When Bitcoin hit an ATH in early December 2026, every single expert were predicting a huge run in Q4 & Q1.

Calls for $180k, $250k and even $444k were common. I bought into the hype based on analysis of previous cycles. I think we all did.

The experts were looking at charts and previous cycles and predicting that it's price would be much higher.

Nobody predicted we'd have a 50% correction over the coming 9 months.

Fast forward to today and we're in the opposite zone.

Same over-zealous calls, but in the opposite direction.

Bears with squiggly charts pointing to previous 4 year cycles to justify predictions of drops to $40k, $30k or even $10k! Yes, I'm looking at you @mikemcglone11 👀

The calls for significant lows are as over-zealous as the bull predictions in October 2025.

Both are likely to be proven spectacularly wrong.

Bitcoin proved that it had broken away from its typical cycle action when it didn't move past the linear price levels on the power law chart for the first cycle ever.

It's acting differently, yet the experts are still fighting to show that its trajectory is the same as what it's done in the past.

Could it drop lower? Of course.

But lets stop pretending it's because it's following the same pattern as it did last cycle because that pattern is dead.

It wasn't the same on the way up. There's every chance it wont be same as everyone predicts on the way down.

Bitcoin will do what it wants in the short term, but in the medium to long term, the only direction the chart will point to is up and to the right.

I'm doubling down on accumulation at these levels.

"We're the largest holder of Bitcoin in the world. We're the largest purchaser of Bitcoin in the world. And we'll continue to be". Watch my conversation with @CNBC@PowerLunch below.

00:00 — "We're net purchasers of Bitcoin." The 32 BTC sale helped inoculate the market, test our processes, and capture tax losses over time

1:47 — We balance the needs of our constituents: $MSTR and $STRC shareholders, $BTC hodlers, and debt holders

3:07 — Four-year cycles, macro volatility, geopolitical conflict, inflation uncertainty, Fed policy, Clarity

4:15 — Bitcoin is a hedge against inflation and big government

5:32 — Capital that rotates from $BTC to AI will come back to $BTC

6:42 — With clearer rules, every major bank is going to flood into $BTC and crypto

7:27 — Expanding financial-system access is good for Bitcoin

Bear market bottoms are a process, not an event.

First, price-sensitive investors capitulate. Then comes the harder phase: months of sideways action that slowly wear down the conviction of those who remain.

In our latest newsletter piece, @_Checkmatey_ examines the evidence suggesting Bitcoin may be experiencing a time-pain capitulation event, and what investor behaviour looks like during this phase of the cycle → https://t.co/DakgPAdzpg

Chart explainer:

The 200WMA Quantile measures where Bitcoin is trading relative to its 200-week moving average. Current readings sit in the bottom ~10% of all historical observations, a region only visited during the deepest stages of prior bear markets.

My beliefs: Retweets are notifications, not endorsements. Constructive dialogue leads to better outcomes. Bitcoin is hope and economic empowerment for everyone. Every good-faith effort to strengthen the network should be welcomed.

Want to understand Bitcoin?

Money used to require trust in kings, priests, central bankers.

Bitcoin replaces trust with verification via energy.

Bitcoin exists because thermodynamics demands it. Each Bitcoin record (block) burns ~$280,000 in electricity.

Wasteful? No, it's an energy wall protecting your wealth and time that you can’t print or legislate away.

Bitcoin is built on energy.

Five thousand years of monetary history overturned.

And while I have your attention, I'd love to hear why you've started embracing shitcoin DeFi protocols and retweeting them, when you used to talk about "ethical money" and how Ethereum was not ethical. I guess shitcoin protocols are suddenly ethical, if they help to take down more STRC?

To believe that Bitcoin has no intrinsic value means:

1. Believing that having a decentralized, global payment and settlement network outside the conventional financial system has no value.

2. Believing that having a way to protect your purchasing power from inflation has no value.

3. Believing that being able to store your wealth without counterparty risk has no value.

4. Believing that the ability to send $5 or $50 million anywhere, anytime, with minimal fees has no value.

Yet, people say bitcoin has no utility or value.

Pick up an investment book & learn to practice some patience. I started investing in $IREN since $4.8 & held through every major downturn since. This is nothing….

A 6-7 month period of stagnant performance won’t change my investment outlook, especially not when considering $IREN was trading at ~$10 this time last year.

It’s also not like $IREN isn’t performing fundamentally. Their secured power pipeline grew by nearly 3 GW since the start of the year & their $NVDA cloud contract, albeit small, will pull as much profits as the $MSFT one. The way I see it, $IREN just secured another “Microsoft contract” in a much more capital efficient manner (same profits for much less upfront capex).

You should probably just move on mate. Investing isn’t for everyone. You gotta practice patience if you aim beat the index over time.

Not long ago I sold my entire $NBIS position to double down on $IREN.

Was that a good idea?

Looking at price action alone, no.

Do I regret it? Yes.

Was it a mistake? No.

$NBIS is actually one of my favorite companies in the world right now and I think they have a very bright future. There are execution obstacles, but I would not be surprised to see it 3-5x from here over the next couple of years.

I just had to choose. And at this point in time, $IREN gives me the most conviction.

To me, it has the most asymmetry, the most defensible moat, and most importantly, owns one of the scarcest full-stack assets in the market today.

Power. Land. Time to compute. Speed. Execution. Global footprint and $NVDA validation in the purest sense.

That is the stack I want maximum exposure to.

Sometimes good investing is not choosing between good and bad.

It is choosing between great and greater.

I may be wrong on the timing. I may even be wrong on the choice. But I am very clear on the reason.

“Don’t put all your eggs in one basket”

$IREN makes up 74% of my individual stock portfolio.

I’ve held over a year and haven’t touched it. I’ve continued to buy again in the 30s 40s and 50s .

Let’s start thinking about investing differently…

You have 5 friends. Each of these has setup a company. You have the option to invest in all 5.

The catch? 3 of these companies are in niches you have little understanding of.

One is in early stage and presents more risk than the others.

Then there’s the final company… you understand the thesis, the vision and the necessity for its service in the future.

Do you distribute equal amounts to the 5 friends companies? This strategy means your involvement is now split, your ability to keep up to date with updates diminishes.

Or do you decide to endeavour 100% of your efforts towards the company you believe offers the best upside?

I’m heavily invested because I understand the thesis, the direction and the competitive advantage of owned infrastructure and secured capacity in the future.

5.8GW in the pipeline.. this figure will increase over time also.

The sum of $MSTR's actions has resulted in a 9.4% increase in BTC per share QTD.

Anyone who tells you they are "DiLuTiNg" shareholders is just spreading FUD.

X is speculating that MSTR's CEO and CFO selling shares is a red flag.

It's not. Here's exactly what happened.

1/ What people saw:

→ CEO Phong Le sold 93,738 shares on June 5

→ CFO Andrew Kang sold 33,062 shares on June 5

→ Stock already down 24% this month

→ Looks terrible on the surface

2/ What actually happened:

On June 3, 2026 both the CEO and CFO had Performance Stock Units (PSUs) VEST.

The CEO received 190,740 shares.

The CFO received 68,120 shares.

This wasn't a choice. PSUs vest on a schedule set YEARS ago.

3/ Why did they sell immediately after?

Simple. The IRS.

When equity awards vest, the IRS treats it as ordinary income, taxable IMMEDIATELY.

You don't get to wait. You don't get to choose the timing.

You pay the tax or you get penalized.

4/ How was the sale structured?

Both executives sold under a pre-arranged Rule 10b5-1 plan.

The CEO's plan was established on May 7, 2024 over 2 years ago.

The CFO's plan was established on May 2, 2024 also over 2 years ago.

Neither of them chose to sell on June 5, 2026.

The plan executed automatically.

5/ This happens at EVERY public company.

Apple executives do it.

Google executives do it.

Meta executives do it.

Nvidia executives do it.

Every time RSUs or PSUs vest executives sell a portion to cover taxes.

It appears in SEC filings. It always looks scary. It never means what people think.

6/ The most important detail everyone missed:

Why did the PSUs vest at a 200% payout factor?

Because Strategy's total stockholder return from June 2023 to May 2026 EXCEEDED the 75th percentile of ALL Nasdaq Composite companies.

The executives sold shares BECAUSE the company massively outperformed.

7/ One more thing.

On May 22 2 weeks before the forced tax sale CEO Phong Le VOLUNTARILY BOUGHT shares of $MSTR.

That's the discretionary signal.

The sale was mandatory.

The buy was a choice.

8/ The bottom line:

The CEO and CFO didn't sell because they're bearish.

They sold because the IRS doesn't care about your stock price.

Don't let misinformation shake you out of a position.⚡️👊

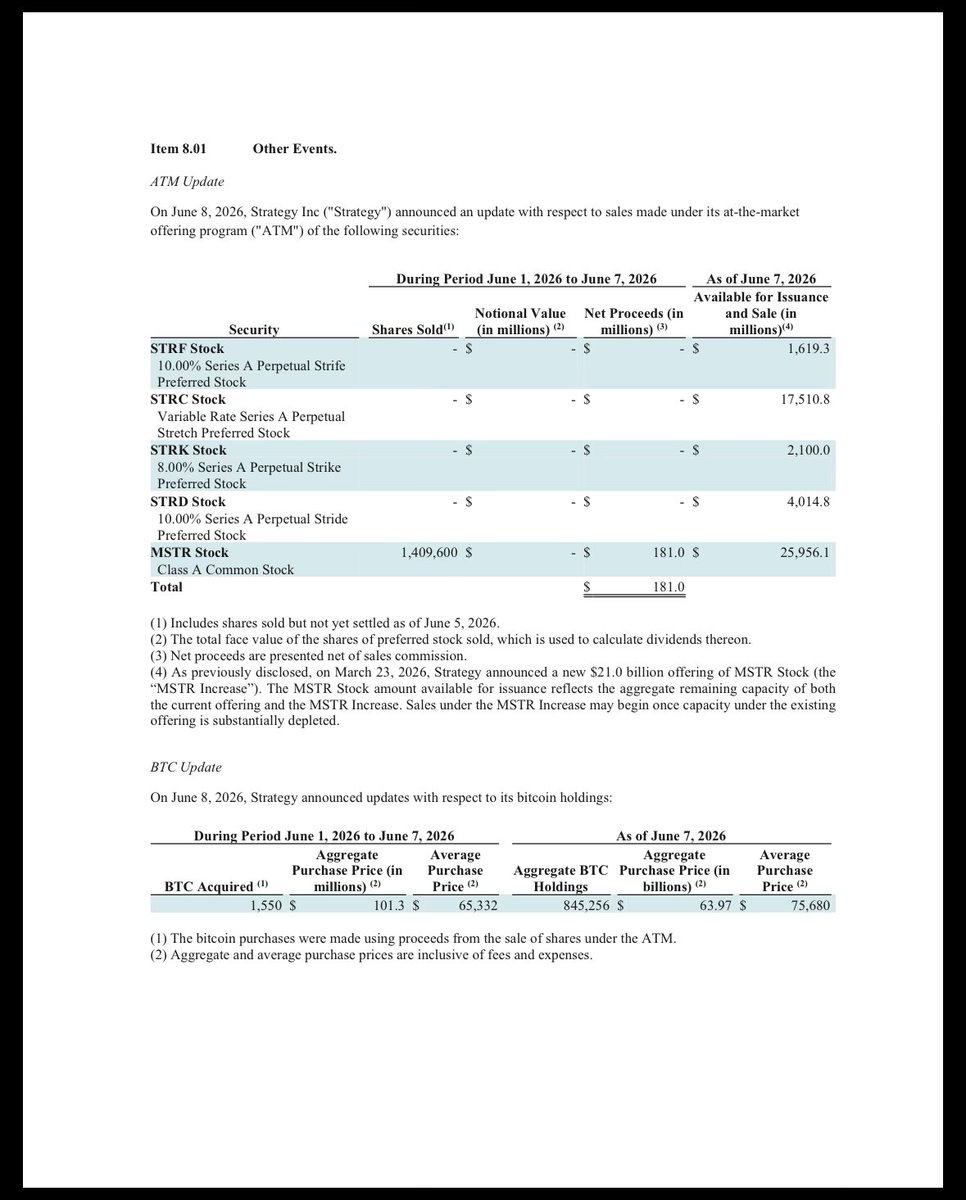

Strategy has acquired 1,550 BTC for $101 million to increase our $BTC Reserve to ₿845,256. We have also increased our USD Reserve by $100 million to $1.0 billion. $MSTR $STRC

https://t.co/94TmyRWVrs

Strategy has acquired 1,550 BTC for $101 million to increase our $BTC Reserve to ₿845,256. We have also increased our USD Reserve by $100 million to $1.0 billion. $MSTR $STRC https://t.co/1Zf1AVsP1H

@dotkrueger@btcjvs I respect you both greatly, but I disagree. Refinancing risk is real (just ask the US government) and non-recourse perpetuals eliminate even the perception of risk. I believe that @saylor and @phongle are on a mission to make the firm as robust (antifragile) as Bitcoin itself.

$IREN: The cloud market's dark horse

I bet most $IREN bulls are starting to get increasingly exhausted by the price action. I certainly am.

However, as long-term investors, we should see day-to-day price action as nothing more than noise.

$IREN is particularly "noisy," which makes it an especially difficult hold. Yet in times like these, it's important to step back and refocus on the company's fundamentals rather than let price action sway one's emotions.

And the way I see it, $IREN's competitive standing is rapidly improving.

I recently came across an interesting research report by Goldman Sachs that highlighted the discrepancy between planned data center capacity and realized capacity.

Out of the ~18 GW planned to be commissioned over the past 6 quarters, only about ~11 GW actually got built.

Not only is the gap between planned and realized capacity rapidly widening, but the rate at which new capacity is coming online has actually declined over the past couple of quarters.

Much of this discrepancy comes down to power continuing to be a major bottleneck.

As grids get more and more constrained with lead times reaching 5+ years, many developers are moving toward behind-the-meter (BTM) generation (on site power generation), circumventing the need for grid connectivity.

Yet that comes with its own set of problems and bottlenecks. The end result is an increasing amount of delays and outright project cancellations.

This industry backdrop plays directly into the hands of $IREN, which now has 5.8 GW of secured grid-connected power across global jurisdictions.

The only reason the industry is switching toward BTM is that it's the only option if you don't want to wait in multi-year queues to secure grid connections. But don't get it twisted, grid-connected power remains the preferred option.

$IREN is in a unique position to capitalize on this structural bottleneck and become one of the few cloud providers that can actually bring on 5+ GW of compute capacity over the coming years.

I'd even go as far as saying that this structural advantage is the primary reason the $NVDA partnership came to be.

While $NVDA undoubtedly remains king of the hill, even they face a real dilemma that could cause cracks in their growth trajectory.

On the supply side, they have to come to terms with the fact that the gap between planned and realized data center capacity is widening, while the trend of new capacity coming online is actually decelerating.

This is the issue I just flagged, and it could act as a potential growth bottleneck for $NVDA, since fewer builds means fewer GPU sales.

Layered on top of this is the demand side. It's perfectly clear that demand for $NVDA's AI hardware remains insatiable. However, when looking closer, it's also apparent that competition is increasing.

Pretty much every hyperscaler is working on their custom chips (TPU, Trainium, Maia, MTIA), and not exclusively for internal use cases anymore, but increasingly to service the compute needs of large AI labs. Anthropic alone has signed deals worth billions for Google TPU and AWS Trainium capacity.

Then you obviously have the likes of AMD and Cerebras directly competing against the AI giant, trying to claim market share.

Taken in aggregate, these two issues could gradually lead to a growth problem for $NVDA if not addressed.

This is exactly where $IREN comes in.

They've got the largest secured power portfolio of any neo-cloud at 5.8 GW and growing fast, they develop 100% of their data centers themselves, and they're not building competing silicon.

That makes them the most reliable demand outlet $NVDA can partner with at scale.

The Sweetwater partnership, positioning the 2 GW campus as a "flagship DSX deployment," isn't $NVDA doing $IREN a favor. It's $NVDA solving its two biggest problems at once.

I'm sure you know the popular saying that "history never repeats, but often rhymes." I think today's neo-cloud market is somewhat similar to the dot com era search engine war.

Back then, the front-runners leading the race were AltaVista, Excite, and Yahoo, while Google was a latecomer that ultimately came out on top.

Today, the vast majority of investors in this space are declaring either $CRWV or $NBIS the obvious winners in the race to become the next hyperscaler.

However, I believe the real dark horse that the mainstream doesn't give much credit to is $IREN.

I believe they have all the ingredients to leapfrog every competitor in a short amount of time, in large part due to their structural advantages and pursuing the right long-term strategy from the get go.

The asset-light model, which both $CRWV and $NBIS have been leaning into, doesn't work well in capital-intensive industries, at least not over the long run.

It's somewhat of an oxymoron, since it seems intuitive that one way to circumvent some of the CapEx burden is to outsource from colocation providers.

Yet that approach leaves you with less control, less flexibility, and ultimately higher costs in aggregate in the form of operating expenses (the landlord also has to earn $).

I studied the Bitcoin mining industry for years, and the asset-light model was once a popular strategy around the 2021 bull market. While it proved to be a strong growth lever, it ultimately ended up being a disaster for anyone who adopted it.

Companies like $MARA are the perfect example.

$MARA heavily adopted the asset-light model and grew to become the largest $BTC miner, yet ended up as one of the most unprofitable public miners of all, leading to significant value destruction for shareholders over time.

Once it became obvious that asset-light wasn't a sustainable strategy, $MARA tried to pivot away from it by increasing self-deployments. But developing infrastructure in-house is a much harder discipline to master, and you don't simply switch into it overnight.

$IREN ultimately won the mining race last cycle by doing the exact opposite of $MARA from the start.

They developed all of their data center infrastructure in-house, backed by a seemingly unlimited pipeline of secured power, which ended up making them the fastest growing and most profitable miner of all time.

While the cloud sector has significant differences from the mining industry, the primary drawbacks of the asset-light model carry over.

Over time, it will become obvious to Wall Street and the broader market that this strategy sounds great in theory, but in practice leads to a stack of operational issues and severe margin compression.

Out of the two current front-runners, $CRWV and $NBIS, I think Nebius will do better. They've at least started moving toward a more diversified mix of self-owned capacity rather than purely relying on hosted colocation, which is the right direction even if they're still early in that pivot.

That said, as the $MARA example showed, developing in-house gigawatt projects at scale is not something you learn overnight.

It's clear to me that a player like $IREN, which has been building this discipline from day one, has the most realistic pathway toward sustained, profitable growth in this space.

In my view, $IREN is the dark horse that will end up winning the race. Thus overthinking today’s price action wouldn't do me any favors.

Cheers guys, have a great weekend! ✌️