Albanese on Monday acknowledged in his most pessimistic remarks to date that Australians would continue to cop “economic aftershocks” long after the conflict ends, as he declared that the decades of global economic growth enjoyed since WWII are over.

https://t.co/zLV3KWT7BE

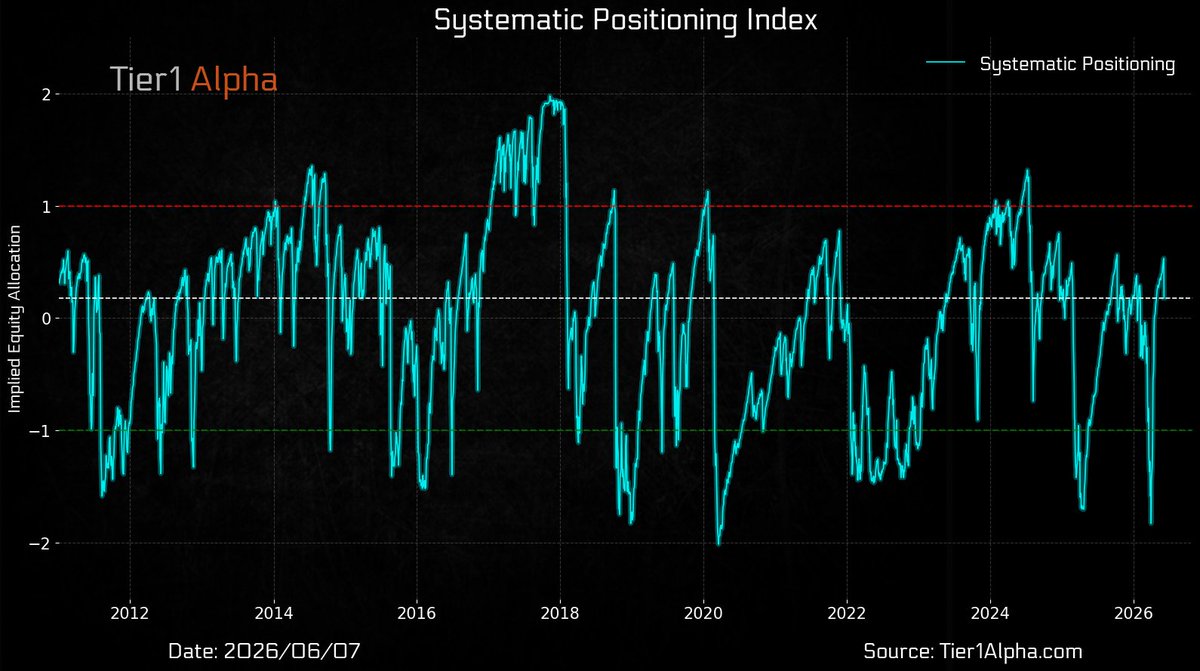

Last week was all about the concentration unwind, which was accelerated by levered ETF flows.

While both of those dynamics remain actively in play, the next wave of structural risk is dealers shifting meaningfully short gamma at the same time we see forced selling from CTAs.

To be clear, last Friday was a concentration unwind exacerbated by forced selling from leveraged funds into the close.

Looking ahead, there is still a significant amount of systematic convexity built up in other areas of the market should downside momentum/ vol start to trend.

The continued lack of progress towards restoring normal energy flows from the Middle East is reinforcing expectations of a prolonged period of elevated oil prices. The 2027 average price for both Brent and WTI is now trading near cycle highs, with Brent at USD 81.4 and WTI at USD 76.5, both more than 20% above pre-war levels.

During the dot com melt-up of 1995-2000, Nasdaq put up gains of 572%.

To date, from the 10/13/22 bear market lows, Nasdaq is up just 162%.

Listening to bears calling this a bubble top could cost you a lot of money.

We have seen some notable shifts in our equity sector indicators over the past month, driving a sizeable change in our sector allocation engine.

Semiconductors, financials, energy and healthcare remain favored, with the most upside to our estimates of fair value.

Employment week again!

Despite some "squishy" numbers in April (& early May) - employment incomes overall did well in May.

Very resilient US economy, innit.

Goldman Sachs: The market has already begun valuing the memory Big Three on a P/E basis, and no longer treats them as mere cyclical commodity companies.

“As evidenced by the recent expansion in ROE, Samsung Electronics and SK Hynix have breached their historical P/B valuation ceilings. This suggests that the market may no longer value these companies as pure cyclical commodity plays. This re-rating is supported by the widespread adoption of LTAs, or long-term agreements, with hyperscaler customers. Unlike previous cycles, these binding LTAs—often accompanied by prepayments—provide earnings visibility and create a structural floor against downcycle losses.”

U.S. capital goods imports—which include the semiconductors and computing equipment fueling the data center buildout—rose a record 40.1% in the 12 months through April, according to trade data out this morning from the Census Bureau (https://t.co/dpi23PmCTa)

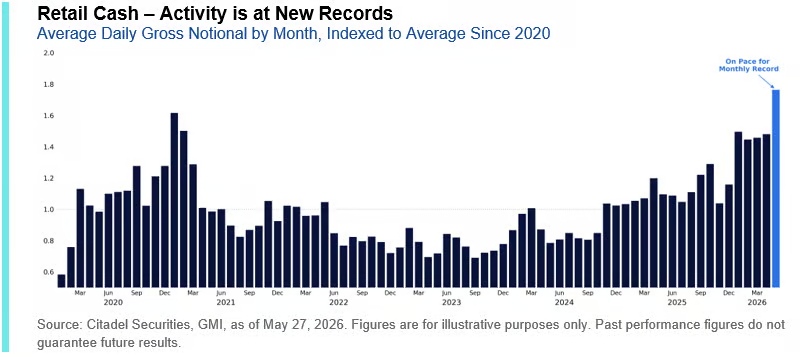

"Retail traders are the new price setters in the market ... Daily volumes on our cash platform are setting new highs and are on pace to finish nearly ~10% above the previous record established during the January 2021 meme-stock era."

-Citadel Rubner