Data center demand is not impossible because of turbine blade shortages.

We’ve done this before:

In 2002, the US grid added 57 GW of natural gas capacity in a single year, and almost 200 GW in 5 yrs.

That’s higher than data center forecasts.

Then what’s the problem? 🧵

The Electricity Grid

I post a lot of stuff about the electricity grid, here the CEO of the largest grid in America (PJM) lays it out pretty clearly.

• What worked for 2 decades… no longer works

• This is structurally different from history

• You are facing an era of scarcity

• The situation is not tenable

PJM are facing a demand explosion. Now a demand explosion in some industries is +500% demand. But this is infrastructure, this is tens of trillions of dollars of assets and it takes time to mobilise and deploy things at this scale.

In infrastructure, when demand growth shifts from +1-2%/yr to +8%/yr, then you suddenly need to be building 4-8 times more assets per year, than you previously did.

If you were deploying $1 trillion / yr to grow at 1%, you now need to deploy $8 trillion / yr to grow at 8%.

Suddenly you need to deploy many trillions of dollars per year to meet this growth. If you cannot get it done, prices will rocket for everyone. Failure leads to inflation.

This is not a PJM problem, this is not even a US problem, this is a global problem. PJM are formally validating what some people have been saying for a while now.

This is not temporary, we cannot uninvent the technologies that have precipitated this change. The world has changed and we must adapt.

Global retail electricity sales are about $3.6 trillion per year, of that, around $900 billion goes to transmission and about $2.7 trillion goes to wholesale generation.

The transmission system many developed countries have is the wrong system going forward. Our transmission systems in the West are built for transporting power from big coal plants to power big towns. That’s not what we are doing now.

We have replaced most of the coal plants with two largely decentralised but highly correlated fleets of intermittent generators (wind and solar), that are growing like fracking wells because they are also quick to deploy.

Their quickness to deploy new generation projects is massively destabilising for the grid. The grid was designed for coal plants. The grid is a $50 trillion machine. It is by far the biggest asset in any country. It isn’t something you can toss away, it isn’t something you can swap out overnight.

We also have new categories of industrial demand (hyperscalers) that will capture an increasing share of GDP. This new demand category is going to set the marginal price of electricity for everyone else, and these guys are not as price sensitive as your widowed grandmother.

This is a difficult problem to address because of:

i) the scale

ii) the capital intensity

It’s also a global problem, because it’s born out of a new technological paradigm. It will not spread around the world at equal pace, but everywhere is going to eventually face it down.

Some people are fleeing to space for solutions to avoid this snafu, but that’s only a temporary fix.

Once the hyperscalers have their demand satisfied, the next demand explosion immediately follows, and this second wave is 20x the scale of the current problem.

The second wave is how do you power billions and billions of robots and billions of autonomous machines, doing work that currently can’t be done?

This industrial revolution is very much a two stage revolution, first you power up the chips, then you power up the actuators.

Chips scale down, actuators scale up.

There’s no Moore’s Law for actuators, they obey Newton’s Laws of motion instead.

This is the crux of the energy problem facing our civilisation. The energy system we have today is the one we wanted 20 years ago. The energy system we will have in 20 years from now, is the one we start building today.

It’s time to build this solution.

🇪🇸 Spain's electricity in 2000: 56% fossil, 2% solar & wind. By 2026: 44% solar & wind, just 17% fossil.

The crossover came in 2023. Gas now sets the price only 15% of the time vs 89% in Italy.

More in my forthcoming Substack newsletter 👇

https://t.co/In5lBaF2ox

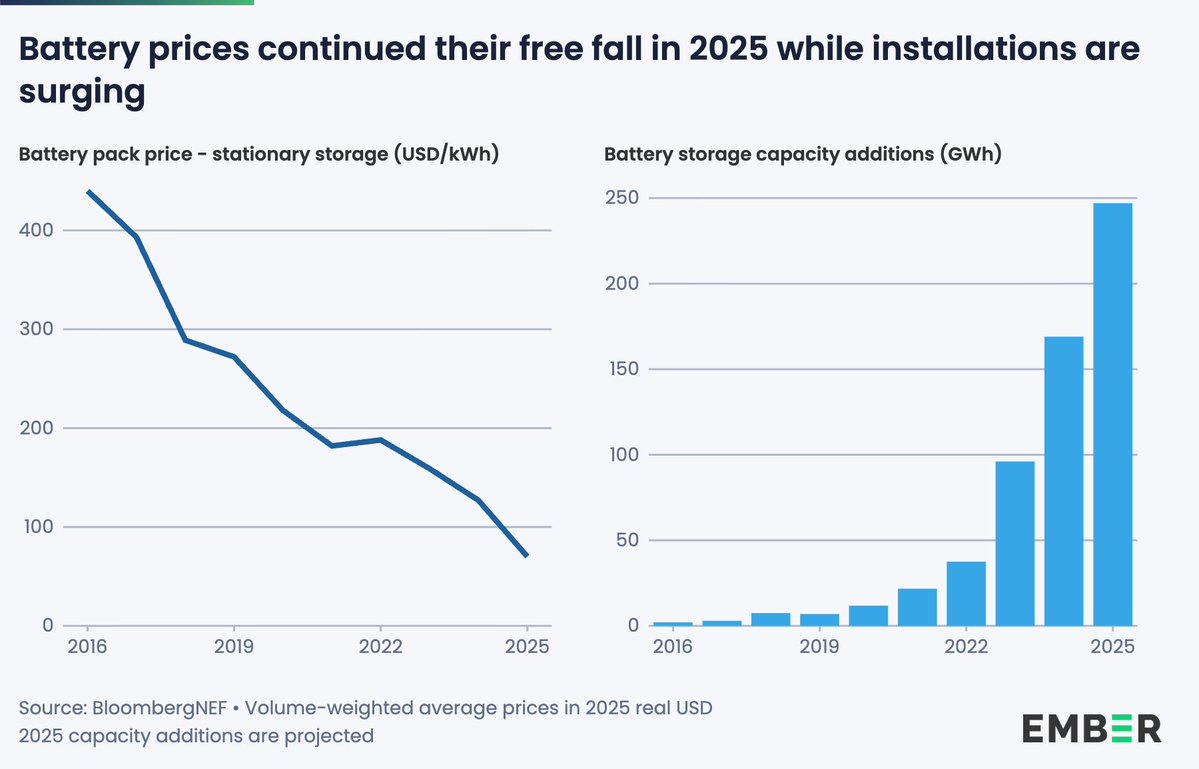

Battery storage will change the global energy system forever.

Battery pack price: down 45% in 2025, first time below $100/kWh

Battery storage deployment: ~250 GWh, up 46% year-on-year

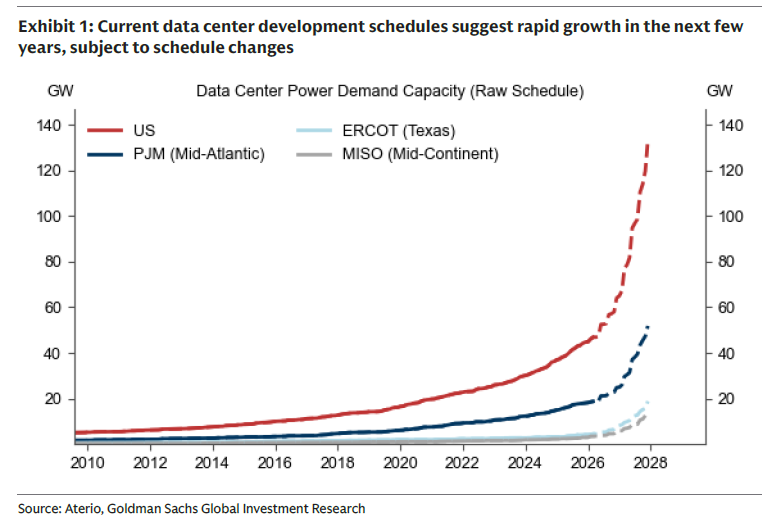

US GRID UNDER PRESSURE: AI DEMAND FORCES REDESIGN

The US power grid overseen by PJM Interconnection (serving 67M people across 13 states) is no longer fit for purpose amid surging electricity demand from data centers, according to CEO David Mills.

In a letter to stakeholders, Mills warned the system cannot both secure enough power and protect households from rising costs under its current design. “The current situation is not tenable,” he wrote, pointing to deeper structural flaws reflected in rising prices, tight reserve margins, and weak investment signals.

The grid is facing multiple strains: potential electricity shortages as early as next year, and uncertainty linked to major utilities such as American Electric Power. Meanwhile, electricity bills have climbed sharply across the region—up 51% in Maryland and 41% in Illinois over five years.

Mills said the region has “years, not decades” to act, and emphasized the need for credible, stable market rules to restore confidence among utilities, investors, and consumers.

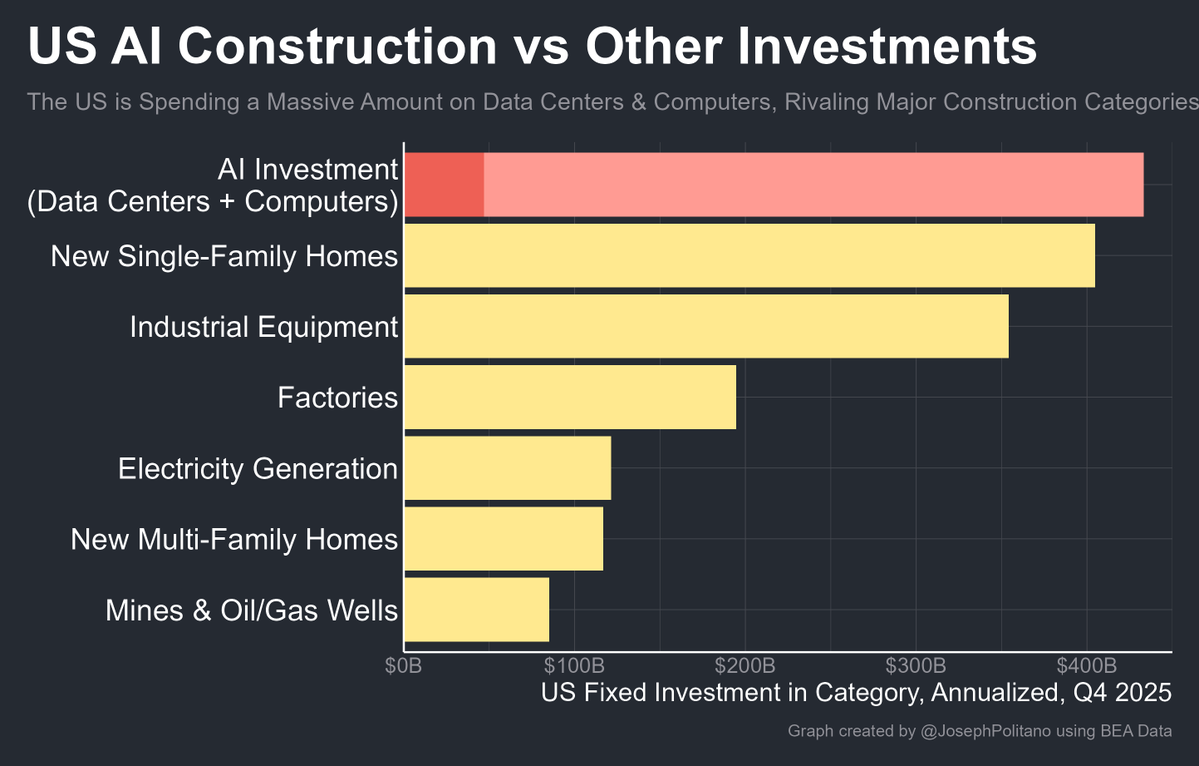

US spending on data centers & computers has grown so much that it's larger than basically all other physical investment categories—more than all single-family housing construction, factories, power plants, industrial equipment, apartments

I'm running out of points of comparison

In just over a decade, Chile went from no utility-scale wind or solar at all to having more electricity from these sources than from all fossil fuels combined:

2000: wind+solar provided 0% of Chile's electricity, fossil fuels 45%

2025: wind+solar 36%, fossil fuels 28%.

Chart from Morgan Stanley, explaining the difference between futures/paper oil market (ICE Brent) and physical oil market (Dated Brent). If Dated Brent stays high, it will feedback into futures (physical disciplines the paper).

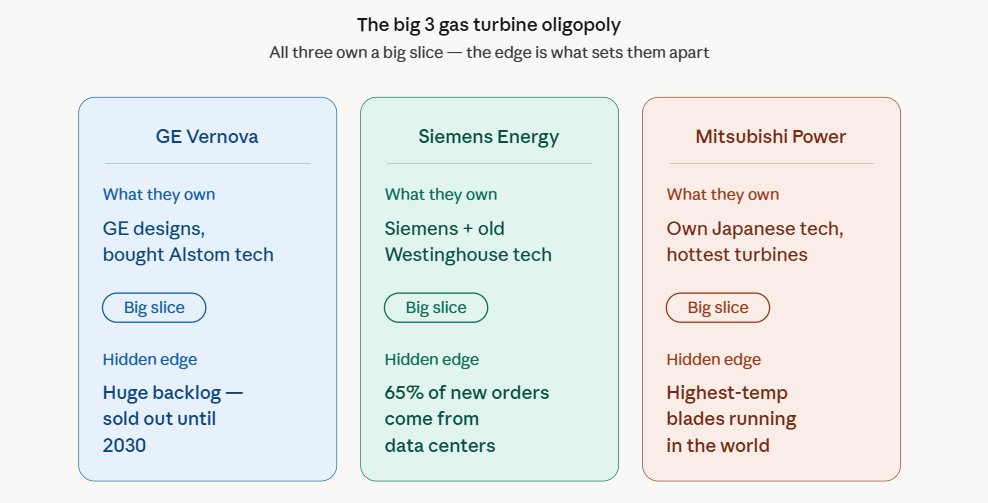

When Yu Read About Gas Turbine, Yu have to know :)

It went from 8 to 3 in just 25 years, In the 1990s there were GE, Westinghouse, Siemens, ABB, Alstom, Mitsubishi, Rolls-Royce, Ansaldo.

Mergers, money problems, and bad deals killed most of them. Example -GE paid €10 billion to buy Alstom in 2014, but had to give some secrets away.

LTSAs are the real money trap - These are Long Term Service Agreements, company that sells you the turbine also signs a contract to fix and maintain it for 20+ years.

If you miss one inspection, you lose the warranty. This locks power plant owners like prisoners, they cannot easily switch to cheaper repair shops. The maker gets steady high-profit money forever.

Making blades is like rocket science - The hot blades inside spin at 3,600 times per minute in 1,650°C heat (hotter than lava).

They use special nickel metal with rare elements and must be cast as single crystals (no weak joins). Only two secret factories in the world (in USA) can do this well. New companies cannot copy it easily.

Efficiency = huge hidden cash - Each 1% better efficiency in a 400 MW power plant saves $12 million over 25 years.

Modern ones reach 64% efficiency, old ones only 33%. That is why these three companies stay on top.

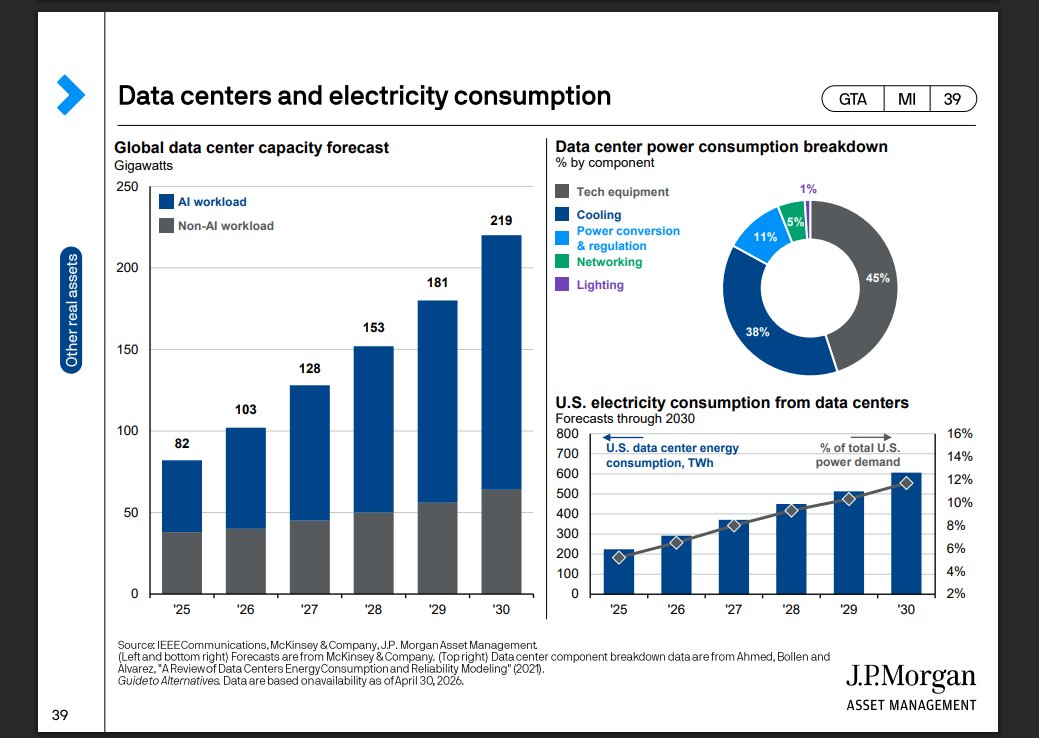

AI boom is making it worse, Data centers will almost double electricity use by 2030. Gas turbines are the fastest way to add power, but factories are already fully booked for 5–7 years.

Some utilities are even keeping old dirty coal plants longer because they cannot get new turbines fast enough.

Data centres are so stuck they are buying old aircraft jet engines to use as temporary power plants.

Landon Tessmer, Vice President of Commercial Operations at ProEnergy, told IEEE Spectrum that they have sold 21 gas turbines for two data-center projects, amounting to more than 1 gigawatt (GW)

Refurbished jet engines, not new ones. That's how bad the shortage is.

The special metal they use has rhenium in it. Despite accounting for only 3–6 wt.%, the cost of Re is approximately ten times as expensive as the price of the remaining 97 wt.% of the alloying elements because of its low crustal abundance at only 0.7–1.0 parts per billion MDPI.

Rhenium is rarer than gold. You need this rare metal + a single-crystal growing process that all use the idea of directional solidification in a vacuum furnace.

Only a handful of factories in the world can do it well. New companies cannot copy in 5 years or 10, maybe not even 20.

Three companies make 75% of the world’s large gas turbines. I wrote the full story of how eight became three, what happened to the engineers, and why LTSAs lock in operators for decades.

I could never quite get a chat-bot to give me a good, institutional-grade earnings preview. It required the confluence of too many separate prompts.

I was working on this today for $DHR, and I personally was quite impressed with the result (this is grading my own homework, for sure). All I have to do is enter a ticker, press button, and this is the output I get.

The key unlock is an orchestrated skills pipeline in a multi-model agentic workspace with tool calling capabilities.

This is built solely on publicly available information - no primary research, expert network calls, data or management touchpoints. One can imagine how much better this gets piping in the right Research Context.

Full preview on comments - let me know what you think.