$FTC (Filtronic) +30% yesterday on the news that FCC voted to increase the capacity of high-speed satellite broadband by 7x.

The news came after the London exchange closed, so I expect Filtronic to gap up on Monday.

Filtronic’s core business is designing and manufacturing the advanced E-band transceivers and solid-state power amplifiers that allow satellite networks—specifically Starlink—to communicate with the ground at ultra-high speeds.

The market immediately interpreted this regulatory move as a massive green light for Filtronic's order book.

Filtronic still massively undervalued if you ask me.

Introducing... my cycles theory for Gold, which I am calling the "10/4 Cycles Theory".

It says that Gold operates around a 15 year cycle. The bull market takes 10 - 11 years, while the bear market takes 4 - 5 years.

In February of this year, the bull market would have ended, which begins the 4 - year bearish phase of the cycle, set to last until 2030 or 2031.

The cycles have incredible accuracy when viewed this way, with one interesting example of a failed bull market period between 1985 and 1996. You can see where the two cycle top events (red dots) landed and fell flat during that time in their appropriate places.

The cycle begins with one bottom event and is followed by two top events, which are the major points. These come during precise 1.5-year windows in the peaks and troughs of the sine wave cycle.

This is my latest major cycles theory to join the Halving Cycles Theory (Bitcoin) and the Quartercent Cycles Theory (S&P 500). All of which remain accurate to the current date.

For the 10/4 Theory to be successful in the near term, the bull market must end by July 2027 at the latest, which is at the end of the 10 - 11 year window. It seems highly probable, though, that February 2026 fulfilled this.

By the time you become a geopolitical expert in one conflict it's time to move on to the next. This is why bulls retire and bears sound smart short term but end up underperforming long term.

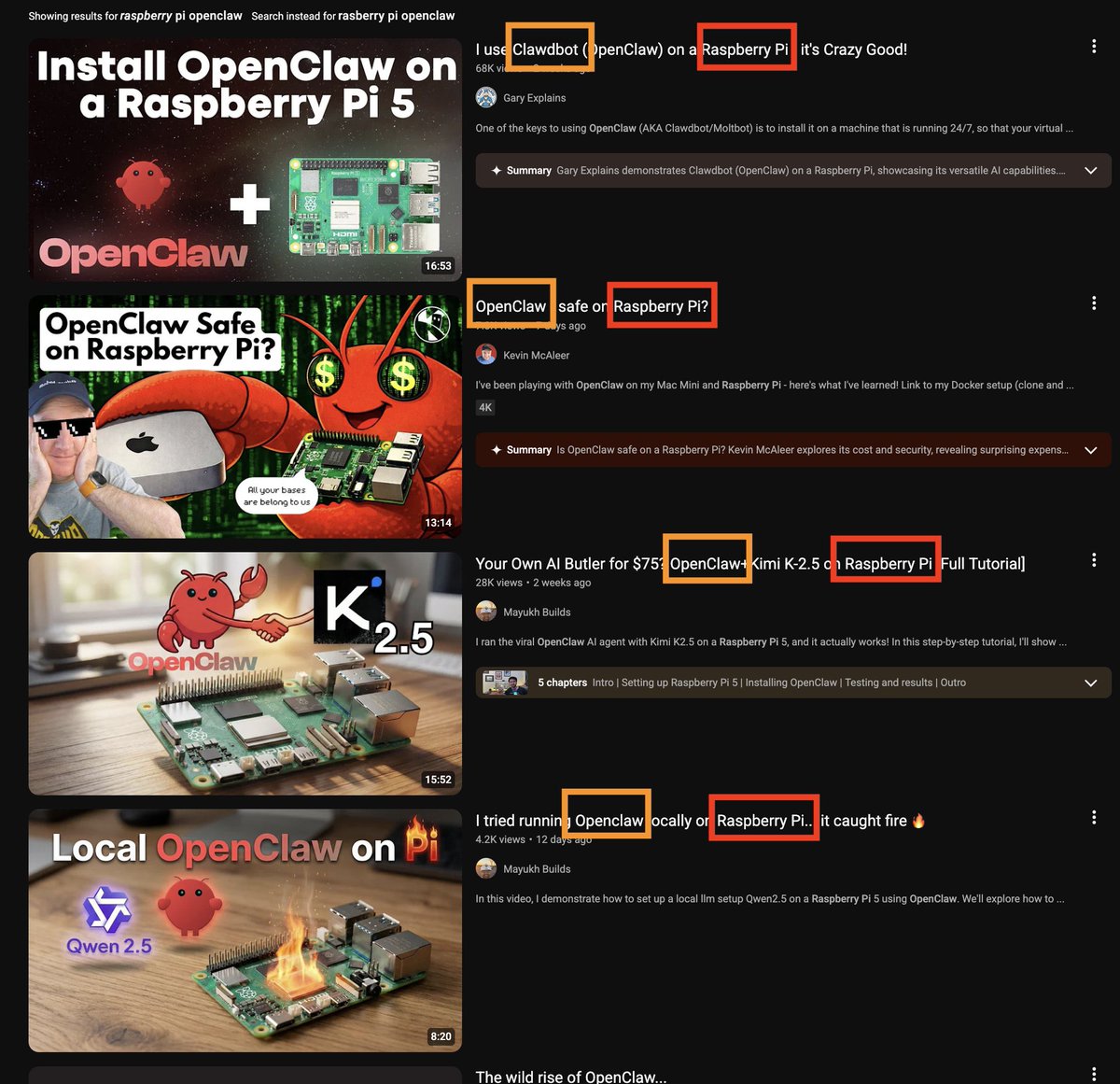

Fun Trade Idea: Long $RPI (Raspberry Pi)

Reason: 🦞 Openclaw / Picoclaw / Nanobot + Hoarding.

Everyone has been openly hoarding Apple Mac Minis and were long Apple.

But $APPL is already a $3.7T+ company. Product mass-buying won't make a dent.

Raspberry Pi, however, is a 542.68M company.

The revenue is material.

Feels like markets haven't priced this in since I've seen almost 0 mentions about the ticker on X (but many product mentions).

And it's only recently that have the hoarding started Raspberry Pis, as they're much cheaper than $500+ Apple products. They also have their mini $NVDA CUDA-light utility ecosystem that people use.

So it turns out these extremely cheap $20 or $200 devices are perfect for deploying mass deploying isolated instances.

The reason is for OpenClaw orchestration (so they don’t mess up your device) -> interfacing with a central LLM via API.

Before people were just buying 1 or 2 for hobby/education purposes, so revenue has slowing.

But now Silicon Valley startups and individuals anecdotally appear to be buying tens or hundreds of these things to run concurrent OpenClaw agentic swarms or do stuff like agentic marketing on Reddit and other places.

And no, there are many applications that can't be done by spinning up AWS VPS, so people do it locally (there's TOS around automation/AI bots, so companies setup their own servers).

That being said main downside risk is that its

- partially foundation owned, and they might not hike rates like $SNDK or $MU does, even if there's extreme demand

- Subject to memory price hikes like LPDDR4 component

so this is not a major position.

However, going forward, revenue should increase due to people buying tens or hundreds of these things for running AI agents.

Balance sheet also looks clean with low downside risk:

- ~$280M - $300M revenue

- ~$75M+ Gross Profit

- ~25% Gross Margin

- Net income: ~$10M - $15M

- Net Cash: $28M

Analysts currently project revenue growth closer to 14–17%.

But if the demand influx continues, we might see revenue numbers might hit increase from 14% growth to a modest 48-55% if hoarding continues.

Consumer segments are roughly 1/3rd of revenue but the newfound buying from Openclaw + variants is a new cataylst nevertheless for re-rating.

Especially now that Picoclaw and compressed OpenClaw variants are now able to be run on $20 Raspberry Pis instead of just the Raspberry Pi 5’s.

But seems like people just forgot Raspberry PI was a publicly stock as well.

The stock price is down 56% 1Y to 542.68M euro MC to an all time low.

So this might be that tailwind for a reversal.

There's also a non-zero chance OpenClaw is a long term catalyst for Raspberry Pi based, agentic deployments.

TLDR: People are openly buying Raspberry Pis and Apple Mac Minis for Openclaw/Picoclaw, so revenue should benefit from increased demand.

Bloomberg on the Raspberry Pi ( $RPI ) and the OpenClaw / PicoClaw / NanoClaw thesis:

In their interview with Adam Montanaro, a fund manager at Montanaro Asset Management:

"Thematically the evolution of a Raspberry Pi from hobbyist board into a core piece of AI infrastructure is correct"

Henry Ren from Bloomberg also stated:

"Another positive for Raspberry Pi has been a rash of share purchases by founder and Chief Executive Officer Eben Upton, who has bought stock on five separate occasions since late January, filings show."

It's great to see institutional validation of Raspberry Pi's transition from educational hobbyist boards into core infrastructure for AI hardware orchestration.

That being said, the rest depends on the company's execution to grow into their new TAM with AI agents.

Yikes if these $TTD allegations from Publicis are true.

Overcharging clients & opting them into up-sells without their consent.

This agency (representing 10% of $TTD's billings) no longer recommending it to clients.

$TTD's response was very short & lacking detail. Maybe they say more in the coming days. I would think they’d have more to say in the near future. 🤷♂️

We'll see how this shakes out.

Intimidating claims at the very least.

Here is how I use $GOOGL Gemini to learn about as much companies as possible. It only takes me 5 minutes per company.

Follow my 4-steps to do the same 👇

PayPay ( $PAYP ) is the newest IPO.

If you're wondering if you should fomo in the $PYPL / WeChat of Japan at an $11.8B MC?

Let's find out.

If you've ever been to Japan: PayPay is everywhere.

It's the Japanese SuperApp for payments, investing, and banking.

Here's a breakdown:

FY 2025 metrics:

Revenue: ¥299.1 billion (~$1.9 billion)

Growth Rate: ~26.3%

Net Income (GAAP): ¥39.2 billion (~$248 million)

P/E: ~44x

Stock Base Compensation: Virtually 0, unlike $SNAP and $DUOL in the US.

If we look at balance sheet:

Consolidated accounting makes things a nightmare when you see $PAYP ¥4.85 Trillion (~$32.3 Billion) in liabilities or customer deposits mixed into assets.

But pre-IPO net debt is approximately -$480M, and post-IPO proceeds of ~$496M.

So balance sheet looks roughly net cash slightly positive but neutral. Also PSA: Softbank is the majority owner, lockup expires September 2026.

At $11B, it's roughly ~5.8x P/S and very profitable for a Japanese superapp growing at 26% with expanding margins and zero SBC.

By US standards, this is normally valued, not exactly a screaming buy.

TLDR: In general, $PAYP is not a terrible long at $11.8B.

Might get some IPO hype + mixed with low float dynamics, but would not chase if it ends up a lot higher.

Maybe there's some TAM expansion like $HOOD that prices it up over time. But Softbank ATM-like overhang in a few months.

But there's a lot better mispriced choices out there like $RDDT right now.

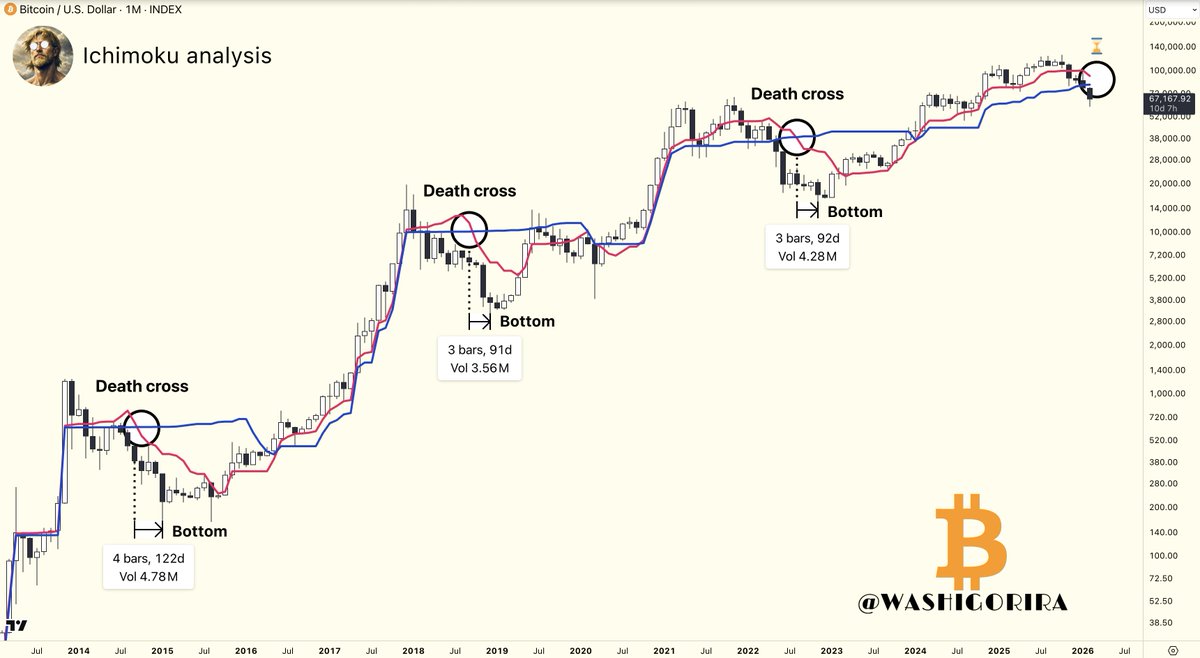

#Bitcoin Death Cross

In previous cycles, BTC bottomed 3–4 months after the Ichimoku monthly death cross.

The death cross has not formed yet.

Structurally, this suggests it may still be early.

As an investor, you NEED to know how to read an Annual Report (10-K).

But they often have hundreds of pages and seem way too complex.

Here's how to efficiently read and understand a 10-K (+example)👇🏼

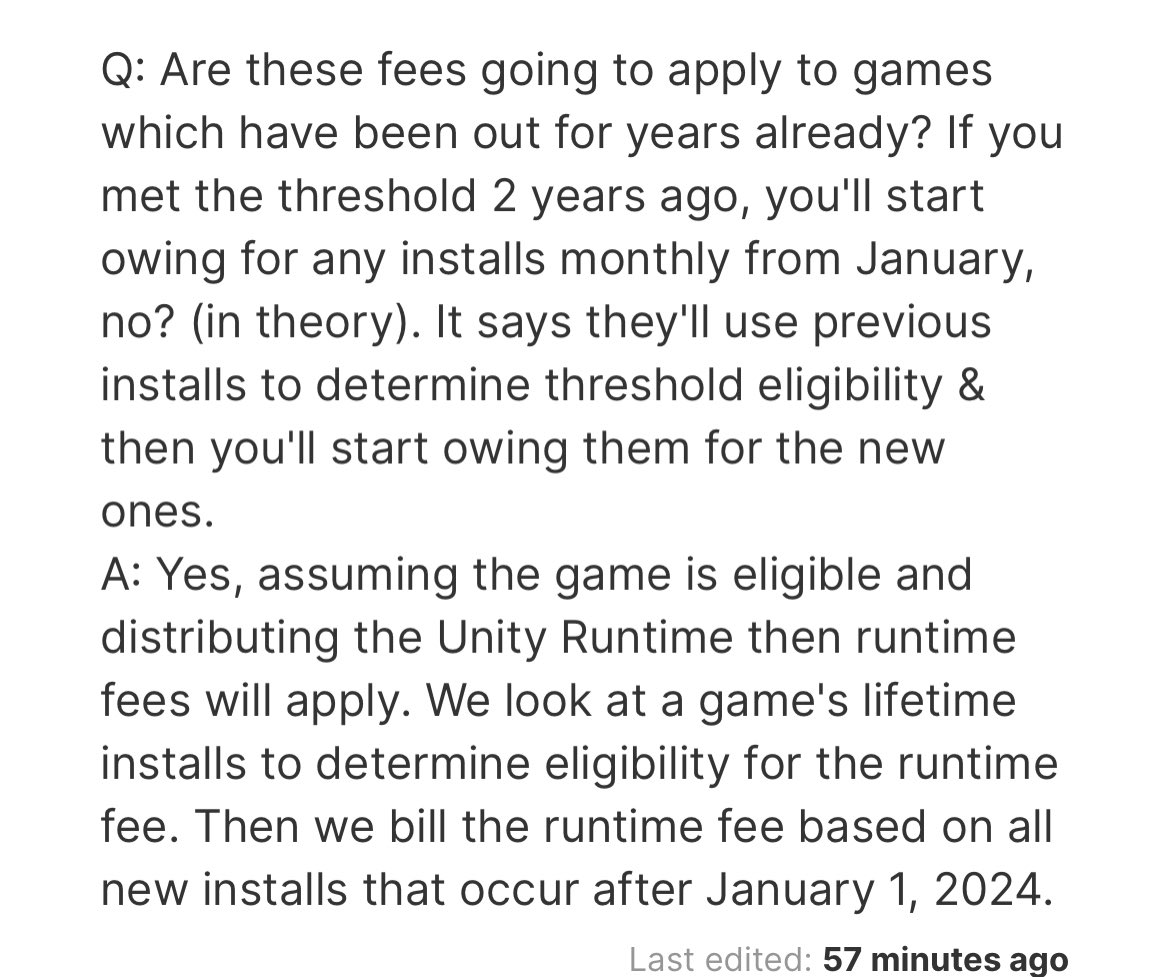

@unity Absolutely unbelievable🤡 Unity confirmed they’re going to make install-bombing indie devs into bankruptcy possible, including for pre-existing games

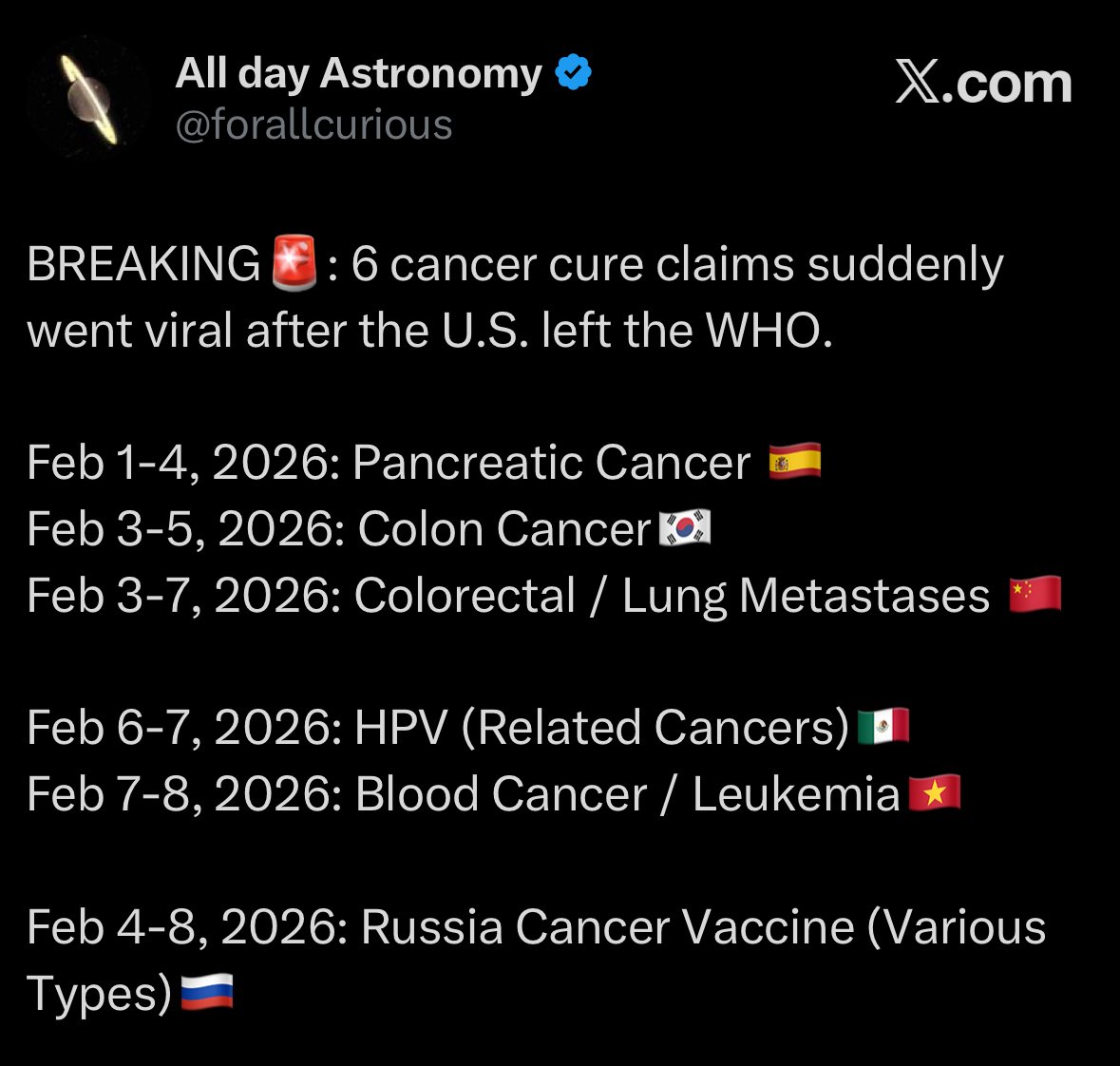

>U.S leaves WHO

>Multiple Countries discover potential cures and treatments for cancer over night

>Mega boom in medical science research across the world

>what was holding them back?