GHO's revenue model is changing and most haven't realized how big this can be for @aave's balance sheet.

Today, a growing share comes from the GHO Stability Module (GSM) itself.

1. User deposits USDT0 into the GSM

2. GSM mints GHO against those USDT0 reserves

3. Reserves are deployed into yield-generating strategies

4. Yield flows back to the protocol

USDT0 on @Plasma's Aave instance is earning a higher yield than sGHO, giving Aave a free carry on sGHO for each GHO minted on Plasma.

The result is that GHO can generate revenue even when no one is borrowing.

Looking at @Token_Logic's breakdown, GSM revenue has gone from almost non-existent to becoming a significant revenue driver for GHO over the past 12 months.

In March, even before the LZ/Kelp exploit took place, GSM overtook traditional borrowing revenue, generating $438K in fees and representing >50% of GHO's monthly revenue.

Traditional stablecoin revenue depends on credit demand, but GHO's new model has a second revenue engine: productive reserves. The GSM went from being a peg mechanism to becoming one of GHO's largest revenue drivers.

Props to Token Logic on leading that initiative via the RemoteGSM.

8/ Aave is now entering a new growth phase with V4.

Preserving the protocol's reputation and balance sheet is non-negotiable.

Thinking long term is what keeps Aave a leader and fuels its continued innovation.

1/ The buyback pause at @aave raised a lot of questions. That makes sense.

Buybacks are a capital allocation decision, and like any capital allocation decision, the right answer changes as conditions change.

A thread on what that means in practice ↓

7/ Some of the best capital allocation decisions in history looked wrong in the short term.

For over a decade, Bezos faced constant criticism for refusing to return capital to shareholders. No dividends, no buybacks. Every dollar went back into building Amazon.

His answer was consistent: when the return on reinvesting capital exceeds the return on giving it back, you reinvest. Every time. Without hesitation.

A DAO should not allocate a disproportionate share of its revenue to holder returns while higher-return growth opportunities remain on the table.

Every dollar reinvested into expanding the protocol compounds into future revenue, future dominance, and future value for every holder.

The goal is not to distribute as much as possible today. It is to build something worth holding for the long term.

Aave Labs’ UK subsidiaries Push Labs Ltd. and Push Virtual Assets Ltd. (together “Push”) have received approval from the UK’s Financial Conduct Authority (FCA) to register as a cryptoasset exchange provider in the UK.

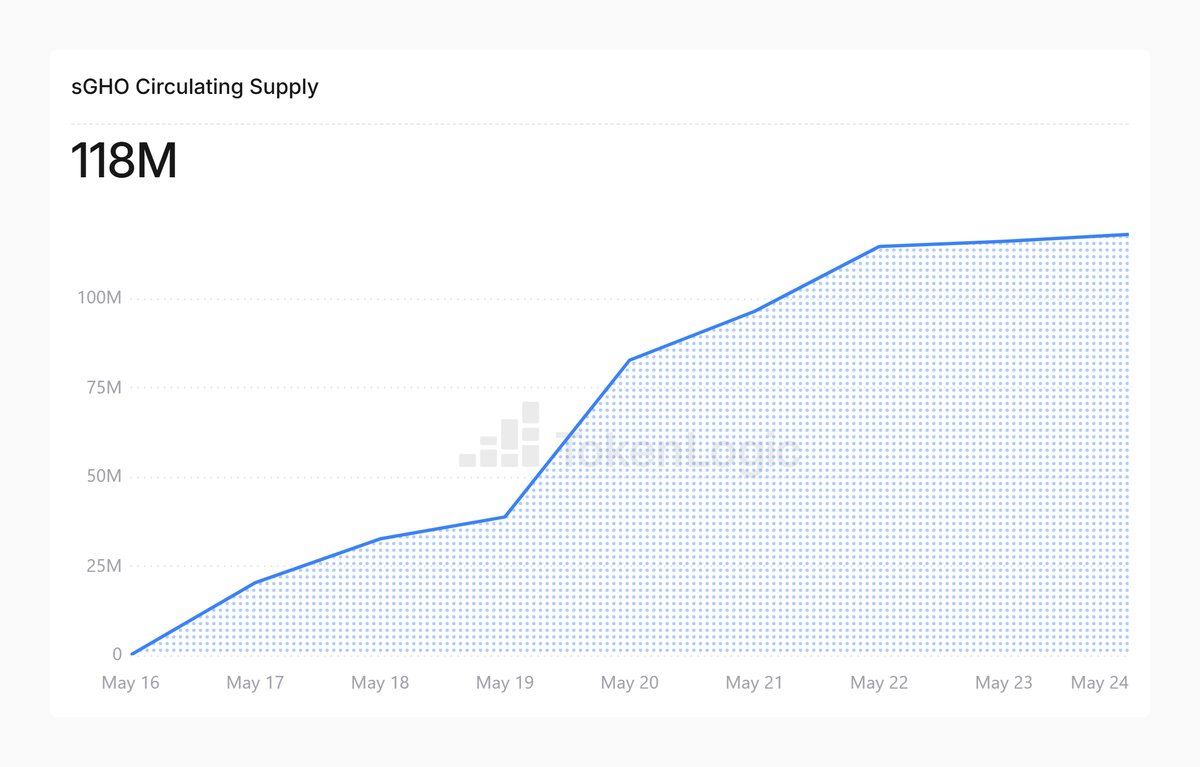

GHO revenue is starting to compound fast.

The ethereum:0x40d16fc0246ad3160ccc09b8d0d3a2cd28ae6c2f Stability Module has now generated over $3.45M in cumulative revenue, with $3.08M coming from deposit yield and only $363K from GSM fees.

That changes the narrative around GHO. The main revenue driver is no longer mint/burn activity or swap fees. It is productive stablecoin liquidity.

Idle liquidity inside the GSM is starting to earn yield at scale, and that revenue flows back into the Aave ecosystem.

This is why the sGHO migration matters.

The important shift is not only more GHO adoption. It is more GHO moving from passive stablecoin liquidity into yield-bearing liquidity.

@aave is slowly building a stablecoin system where liquidity itself becomes productive capital.

Data via @Token_Logic

Aave's yield-bearing assets are powering everyday spending through the @MetaMask Card.

We published a case study on how Aave, MetaMask, and @Mastercard enable users to spend yield-bearing assets at any Mastercard-accepted location.

Read it below.

Over 100 active positions and $310M+ in syrup assets are already live on Aave, users depositing yield-bearing syrupUSDC and syrupUSDT as collateral, borrowing stables, and running tight leverage loops.

It’s about time we see yield-bearing collateral in action at this scale.

One of the most compelling use cases emerging on Aave is the integration of @maplefinance syrup assets (syrupUSDC and syrupUSDT) as yield-bearing stablecoins backed by overcollateralized institutional lending

These tokens don’t just sit idle, users actively deploy them as collateral to create leveraged yield strategies

➥ How the Strategy Works

1. Deposit yield-bearing collateral ➝ Users supply syrupUSDC or syrupUSDT (which themselves also earn 4–5% APY from Maple’s secured lending pools) into Aave

2. Borrow stables ➝ They then borrow against this collateral in assets like USDT0, GHO, or other liquid stables

3. Loop / Leverage ➝ The borrowed stables are often swapped or redeposited elsewhere (or back into Maple) to amplify exposure, while keeping positions tight

This creates capital-efficient loops where users capture the spread between @maplefinance institutional yield and @aave borrowing costs

Approximately 101 active syrup-related positions are live across Aave deployments (primarily Plasma, Base, Mantle, and Ethereum Core)

Many run with tight Health Factors in the ~1.02–1.08 range, classic behavior for experienced leveragers who monitor closely and rebalance as needed

Activity is concentrated on syrup assets acting as a multi-chain collateral layer, enabling users to park idle stables while generating layered yield

FYI, @Token_Logic dashboard lets you instantly search 'syrup', drill into individual positions, see collateral composition, debt breakdowns, and health factor distribution.

Quick video preview by my fren @DeFi_Andree ↓↓

One of the clearest signs that institutions are starting to use DeFi seriously is happening on @aave Horizon.

A metric I like tracking on @Token_Logic is the supply growth of RWA collateral assets like:

• USCC

• USTB

What makes this interesting is: this is not typical retail flow.

To supply these assets usually requires:

• KYC

• whitelist access

• qualified investor status

So when supply grows aggressively, it often means: → more institutional capital is moving on-chain.

But the important part is how these assets are being used.

Institutions are starting to:

• deposit USCC/USTB into Aave Horizon

• use them as collateral

• borrow RLUSD, USDC, or GHO

to unlock liquidity without selling the underlying assets.

This is why Horizon is becoming an efficient bridge between:

RWA assets ↔ DeFi liquidity.

The growth already reflects this:

• Horizon TVL: ~$515M+

• Utilization: ~55–57%

• One of the fastest-growing RWA lending markets on Aave

Institutions are beginning to use DeFi similarly to traditional finance:

• hold yield-generating assets

• borrow against them

• maximize capital efficiency

The difference is: everything now happens on-chain, in real time, and 24/7.

DeFi is slowly evolving from a crypto trading system into a liquidity layer for real-world capital.