Agent finds very little Industrial gas burn correlation to PMI in Europe. Bottom line, industrial gas usage is not going to save European storage . They've already lost a lot of industry. #TTF

gm!🌊

Just arrived in Monaco for the F1 Grand Prix week.

We are exhibiting four artworks aboard this 240-foot yacht, moored in the harbour during the races.

below:

‘Tides of Time’

2025

Edition of 3

203 x 114 cm

Some notable lines from this weeks conference calls

Fluor 'on deck' to start on LNG Canada Ph2, many operators holding the line on activity (FANG notable exception), and TC seeing gas egress becoming demand pull in the mid west vs supply push.

Fluor: "Prospects in the next few quarters in energy solutions include LNG Canada Phase 2, a gas compression project [in California], a gas fired power plant in the Northwest, and a chemical facility in Canada."

Exxon: "Just with respect to what we've been doing in the Permian, I think you all know, you know, we've had the pedal to the metal here from the very beginning... And so we're going to continue on the pace that we've been at."

Chevron: "it's too early to have a different view on, you know, the fundamental outlook around price and it's too early to see or have a view of whether that is structurally changing. And so when it comes to capital allocation, um, we're comfortable with where we are and we're staying consistent and disciplined."

TransCanada: "In terms of the Midwest, you know,

we are seeing incredible opportunities across that acrossthat corridor, specifically in the power demand sector. We see about 4-plus Bcf per day of incremental gas demand across the Midwest corridor over the next 10 years...A couple of our projects into Wisconsin over the last several years have broughtin more WCSB supply. Some of the producers are interested in that opportunity, but it's really the demand component of that that's looking towards sanctioning projects here in the near term."

Conoco: "And, you know, as we look at it, if there's competitive liquefaction fees from expansions that happen and new projects in Canada, we'd certainly want to take a look at that, just like we'd take a look at offtake from many other locations. I think having some West Coast offtake wouldn't be a bad thing in our portfolio."

Antero: "The power projects that have been publicly announced in our region to date and amount to over 8 Bcf per day of demand. Based on the conversations we have had, which also include non-disclosed projects, we estimate that regional power demand projects exceed 10 Bcf per day in total."

EOG: "Given robust oil prices and softness in natural gas, we have refined our plan for the balance of 2026. We are increasing oil and NGL production while maintaining our $6.5 billion capital budget by reallocating capital from gas to oil-weighted assets... We expect US natural gas demand to grow at a 3% to 5% compound annual growth rate through the end of the decade, and believe the previously forecasted potential for global LNG oversupply has been significantly reduced with the damage to LNG infrastructure abroad."

FANG: "Because of our positioning, our preparation and this price signal, we are bringing incremental barrels to the market immediately. We have made the decision to begin to work down our drilled but uncompleted well (“DUC”) balance to maintain our current production level of over 520,000 Bo/d - up 3% from our original 2026 guidance. Diamondback is capturing the production response now and will subsequently backfill activity to maintain our future operational flexibility.

To execute this plan, we expect to run 5 completion crews consistently for the remainder of the year and to add two or three rigs to preserve a healthy backlog of projects to maintain operational flexibility. This level of incremental activity maintains our current level of capital efficiency and puts Diamondback in a differentiated position.

On top of increasing Cash Flow per share, this revised plan generates more Free Cash Flow per share in 2026 assuming WTI averages over $60 for the rest of the year. This gives us the ability to maintain current activity levels even if oil prices decline. While our “stoplight” analogy for the macro environment served its purpose over the last year, we are going to put it on the sidelines for now as the light has turned green, and Diamondback is well-positioned to respond to the current macro environment."

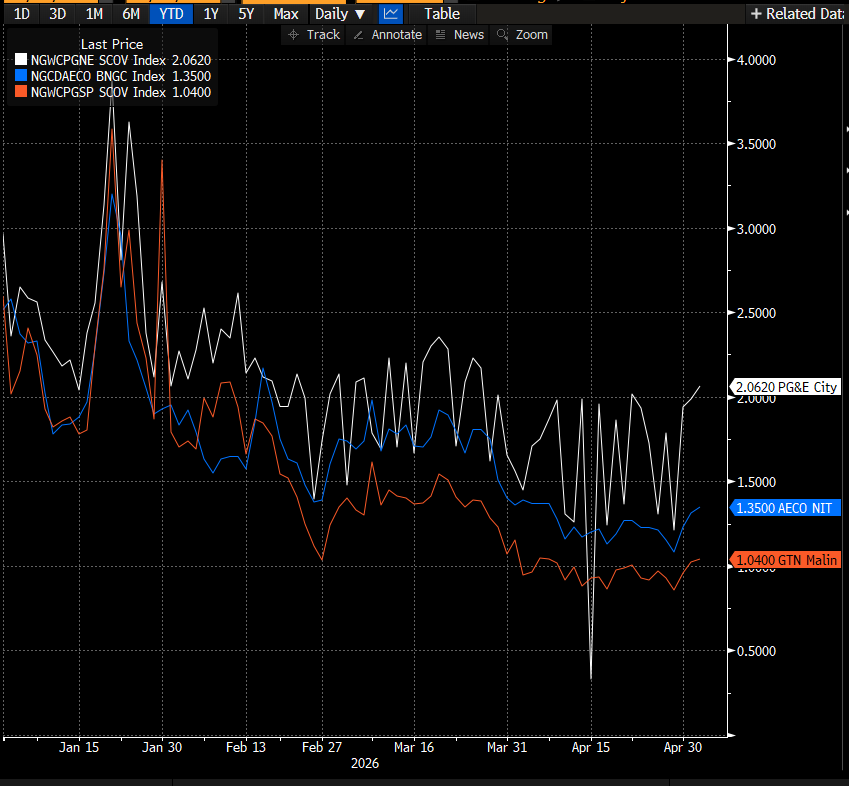

West Gas Bottoming?

Low snowpack starting to factor into PACNW/CA power dynamics (lower May hydro). This is the path to normalization for PG&E, Malin, AECO.

If we get heat, normalization (AECO basis <$1.50, AECO >C$2.00) is possible by July/Aug.

gm!

@alicewexell and I are preparing for an upcoming busy stretch of group exhibitions in Italy, France, Monaco, the UAE, Spain, Istanbul and New York City.

Also preparing for our next solo show, opening this September in NYC!

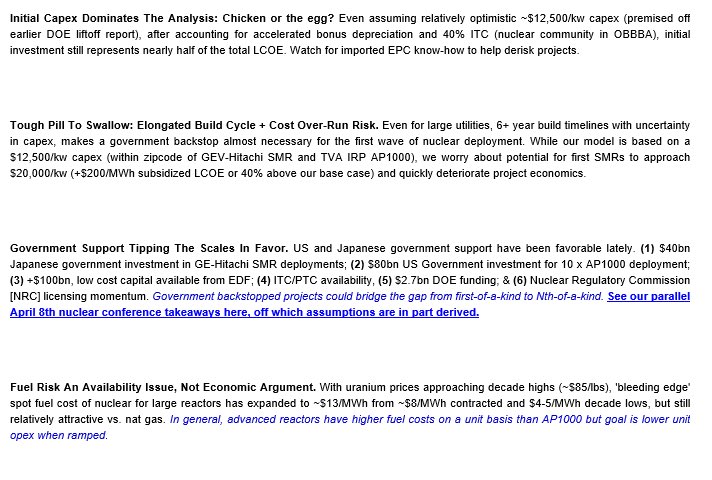

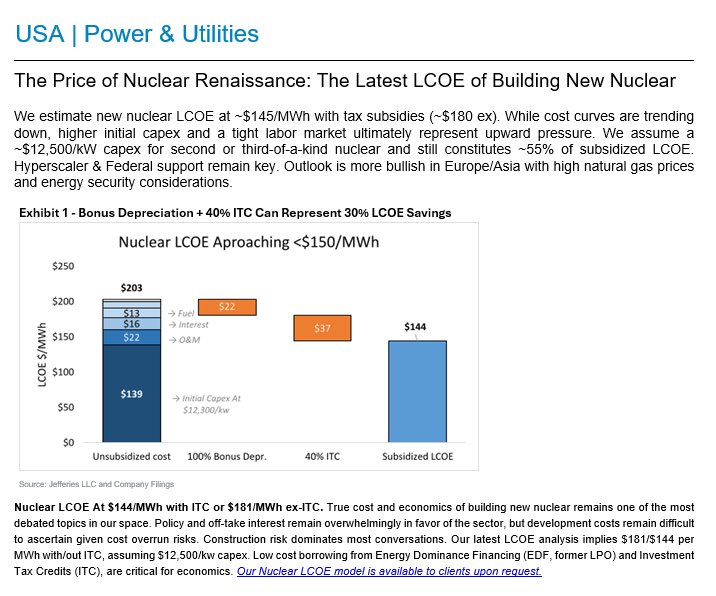

Change my mind: Nuk is a stupid generation source

-$180/mwh lcoe w/o ITC (existing tech)

-$20,000/kw for SMR lol

-6 yr capex profile

-fuel now up to $13/mwh… compare that to a 6.5 HR ccgt… if uranium bulls are right we are not gonna dispatch these @ 99% cf

#POWER#natgas

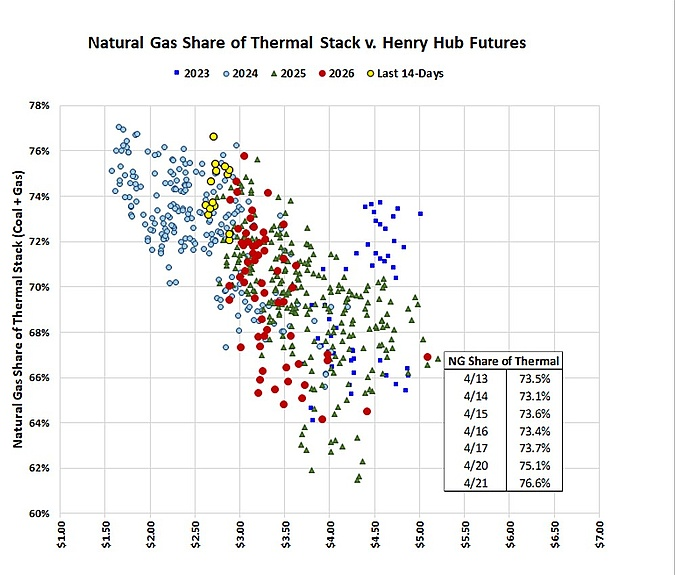

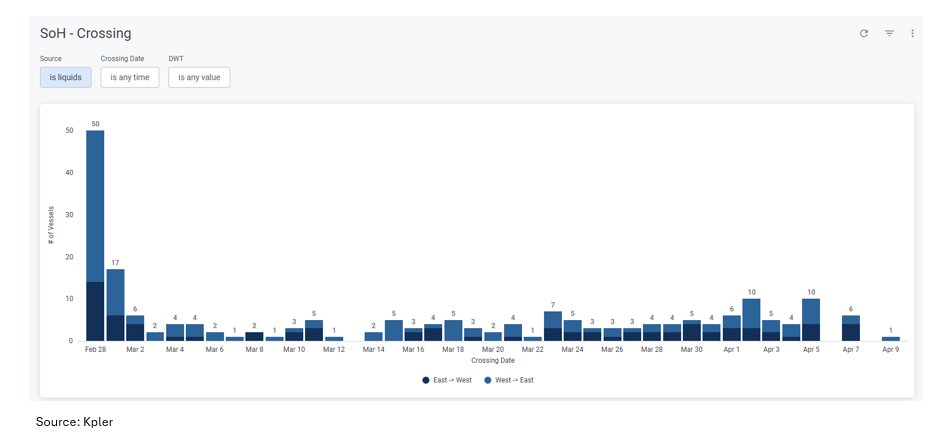

Gas thermal share at 76% in USA; that's an all-time high for this price (I believe). Power burn poised to be the unexpected positive surprise in the US demand stack this year and has room to run if an extended SoH conflict buoy's global coal prices.

Credit Criterion

The Strait of Hormuz is effectively shut and Middle Eastern production is down by 13MM Bbl/d. It will take at least 2 months once fully open to restore production. Over that time the world will lose 780MM Bbls. Historic, unprecedented, cataclysmic...pick your adjective of choice.

The gulf conflict, even if resolved, has impaired supply from the region. Refineries and oil fields will take months to years to repair. Complex LNG facilities are estimated to take 3-5 years to bring fully back online.

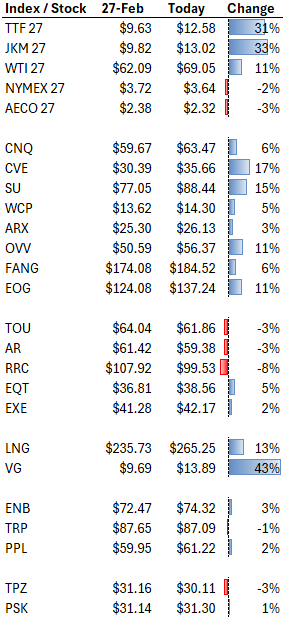

The commodities seem to get this. '27 WTI remains +11% today vs pre war levels. '27 TTF and JKM are +30% vs pre war levels.

The equity market hasn't quite sorted this all out. There are several producers with meaningful liquids and LNG exposure that are flat to even down vs pre war.

In the crisis the market sold tech and bought energy. Within energy investors sold gas to buy oil torque. Today the market is selling energy and buying tech.

As a result the gassier names have been sold twice, and are meaningfully cheaper today then they were pre-war, particularly if they have crude / NGL / LNG exposure.

If you're looking for opportunities in the correction, look first to LNG and liquids exposed gas producers.