Over the course of building Solv for the past 5+ years, i’ve seen plenty of narratives come and go. Most of the projects 5 years ago doesn’t even resemble the sectors we have today. Solv has also evolved since we started building it, but our fundamental approach never changed. We always built it with economic value in mind:

-Solv addresses a problem on how Bitcoin can become more productive.

-Solv generates significant contributions to the economic flywheels of the ecosystem it lives in.

-Solv supports its self-sustainability through a positive cash-flow.

Markets will always have cycles, but i’m confident that the systems we built and workflows we’ve implemented will endure.

We’ll continue to expand the largest onchain BTC reserve, work to be done

Security is not a feature. It is the foundation.

As SolvBTC scales across chains and becomes core infrastructure for BTCFi, we will always choose the most battle-tested standards for users, institutions, and partners.

That’s why SolvBTC and xSolvBTC are now powered by Chainlink CCIP.

Trust is built in decisions like this.

🚨 NEW: Solv Protocol migrates from LayerZero to Chainlink's CCIP as its official cross-chain infrastructure for $700M+ in tokenized BTC following a security review.

solv protocol ate a $2.7m exploit in march, reimbursed every user from treasury within 48 hours, passed 5 security audits, and shipped institutional staking tools by april. mango socialized $114m onto users. drift is still negotiating $285m in recovery. balancer shut down entirely. solv trades at $6.6m FDV. the bitcoin yield infrastructure layer is going to be worth hundreds of billions and the protocol that just passed its stress test in public costs less than a miami penthouse.

I see the SEC’s new crypto taxonomy as more than a sentiment boost. I think it materially improves the operating backdrop for what Solv is building.

What stands out to me is that the SEC is starting to distinguish more clearly between speculation, securities activity, and infrastructure. That distinction matters because, for a long time, much of crypto was forced to operate under broad legal ambiguity. In practice, that ambiguity became a tax on innovation, making integrations harder, raising diligence costs and causing institutions hesitant to engage.

From my perspective, the most important part for Solv is the SEC’s treatment of wrapping. I think this goes directly to the heart of our thesis. If a wrapped representation of a non-security crypto asset is simply preserving ownership, redemption, and utility, then making Bitcoin usable onchain should not be viewed the same way as issuing a new security. That is a very important conceptual and fundamental shift.

I have always believed that one of the biggest inefficiencies in crypto is that Bitcoin, the largest and most important digital asset, remains underutilized relative to its economic potential. At Solv, the problem we are solving is not how to reinvent Bitcoin, but how to make it functional as collateral, liquidity, and productive capital across DeFi, CeFi, and institutional onchain finance. To me, that is not financial engineering for its own sake. It is about unlocking the full potential from an asset that has historically been held passively.

Regulation clarity most certainly leads to cleaner business models that are easier to understand and scale. For Solv, this means the wrapper layer becomes much simpler to explain, the collateral layer is easier to justify, and institutional conversations become significantly more straightforward. We can now focus our energy on the essential topics: backing, redemption, transparency, risk controls, and product integrity.

Perhaps a second-order effect that is just as important as the legal interpretation itself is how regulatory clarity improves institutional readability. It lowers the friction for integrations and makes counterparties more comfortable evaluating wrapped BTC as usable, production-ready infrastructure rather than something structurally suspect. When that happens, every investment we have made in proof of reserves, cross-chain transport, and product design becomes significantly more valuable.

Of course, I do not think this means everything is suddenly risk-free. The SEC is still clearly saying that context matters. I think that is an important reminder. The market will reward protocols that are disciplined about structure, transparency, and utility. In my view, that is actually constructive, because it favors teams building real infrastructure instead of relying on just narratives.

So when I look at this release, I see it as validation of a core principle I have believed for a long time: making Bitcoin usable is not the same thing as turning it into a security. And if that principle is increasingly recognized, then I believe the path becomes much clearer for Solv to help build the next phase of Bitcoin Finance.

ICYMI!

SolvBTC is positioned as a leading, compliant infrastructure for Bitcoin-native finance, especially following the SEC's 2026 regulatory clarification.

The new regulatory taxonomy recognizes Bitcoin as a digital commodity and clarifies that redeemable wrapped tokens, like SolvBTC are generally not securities.

This structural shift validates Solv's mission to transform idle Bitcoin into a productive financial building block.

Incident Update: BRO Vault

A limited exploit occurred in one of our BRO vaults, affecting a very small number of users (<10).

The impacted amount is 38.0474 SolvBTC.

All other vaults and user funds remain secure and unaffected. We're actively investigating with top security partners and have taken steps to prevent any recurrences.

We are covering related losses for affected users.

Your funds are safe—thank you for your trust as we strengthen the protocol.

Special thanks to @HypernativeLabs, @SlowMist_Team, and @CertiK for promptly alerting us—enabling rapid response.

To the exploiter: We offer a 10% white hat bounty if you return the funds promptly. DM or reach out via on-chain message to 0x08259F9D1De695329b5a0FDF4703F72c7C2326A9.

We keep calling this borrowing. But a 365-day BTC-backed loan is closer to private banking behavior: keep the asset, finance around it, and treat collateral like a core position.

@xapobankapp 2025 Digital Wealth Report shows:

- Bitcoin-backed borrowing shifting from short-term liquidity to long-term planning

- 52% of BTC-backed loans issued at a 365-day term.

- people like to retain BTC exposure, unlock liquidity, and treat BTC as productive collateral.

That’s why I think BTCFi is inevitable. The market is moving from BTC as trade → BTC as collateral primitive. Once that shift happens, the moat is risk transparency + execution quality, not APY.

https://t.co/aoZhJ5XRop

Saw the Business Times piece quoting my take on the BTC plunge—thanks for the feature! (link: https://t.co/d3exLtEiIN)

Honestly, it's a tough moment, but this is exactly the kind of macro induced shakeout I've seen before. BTC dropped hard from $126k peaks to test below $60k this week, wiping out a ton of paper gains.

But zoom out: this isn't a failure of Bitcoin, it's a feature of where it is in its lifecycle.

Right now, everything risk-sensitive is getting hit: Fed signaling higher-for-longer rates, geopolitical nerves driving flight to "safe" havens, equities and tech bleeding. When liquidity tightens like this, leverage gets unwound fast, that's the cascade we're feeling.

Spot demand cools, ETF outflows pick up (rational in this fear phase), and yes, big holders like Strategy are staring at massive unrealized losses. But are they dumping? No. Tesla, Block, others holding steady. Institutions aren't bailing, they're weathering it.

Bitcoin itself? Network is rock-solid. This dip is testing resolve, not the thesis.

For me, it's a healthy correction in a young asset (only 17 years old!). We've built Solv through multiple winters. The platforms that come out stronger are the ones stress-tested right now~ decentralized, transparent, with real adoption.

Plunge feels brutal today, but liquidity cycles back. Macro will stabilize (it always does), and when it does, capital flows to what has genuine edge: fixed supply, institutional treasuries, growing utility.

Not calling the bottom (no one can), but I'm not panicking. This is the maturation phase...shifting from hype to real store-of-value status.

Cycles come and go. Bitcoin endures. Stay steady, friends. 💜

Here's an interesting validation of our BTC productivity thesis.

Our investor @LaserDigital_ is launching a tokenized Bitcoin Yield Fund targeting diversified long exposure.

There are 2 macro forces converging here:

1) Institutions viewing BTC as a portfolio diversifier amid uncertainty

2) Growing demand for yield beyond just hodling

We are originally positioned to fill this gap, to bring institutional-grade BTC yields onchain.

Our edge comes down to infrastructure, transparency, security. Its not sexy, but critical for institutions crossing into DeFi.

This is why I’m increasingly confident that the “BTC-denominated yield stack” is going to consolidate around platforms that can do risk-adjusted yield at scale and secure, not just ship strategies.

We'll become the default infra for productive Bitcoin.

Solv will eat all BTC-denominated yields and will continue to expand the largest onchain BTC treasury.

🚀 Nomura backed @LaserDigital_ launches a tokenised Bitcoin yield fund targeting excess returns on top of BTC performance.

#Bitcoin#CryptoFunds

https://t.co/pxYQHK2T7U

I was wrong, Bitcoin doesn't need to beat gold.

If you have watched CZ's debate with Peter Schiff at #BinanceBlockchainWeek in Dubai and you will see why.

Everyone's asking the wrong question. It's not which one wins? It's what happens when the programmability of Bitcoin meets the stability narrative of gold?

After an hour of watching them spar, the conclusion results in the same scarcity thesis, same decentralization story, same inflation hedge, just different market cycles.

- Gold = crisis hedge, risk-off flight to safety

- Bitcoin = asymmetric bet, risk-on digital scarcity

But there's one asymmetry: Bitcoin is programmable money.

And programmable money can do something gold never could, generate native yield without counterparty risk or leverage loops.

This is what keeps me up all night, I am also thinking about the next 10, 20 years for Solv.

The answer is RWAs.

The tokenized RWA market did 5X last year. Standard Chartered says $2T by 2028 (excluding stablecoins).

At Solv, we built SolvBTC.RWA Vault specifically for this moment. We are the largest onchain BTC treasury. Partnership with Binance and BNB Chain with one goal: let Bitcoin earn real yields from real-world assets.

Users get actual exposure to tokenized treasuries, credit, commodities, things with cashflows and risk-adjusted returns that institutions actually understand.

My thesis have been the same since 5 years ago when I decided to build Solv. Bitcoin becomes the base collateral layer for the next generation of stable, yield-bearing reserve assets.

Again, we are NOT competing with gold. NOT replacing TradFi, but aims to ABSORB *both into a programmable layer.*

Think about the second-order effects when BTC holders can earn 4-8% yields from investment-grade RWAs without giving up self-custody, you change the game for every fund, treasury on earth.

DAOs holding treasuries. Family offices diversifying. Sovereigns exploring alternatives to USD exposure.

This is the convergence trade the market isn't pricing in yet.

We're NOT building Bitcoin or RWAs at Solv. We're building Bitcoin PLUS RWAs, and the infrastructure to make that work at institutional scale without compromising on decentralization or security.

The debate in Dubai made it obvious.

And the rails we're building right now will define how the next $10T moves onchain.

This is just the beginning.

Read our Manifesto 👇

https://t.co/GcF1vR2hlz

GSOLV!

We're opening the year with an AMA with @BinanceWallet in Binance Square.

Join our CEO and Co-Founder @RyanChow_DeFi along with other guests from top @BNBCHAIN DeFi Protocols @bouncebit and @VenusProtocol

📍https://t.co/NCWsKP4XRl

⏰ 1PM UTC

One of the most important days of 2025 for me - after years of being in development RGB finally went live where I was so happy to be involved with my team mates from @utexocom & @RGBAssociation & legendary @giacomozucco

One of the most exciting trends: stablecoins borrowed against SolvBTC are becoming the foundation for more and more yield scenarios. BTC as collateral is just getting started.

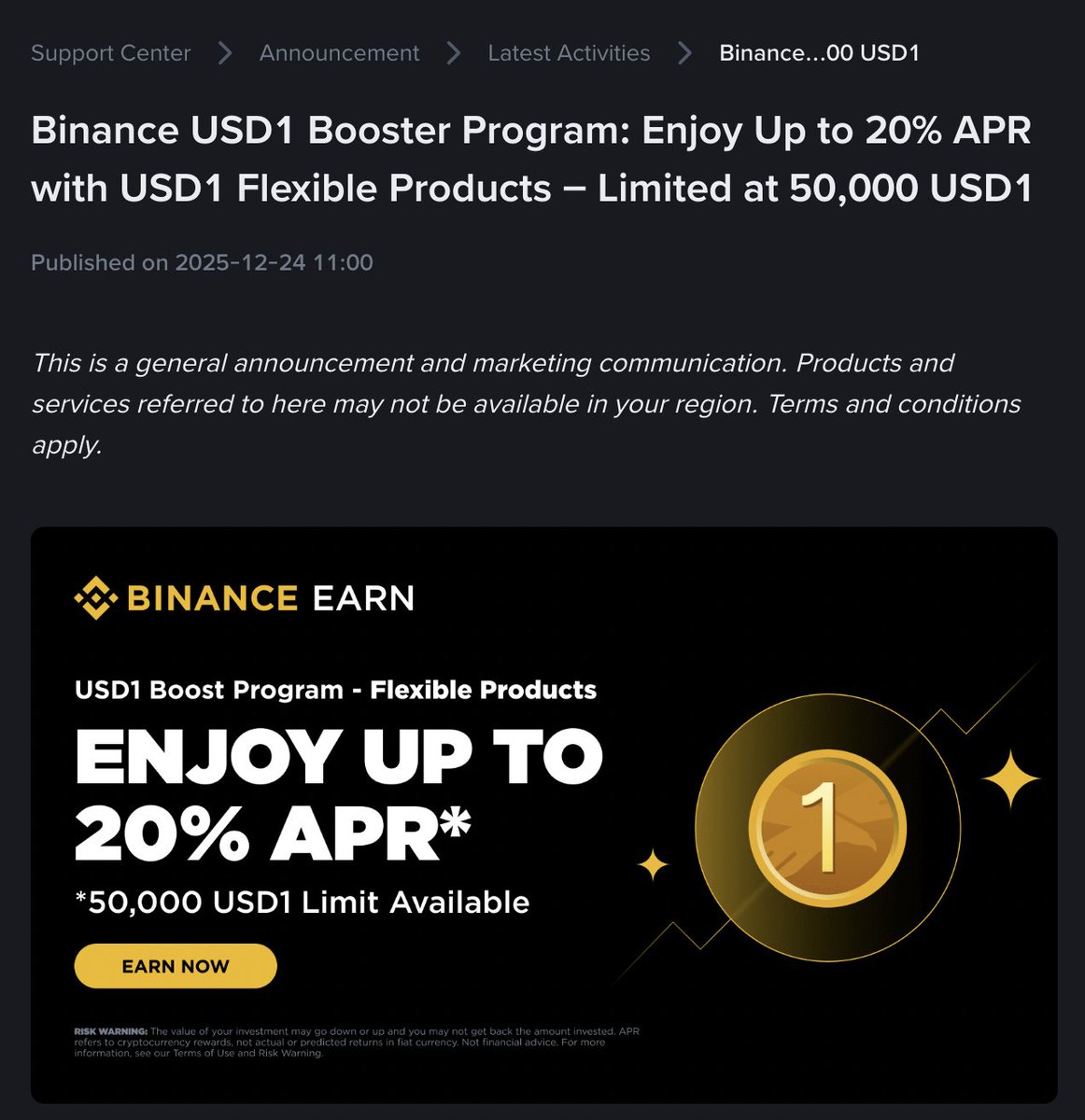

USD1 Fixed 20% APY on Binance Simple Earn. 6.3% for SolvBTC holders!

- Borrow USD1 using SolvBTC on @lista_dao (~5% APR), then deposit it into Binance.

- Borrow USDT (~5%) or USDC (~3.9%) using SolvBTC or xSolvBTC on the @VenusProtocol Core Pool, deposit into Binance, and swap to USD1.

Currently USD1–USDT is trading at ~1.002 (a ~0.2% premium), so the effective APY is ~17.6%.

17.6% − 5% ≈ 12.6% net, or 6.3% in SolvBTC-denominated terms (LTV 50%).

The campaign lasts 30 days.

Merry Christmas! 🎁

My view on RWA:

1. RWA looping

There are very few truly high-quality RWAs that can be looped. Superstate and sUSDe have cyclical yields (bull market product), and ultimately they are tokenized hedge funds, i.e. faux-RWA.

Private credit looping has just blown up (Fasanara mF-ONE). Drawdowns are always a feature, not a bug. Thus there is always a limit to which it can be scaled.

2. Onchain T-bills repo: Not here yet but this can be a very, very large market. Banks & dealers cannot sell US Treasuries due to Basel III constraints, so they can only obtain cash/ liquidity via overnight borrowing. The overnight repo market is limited to HQLA, like US Treasuries, which the US government will strongly support. I believe this is what Aave is betting on. Even a slice of this market is still on the order of $billions, per day. Aave Horizon has already listed all tokenized T-bills out there, e.g. VanEck VBILL, Circle USYC, Centrifuge JTRSY.

We have been exploring RWA yields for BTC holders for quite some time. Stay tuned.

BNB Chain Lending Landscape 🔶

The recent @jup_lend and @kamino fight is interesting.

Lending is the few onchain use cases with proven PMF. Borrow demand is almost the first metric for how “real” a chain’s users are.

The pattern repeats itself:

- Ethereum: @aave & @Morpho

- BNB: @VenusProtocol & @lista_dao

- Solana: Kamino & Juplend

The competitive evolution is awfully similar: a long term dominator, and a challenger rapidly gaining market share:

🟦 Morpho (ETH): grew to 10% of Aave

🟨 Listadao (BNB): grew to 50% of Venus in 9 months

🟪 Juplend (SOL): grew to 40% of Kamino in 4 months

How do challengers grow so fast? I can’t speak for eth or @solana, but solv was building alongside with Listadao lending since their day 1.

🔹 Borrow Side

> Strong base collateral with active users: $SolvBTC for Listadao / $cbBTC for Morpho

> A good yield bearing stablecoin: @ethena for Listadao / @maplefinance SyrupUSDC for Morpho

> Institutional grade RWAs: @Securitize@BlackRock BUIDL, @vaneck_us VBILL, @FTI_Global Benji, @circle USYC [rails via @binance]

🔹 Supply Side

> A good stablecoin partner: @worldlibertyfi $USD1 for Listadao / $USDC for Morpho

> Strong ability to source native asset supply: BNB, ETH, SOL

SolvBTC users are currently split on @BNBCHAIN:

💛 $270M on Listadao

💙 $200M on Venus core pool

Interesting thing is — Listadao didn’t vampire attack our users from Venus (not all at least), instead:

- It attracted @SolvProtocol users from other ecos onto BNB chain

- It also creates net new user for solv as they offer competitive rates

I see it as win, win, win.

I’m excited to see:

- Listadao launching Smart Lending

- Venus teaming up with @0xfluid for Venus X

- Aave already deployed on BNB with lots of idle assets — curious what @Marczeller@StaniKulechov will build with @binance

A strong challenger → healthier competition → better rates → faster feature rollouts.

Done right, the whole ecosystem grows and attracts users from outside 🔥