@mercoglianos Thanks so much for sharing your thoughts & questions here. Many professional investors in the sector like myself are grateful for your generosity and we value your perspective. You are a master teacher. Thank you!

@ManihiB VLCC tailwinds: The shift of crude to compliant from shadow tonnage, e.g., Venezuelan crude flows now move on compliant tonnage. Also, attrition is high for shadow fleet, pulling older tonnage out of compliant fleet. 30-40% of VLCC fleet is over 15 yrs. vs order book of 18%

@100xCompounding Thanks for sharing, this is good downside protection at the least; we know $TDW has strong earnings power going into 2027 against a constructive backdrop for offshore. We'll see how it plays out, but I like the future prospects for the segment

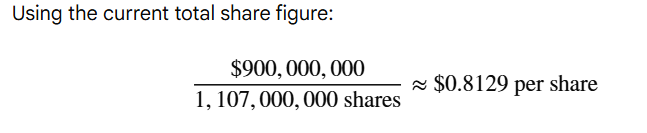

@Armin_Hartl Some math regarding debt reduction: 2025 total interest expense was $555M. Reducing debt by half frees up $277M, elevating FCF to $900M or .81c/share. Post merger economics change this, but if rates stay flat, still a pretty sound asset. (12% yield, FCF/Share)

@Armin_Hartl $RIG has significant upside if they can simply maintain high utilization of their assets for the next 5 years; the debt reduction alone will dramatically increase earnings even if lease rates only appreciate modestly from here. The reduction in interest expense is material

@wisdomandboats I appreciate you analysis. Perhaps the situation is just too dynamic at the moment to analyze quantitatively. Once the dust settles, I think we return to a strong market for the compliant VLCC fleet. The recent consolidation by Sinokor is another x factor

@DA28030@DryBulkETF I agree, significant VLCC tonnage is trapped in the gulf. There may be some headwinds from the relaxation of Russian sanctions, but we should still see strong demand for compliant vessels

@TheDriller11 This is a rational position. Also, there is strong structural support for more offshore activity. The pendulum is swinging that way and these higher prices aren't going to hurt capex spending by the producers.

@christankerfund Chris, thanks for sharing. Sustainability is key here. We're getting confirmation that more freight is moving on compliant tonnage (e.g., post sanction Venezuelan exports)- shadow fleet has been distorting real economics of the market. This plus Sinokor consolidation.

@christankerfund Chris, I think the real catalyst is the shift towards compliant freight that has been underway + shadow fleet attrition- if I had to call out a single factor. Sinkokor is certainly a tailwind.

@olaharaldmoen1 I think this coupled with strong spot rates will trigger a re-rate. Good move by management, gives some earnings stability and helps them focus on getting more upside from the remaining assets.

@AyusoValue That is potentially game changing. This suggests strong liquidity in the term market. If we see term fixtures at these levels persist, then 2026 could be the year for VLCCs

@ZannisManolis This is just business as usual for Mr. Market; he is super worried that a peace deal will collapse rates to break even levels for VLCCs. I'm going to remain patient-the 2026 setup is actually quite constructive for crude transport. We'll see how it plays out.