지금 대형 IB들의 반도체 관련 모든 전망은

빅테크가 CAPEX 지출 속도를 줄이지 않을 꺼라는

전제를 깔고 있다.

빅테크가 CAPEX 지출 속도를 줄이지 않는 이유는

토큰 사용량 증대로 영업현금흐름이 폭발하여

CAPEX지출한 것보다

거기에 자사주 매입과 배당까지 포함해도

넘칠 정도의 영업현금흐름을 창출할 걸로 본다.

그러나, 그들의 데이터 센터 고객들, AI Lab과

SaaS 기업들에 대해서는 엇갈린 전망을 한다.

치킨게임을 할 것으로…

그리고 그 결과 2027, 2028년에는 치킨게임이

마무리되면서 2026년에 이어

수요가 아무런 굴곡없이

공급 늘어나는대로 J 커브로 증가할 것이라고.

그래서 자연스럽게 CAPEX 늘어나는 걸

자사주 매입과 배당까지 커버할 정도로

영업현금흐름이 폭발한 거라고.

여기에 배팅하실 분들은 배팅하는 게 맞음. 😎

🚗 $TSLA 차트가 진짜 재밌어지는 구간.

📈주봉은 하락 채널을 돌파했고,

월봉은 5년 넘게 만든 대형 베이스를 완성하는 모습.

지금 핵심은 500달러.

🚀여기만 뚫어주면

600 → 700달러 이상도 충분히 열려 있는 그림.

🚀반대로 조정이 나오더라도

414달러 부근만 지켜주면 추세는 아직 살아있다고 봄.

단기 노이즈보다

월봉이 이렇게 좋은 자리는 흔치 않은 듯 👀

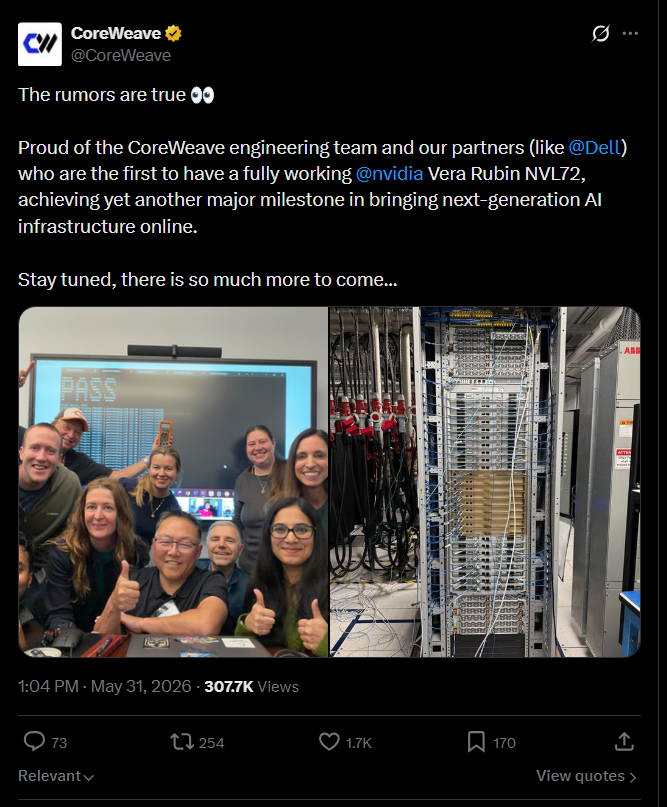

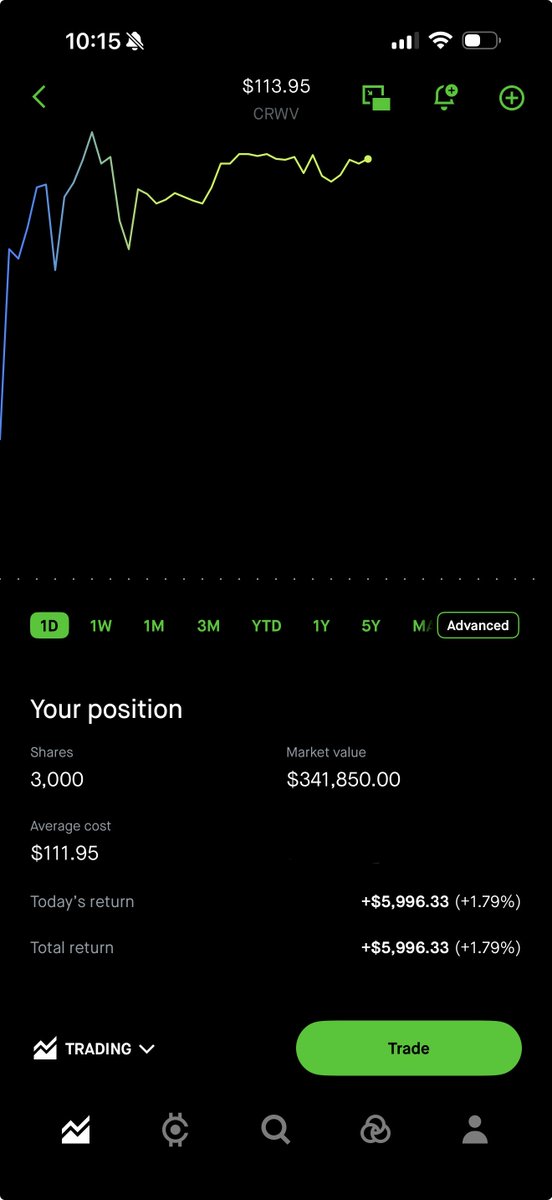

I've initiated a position in $CRWV in the overnight markets.

After being full-port $NBIS for a year, here's why I believe $CRWV is going to skyrocket in price over the next few months:

- $CRWV was named one of the first cloud providers to deploy Vera Rubin in H2 2026. Then Nvidia announced a brand new product, the standalone Vera CPU, and named CoreWeave as the first and only known customer. Another $2 billion invested directly into the company. 11% ownership stake. 8 gigawatts of AI factory capacity targeted by 2030.

- The "catch-up" trade: $CRWV is guiding $12 to $13 billion in 2026 revenue. $NBIS is guiding $3.3 billion. Same market cap. 4x the revenue.

The gap exists for a reason. CoreWeave carries severe debt and does not have a raid-boss CEO like Arkady running the show. Those are real risks.

But in a world where every tech company on the planet is compute-constrained, $CRWV has one direction in my opinion.

$200.

- SemiAnalysis, the most respected neocloud research firm in the world, gives CoreWeave their highest tier ranking. Not second. Not tied. Highest. The only cloud on earth with Platinum ClusterMAX status. Two years running.

- Revenue up 112% year over year. Backlog approaching $100 billion. The hyperscalers are customers, not competitors. Meta. Microsoft. Anthropic. They all pay CoreWeave because they cannot build what CoreWeave built fast enough themselves.

- The market cap is $60 billion on a business with $99 billion in locked revenue. Lol.

- I'm not worried at all about their debt. If they're not able to pay their debt for whatever reason, we've got bigger problems IMO.

I am the worlds biggest $NBIS bull, I could name every last aspect of that company, but $CRWV has gotten so cheap in my opinion that I had to take a position.

Not financial advice.

32B까지 커졌군요. (Teacher모델이겠지만) 얼마전에 저에게 차에는 1B 이상 모델은 넣지 못한다고 이야기하던 자율주행 엔지니어가 생각 납니다.

제 계산 기준 single thor에 약 2~3B VLA 모델 탑재 가능합니다. E2E로 가면 70B도 가능합니다.

+ 엔비디아 Hyperion 10의 OEM 공급가를 들으면 놀라실 겁니다. 엔비디아는 자율주행 시장의 주요 플레이어 중 하나가 될겁니다.

Just some mobile shower thoughts around $XFAB and train of thought:

1. 800vdc $NVDA push look for GaN/SiC players / power semis.

2. $NVTS and other fabless/fab-lite beneficiaries of $NVDA push probably use foundry models

3. care more about Western supply chains over Asia, want to build up Western capabilities + Western premiums.

4 China has a lot of capacity, maybe risk into 2028, but again it’s building up Western supply chains

5. XFAB only high volume SiC foundry in America (others like $ON or Infineon are vertically integrated)

6. advanced 6in SiC, 8in GaN on Si, building out 8in GaN

7. Maybe likely they’re developing 8in SiC from CHIPS backing, just not public material

8. check SiC revenue -> 152% Y/Y growth okay. Probably something markets missed, since blended looks worse from automotive slump, that should come out recovery

9. $NVTS and others turns out to use $XFAB. $POWI cites $XFAB in filings, among others.

10. both are $NVDA power semi explicit partners, great exposure indicator to 800vdc power semi players.

11. US Dpt. of commerce cites $XFAB as only high volume SiC foundry in the US, $50M PMT

12. validation from US Gov about critical component in supply chains is amazing

13. EU CHIPS Act gives $XFAB $128M EU, for foundry (MEMS, AI, etc), okay turns out they’re critical MEMS player

14. So that’s validation from EU gov about critical component in supply chains, dual continent subsidies

15. So now we know $XFAB is a critical MEMS foundry so you get SiC capabilities, GaN development, and MEMS upside

16. they also got $47.6M EU funding for leading Silicon Photonics supply chain in EU. So that’s EU funding on multiple angles.

17. Turns out, I know all the players there from smartphotonics from $GFS deck.

18. $NVDA and $NOK are qualifying them for silicon photonics HVM. I think this is just a government backing angle for success in EU photonics so likely to succeed… kinda like how Us gov encourages everyone to use $INTC.

19. Okay chips act 2 is coming out next week… so they’ll probably get funding there or more revenue commitments

20. 1.28 p/b, now that’s probably just book cost? Likely coming out of $SOI type legacy drag cycle.

21. Did some modeling around actually replacement values, true replacement p/b cost likely ~.5/.7.

22. Getting business for free, while having upside from SiC near term into Silicon Photonics / GaN as main growth past H2 2027.

Thoughts: derisked by p/b values + replacement value. maybe like 20% downside from macro.

However, critical dual continent importance. So downside risk seems low, but upside is compelling.

Lot of capex likely backstopped by upcoming chips act catalyst + national security concerns.

Maybe 2.5-4x rerating seems possible/likely.

Not a 10-20x, but recovery from depressed valuations from silicon photonics upside with SiC / GaN bridge.

TLDR: likely trading lower than replacement value, dual continent subsidies likely subsidize capex.

Gov grants shows importance to Western supply chains, photonics longer term upside, SiC/GaN demand likely near term upside and bridge.

Don’t control any recent volatility, should shake out anyone not really confident in the thesis though.

CHIPS act 2 from EU is coming up, $XFAB was listed in earlier blueprints for optical ecosystem, so should get a boost after that comes out as near term event catalysts.

So now is the risk reward seems compelling, we’ll see if this is right or not

https://t.co/rdpdCc2SrK

$AOSL

오늘 BusinessWire로 PCIM 2026 참가 및 제품 전시 보도자료 발표.

이번 포인트는 AOSL이 AI Core Power / AI Data Center / Industrial Power 전력반도체 포트폴리오를 전면에 내세웠다는 점임.

가장 중요한 문장은 AI 데이터센터용으로 MOSFET, αSiC, GaN 솔루션을 48V/54V 및 emerging 800VDC power architectures로 확장한다고 명시한 부분.

즉 AOSL은 단순 PC/소비재 전력반도체 회사가 아니라, AI 서버와 AI 데이터센터 전력 인프라 쪽으로 포지셔닝을 강화하고 있음.

보도자료에서 언급된 키워드도 중요함.

고밀도 DC/DC 변환

AC/DC 전력 변환

열 성능 개선

낮은 스위칭 손실

냉각 효율적 설계

MOSFET / SiC / GaN 포트폴리오

이건 NVIDIA 800VDC 랙 전력 구조와 직접 연결되는 테마임.

다만 아직 고객명, 대형 수주, 매출 가이던스 상향이 나온 것은 아님.

그래서 지금 단계에서는 “실적 확정 뉴스”라기보다 AOSL의 AI 데이터센터 전력반도체 thesis를 강화하는 제품/포지셔닝 뉴스로 보는 게 맞음.

개인 기록용. 투자 조언 아님.

이걸 보고 허겁지겁 네이버를 산다 = 하수

이걸 보고 엔비디아가 한국 시장을 전략적으로 굉장히 중요하게 생각하고 있으니 관련 종목을 폭넓게 매수한다 = 고수

네이버 데이터센터는 세종에 240mw 짜리 하나 밖에 없습니다. 춘천에 하나 더 있긴 한데 많이 오래됐구요.

그럼에도 불구하고 상당히 중요한 포지션에 올려둔 데에는 다분히 의도가 있어 보입니다.

한국의 촘촘한 5G 통신망을 활용해서 알파마요2를 비롯한 휴머노이드 등 피지컬 AI의 테스트 배드로 본격적으로 활용하려고 할 가능성이 높고,

이 두 가지 테마에 모두 가장 직접적으로 걸쳐있는 건 당연히 현대차입니다.

당분간은 휴머노이드를 비롯한 피지컬 AI, 엣지 AI 관련 종목들이 활활 타오를 것 같은 느낌입니다.

SKT, 삼성SDS가 준비 중인 한국형 데이터센터 진행 속도에도 가속이 붙을 가능성 또한 매우 높아 보이네요!

물론 이런 이유로 엔비디아 깐부치킨 먹을 때 네이버 샀다가 손절한건 안비밀😂😂

https://t.co/BwoYLVA9iB

유리기판이 실제 공장 투자 단계로 들어가고 있음.

Intel과 3DGS가 인도 Odisha에 약 33억 달러 규모 substrate plant를 추진한다는 보도가 나왔음.

대상은 advanced packaging glass core substrate, HDI substrate, 3D heterogeneous integration module 쪽이고, buildout은 5~6년으로 언급됨.

핵심은 단순함.

유리기판이 더 이상 연구개발 테마가 아니라, 실제 양산 로드맵으로 내려오고 있다는 점임.

AI 칩이 커지고, chiplet·HBM·고속 I/O·광인터커넥트가 붙을수록 기존 organic substrate만으로는 한계가 커짐.

그래서 유리기판은 단순 소재 교체가 아니라,

더 큰 패키지 면적, 더 촘촘한 배선, 더 나은 열 안정성, 더 높은 전력·신호 전달 능력을 위한 차세대 패키징 플랫폼임.

Intel뿐 아니라 TSMC도 CoPoS로 panel-level packaging을 준비 중이고, SKC/Absolics와 Samsung Electro-Mechanics도 유리기판 양산 로드맵을 갖고 있음.

다만 바로 매출이 터지는 뉴스로 보면 안 됨.

Intel-3DGS 프로젝트는 5~6년 buildout이고, TSMC·Samsung 쪽도 대체로 2027~2030년 양산 프레임에 가까움.

결국 지금 봐야 할 건 “당장 돈이 되냐”가 아니라,

AI 패키징 병목이 2027~2030년에 어디로 이동하느냐임.

유리기판의 진짜 관건은 이름값이 아니라 warpage, 미세 via, 수율, 고객 인증, 대량생산 능력임.

유리기판은 점점 진짜가 되고 있음.

진짜 수혜주는 “유리기판 한다”는 회사가 아니라, 실제 양산 난제를 통과하는 회사가 될 가능성이 큼.

개인 기록용이며 투자 조언 아님.

AI가 전기를 먹기 시작했다!

데이터센터 내부에서 벌어지는 조용한 혁명!

많은 사람들은 AI를 반도체 산업의 이야기라고 생각한다.

하지만 엔지니어들이 보는 AI는 조금 다르다.

그들이 보는 AI는 사실상 거대한 전기 소비 장치다.

예를 들어 최신 AI 서버 랙 하나는 과거 데이터센터 전체가 사용하던 수준의 전력을 소비하기 시작했다.

1. 문제는 GPU가 아니다.

전기를 어떻게 넣을 것인가가 문제다.

GPU는 1V를 사용한다. 그런데 데이터센터는 800V를 원한다.

흥미로운 사실이 하나 있다.

AI GPU는 실제로 매우 낮은 전압에서 동작한다.

대략

GPU 코어: 0.7~1.0V

HBM 메모리: 1~2V 수준이다.

하지만 데이터센터는 반대로 높은 전압을 원한다.

왜일까?

전력 공식 때문이다.

P = VI

전력(P)이 같다면 전압(V)을 높일수록 전류(I)는 줄어든다.

전류가 줄어들면

케이블 굵기 감소, 발열 감소, 구리 사용량 감소, 전력 손실 감소가 발생한다.

그래서 최근 AI 데이터센터는

48V→ 400V→ 800V DC구조로 이동 중이다.

2. 왜 800V가 중요한가?

전력 손실은 전류의 제곱에 비례한다.

Ploss = I2R

여기서 엄청난 차이가 발생한다.

예를 들어 1MW를 전송한다고 가정하자.

48V 시스템: 전류 약 20,800A

800V 시스템: 전류 약 1,250A

전류가 16배 감소한다.

손실은 전류 제곱에 비례하므로

16² = 256배 차이가 난다.

그래서 업계가 갑자기 800V DC 이야기를 하기 시작한 것이다.

이건 단순한 기술 업그레이드가 아니라 데이터센터 경제성을 바꾸는 구조 변화다.

3. 여기서 등장하는 것이 SiC

기존 실리콘은 800V 이상 영역에서 문제가 생긴다.

고전압에서는 스위칭 손실 증가, 발열 증가, 효율 감소가 나타난다.

그래서 등장한 것이 실리콘 카바이드(Silicon Carbide, SiC)다.

SiC는 절연파괴 전압이 높음, 고온 동작 가능, 스위칭 속도 빠름이라는 특징이 있다.

쉽게 말하면 "더 뜨겁고 더 강한 전기를 다룰 수 있는 반도체"다.

데이터센터 내부에는 사실 수천 개의 초고속 스위치가 있다

4. 많은 사람들이 전력반도체를 전선을 연결하는 부품 정도로 생각한다.

실제로는 아니다.

전력반도체는 초고속 스위치다.

초당 수십만 번에서 수백만 번 전기를 켰다 껐다 한다.

왜 그럴까?

전압을 변환하기 위해서다.

예를 들어

800V

↓

50V

↓

12V

↓

1V

과정을 거쳐야 GPU가 사용할 수 있다.

이 과정에서 전력반도체는 엄청난 속도로 스위칭을 반복한다.

진짜 병목은 자기(Magnetic) 부품이다

여기서 투자자들이 거의 보지 않는 영역이 나온다.

대부분 사람들은

GPU→ 전력반도체까지만 본다.

하지만 엔지니어들은 전력반도체 → 자기소자를 본다.

왜냐하면 전력 변환 과정에는 반드시 인덕터, 변압기, 초크 코일이 필요하기 때문이다.

전력반도체가 아무리 좋아져도 자기소자가 따라오지 못하면 효율이 무너진다.

5. SST(고체변압기)가 주목받는 이유

현재 변압기는 수십 년 전 구조와 크게 다르지 않다.

무겁다. 크다. 반응 속도가 느리다.

반면 SST는 전력반도체, 고주파 변압기, 디지털 제어를 결합한다.

기존 변압기가 수 톤이라면, SST는 훨씬 작고 빠르게 전압을 제어할 수 있다.

AI 데이터센터가 늘어날수록 변압기 → SST전환 압력이 커질 수 있다.

6. 그런데 SST의 진짜 문제는 열이다

사람들은 SST를 전기 기술로 생각한다.

실제로는 열 기술이다.

전력 밀도가 높아질수록 전력반도체 발열, 자기소자 발열, PCB 발열 이 동시에 증가한다.

그래서 최근 데이터센터에서는 공랭→ 수랭→ 직접액체냉각→ 액침냉각으로 이동하고 있다.

결국 전력 산업과 냉각 산업이 합쳐지기 시작한 것이다.

7. AI의 다음 전쟁터

많은 사람들은 AI 전쟁을 GPU 전쟁으로 본다.

하지만 데이터센터 내부를 들여다보면 진짜 전쟁은 다른 곳에서 벌어지고 있다.

800V 직류 전력망. SiC 전력반도체. 고체변압기. 자기소자. 액체냉각. 그리고 이 모든 것을 연결하는 전력 아키텍처.

AI가 발전할수록 GPU의 성능보다 중요한 것은 전기를 얼마나 효율적으로 움직일 수 있는가가 된다.

결국 미래의 AI 데이터센터는 컴퓨터 공학의 결과물이 아니라, 전력공학·재료공학·열역학이 결합된 거대한 산업 시스템에 가까워질 가능성이 높다.

그래서 지금 가장 흥미로운 질문은 "어떤 AI 모델이 이길까?"가 아니라,

"1MW짜리 AI 랙에 전기를 넣고 열을 빼낼 수 있는 기업은 누구인가?" 일지도 모른다.

A more complete basket of analog/power semis:

In case anyone wanted to do more research:

- $POWI: GaN ICs for AC-DC power conversion

- $WOLF: vertically integrated SiC substrates + power devices

- $NVTS: pure-play GaN + SiC power devices

- $AOSL: power MOSFETs, DrMOS + power mgmt ICs

- $VICR: modular power modules

- $MCHP: microcontrollers, analog + SiC power devices

- $IFX (Infineon): broadest power portfolio: Si, SiC + GaN

- $STM (STMicroelectronics): vertically integrated SiC supply chain

- $DIOD: discrete diodes/MOSFETs + analog power mgmt ICs

- $IPWR: power switches

- $ON: SiC + silicon power semis

- $VSH: discrete power MOSFETs, diodes + passives

- $ADI: analog, signal-chain + power mgmt ICs

- $MPWR: DC-DC power mgmt

- ROHM (6963): SiC, GaN + analog power mgmt ICs

- Renesas (6723): analog, power mgmt + GaN

- $ALGM: magnetic current sensing + motor driver power ICs

- $TXN: everyone knows?

A lot of these have run up a fair bit over the past quarter.

But just comparing to optics:

$NVDA's $4B check into $LITE + $COHR validated optics as core AI infra.

Nvidia has done similar architectural & named-partner equivalent for power. But without the capital injection / single wake-up catalyst.

So personally feel that there's room for further growth, mainly within some of the smaller MC names that I'm currently looking into more intensely.

Best accounts to follow from each frontier lab to stay constantly up to date

Anthropic

@karpathy

- must-follow account for AI; recently joined Anthropic

@bcherny

- Claude Code creator, always shares great tips

@trq212

- also a Claude Code developer; writes amazing articles on CC

OpenAI

@polynoamial

- works on reasoning research, shares a lot of technical details

@gabriel1

- Sora developer, great career path

@jxnlco

- works on dev experience, shares a lot about Codex

Google AI

@OfficialLoganK

- all the major Google Gemini and AI Studio updates

@ammaar

- product and design; shares great things about vibe-coding in Google AI Studio

@fofrAI

- cool use cases for generative models

Cursor

@leerob

- the loudest voice behind Cursor updates

@ericzakariasson

- shares great insights on using Cursor

@mntruell

- Cursor’s CEO; major releases and usage updates

xAI

@milichab

- recently joined xAI, shares updates on Grok

@skcd42

- also covers major Grok releases

My favorite humanoid stocks ranked:

1. $AMBA (Ambarella) — Best pure-play edge AI vision for robotics. 37% revenue growth, 60% gross margins,$100M+ robotic pipeline, still under $5B market cap. The risk is concentration and scale. The upside is being the de facto vision processor as robots proliferate.

2. $6324.T (Harmonic Drive) — Irreplaceable. There is no substitute for strain wave reducers in high-precision robot joints. 75% market share with Nabtesco. Hard to replicate. If humanoid robots ship in any volume, this company prints money.

3. $ALGM (Allegro MicroSystems) — Near-monopoly in motor current sensing, priced like an auto cyclical. 30-50 sensors per humanoid at automotive-tier P/E multiples. The market hasn’t re-rated this for robotics yet.

4. $VPG (Vishay Precision Group) — The purest humanoid hardware play. Precision load cells and force sensors with a 1.21 book-to-bill. Risk: trading at 255x current earnings on ~$320M revenue. If humanoid volumes slip, this gets crushed. But if they don’t, VPG is the most direct bet on robot touch.

5. $MOG.A (Moog) — Aerospace-grade precision actuators with a credible humanoid crossover. Already up 83% on the thesis but the volume ramp hasn’t started. Defense + robotics optionality.

3분기부터 내년 예산 편성 얘길 드리는 이유.

2018년까지 이어진 메모리 수퍼 사이클에서도

2018년 초가을까지 기업 내에서도 2020년까지는

엄청 좋을 꺼라 했음.

당연히 애널들도 2020년까지는 문제 없다 했음.

그래서, 2018년 3분기에 2019년 계획을 수립할 당시에도

엄청 Positive하게 수립.

왜냐하면 서버 고객들(지금의 하이퍼 스케일러)한테서도

다른 이상 신호가 없었기 때문.

그런데, 실제로는 2분기부터 마소 CEO인 사티아 나델라가

효율성에 대한 얘기를 시작함. ROE.

그러고 나서는 2018년 10월에 서버 기업들의 공습이 시작됨.

그것도 2019년 계획이 승인 받은 직후에.

들어왔던 주문이 점점 차주로 밀리기 시작.

급기야 그 속도가 빨라짐.

그러더니 4분기 폭망 분위기.

그러면서 가격도 급속도로 떨어짐.

이유는 서버 기업들이 재고가 쌓였던 것.

그래서 2019년 계획을 다시 수립.

애널들도 찬양 분위기에서 급랭 분위기로 전환.

그런데, 지금 빅 4 하이퍼 스케일러 기업들의

건설중인 자산이 급증.

이 건설중인 자산에는 데이터 센터 완공이 지연되어

아직 서비스에 투입되지 않은 GPU, 메모리도 있음.

원가 구조를 보면 아마 대부분일 것.

그 내용은 여기에...

https://t.co/r0QwDXB4oD

그냥 그렇다고...알고 있어서 나쁠 건 없으니.😊

아래는 삼전 DS의 영업이익 변동. 노란색 표시가 2018년 4분기.