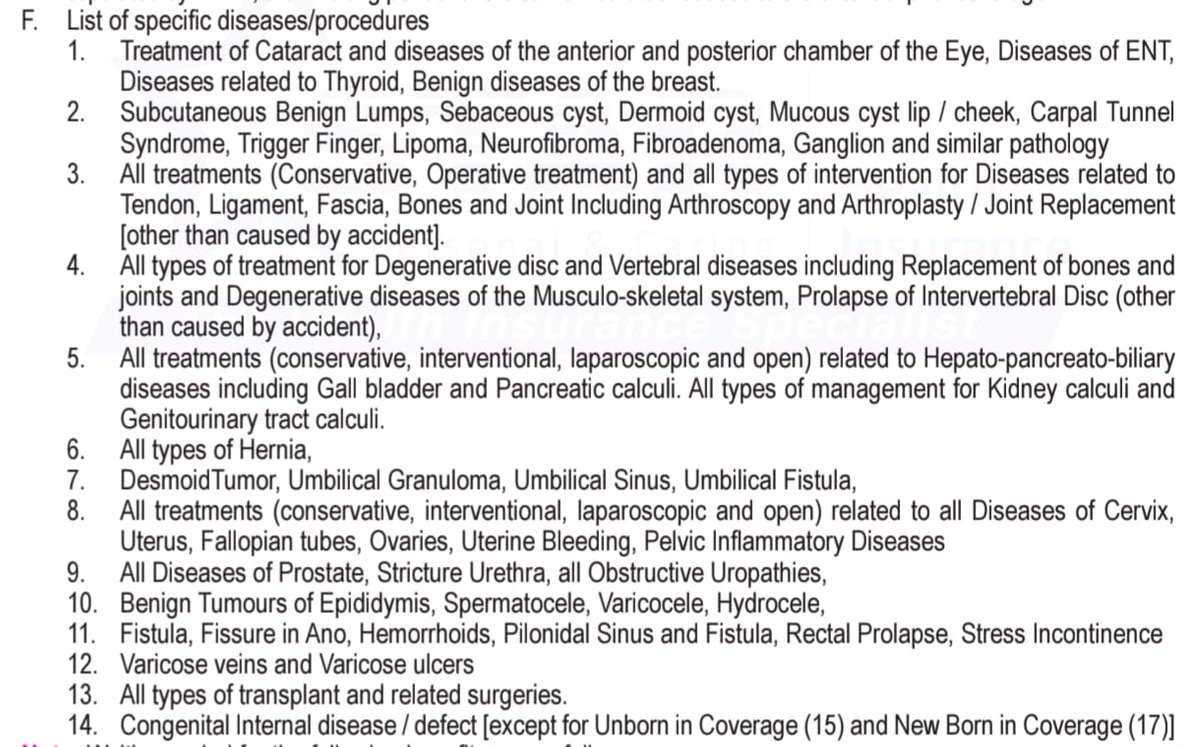

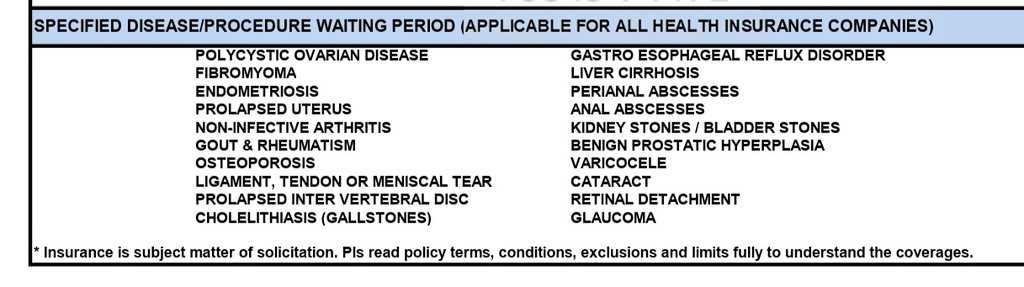

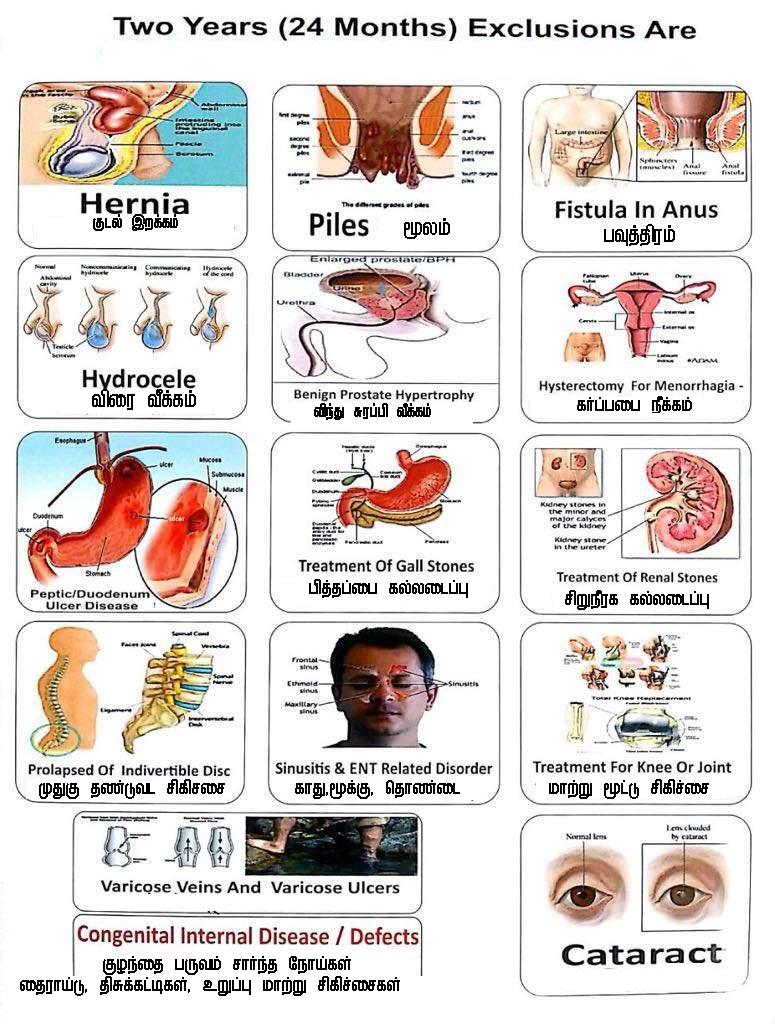

Specified Diseases Waiting Period of 2 Years applicable in all health insurance policies of every insurance company.

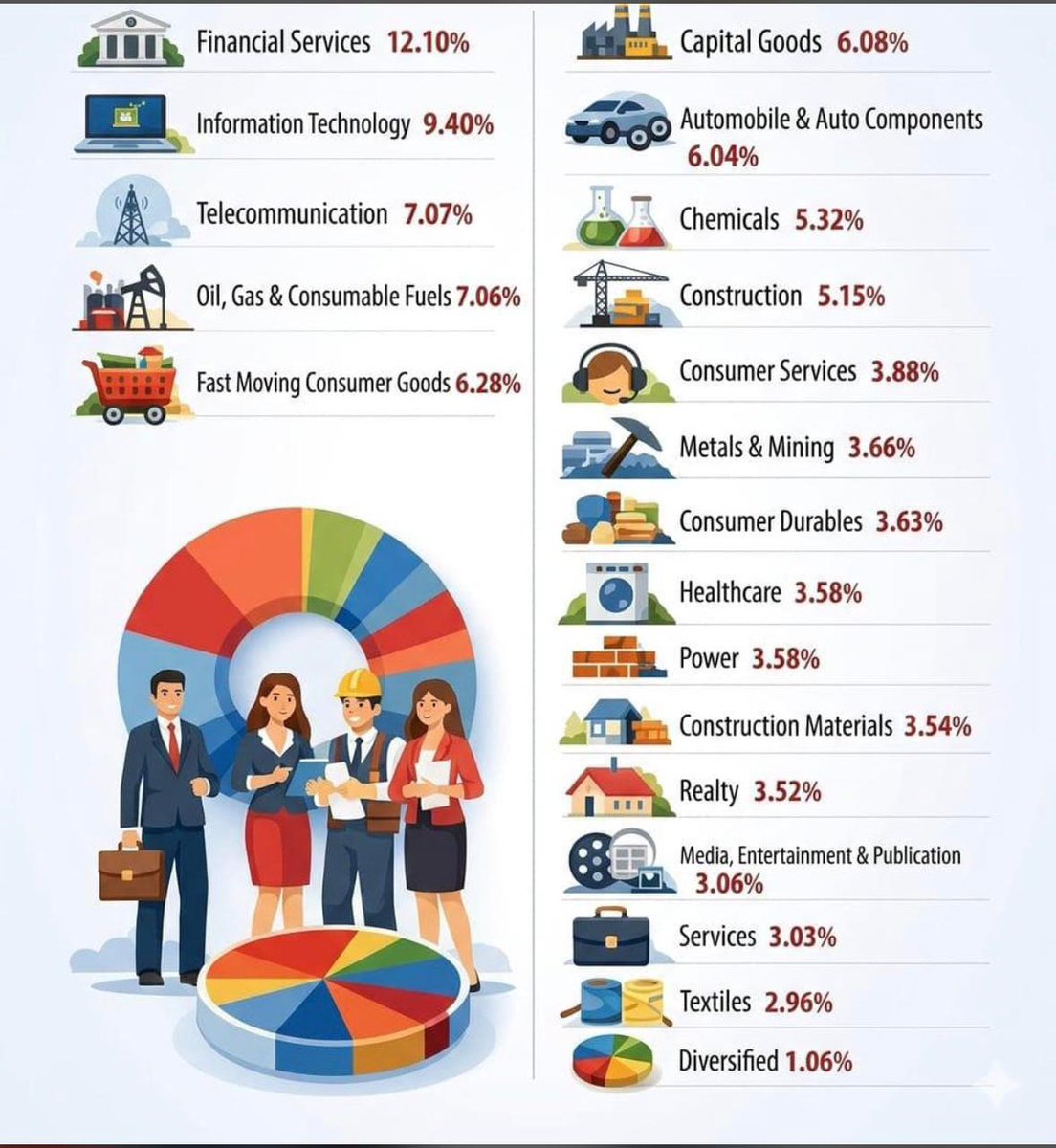

Pls find 3 presentations but same contents. #HealthInsurance#Claim#MedicalInsurance

From the OPD: The Most Dangerous Health Misconception I See Every Day

The most frustrating part of my OPD practice is not the complex neurological cases; it is watching patients lose a battle they think they are winning.

Every day, I see patients with obesity, Type 2 Diabetes, or hypertension who tell me:

"I walk every morning, Doctor."

"I do all the household work."

"I have stopped adding sugar to my tea."

They feel they have done their part. But their blood work and body composition tell a different story.

Here is the evidence-based reality of why "walking and quitting sugar" is often not enough.

1. The Exercise Trap: Walking vs. Muscle

🔸Walking is a great baseline, and household chores are better than sedentary behavior. However, neither is a substitute for Strength Training.

🔸After age 30, you lose 3-8% of muscle mass per decade (Sarcopenia). Muscle is your body's primary "glucose sink."

🔸Walking burns a few calories while you do it. Strength training builds the "engine" that burns glucose even while you sleep.

🔸If you are not lifting weights or doing resistance training at least twice a week, your insulin resistance will likely persist, regardless of your step count.

2. The Diet Trap: "No Sugar" is the Bare Minimum

🔸Patients often think that by cutting out "sweets," they have fixed their diet. Meanwhile, their plates are still 80% carbohydrates (rice, rotis, poha) and nearly 0% protein.

🔸Refined carbohydrates (even without added sugar) spike insulin similarly to sugar. Furthermore, a protein-deficient diet leads to muscle loss and increased hunger.

🔸Most Indian diets are high-carb, low-protein disasters. Cutting sugar but eating 4 rotis or a mountain of rice is just trading one glucose spike for another.

✅Focus on Protein Leverage. Prioritize 1.2g to 1.5g of protein per kg of body weight. When you hit your protein goals, your craving for carbs naturally drops.

Neurologist’s Perspective

Why does a brain doctor care about your squats and your protein intake?

Because Muscle is an endocrine organ. When you strength train, your muscles release Myokines, which:

🔸Improve cognitive function.

🔸Reduce systemic inflammation.

🔸Protect against neurodegenerative diseases like Alzheimer’s.

✅ The "Metabolic Reset" Protocol

If you want to see real change in your HbA1c and BP, stop settling for the "Walking/No Sugar" myth.

1. Stop "Just Walking": Add two days of resistance training (bodyweight, bands, or weights).

2. Flip the Plate: Start your meal with protein (paneer, eggs, sprouts, lean meat). Eat your carbs last, and in smaller portions.

3. Recognize Household Work as "Activity," not "Exercise": Exercise requires progressive overload. Sweeping the floor doesn't challenge your muscles the way a squat does.

Dr Sudhir Kumar

@hyderabaddoctor

Disclaimer: Mutual fund investments are subject to market risks. Pls read the offer documents carefully. Past performance may not indicate future returns.

This is an insurance product linked with share markets. This can't be your primary investment or insurance. Pls DM to know more about term insurance suitability. #TermInsurance#Financialplanning

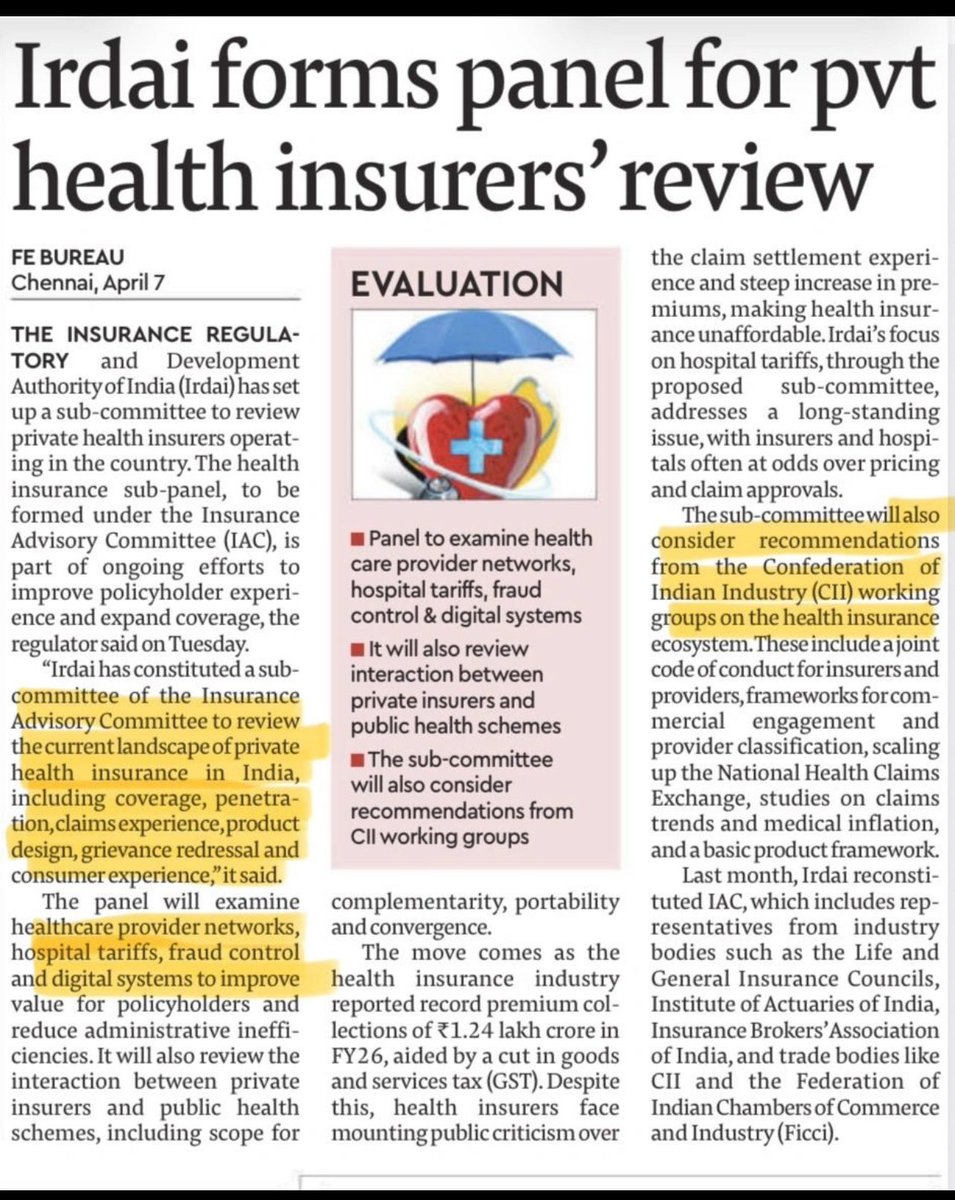

🚨 Big Move in Health Insurance 🚨

Insurance Regulatory and Development Authority of India (IRDAI) has formed a panel to review private health insurers.

What will be reviewed? 👇 • Claim experience & customer complaints • Rising premiums 📈 • Product design & transparency • Hospital tariffs & pricing issues • Fraud control & digital systems

👉 Focus is clear: Improve policyholder experience & make health insurance more fair and affordable.

Also, recommendations from Confederation of Indian Industry (CII) will be considered — which means industry-level changes may come soon.

�� My Take: This is a much-needed step. If executed properly, it can reduce claim disputes and bring better clarity between insurers & hospitals.

Now the real question is Will this lead to better claim settlement experience on ground? 🤔

#HealthInsurance #IRDAI #InsuranceNews #Policyholders #IndiaInsurance #Claims

Try it out.

1. Strong financial backing with a Solvency Ratio of 3.85(FY24-25).

2.Competetive Premium Rates offering the best value.

3. Smooth and Rational purchase journey. #Godigit#Digitlife#TermInsurance

Have a ₹50L term insurance from 2017.

Realising now it may not be enough.

Looking to increase cover to ₹1Cr.

Better to top up with a new policy or make changes to the existing one?

Sanjay ji, Union Bank is already a promoter of STAR UNION DAICHI Life Insurance where they've ~25% stake.

UBI do have ~9% stake in IndiaFirst Life inherited by merger of Andhra Bank.

So UBI was strategically moving towards STAR UNION DAICHI. #Banca#LifeInsurance

🚨 BIG UPDATE IN BANKING & INSURANCE 🚨

🏦Union Bank has officially discontinued its corporate agency tie-up with IndiaFirst Life Insurance (IFLIC) effective 1st April 2026.

📌 Strategic Shift in Bancassurance

Union Bank has officially exited its corporate agency partnership with IndiaFirst Life Insurance (IFLIC), effective 1st April 2026.

🔍 Key Highlights:

▪️ No fresh business will be sourced under IFLIC

▪️ Existing customers will continue to receive uninterrupted service & renewal support

▪️ Zero impact on customer experience and servicing

💡 Insight:

In today’s evolving financial ecosystem, institutions are continuously realigning partnerships to optimize value, efficiency, and long-term growth. This move reflects a broader strategic recalibration in the bancassurance space.

📊 What to watch next:

Will Union Bank onboard a new insurance partner or adopt a diversified distribution strategy?

Stay tuned—this shift could redefine future insurance distribution models.

👉Why did this happen (tie-up discontinued)?

Banks and insurance companies often change partnerships due to strategic reasons like:

https://t.co/OKSV4xd9mm Strategy Change

Union Bank may want a new insurance partner or multiple partners to increase revenue.

2.Better Commission / Profit Terms

Banks earn commission from selling insurance. They may switch if better terms are available.

3.Performance Issues

If sales targets or business growth were not as expected, the bank may exit the partnership.

4.Regulatory / Market Changes

The insurance sector is evolving, and banks are moving toward open architecture (working with multiple insurers).

#India #Insurance #Bancaassurance #Insuranceindustry #Bank #Unionbank #BankingSector #FinancialServices #FinanceNews

In order to be born, you needed:

2 parents

2² = 4 grandparents

2³ = 8 great-grandparents

2⁴ = 16 second great-grandparents

2⁵ = 32 third great-grandparents

2⁶ = 64 fourth great-grandparents

2⁷ = 128 fifth great-grandparents

2⁸ = 256 sixth great-grandparents

2⁹ = 512 seventh great-grandparents

2¹⁰ = 1024 eighth great grandparents

2¹¹ = 2048 ninth great-grandparents

For you to be born today from 12 previous generations, you needed a total of 2¹² = 4096 ancestors over the last 400 years.

Think for a moment:

How many struggles?

How many battles?

How many difficulties?

How much sadness?

How much happiness?

How many love stories?

How many expressions of hope for the future? – did your ancestors have to undergo for you to exist in this present moment...

#WATCH | Delhi: On study conducted on 5000 heart attack patients, Professor of Cardiology, GB Pant Hospital, Dr Mohit Gupta says, "... In India, a heart attack happens 10 years before the death of a person. It is more severe. Often, if you and I go to a doctor and ask what the risk of a heart attack is, to calculate that, we have risk scores... All the risk scores that we have are either using Western risk scores, which are made up of 6 or 7 risk scores. We believed that if we apply these risk scores to the Indian population, that is, what are the chances of a heart attack in 10 years, if we apply these risk scores to the Indian population. These risk scores should not be validated for us because when these scores were made, they were made on the Western population... When we used Western risk scores in Indian heart attack patients, we saw that 80% of the people were classified in low risk and moderate risk..." (2.4)

Your "Low Risk" heart score might be a dangerous lie.

🔴A shocking new study from GB Pant Hospital (Delhi) just dropped a truth bomb:

80% of Indians who suffered a heart attack were previously declared "Low Risk" by standard medical calculators.

▶���If you are relying on the ASCVD score to feel safe, you need to read this.

1. The "Western Bias" Trap

Most risk calculators (like ASCVD) were built using Western data. But Indian hearts behave differently. We develop heart disease 10 years earlier, often with "normal" LDL levels.

2. The South Asian Phenotype

Even if your BMI is "normal," you might be carrying "Thin-Fat" syndrome.

We have a unique cluster of risks:

🔸High Triglycerides + Low HDL

🔸High Visceral Fat (Internal organ fat)

🔸Severe Insulin Resistance (Prediabetes)

3. The Invisible Killers

The ASCVD score often ignores the big players for Indians:

✅ Lipoprotein(a): A genetic risk factor present in 1 in 4 Indians.

✅ ApoB: A better measure of "bad" particles than LDL.

✅ Psychosocial Stress: A massive, unmeasured driver in our cities.

4. What should you do instead?

Do not just look at a "Low Risk" printout and celebrate.

🔸If you are 40+, consider a CAC (Calcium Score). It sees actual plaque, not just probability.

🔸Check your HbA1c (once a year) and Lp(a) at least once in lifetime.

🔸Focus on Metabolic Health, not just "normal" numbers.

The Bottom Line:

A "Low Risk" score is not a shield; for many Indians, it is just a blindfold. We need India-specific risk models.

Prevention is only as good as the tools we use.

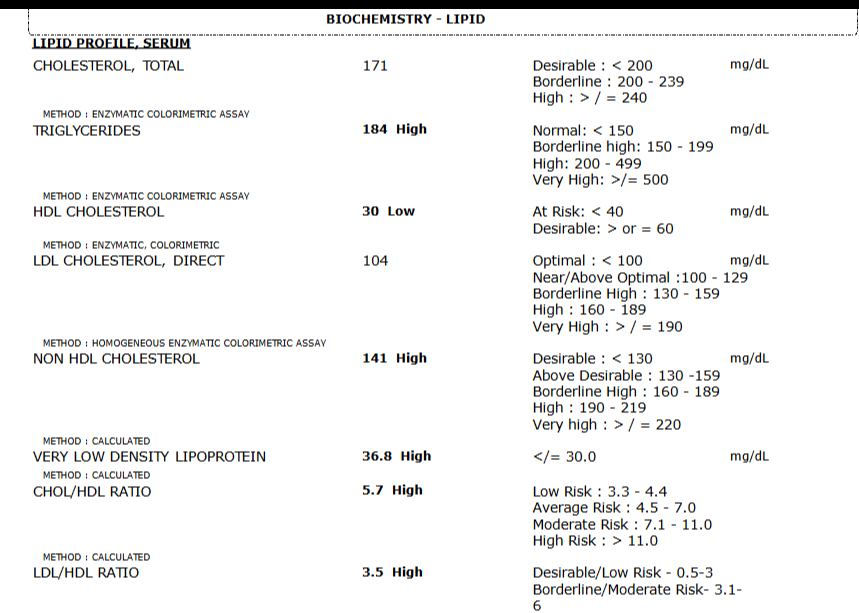

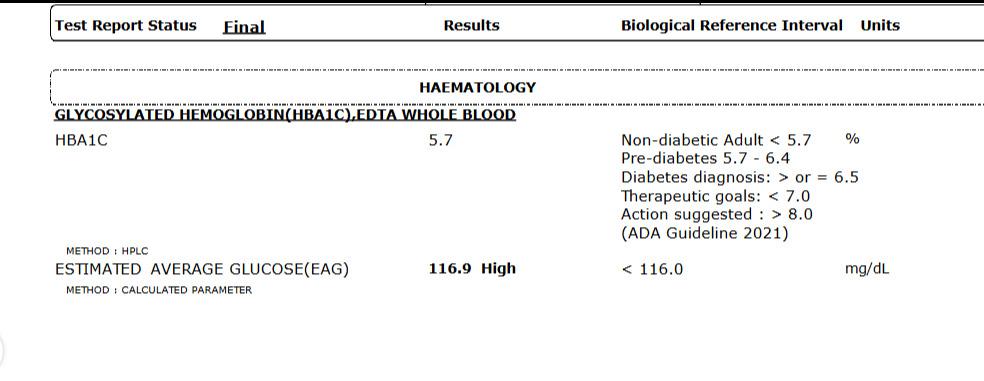

(Below is a representative sample of blood test reports of a young man in his early 30s)

Dr Sudhir Kumar @hyderabaddoctor

(Disclaimer: The information provided is general in nature. Please consult your doctor for individual medical advice.)

⚠️ Essential Thrompocytosis - ET carries a lifelong risk of blood clots and bleeding.

· Annual monitoring cost: ₹40,000–1.2 Lakhs.

· Cytoreductive therapy: ₹60,000–3.6 Lakhs/year.

· Health insurance planning is critical from diagnosis

#Bloodcancer#Thrombocytosis#Insurance

Parent care costs can blindside even financially savvy. Planning proactively, ideally in your 40s, is the key message.

This connects directly to the value of senior care insurance, super top-up health plans covering parents, and dedicated geriatric care budgets. #Elderscare

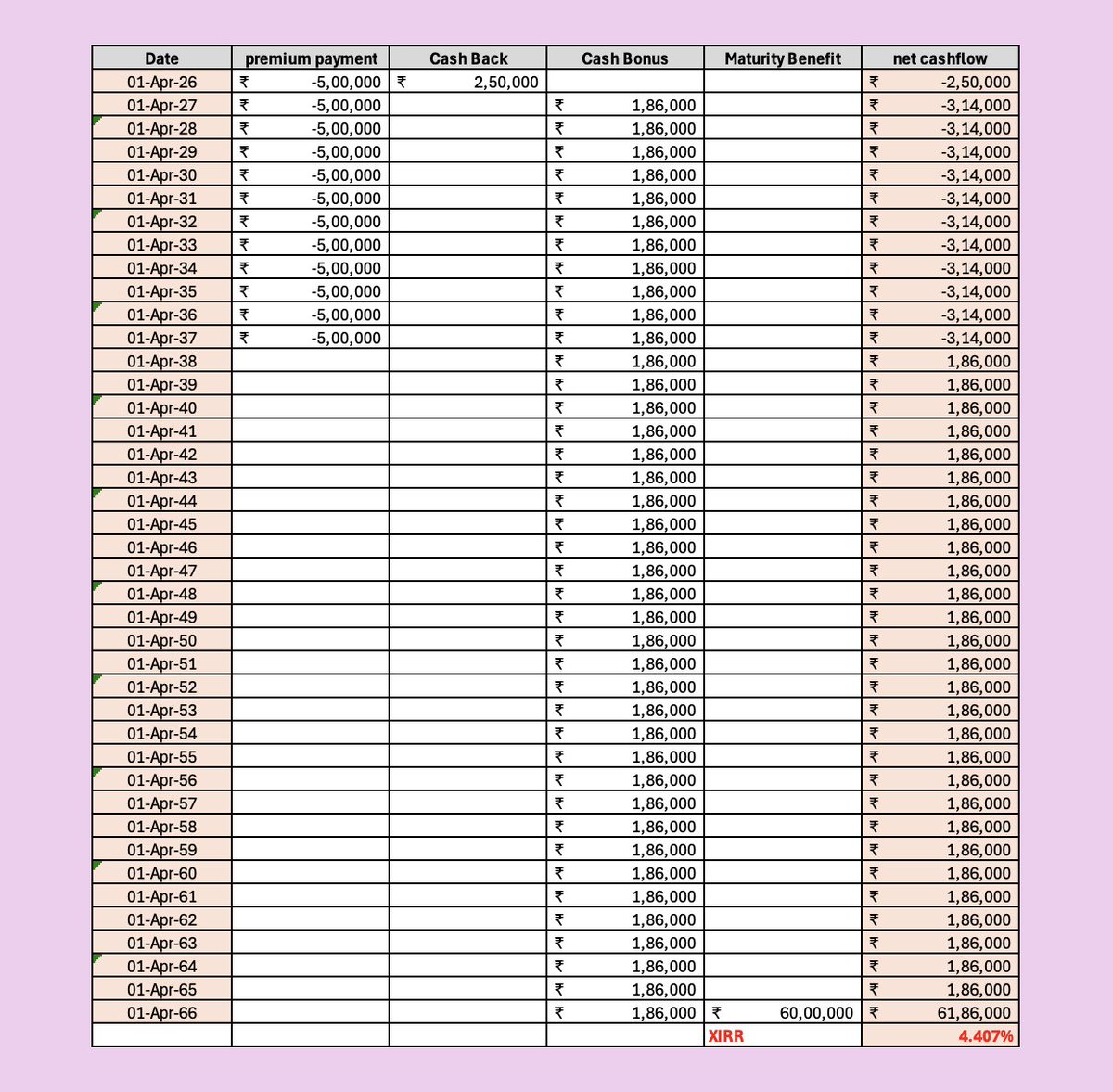

Real returns (XIRR) of Traditional Life Insurance Policy.

- This 4.407% is at the end of the 40th Year with no partial withdrawal/loans/timely payment of premium.

- It should be in a deep sea for the first 25-30 years.#XIRR#Moneyback

Term Life Insurance is GOAT.

just did this working for a prospect..

the cash back of 50% is a kind of pass back from Agent's pocket..

40 years of money getting locked in..

much better - invest in a Equity Savings, Balanced Advantage Fund, Multi Asset fund

insurance is never for investments.

HDFC Bank made ₹7,938 crores of commission in FY25 from sale of financial products* such as insurance.

20% of policies lapse within one year meaning these people lose all their investment.

Something is not adding up. Why so much debate over ₹20-30 crores of mis-sold AT1 Bonds to HNIs?