Former Hedge Fund guy, now devoting my time to educating individual investors. For me: God - Family - Flyfishing - Options trading, in approximately that order.

I am personally *very* happy that a bunch of Space obsessed science nerds just became very rich. I love space. I love nerds. None of that has anything to do with whether I think Elon is a turdmuffin or what SpaceX is "worth" or the mess we've made of market capitalism.

UPDATE:

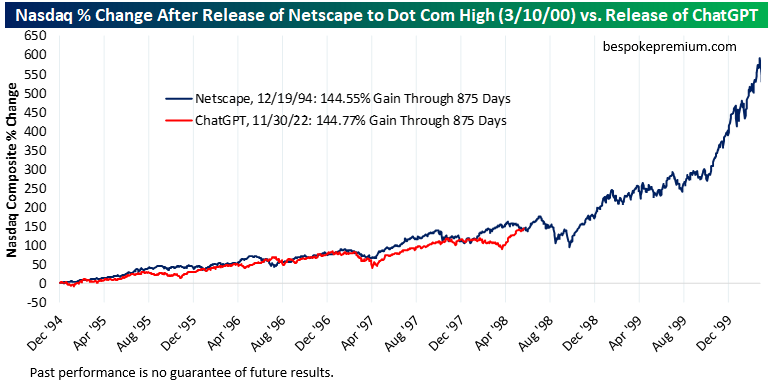

Nasdaq at 875 trading days after the release of Netscape on 12/19/94: +144.55%.

Nasdaq at 875 trading days after the release of ChatGPT on 11/30/22: +144.77%.

Past performance is no guarantee of future results!

Investor demand for downside protection is plummeting:

The average 3-month put-to-call skew of S&P 500 single stocks is down to 0.04, the 4th-lowest reading over the last 20 years.

This measures how much more investors are paying for downside protection via put options than for upside exposure through call options.

The lower the reading, the less investors are paying to protect themselves against a market decline.

The average 3-month put-to-call skew has fallen -75% since March, posting the sharpest drop since April-May 2025.

This metric is even lower than during the 2021 meme stock frenzy.

Investors are no longer thinking about downside risk.

Wrapped up the global @EQDerivatives conference.

Recap:

Option selling and call overwriting programs continue to grow rapidly as they fit neatly into the modern adviser suite selection process. Institutions and advisers continue to gravitate toward products that generate distributable yield and smoother return profiles. Dealers are feasting off the persistent price insensitive and largely dogmatic flows that naturally emerge from these programs.

Buffered ETFs are scaling at an incredible pace and are quickly becoming another dominant yield enhancement vehicle within adviser platforms. The growth trajectory and investor appetite are substantial. Similar to covered call products, these structures create large, recurring, price insensitive flows that dealers are increasingly monetizing and positioning around.

QIS allocations continue to get larger across institutional portfolios. A significant portion of that participation remains yield generating in nature. But people are wary that it’s just all a game of elegant backtests and poor live results.

FLEX options are growing massively in size. Although they function somewhat like quasi structured products due to their customization, dealers and hedge funds are becoming increasingly creative in how they utilize them for hedging. It feels like only a matter of time before FLEX volume meaningfully explodes from current levels.

Classical relative value signals appear to be decaying at a rapid pace. Many of the traditional vol arb relationships that worked for years are becoming increasingly noisy. The industry as a whole has become much more sophisticated in sourcing and implementing newer RV frameworks, while many legacy shops appear to have been left behind structurally.

There are still many fantastic managers across L/S equity, commodities, macro, and other areas. However, it is becoming increasingly difficult to allocate to high quality volatility hedge funds. Many of the strongest vol managers have already been absorbed into pod structures at large multi manager firms. As a result, there is a growing sense of adverse selection among the remaining standalone vol managers. Hedge fund database performance numbers across the vol space seem to reinforce this dynamic as well.

There is now such a large oversupply of volatility selling coming from U.S. structured product issuance, particularly in the 1Y to 2Y part of the surface, that larger trading firms are actively building specialized teams specifically designed to capture and warehouse that edge.

Despite nonstop geopolitical tension and increasingly unstable macro headlines, the overwhelming institutional appetite still remains yield focused. In practice, that largely translates into continued structural short volatility exposure across the system. The demand for income generation continues to dominate discussions.

Insurance companies remain, by a very wide margin, some of the largest volatility traders on the street. The amount of Vega sold through the VA market has become staggering. Simultaneously, the RILA market has grown into hundreds of billions of dollars in assets and has become one of the fastest growing insurance product categories in the United States over the last several years.

A meaningful portion of the industry does not appear to be hedging tenor for tenor in this environment. Instead, we are increasingly seeing shorter dated puts being utilized as substitutes for longer dated downside protection. In a scenario where equities continue grinding lower over time, that mismatch could become extremely problematic.

Portable alpha appears to have fully repaired its reputation. A growing number of large institutions are revisiting and implementing portable alpha frameworks as a portfolio optimization tool. In a world where passive investing continues to dominate traditional sources of outperformance, institutions are increasingly looking for ways to layer differentiated alpha streams on top of core beta exposure

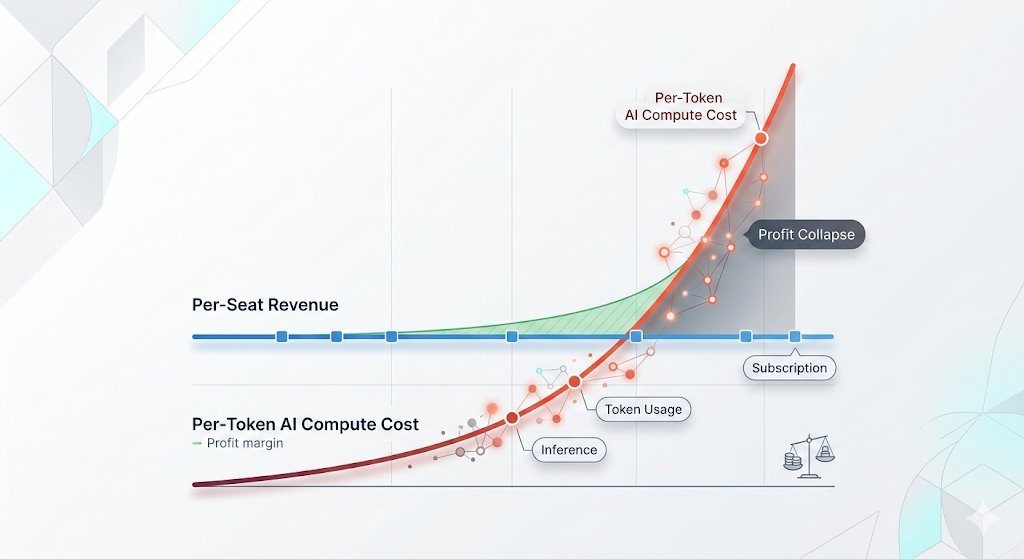

This @HedgieMarkets post illustrates where the infinity scalable asset-light technology model meets the physical realities of an asset-heavy business that faces an upward sloping supply curve.

We have long argued that AI compute is just another bit-atom commodity (like crypto) that uses a lot natural resources to create a valuable (unlike crypto) virtual asset.

On the bit side, Big Tech is a price-maker with fat margins. On the atom side, a price-taker.

Big Tech grew up in bits — search, social, e-commerce, office software: asset-light, infinitely scalable, natural monopolies. Build once, serve billions, watch costs fall every year. So they assume AI is the same game and will spend whatever it takes to own the market.

But inference is also atoms, i.e. land, critical minerals and electrons, which are mostly molecules. In the commodity world, competition drives price to marginal cost: P = MC, which is upward sloping as volume rises. The better the models get, the faster they compete their own margins down to the physical floor which rises with volume.

You can already see it. Microsoft just cancelled Claude Code because the cost to run it exceeded the value it returned — demand retreating the moment price met real cost. The irony: the customer pulling back was itself a hyperscaler. In April, Uber confirmed once again that AI compute demand is price elastic.

Bottom line: they assumed AI costs would keep falling like they always did on the bit side; however, on the atom side, there is a hard floor that likely rises in the short run.

I am not denying that the margins are still fat. But it’s not the same model. These guys are running towards obsolescing their own pricing power. Why did Rockefeller stop at the gas station and not vertically integrate into cars?

🦔Microsoft canceled its internal Claude Code licenses this week after token-based billing made the cost untenable, even for a company with effectively infinite cloud resources. Uber's CTO sent an internal memo warning the company burned through its entire 2026 AI budget in just four months. American AI software prices have jumped 20% to 37%, and GitHub (owned by Microsoft) is dropping flat-rate plans for usage-based billing across its products.

My Take

The AI subsidy era is ending in real time. The same company that put $13 billion into OpenAI and built the Azure infrastructure powering most of Anthropic's compute just looked at the bill from a competitor's coding tool and decided it was not worth paying. That is not a productivity failure on Anthropic's end. Token-based pricing is forcing every enterprise customer to confront the actual cost of running these models at scale, and the number turns out to be far higher than the flat-rate experiments suggested.

This ties directly to my Gemini Flash post yesterday. Anthropic, OpenAI, and Google all raised effective prices in the last six months. Enterprises that built workflows assuming AI costs would keep falling are now watching annual budgets evaporate in months. Two outcomes look likely from here. Either enterprises scale back AI usage to fit budgets, which slows the revenue ramp the labs need to justify their valuations ahead of IPOs, or the labs cut prices and absorb the losses, which makes the unit economics worse at exactly the wrong moment. Both paths land in the same place, the numbers stop working, and somebody has to take the writedown.

Hedgie🤗

As pointed out below, “stocks are increasingly seen as an inflation hedge,” so fund managers are piling in.

The idea that stocks are a hedge against inflation is not new and has not worked for over a century.

BofA’s Michael Hartnett’s latest “Flow Show” from Friday:

* above 4% on CPI where risk assets get twitchy…

past 100 years once CPI crosses 4% on average SPX -4% next three months, -7% next six months.”

Note that year-over-year CPI inflation was 3.8% through April.

Warren Buffett warned about this almost 50 years ago:

Fortune, May 1, 1977

Buffett: How inflation swindles the equity investor

“For many years, the conventional wisdom insisted that stocks were a hedge against inflation. The proposition was rooted in the fact that stocks are not claims against dollars, as bonds are, but represent ownership of companies with productive facilities. These, investors believed, would retain their value in real terms, let the politicians print money as they might.”

He goes on to describe when this belief peaked: “This heaven-on-earth situation finally was ‘discovered’ in the mid-1960s by many major investing institutions. But just as these financial elephants began trampling on one another in their rush to equities, we entered an era of accelerating inflation and higher interest rates.”

Finally, note that fund managers’ top three tail risks are in the chart on the right:

* Second wave inflation (40%)

* Geopolitical conflict (20%)

* Disorderly rise in bond yields (18%)

These three risks total 78%, and they could be argued to be variations on the same theme – the war will continue to drive crude oil prices higher, creating a second wave of inflation and higher bond yields.

----

“Those who cannot remember the past are condemned to repeat it.”

– George Santayana, from The Life of Reason (1905)

The fear over AI is palpable.

So, it's time for my optimistic take ....

Why the AI doom-and-gloom story is missing the bigger picture

A lot of people hear “AI” and immediately think one of two things: it’s just Google search on steroids, or it’s a magic machine coming for everyone’s job. Both miss the bigger picture.

A job is not one single task; it’s a bundle of tasks supported by a massive, fragmented software stack. Email, spreadsheets, presentations, Slack, CRM platforms, and, in finance, a Bloomberg Terminal, FactSet, and market data feeds. For millions of jobs, the cost of software to provide basic tools for these tasks can run to $1,000 a month, and more for complicated roles.

Much of the modern workday is consumed by the friction of this stack: moving data between systems, cleaning spreadsheets, searching for files, and summarizing meetings.

AI is emerging as the new interface for enterprise software. Think about the iPhone. It collapsed cameras, GPS devices, and music players into one simple, powerful device. AI is doing something similar for workplace software, turning 10 clunky programs that don't talk to each other into a single conversational prompt.

Just as we stopped buying standalone cameras and tape recorders once the smartphone came around, companies will happily pay for an AI layer. It will be far cheaper and eliminate the bloated costs of that fragmented software stack that requires you to perform endless, mundane tasks because these programs do not talk to each other.

The immediate fear is that if AI lets three people do the work of five, companies will fire two people. But that ignores economic history.

When the electronic spreadsheet was invented, the cost of calculations plummeted. But accounting jobs didn't vanish; demand for complex financial modeling exploded. Accounting clerks became financial analysts, a more in-demand role.

Jevons Paradox suggests that making a resource more efficient actually increases total demand for it. By absorbing the drudgery, AI allows the employee to focus on judgment and strategy—making the human element more valuable, not less. In this framework, demand for high-output workers doesn't shrink; it explodes.

Does this justify the mind-numbing capital expenditure currently pouring into AI infrastructure? If AI fulfills this promise of enterprise-wide productivity, the investment isn't just justified—it’s a bargain. That said, we are clearly near the peak of a hype cycle, just like the internet was in 1999.

But remember: the dot-com crash did not mean the internet was a bust. It simply meant the hype outpaced the infrastructure. After the wreckage cleared, the optimistic predictions about connectivity and productivity were not only fulfilled—they were exceeded.

The same path can lie ahead for AI. And instead of the fear that AI will replace workers, it's the joy of replacing soulless busywork, making jobs more fulfilling... and more profitable for employers.

I do wonder, with so much public market capital flowing into LLMs, how much of that ends up reinforcing a simple conclusion: equities trend higher over time.

If these models are trained on data that overwhelmingly reflects that reality, they may naturally surface signals that affirm “stocks go up.” That, in turn, can create a reflexive bid, turning the output of the models into a self fulfilling dynamic.

In a way, this resembles a new form of crowding. The growth of learning models is concentrating around one of the strongest historical truths in capital markets, and that concentration itself may be reinforcing the trend.

BREAKING: Treasury Secretary Scott Bessent and Federal Reserve Chair Jerome Powell summoned Wall Street leaders to an urgent meeting on concerns that Anthropic's new Mythos model could pose a systemic risk, per Bloomberg.

What if the whole LLM thing is a false start? If the flaws are inherent systemic problems - if the compounding of hallucinations/errors can't be sorted out? If the capex build out is one of the biggest misallocations of capital ever? Then what? https://t.co/XVhr6mfCTN

@donnelly_brent That has been the name of my fantasy basketball team for the last decade! I still say that term in the exact accent that was used in the opening scene of the game!