@jukan05 i don’t think there’s any precedent of a leading edge foundry packaging another leading edge foundry’s silicon

e.g. typically TSMC only packaged their own silicon

More bullish read. Dylan Patel dropped some aggressive AI compute numbers on the Sequoia pod:

+20 GW deployed in 2026, net of delays

+30 GW forecast for 2027, also net of delays

-OpenAI + Anthropic alone at 100+ GW combined by 2030

-Compute moving into the terawatt range by 2040

He never said whether the 20/30 GW figures are US or global, or whether they're IT load, facility load, AI-only, or broader data center capacity. Sounded more like global additions to me. I wouldn't treat it as a clean US number but it's in the range of possibilities assuming more aggressive conversions/timelines.

Same problem with the 100 GW forecast. I don't read that as OpenAI and Anthropic owning 100 GW of self-built campuses. Neither company owns gigawatt-scale generation today. Most of their committed capacity sits inside hyperscaler and neocloud contracts, GPUs, TPUs, Trainium, third-party deals. Stack "100 GW for OpenAI + Anthropic" on top of hyperscaler/neocloud buildout numbers and you're double counting. Better read is compute available to the labs, not a separate owned supply stack. Still, the ramp is nuts if it lands!

From Dylan's prior comments on pods, OpenAI + Anthropic were sitting around 3.5-4 GW combined exiting 2025, heading toward 10 GW exiting 2026 and 20 GW exiting 2027. Get to 100 GW by 2030 and that's:

>~96 GW added from YE25 to YE30, ~19 GW/year

>~80 GW added from YE27 to YE30, ~27 GW/year

For scale:

-100 GW × $50B/GW = ~$5T

-Global GDP 2025: ~$117T. $5T is ~4.3% of it

-US GDP 2025: ~$30.8T. $5T is ~16.2% of it

-100 GW is roughly Texas-scale power capacity

Given I don't have specifics, the more interesting part is token economics to me vs the GW headline. If frontier labs can monetize scarce tokens at very high gross margins, they can rationally overbid for compute. Dylan cited Anthropic as net-income profitable ex-stock comp in Q2, possibly profitable including stock comp by Q3, with frontier API token gross margins above 80% before blended-channel effects kick in.

That changes the clearing price for compute. At those margins, doubling the compute cost still leaves attractive gross margins and higher absolute gross profit if capacity is the bottleneck. Renting more GPUs/TPUs/Trainium doesn't scale headcount 1:1 either. Also explains the rental dispersion he cited:

-Trainium under $10B/GW/year

-GPUs historically ~$12-13B/GW/year

-SpaceX-Google GPU deal ~$25B/GW/year annualized (ST spot deal given compute constraints)

Same story at the data center layer --> Power-only colo has moved from ~$60/kW-month historically to $120-160/kW-month, with a wider spread depending on grid reliability, counterparty credit, location, time-to-power.

Comes back down to we can all guess how many GW get built but the real question is whether model-driven demand and token monetization keep outrunning physical supply, capital, and grid execution.

we are hiring for many engineering roles

electrical, mechanical, SWE, MTS, TPM, and more

apply below or dm me.

if you don't see a role that fits you exactly, still dm me.

we make roles for exceptional talent.

https://t.co/UVGMRXtfak

in finance but wanting to build something beyond pitch decks and management presentations? Come build the future of AI at Fluidstack! If you've been wanting to make the jump but not sure if you have the skill set, we are looking for the following backgrounds:

Capital markets, project finance, real estate, power and utilities, FP&A, and accounting

Apply below or dm me. If you don't see a role that fits you exactly, still dm me. We make roles for exceptional talent.

We are hiring people that want to get hands on and create the scale AI needs to revolutionize work

https://t.co/d6Ya6qZhAo

Mira Murati's Thinking Machines made Bridgewater’s private expert judgment trainable, beating frontier models with 29.8% fewer errors.

With naive prompts, all tested models sit around coin-flip accuracy, roughly 46% to 50%.

Expert prompts lift them sharply, reaching about 74% to 78% average accuracy.

The workflow was filtering finance articles, reports, central-bank documents, and emails to decide what investors should read.

This is a serious signal for enterprise AI, that bringing private judgment in the loop beats general intelligence.

The problem was not reading finance documents, because frontier LLMs can already read them.

The harder task was deciding which facts deserve attention inside an investor’s workflow.

A tariff headline can move markets, while another geopolitical headline may add no signal.

The breakthrough came from replacing written rules with high-quality labels from expert investors.

Non-expert labels failed because the task depends on taste, not surface financial language.

Bridgewater cleaned those labels by sending model-disputed cases back to experts for review.

The model then learned patterns that experts could recognize, but could not fully verbalize.

Training used interleaved batches, CISPO loss, and on-policy distillation from stronger teacher checkpoints.

Interleaving helped the model share judgment across tasks without blending them into noise.

CISPO controlled policy updates, so learning stayed aggressive without drifting into brittle shortcuts.

(CISPO is a new reinforcement-learning loss that caps how strongly each generated token can update the model, improving training stability while keeping useful rare tokens active. It was initially proposed by MiniMax team in 2025)

On-policy distillation penalized moves away from better teachers, then promoted stronger checkpoints.

The result beat the best frontier model, with 29.8% fewer mistakes and 13.8x lower inference cost.

@bubbleboi@bubbleboi Also any of the pure-play companies outside of the supply chain play are 1) typically private, 2) likely to be acquired by AMD/NVDA/INTC 3) hard to diligence due to different tech approaches

I've seen people on X talk about how this is a signal that demand is not as unconstrained as analysts make the market out to be - but I believe this is a backwards read

Building a NeoCloud, especially a GPUaaS one, is a lot like baking a cake where you need all of the ingredients to come together at once:

1. A viable site with power

2. A customer to offtake the capacity or a backstop agreement to provide contractual support

3. Financing for said equipment

4. Equipment delivery dates that meets customer and site timelines

Financing is the ingredient people underrate. Lenders want a collateral base, and they treat these offtake contracts as something they can securitize (think SaaS ARR-based lending). No contracted demand, no financing

Arrangements like this enable NeoClouds to meet insatiable demand by accessing more financing - this article speaks to that supply-side challenge, not demand weakness

https://t.co/EBiG2MpFOT

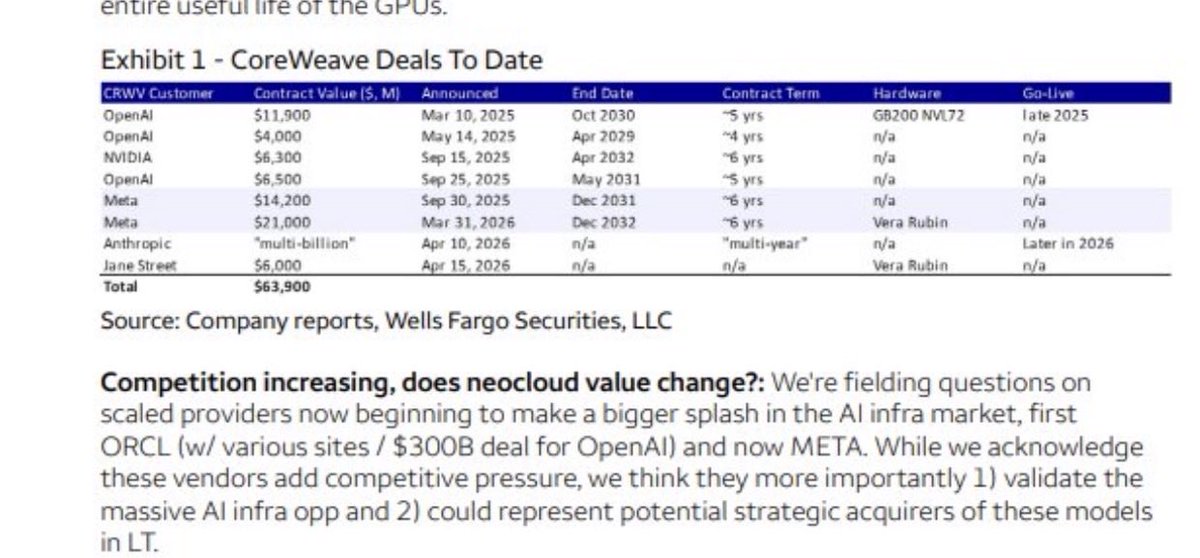

Wells Fargo: $META intent to sell excess compute is a positive signal around underlying demand and unit economics of AI.

“Despite this shift, we don’t expect a pullback in Meta’s capex or that overall compute needs are lower”

Regarding Neoclouds: WF thinks it validated the massive AI infra opportunity as well as acquisition opportunities. Despite any potential competition for Neoclouds.

I’m inclined to agree with Wells Fargo here and say markets completely misunderstood Meta’s excess compute comment.

$nbis, $meta, $crwv, $orcl Mstanley out tonight w/ clarifying comments re: bb report. Tldr: If meta does sell compute, it will be as a bare-metal offering of spare internal 1P capacity (not 3rd party-leased) to serve as an "eps bridge" while they develop their core products.

What's key is ms doesn't believe meta can or wants to compete as a full-service stack, since their models are limited & they don't have the expertise, software, or salespeople to service specialized, high-touch enterprise inference markets (precisely the markets $nbis, for instance, seeks to serve). MS suggests meta is not contractually-allowed to resell any of their 3P leased raw silicon from nbis, crwv, orcl, etc., Believes they will save their cutting-edge contracted capacity (e.g., the nebius 12B Vera Rubin order), for internal use.

Net/net: If meta does enter the compute market it will be as a stopgap, and in the bare-metal, older chip market. A minor supply addition, at best; least threatening, arguably, to nebius of all the neo's; and all this only assuming a backdrop where the compute supply were to materially loosen.

A data point on the supply-demand balance for AI, users across percentiles continue to see their usage scale over time - demand follows the scalability of SaaS, while supply is constrained to hardware/infrastructure limits https://t.co/wejaNpiN1Q

@dee_bosa this speaks exactly to the scarcity of compute and highlights 2 things:

1. this is an allocation issue. Firms like SpaceX and Meta have frontier models that are underutilized, while anthropic continues to see revenue ramp with enterprise adoption (SemiAnalysis). Reallocating capacity used to support these in-house models is key to enable those that need capacity the most

2. selling in-house silicon capacity to outside parties allows you to get better economics when using your own silicon. The costs paid to DSPs (Broadcom, Mediatek, etc.) get scaled across more silicon, making the economics of running an in-house silicon program even more appearling

Etched came out of stealth at $800M and by lunch X had NVIDIA in the ground

We do this every few months. A chip launches, the deck says killer, the timeline holds a funeral, and NVIDIA closes green anyway

Etched hardwires the transformer into silicon. That is where the speed comes from, nearly the whole die on one job instead of the ~30% a GPU uses. It is also the trap. The day that chip tapes out is the best it will ever be. You cannot patch it. You burned progress into a wafer and now pray the field stops moving

NVIDIA made the opposite bet. Same board, faster every quarter in software. Dynamo is pulling more tokens per watt out of the same rack, on version 1.0

The depreciation risk the bears aimed at NVIDIA for two years does not live at NVIDIA. It lives here, on the chip built to bury it

Etched is not a fraud. It is a niche tool priced like a general one, and $800M is not enough to run a frontier supply chain. The rest get bought on the next down cycle

Bury the lead, not the leader. Full case with @JackFarley96 and @maxwiethe on @MTSlive

And special thanks for @baseten for the cool T Shirt!

Chapters

00:00 Switching from bonds to semis

00:33 What Etched actually is

01:31 Faster and cheaper, but how much HBM

02:56 Maturing market, not an NVIDIA killer

05:01 $1B in contracts and a Taiwan factory

05:20 Why these startups all get absorbed

06:48 Tiered inference and the obsolescence trap

09:39 Etched vs TPUs and Trainium

12:17 Is the CUDA moat weakening

13:21 Co-design, squeezing every token per watt

14:37 NVIDIA is a software company that sells a chip

14:58 Who is NVIDIA's most dangerous competitor

16:23 The NVIDIA killers, ranked

18:19 A rich man's game

18:43 AMD's MI500 vs Rubin Ultra

20:19 The neocloud business decision

22:46 Lightning round, Rambus the toll on HBM

25:11 The CXL run-up on Astera, Marvell, Credo

26:22 Use AI less, go to the booth

28:10 EDA is not dead

We are hiring:

- Talent Acquisition

- Electrical Engineers

- Mechanical Engineers

- Prod Engineers

- MTS

- SWE

- People Ops

Dm me or apply https://t.co/c8der2CHJQ

If modular construction is waiting on a scalable application to take off, data centers are an interesting angle to see how this process can really take off.

Compared to traditional housing, data centers tend to leverage a defined basis of design and then drop it at various sites. If players like Crusoe, GIGA, etc., can learn the difficult lessons of modular manufacturing and then deploy at scale, we may see the benefits heralded for housing in the data center space, where time to market and cost are at even more of a premium

https://t.co/5rkvN2OhoS

Hey everyone, I have received permission from my employer to publish this research.

It is a lengthy investment thesis on what I believe will be the next chapter of AI. After months of research, we are turning bullish on the hyperscalers and explain why we believe the market is underestimating where the economics of AI are ultimately heading.

The rest is covered in the X article below. I hope you enjoy reading it, and I look forward to hearing your thoughts and challenges.